Chip Somodevilla/Getty Images News

The inflation data this past week certainly shocked markets, with rates moving sharply higher and indexes posting losses for the second week in a row. But more importantly, it led to a repricing of the market’s view on the rate cuts the Fed is likely to deliver in 2024.

It sets up a pivotal Fed meeting that isn’t expected to see a rate change but could change the number of rate cuts the Fed thinks may be coming in 2024 and the longer-run neutral rate. Therefore, investors will focus on the Summary of Economic Projections (SEP), the “dot-plot,” governors and board members of the Fed project, and its expected path for inflation.

Fewer Cuts Coming in 2024

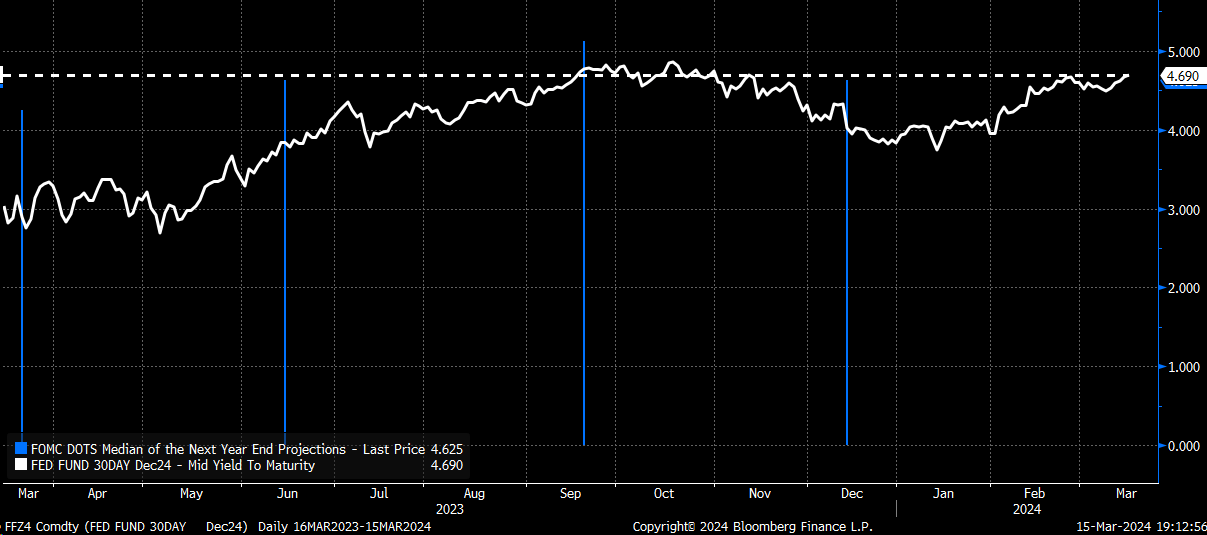

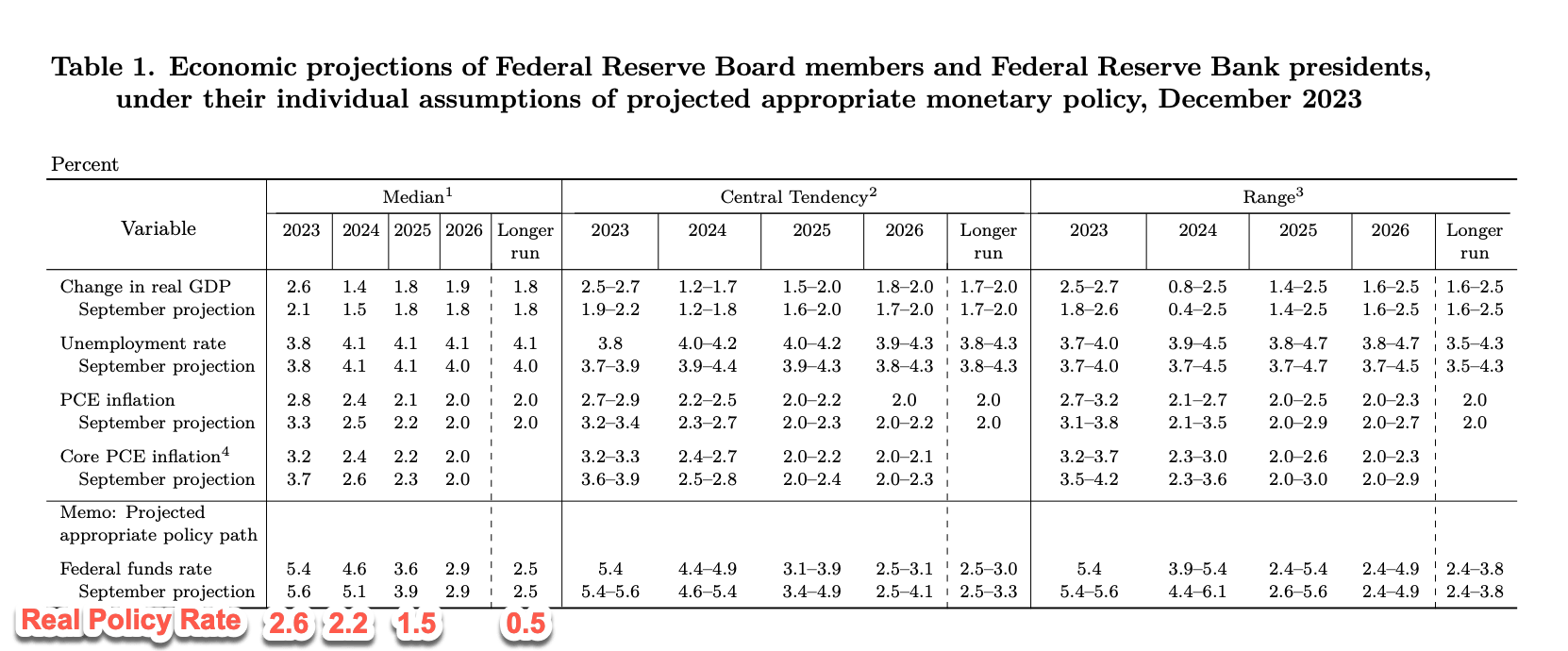

What seems clear is that the market now has doubts about the number of rate cuts the Fed projected at the December FOMC meeting. At that time, the SEP had projected a median rate in 2024 of 4.6%, indicating that the Fed would give the market three rate cuts. However, this week’s hotter-than-expected CPI, PPI, and import price reports have markets pricing fewer than three rate cuts this year.

Fed Fund Futures are now forecasting rates at the end of 2024 at almost 4.7%, up from 4.5% last week. In fact, at one point, Fed Funds futures saw the Fed Funds rate falling to 3.75% in January. That’s all out the window, given back-to-back months of hot inflation data and expectations for a hot inflation reading in March.

Bloomberg

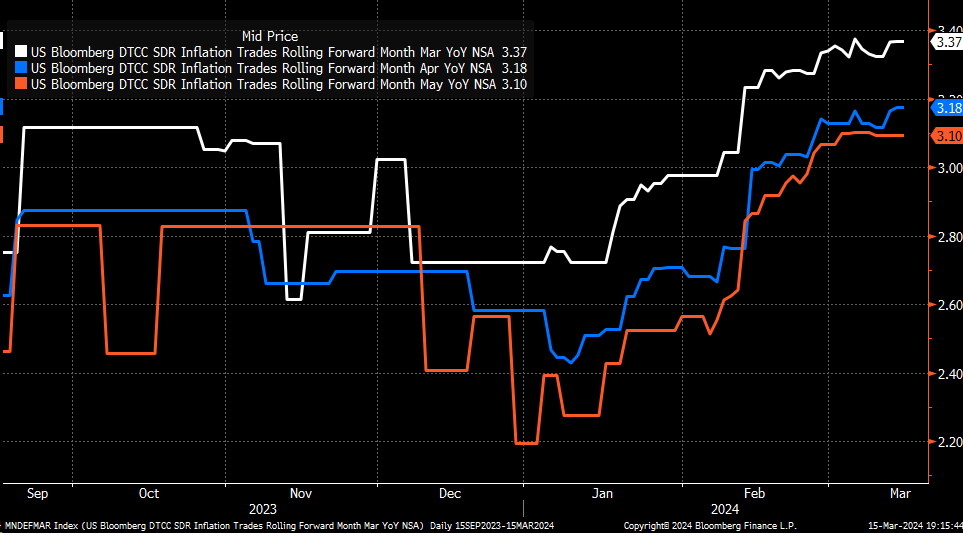

Inflation swaps for March CPI are now 3.37%, and April is 3.18%, higher than before the February CPI release. Meanwhile, May is still expected to be around 3.1%. Expectations for inflation had risen from the dead since the middle of February when markets were surprised by the hot January CPI report.

Bloomberg

The Disinflation Narrative In Serious Trouble

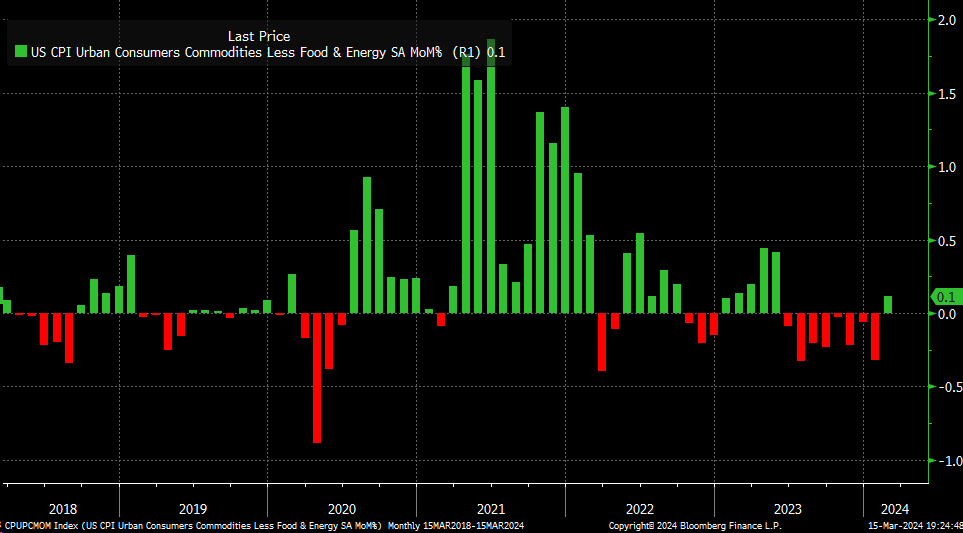

What makes it worse for the Fed is that CPI Consumer commodities, less food and energy, were higher in February by 0.1% m/m when seasonally adjusted for the first time since June, with “goods prices” being a significant source of the disinflation process in the second half of 2023. If good disinflation has stalled or, worse, reversed, it will mean that the overall disinflation process will face significant hurdles in 2024.

Bloomberg

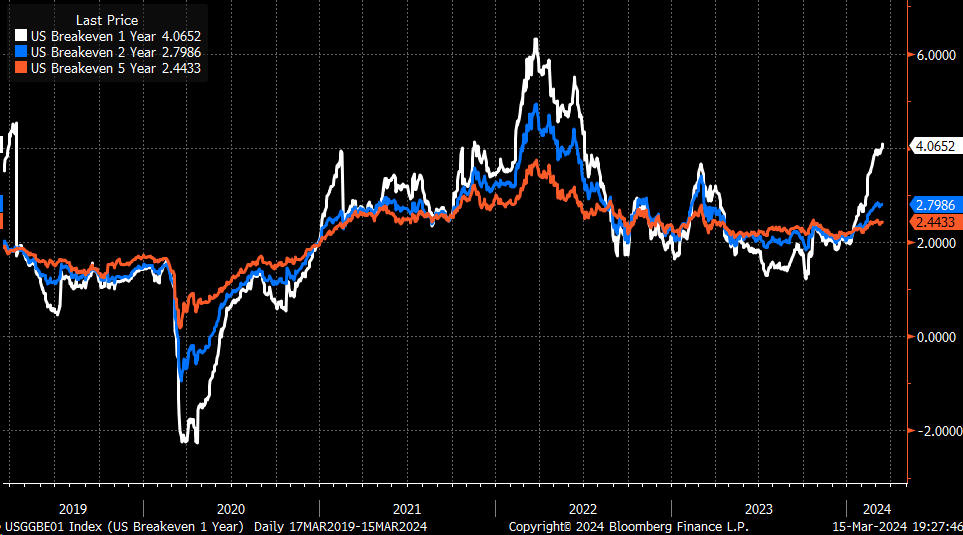

Adding to the problems the disinflation narrative faces from goods prices, gasoline, oil, and copper are steadily climbing. These higher commodity prices, critical inputs for manufacturing, appear to be impacting and pushing inflation expectations for 1-, 2-, and 5-year breakevens higher.

Bloomberg

Policy Is Not Restrictive Enough

Given the number of pieces in motion and the potential risk the disinflation process faces, the Fed might be wise to follow the Fed Fund Futures lead and remove a rate cut or even two from its projections in 2024. This would undo some of the mess the Fed created in December when it signaled three rate cuts in 2024, which led to easing financial conditions.

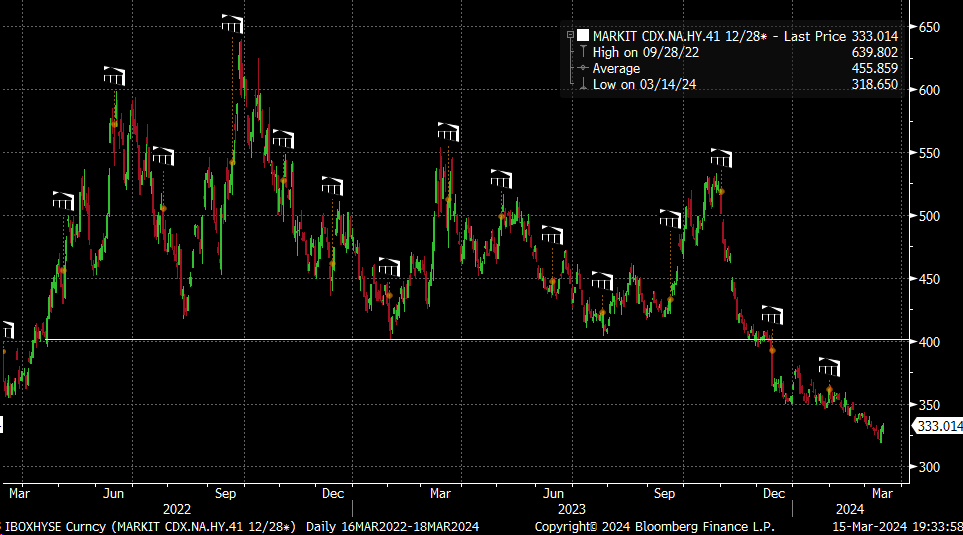

Credit spreads collapsed following the December FOMC meeting, leading the CDX High Yield Index to plunge below 400 for the first time since the spring of 2022. The Fed meeting in November did not help either, with credit spreads collapsing following that meeting. But at least in November, there was an unexpected dovish US Treasury Quarterly Refunding Announcement and a more dovish than expected Bank of Japan policy announcement to share some of the blame.

Bloomberg

Still, financial conditions have eased dramatically in just a few months, so it’s no wonder risk assets have soared. This is why now is the time for the Fed to reign in markets and take back control of the narrative, or the inflation forecast the markets are projecting will likely only go higher because commodities, oil, gasoline, and copper are risk assets themselves. If stocks go higher, it would only make sense that commodities prices also go higher.

The only tool the Fed has to tighten financial conditions up at this point in the game, since they have removed rate hikes from the table for now, is to take rate cuts away. Not only must they take rate cuts, but they also need to raise that longer-run rate from its current 2.5% to, say, 2.75% to 3%, signaling that the economy is running at a higher neutral rate, and it requires higher real rates to keep inflation at target.

They could achieve the same effect by leaving their PCE and core PCE targets unchanged for 2024 but removing a rate cut or two from their forecast. This would signal a higher real rate to ensure that policy remains restrictive enough to bring inflation down. For example, the Fed was signaling a Fed Funds rate of 4.6% in 2025 and a PCE rate of 2.4%, which implies a 2.2% real rate. The Fed could leave its PCE forecast at 2.4% but raise the Fed Funds rate to 4.9% and signal a 2.5% real rate, which would be more in line with the 2.6% real rate the Fed had in 2023. Again, it goes to the Fed admitting that policy isn’t restrictive enough.

FOMC

The Fed must do this to get financial conditions to tighten again and keep the disinflation process working. If the SEP guidance doesn’t do the trick, the only option left would be to threaten more rate hikes, which would have to come in the form of communication leading up to the June meeting, and that’s a step the Fed won’t want to take without trying to use guidance first.

Of course, the Fed could choose to do nothing, leave the SEP alone, leave the three rates for 2024 on the table, and even maybe cut its PCE projection. That would be a risk-on signal for markets and commodities. At that point, financial conditions would likely ease even further, and all bets on bringing inflation back to target would seem to be off.

Q2 2024 Earnings Call Transcript")