tifonimages/iStock via Getty Images

2023 was another tough year for the precious metals sector, with a few of the larger gold and producers missing their guidance midpoints and reporting higher than expected costs overall. However, royalty/streaming companies like Wheaton Precious Metals (NYSE:WPM) have continued to put up phenomenal results, with this being despite setbacks at key assets last year among the group like Penasquito (strike) as well as Cobre Panama and Renard which headed into care & maintenance. However, despite the record results from multiple royalty/streaming companies, the group has been dragged down with the negative sentiment sector-wide, with Sandstorm Gold Royalties (SAND) sinking to multi-year lows before its recent rebound.

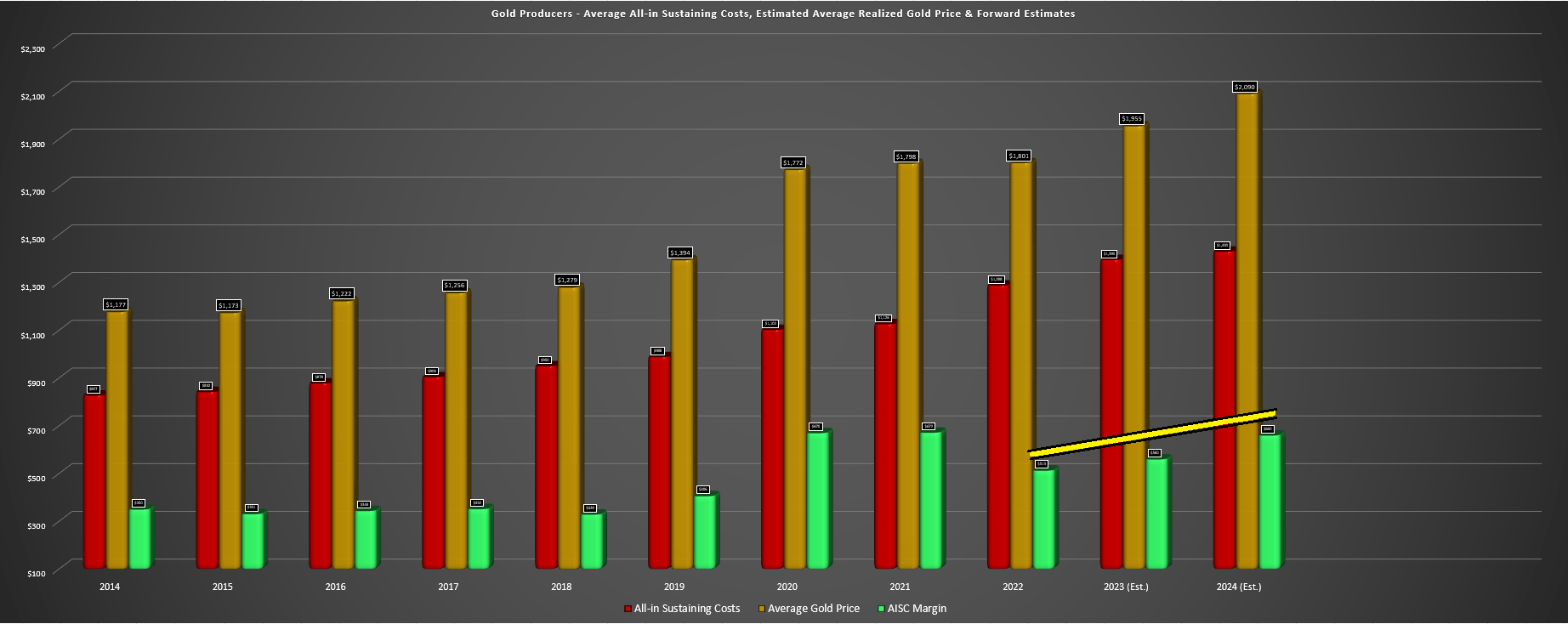

Gold Producer Universe – AISC, Gold Price, AISC Margins & Forward Estimates – Company Filings, Author’s Chart & Estimates

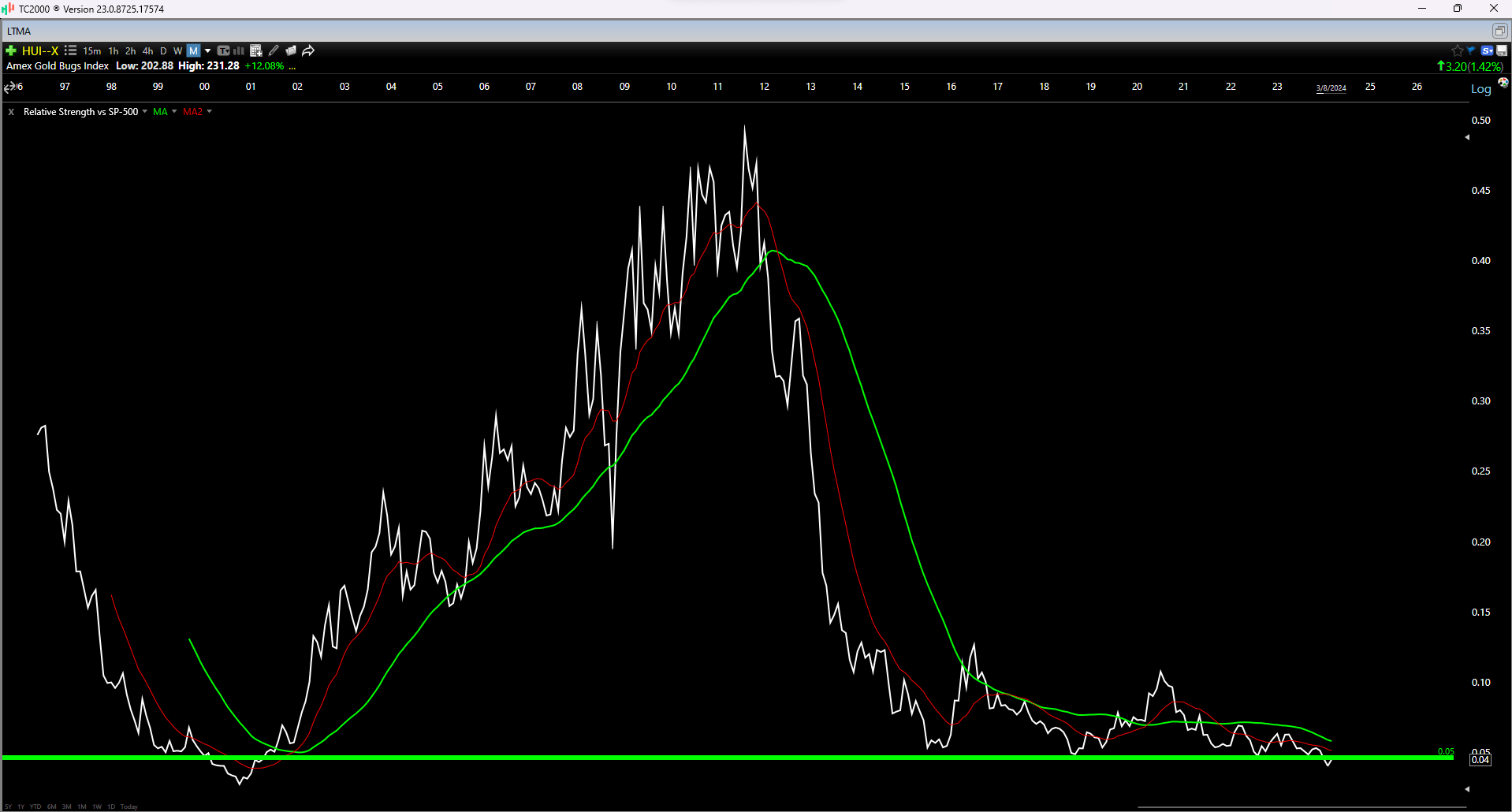

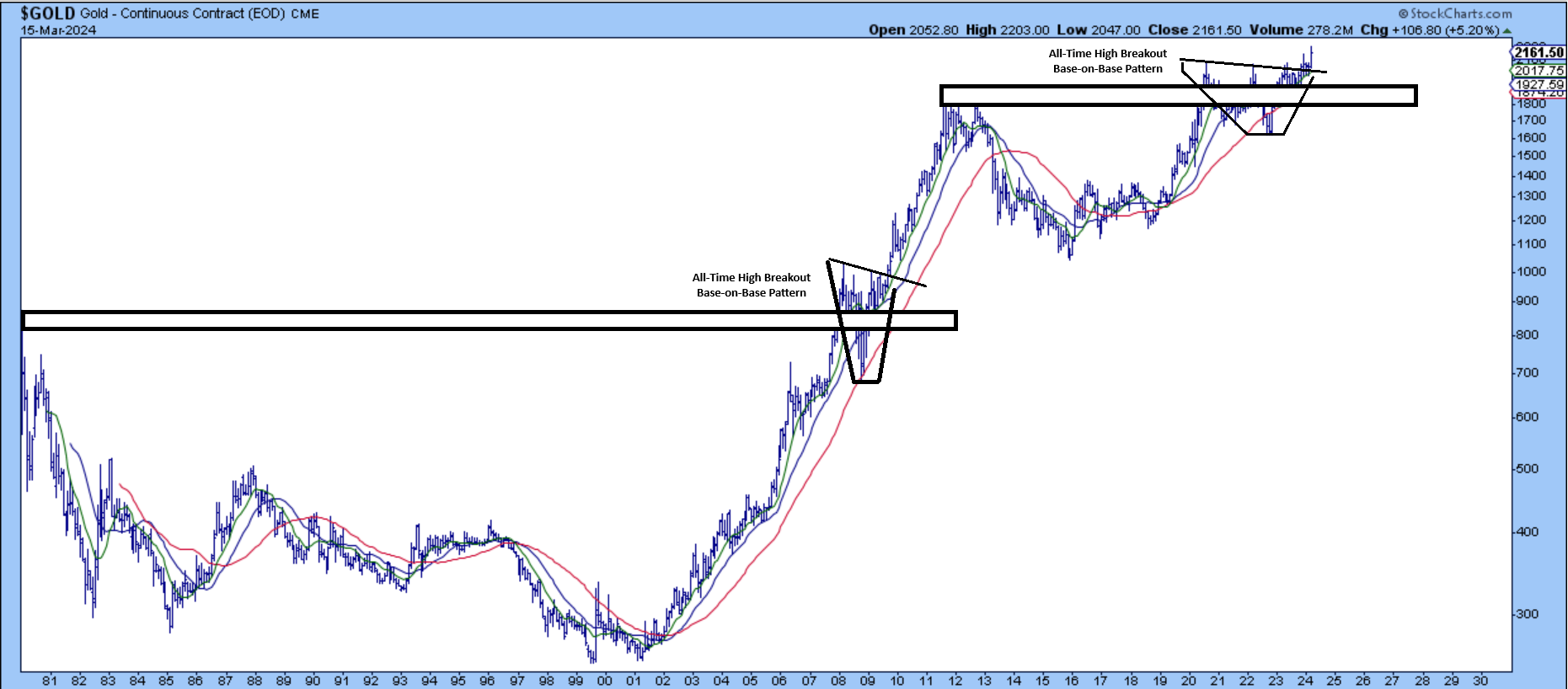

Fortunately, we have a much better setup to start March, which has placed a persistent bid under the sector. For starters, the margin compression suffered by the producers because of inflationary pressures has been offset by a higher gold price, with gold producers set to report significant margin expansion year-over-year in their Q1 results, and for 2024 if gold can remain above $2,050/oz. Meanwhile, margins in the royalty space have also improved materially, with royalty-heavy names on track for further margin expansion and stronger pipelines after a busy year of deal flow for the group. Hence, while the disconnect between the Gold Miners Index (GDX) and gold’s performance was partially justified last year, further upside looks likely with the sector in much better shape at current metals prices. In addition, the Gold Bugs Index [HUI] relative to the S&P-500 has rarely ever been low, pointing to the potential for significant mean reversion here as well.

Gold Bugs Index vs. S&P-500 – TC2000.com

In this update we’ll dig into Wheaton Precious Metals’ Q4 and FY2023 results, recent developments and where the stock’s updated buy zone lies:

Q4 & FY2023 Results

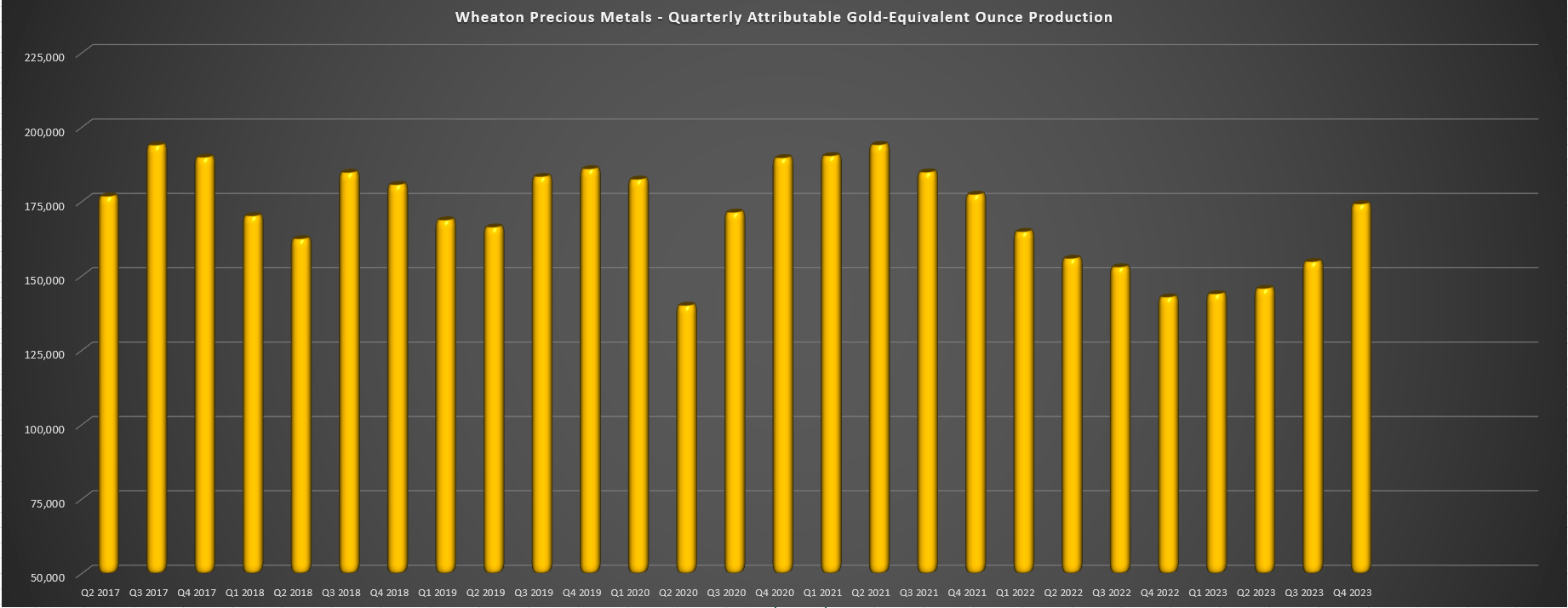

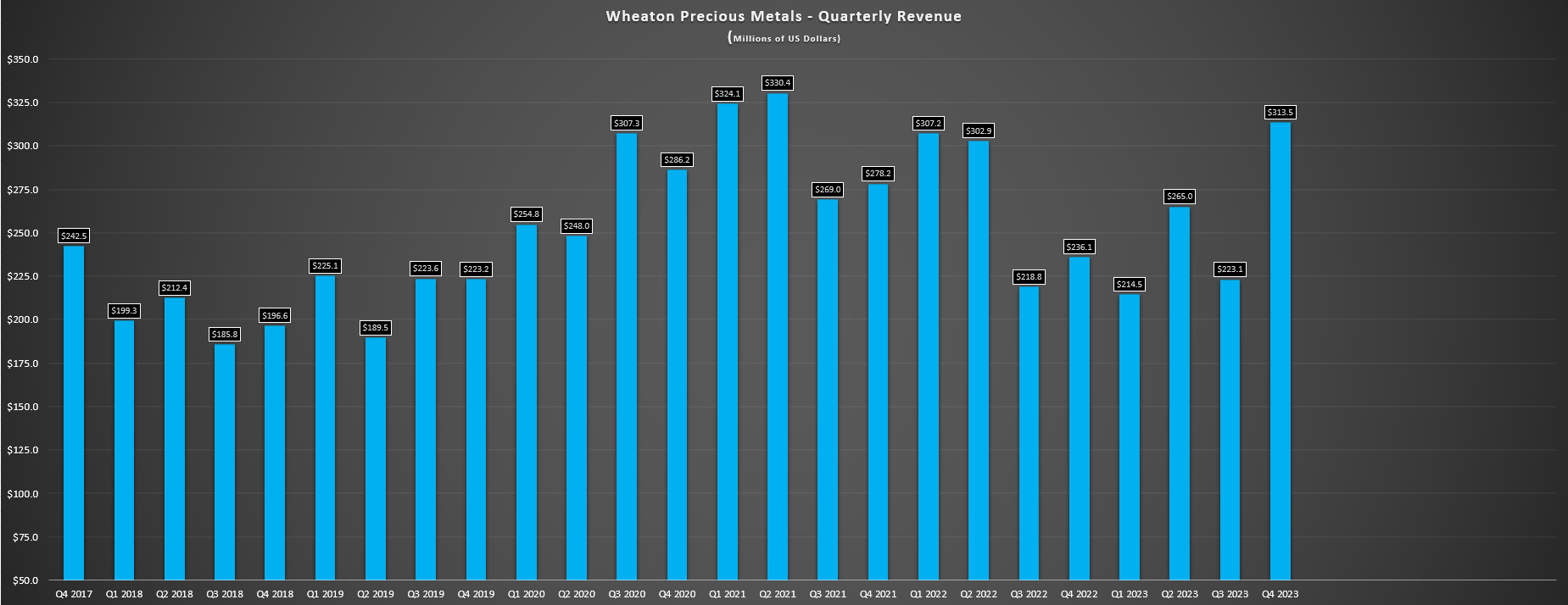

Wheaton Precious Metals (“Wheaton”) released its Q4 and FY2023 results this week, reporting quarterly attributable production of ~174,200 gold-equivalent ounces [GEOs], a 22% increase over the year-ago period. The increase in attributable production was despite a much softer quarter at Penasquito which was busy ramping up after its strike ended in October, offset by a massive quarter from Salobo with ~71,800 attributable ounces of gold produced (Q4 2022: ~37,900 ounces), a better quarter from Sudbury (~6,300 ounces), and significant growth at Constancia (~22,300 ounces), with much higher grades as mining moved into high-grade zones at the Pampacancha satellite deposit. Unfortunately, attributable production at Constancia will dip this year and weigh on production, but we will see initial contributions from streams at the Blackwater Project in British Columbia (Canada) and Platreef in South Africa.

Wheaton Precious Metals Quarterly GEO Production – Company Filings, Author’s Chart Wheaton Quarterly Revenue – Company Filings, Author’s Chart

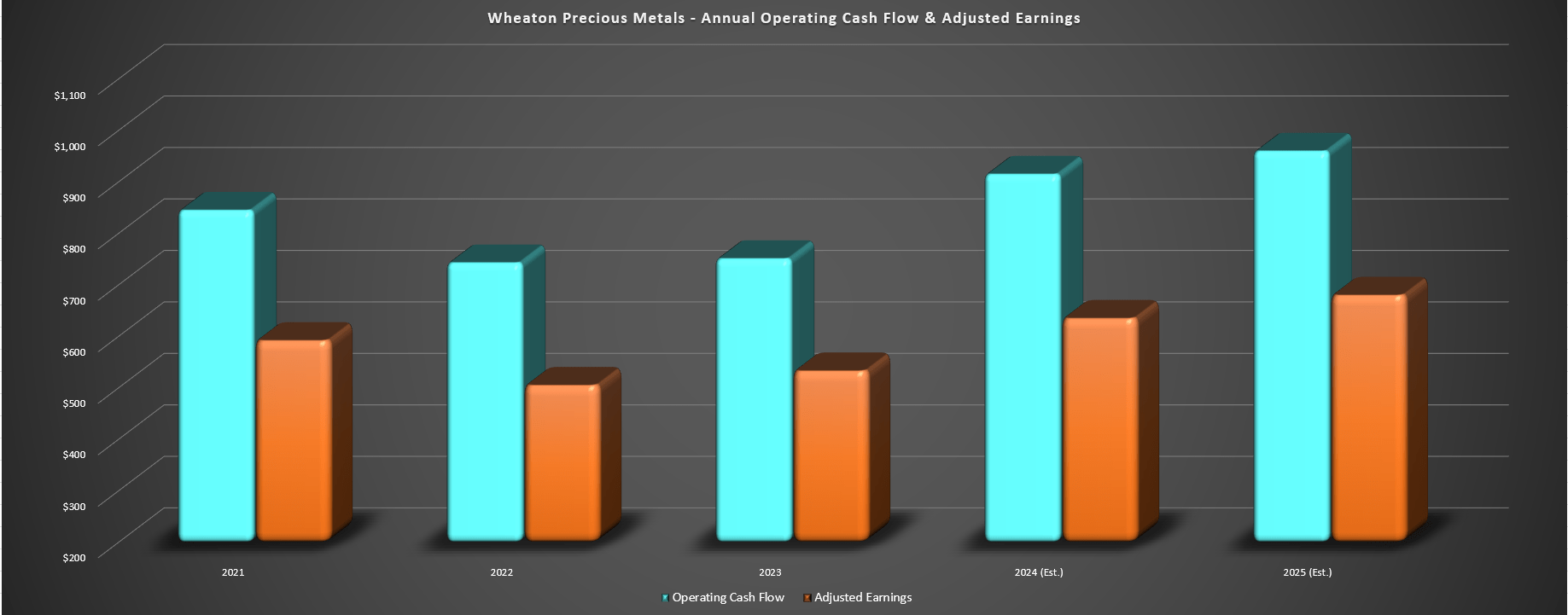

Moving to the annual results, Wheaton’s attributable GEO production came in slightly below its guidance midpoint at ~619,600 GEOs (FY2023 guidance midpoint: 630,000 GEOs), impacted by the significant shortfall at Penasquito because of the 4-month strike and a higher gold/silver ratio which impacted its gold-equivalent ounce production. This resulted in a 5% decline in annual revenue to ~$1,016 million (FY2022: ~$1,065 million) and operating cash flow increased just 1% to ~$751 million (FY2022: ~$743 million). And while annual operating cash flow and adjusted earnings of ~$533 million were below 2021 levels, results came in at near-record levels and will meaningfully this year. Notably, this is despite the negative impact of Aljustrel heading offline temporarily (suspension of lead/zinc concentrate production because of low zinc prices) and Minto also offline and under care of the Yukon government, with these assets contributing ~949,000 ounces of silver and ~4,400 ounces of gold (and ~43,000 ounces of silver) in 2023, respectively.

Wheaton Precious Metals – Annual Operating Cash Flow & Adjusted Earnings – Company Filings, Author’s Chart

The reason for the better setup into 2024 is largely related to higher metals prices, with gold sitting over 10% above Wheaton’s average realized price in 2023 ($1,968/oz) and silver also at higher levels at ~$25.20/oz vs. $23.64/oz last year. And while there’s no guarantee that we remain at/above spot levels for the remainder of the year, the stronger metals prices should help to offset what’s expected to be lower production at Salobo (lower grades partially offsetting higher throughput with Vale’s Salobo III Expansion) and lower production at Constancia. And while Wheaton is guiding for roughly flat attributable production this year based on its updated commodity price assumptions, 2025 will be a monster year, with the potential for Wheaton to generate closer up to $950 million in operating cash flow if commodity prices can continue to cooperate.

Wheaton Cash Costs & Cash Cost Margins – Company Filings, Author’s Chart

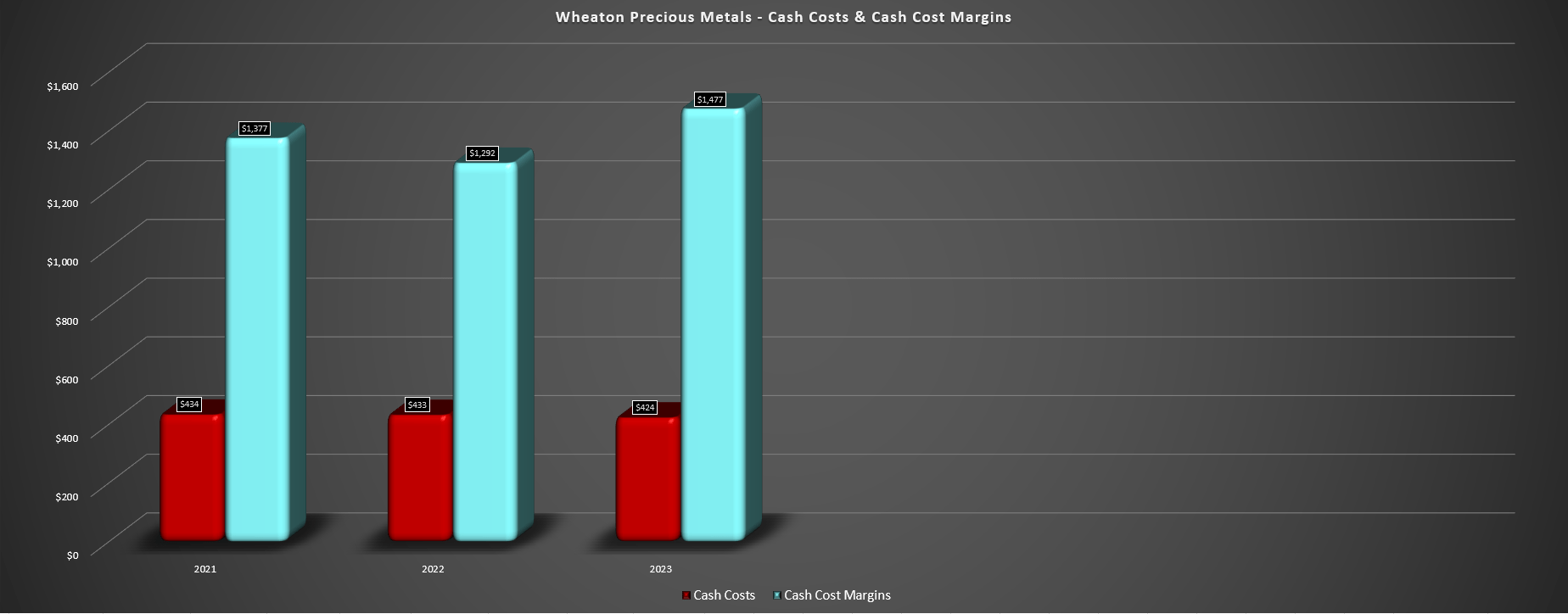

As for Wheaton’s balance sheet, the company ended the year with ~$550 million in net cash after making a $370 million payment to Vale (VALE) and $452 million in total upfront cash payments. The significant payment to Vale followed the completion of the throughput test, which was triggered with the Salobo Complex average throughput exceeded 32 million tonnes per annum over a 90-day period. This gives the company an enviable liquidity position of ~$2.6 billion with its undrawn $2.0 billion RCF to take advantage of any new deals that might come across the plate after an already year of transactions in 2023. Finally, Wheaton’s margins ticked up in 2023 to ~$1,477/oz, with cash costs down slightly year-over-year to $424/oz, translating to cash cost margins of 78%.

Recent Developments

Recent Deals

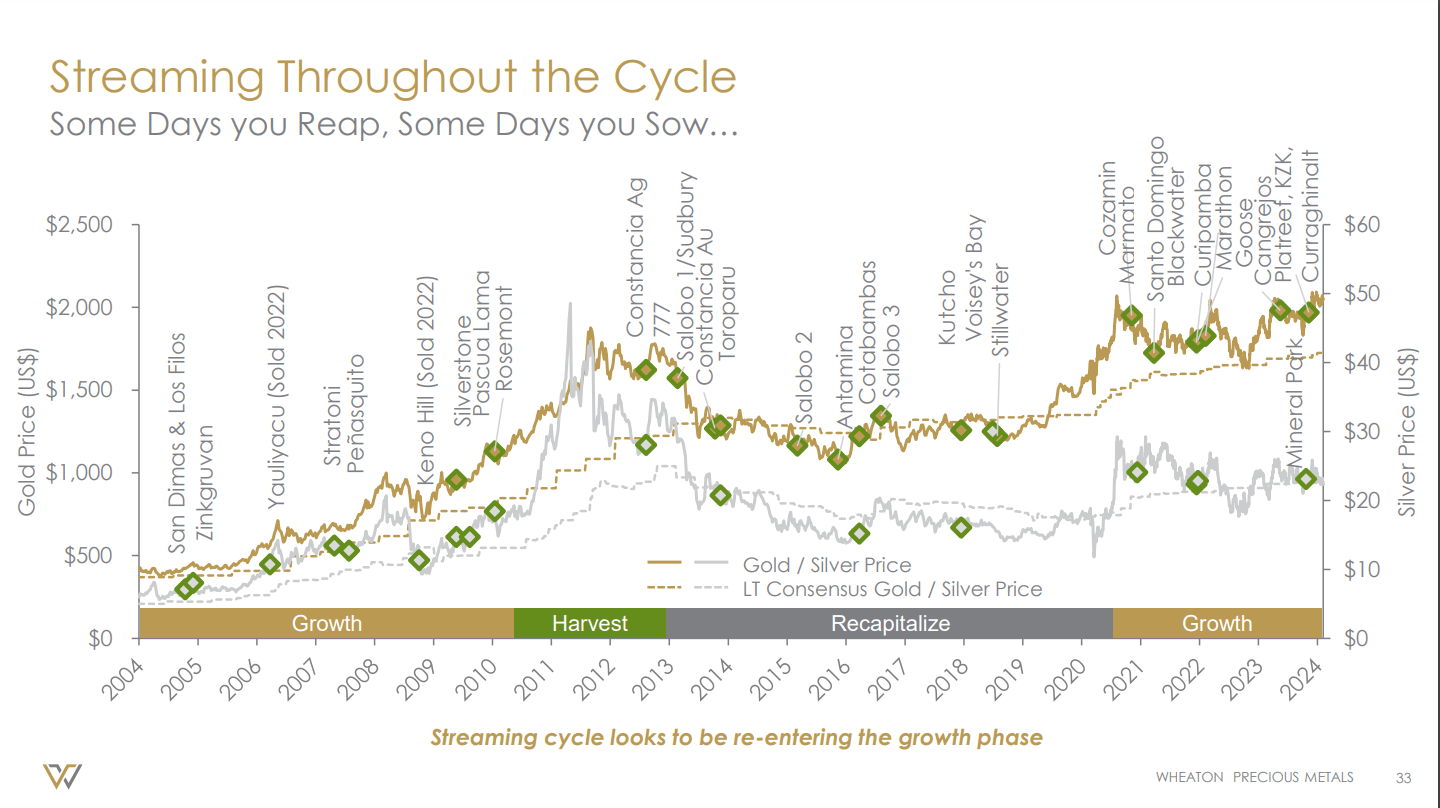

As for recent developments, 2023 was an extremely busy year for the company, with Wheaton ending the year with over 40 royalty/streaming assets, and 18 of these on operating mines after a record eight acquisitions for a value of over $1.0 billion. Some of the larger deals included a gold, platinum and palladium stream in South Africa on the Platreef Project (production expected in Q4 2024), a gold/silver stream on the Kudz Ze Kayah Project in Yukon, Canada, a silver stream on the Mineral Park Project in Arizona, and a gold stream on the massive Cangrejos Project in Ecuador.

These new streaming assets along with other assets already in construction like Blackwater and Goose in Canada are expected to help the company significantly grow production over the next several years, with Wheaton continuing to target an industry-leading growth profile, guiding for 850,000 GEOs on average in 2029-2033 (~45% growth relative to 2023 levels). And just as importantly, this has resulted in a significant improvement in jurisdictional and asset diversification with its high concentration to Salobo, especially after losing contributions from a few producing assets like Yauliyacu, 777, and Minto over the past couple of years.

Some new jurisdictions include South Africa (Platreef), Ireland (Curraginhalt), Ecuador (Curipamba/Cangrejos), Nunavut (Goose) and the Yukon (KZK) to complement its exposure to Blackwater (British Columbia), Marathon (Ontario), and other producing assets elsewhere in Canada like Voisey’s Bay, Kutcho, and Sudbury. Finally, Wheaton has added to its Tier-1 exposure in the United States with another copper asset in Arizona held by Waterton Copper, a gold development asset in Idaho (DeLamar) where it’s scooped up a royalty, and another gold development asset in southern Idaho at Black Pine, with both being relatively low capex heap-leach projects.

Wheaton Precious Metals – Gold Price & Transaction History – Company Website

Dividend

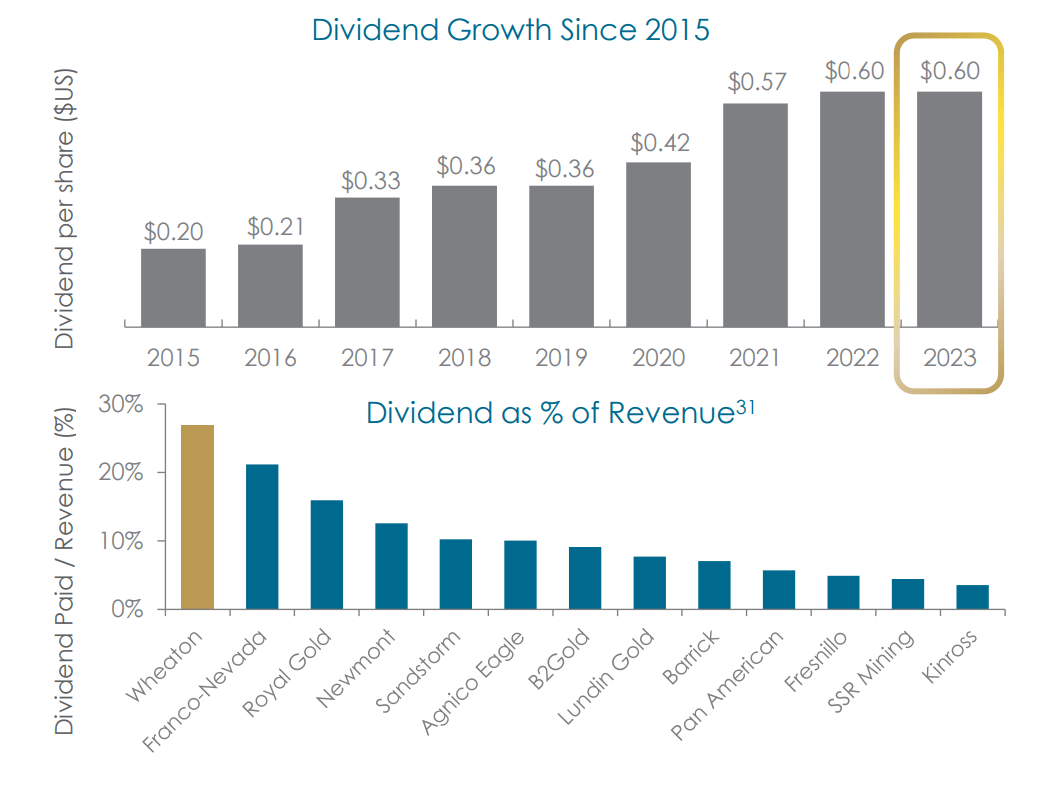

As for Wheaton’s dividend, the company raised its dividend this year to $0.155 (~3%) or $0.62 per share after holding it steady last year, noting that it is moving to a progressive dividend and that it will be increasing the dividend on an annual basis going forward. This is more in line with some of its peers in the royalty/streaming space that have consistently increased their dividends each year. Not only does this make Wheaton more attractive to dividend growth investors, but it’s certainly an exciting development for long-term shareholders already collecting a very attractive yield that can look forward to consistent increases going forward. And while this might seem risky given the volatility in commodity prices, Wheaton has the balance sheet and growth to support these increases, with its significant GEO growth from current levels able to more than offset any softer periods for precious metals prices.

Wheaton Dividend Growth & Dividend As % of Revenue – Company Website

Deal Environment

As for the current deal environment, the company stated that it’s open to looking at streaming opportunities on some of the more robust assets being shopped by Newmont (NEM) as part of its portfolio optimization and that it seems to have a healthy pipeline of opportunities it’s looking at. According to the company, this includes a couple of deals greater than $500 million, with most under the $300 million mark which is still quite significant for the company. As it stands, Wheaton has been more aggressive than its peer group which might suggest it’s over-paying, but its deals last year came in at below 1.0x NAV, making these attractive deals that have helped it get a further lead on its peers.

“For the last few years it has been focused on development, what we’ve seen is a little bit of focus on balance sheet strengthening by some of the potential diversified and other producers out there. So, I think it’s probably a 50-50 mix, I’d say, right now. 50% is probably still looking at development stage opportunities and the other 50% is looking at balance sheet strengthening. I don’t want to say balance sheet repair, but people are trying to shore up their balance sheets to be able to add and to increase, acquire, etcetera, in this environment. And that’s an area that they’re coming to us and looking for guidance on. I would say that the majority of the opportunities we’re looking at are still sub-300. But as always, there’s a couple that are greater than 500 that take some time to foster, and hopefully, we can get those across the line.”

– WPM Q4 2023 Conference Call Transcript

Long-Term Outlook

When questioned on its longer-term outlook and its ability to sustain deal generation given the lack of major new discoveries, this is certainly one worry for the junior royalty/streaming companies that have a higher cost of capital and may be less preferred partners as some developers would rather have the big-5 seal of approval and vote of over the bottom-5 royalty/streamers on their assets. Fortunately, Wheaton continues to find deals despite the competitive environment and the difficult market for developers somewhat balances the increased competition as selling streams or royalties at 0.50x – 0.80x NAV is a far more attractive option than raising equity at depressed levels with share prices trading at less than 0.30x NAV for many developers. Hence, I am confident that Wheaton will be able to continue to transact, though I’m a lot less optimistic about the outlook for some of the smaller names may have to fight tooth and nail or accept a much lower IRR to lock up any quality royalties and streams.

“And I can tell you for the last four years, it’s less and less and less. We’re not seeing as many good quality projects out there. And I’m fearful for the industry in the sense that there’s just not a lot of risk capital out there, so there’s not a lot of exploration and that means there’s just not a lot of good new discoveries that we see coming down the pipe. It’s getting to be a tighter and tighter market. I think in that space, the number of the success that we had last year where we more acquisitions than ever before, I mean, I just really do hand that to the team in terms of the work that we did on pushing that forward. A lot of those transactions were with people or companies that we’ve worked with in the past, and that really does come down to working on being a partner of choice. It’s something that we really strive to be here at Wheaton.”

– WPM Q4 2023 Conference Call Transcript

That said, if Wheaton can’t find a good use for its cash, the company noted that it doesn’t plan to let cash sit on the balance sheet and it would look at returning this to shareholders. This commitment to not stoop to lower-quality deals and to return cash to shareholders if it can’t find attractive opportunities and its cash position grows meaningfully is certainly a great setup for long-term investors and this combination of significant GEO growth plus long-term dividend growth is a great combination for those looking for an alternative to simply holding gold and silver. Let’s take a look at the stock’s valuation below:

“And with respect to the cash on hand, it’s been a pretty consistent message. If we can’t put it back into the ground effectively, it goes back to shareholders. I don’t see us ever if we ever bump up over $1 billion cash on hand, that to me is pretty lazy balance sheet. And that’s the point that if you ever see a cash balance kicking up at those kind of levels, we’ll start ramping up that dividend and start feeding even more of that back to our shareholders. We already lead the entire precious metal space on that front in terms of how much we, what percentage we give back to our shareholders, but we can amp that up further.”

– WPM Q4 2023 Conference Call Transcript

Valuation

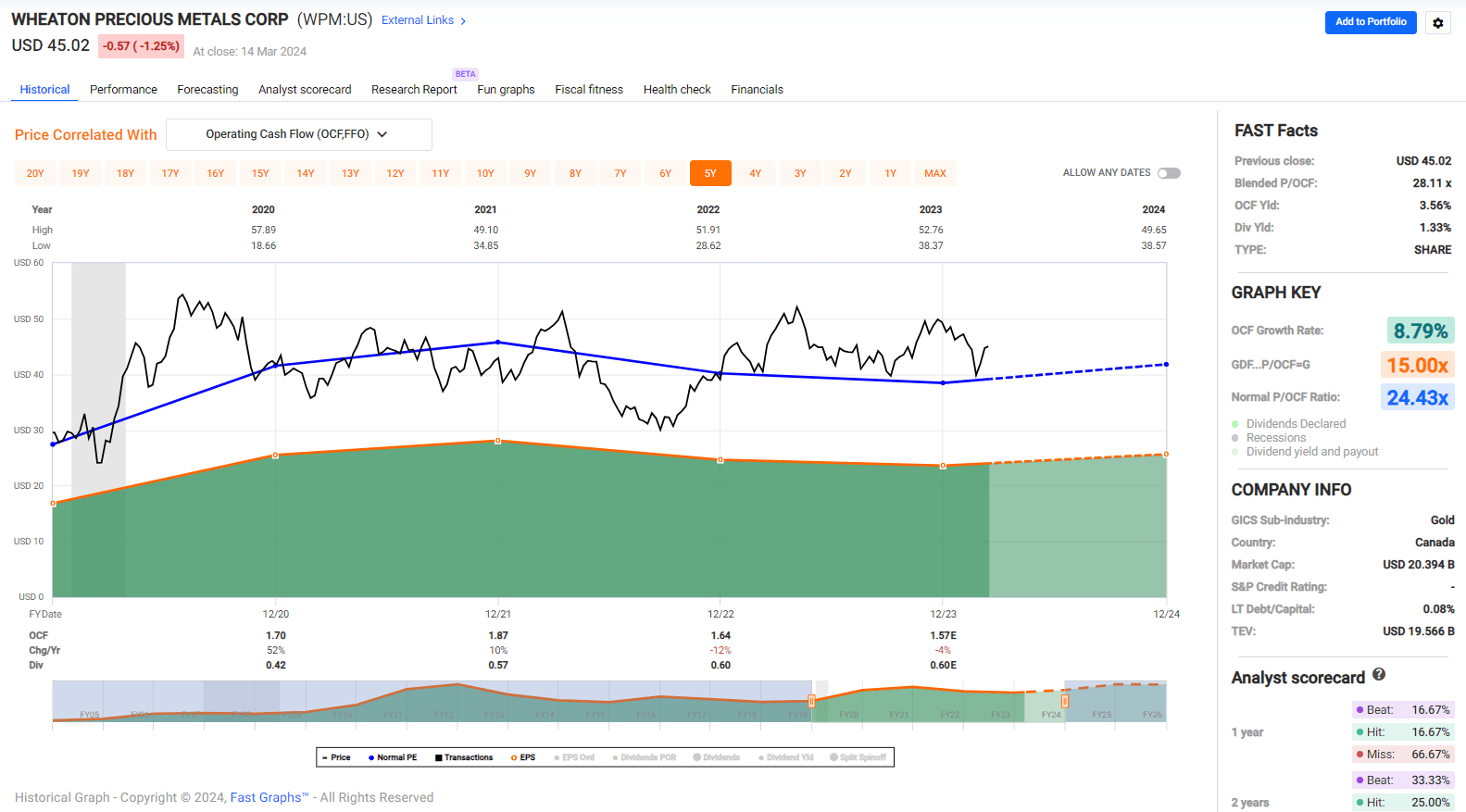

Based on ~454 million shares and a share price of US$44.50, Wheaton trades at a market cap of ~$20.2 billion and an enterprise value of ~$19.7 billion. This makes it one of the highest capitalization names in the sector currently, with it currently trading at ~22.2x FY2024 cash flow per share estimates. The stock’s current cash flow multiple places it slightly below its 5-year average multiple of ~24.4x cash flow, but this has been in a period of relatively stagnant silver prices and mostly negative sentiment sector-wide. And in better environments for the precious metals sector, Wheaton has regularly traded above 30x cash flow, and as high as 37x cash flow at its July 2020 peak. Hence, if we are heading into a new bull market for the sector as the recent breakout in gold might suggest, Wheaton’s could have significant upside as a cash flow multiple of 28-30x would place the stock US$57.00 – US$61.50 per share.

Wheaton Historical Cash Flow Multiple – FASTGraphs.com Gold Price Long-Term Chart – StockCharts.com

I prefer to use more conservative multiples to derive fair value rather than assume we trade back to higher multiples and think using multiples of 2.1x P/NAV and 26.0x cash flow is more appropriate. However, even using these more conservative multiples and ignoring FY2025 for now, which will see significant growth in cash flow per share with a full year of production from Platreef and Blackwater, WPM’s estimated fair value comes in at US$56.70. This translates to a 25% upside from current levels, suggesting that WPM could re-test its all-time highs if it trades in line with its updated fair value estimate, and could exceed all-time highs if silver finally joins the party and plays some catch-up to the gold price.

So, is the stock a buy?

While WPM has a meaningful upside to fair value and continues to be one of the safest ways to get precious metals exposure, I am looking for a minimum 25% discount to fair value to justify starting new positions in large-cap royalty/streaming companies to ensure a margin of safety. And if we apply this required discount to WPM, the stock’s updated ideal buy zone comes in at US$42.50 or lower. Hence, while I see it as a top-10 name sector-wide given its superior business model, I think Triple Flag (TFPM) continues to be the more attractive bet here. This is because it also has an impressive growth profile, nearly 40% of its revenue comes from silver (well above its royalty/streaming peer group), but it has a 34% upside to fair value based on its updated fair value estimate of US$18.00.

Summary

Wheaton Precious Metals had another solid year from a financial standpoint despite the setback at Penasquito given its superior business model that’s allowed it to increase its margins in what’s been a tough three-year stretch for the overall sector. More importantly, though, Wheaton is set up to report record annual earnings per share [EPS] and cash flow per share in FY2024, with further growth in 2025 as key assets come online. And looking out longer term, Wheaton has an enviable organic growth profile for a company of its size, with the potential to hit the 900,000 GEO mark in FY2029 (FY2023: ~619,600 GEOs) as several new streaming assets begin production and with the help of another few acquisitions in the period.

Even assuming no further upside in gold and silver prices ($2,125/oz gold and $25.00/oz silver), this would translate to over US$3.00 in cash flow per share, translating to a fair value of US$90.00 at a cash flow multiple of 30, which I think could easily be justified by a royalty/streamer of that scale with a solely precious metals focus. So, for long-term investors looking for a low-risk way to add precious metals to one’s portfolio combined with consistent dividend growth, I would view any pullbacks in WPM below US$42.50 as buying opportunities.

Q2 2024 Earnings Call Transcript")