Naeblys

On a trailing basis, Eisai (OTCPK:ESALF) looks like not much more than a pretty high multiple Japanese specialty pharma stock with large exposures in oncology and neurology.

Highlights (2023 Value Creation Report)

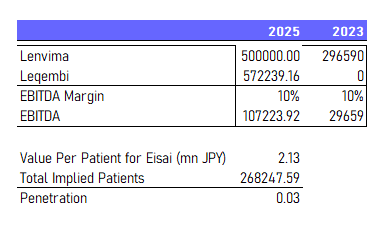

But the multiple is high because they have latent earnings from important releases. One has already released in oncology with considerable growth expected as they leverage the product for new indications, and the other is Leqembi for Alzheimer’s. We think rather than the multiple above 18x EV/EBITDA, 10x would be fair for a company in its treatment areas on forward statistics, doing a broad look at possible peers like Bristol-Myers Squibb (BMY) and Merck (MRK), which are also two companies that Eisai engages in partnerships with. Leqembi would have to be roughly a 570 billion JPY product in 2025 for Eisai to be at fair value today. It’s very doable considering that it only requires 3% penetration of Leqembi in the US alone based on prevalence figures (with China being another large market), and for Lenvima to hit its 500 billion JPY target in 2025.

Briefly on Recent Earnings

The most salient point is that major FDA approvals have come in for Leqembi, so it’s ready to roll in the US, although delayed, and has already launched in Japan but that launch hasn’t featured meaningfully before the close of the quarterly books. They are working to get Lenvima approved for co-indication with Keytruda, getting it into new indications of small-cell lung cancer which is a massive market, and it is working on an antibody drug conjugate with BMY to try to create new markets for its other oncology product Halaven.

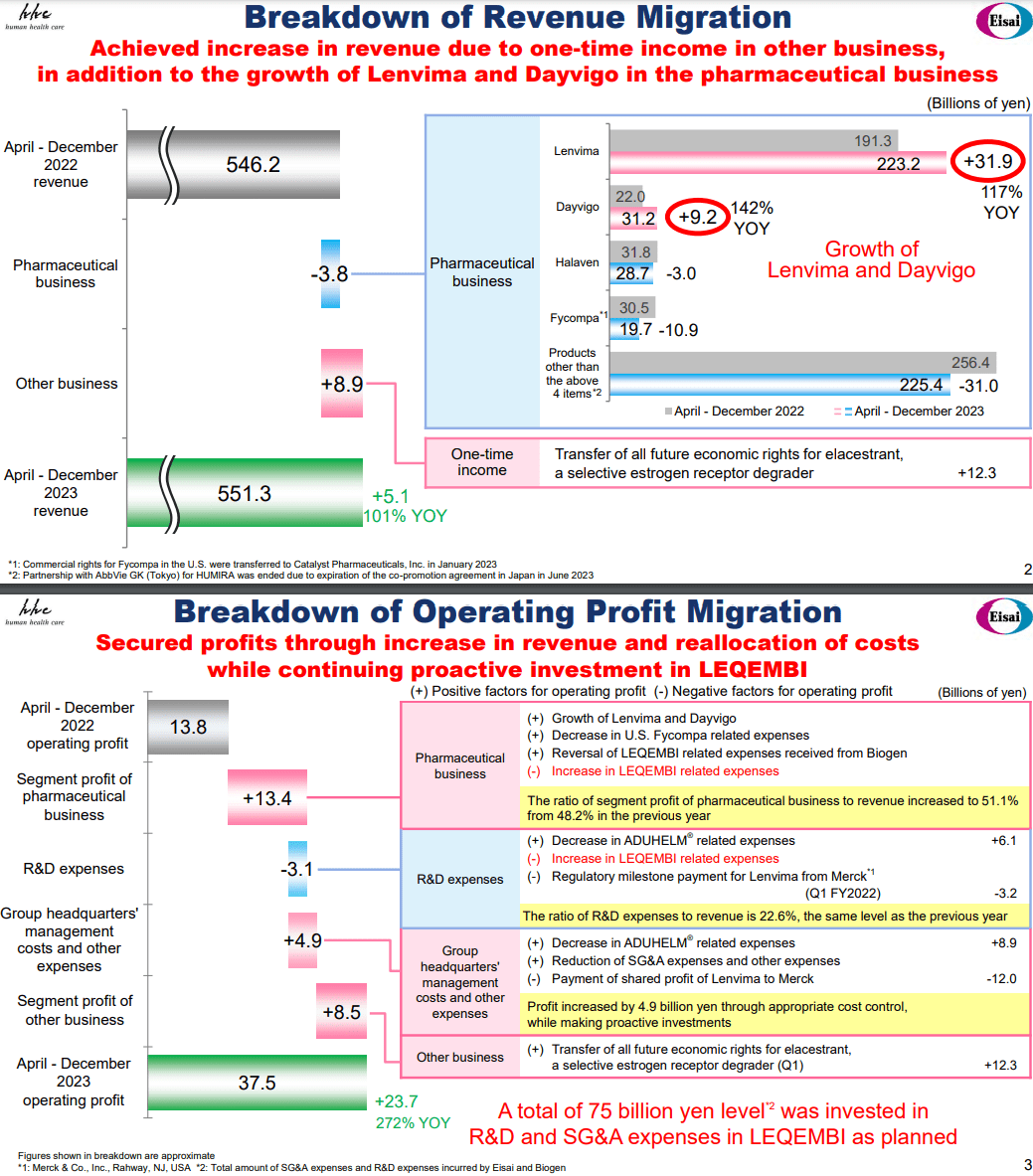

In terms of the financial performance, there were some gives and takes in the pharma revenue picture.

Q3 Cumulative (Q3 Pres)

Looking at cumulative figures, there was some pressure from Fycompa because they sold the US franchise for the drug at the beginning of the year, so that is no longer contributing. Otherwise, the smaller product Dayvigo for insomnia and Lenvima performed well, offsetting general declines in the rest of the portfolio. The revenue picture is run-rate at a slight decline, but basically stable. Including the one-off effects from a transfer of a gynecology drug, there would have been growth.

While revenues stagnated, profits grew. Excluding the gynecology one-offs, profits actually doubled entirely on account of reductions on the cost side. Aggressive work on getting Leqembi into the market is driving up R&D expense, but expense reversals on milestones are more than offsetting those effects. The Fycompa franchise in the US is no longer contributing an expense drag, but of course it’s no longer contributing in revenue either. The Leqembi reversals should be one off benefits. Aduhelm studies have been terminated as we understand it, so those profit benefits should be permanent. They also had expenses related to one offs paid out to their partners on various milestones. The one related to Lenvima should be the last as it pertains to a pretty limited set of regulatory milestones. The profit sharing on Lenvima of course is not a one-off.

Japanese disclosure and guidance tend to be really bad. They are just telling us what they expect for the full year, where we’re currently at Q3 being the latest release. Not much help as we don’t have an idea of what run-rates will look like after all these milestone effects, even just for FY 2024, so we’ll have to make a coarse guess. Aduhelm savings match Leqembi expense increases in R&D. The regulatory milestone in R&D is a one-off. The -3 billion JPY effect should revert to zero which is positive. Net corporate effects should hold where they are. Gynecology one-offs need to be excluded which is a negative effect. The expense reversal of Leqembi was probably quite large, so we think that since that’s a one off benefit, and they are still pushing Leqembi into the various markets, costs should actually grow at run-rate assuming no further revenue growth. Considering there will be some revenue growth at least, likely profitable growth that can offset these effects and more considering the large releases we’re about to get into, we’re just going to use current EBITDA figures annualized but excluding the distorting gynecology sale for our 2025 forecasts, which give two years of growth to justify the overcoming of this quarter’s one-off benefits.

At any rate, just the forecasts of Leqembi and Lenvima dominate the current mix as they are potential blockbusters. The deltas of these other components will matter less and less.

Sanity Check

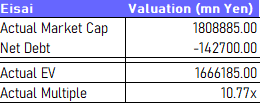

The Eisai EV/EBITDA is above 20x when using annualized EBITDA or trailing figures which are very close, and above 18x EV/EBITDA using forecasts for the finished FY 2023. That’s not a fair multiple, which means we have to assess the implied growth that makes it fair.

The market is aware of the two major revenue levers currently which are Lenvima, and already successful product with almost 300 billion JPY in sales, and Leqembi which is around 50 billion JPY in sales in the US, although it’s not broken out yet since it’s a very new release. Eisai expects that Leqembi, which is for Alzheimer’s, is going to be a trillion dollar product. Lenvima is working on a major foray in combination with Merck’s Keytruda into lung cancer. They expect that to bring Lenvima to 500 billion JPY in FY 2025, which is the year we’re using for our forward statistics and valuation. They are still just identifying possible patients in the US, and China is also a nascent market where Eisai will distribute the product. Important to note is that Leqembi and Lenvima are both co-commercialized products, with Biogen (BIIB) and Merck respectively. Assuming that means that they share 50:50 revenue with Biogen for Leqembi, and taking the 500 billion JPY forecast for Lenvima at face value, we can see what the implied penetration is of Leqembi looking at just the US based on the figures they gave us, which is a $26.5k annual price tag for Leqembi. Assuming a 10% EBITDA margin for the products, Leqembi will need to reach around 270k patients in the US. With demographics fueling growth of AD markets, 2025 prevalence is expected to be around 200 million in the global market. In the US, it’s probably around 8 million by 2025.

Eisai At Fair Value (VTS) Leqembi Implied Patients (VTS)

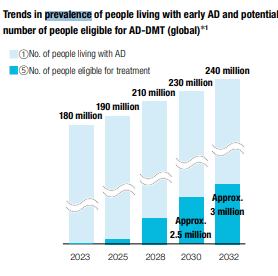

That’s a penetration of just 3% in the US by 2025. Only a proportion of AD patients will be eligible, but they can try to grow the indication list and get a larger proportion over time. A good chunk, maybe a quarter, could be eventually eligible according to their charts. It’s just then a matter of execution.

Eligibility (2023 Value Creation Report)

They are a bit more conservative, and believe it will take till 2028 before Leqembi hits targets. Nonetheless, penetration required is low, and then there’s potentially a massive market in China that we haven’t even taken into account.

Bottom Line

The assumptions aren’t grand in order to get the financial statistics to a level in the growth forecasts where they will dominate the mix and justify the current valuation. They don’t need to dominate the US market to be a fair prospect, and that’s before even considering the cushion of penetration in other markets too, like China. It actually looks reasonably valued, although the market is already looking forward. Leaning on a buy, especially as AD and oncology markets are always on the secular up, and pricing power is fantastic.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")