bjdlzx

Comstock Resources (NYSE:CRK) is in a “swing basin”. Those kinds of basins are generally the higher cost but still competitive dry gas-producing basins. That means the basin is generally the first to idle rigs whenever costs are unfavorable. But this company has a few “aces” that many competitor basins do not have. As I wrote a few years back, management bought acreage when there were few or even no buyers around. It is kind of hard to overpay when you are the only one “on the other side of the table”. That means the company has a low location cost for its wells that is equivalent to a competitive moat compared to the latecomers.

Swing Basin

The Haynesville dry gas production is now heading towards a decline. But as shown below, that has yet to happen.

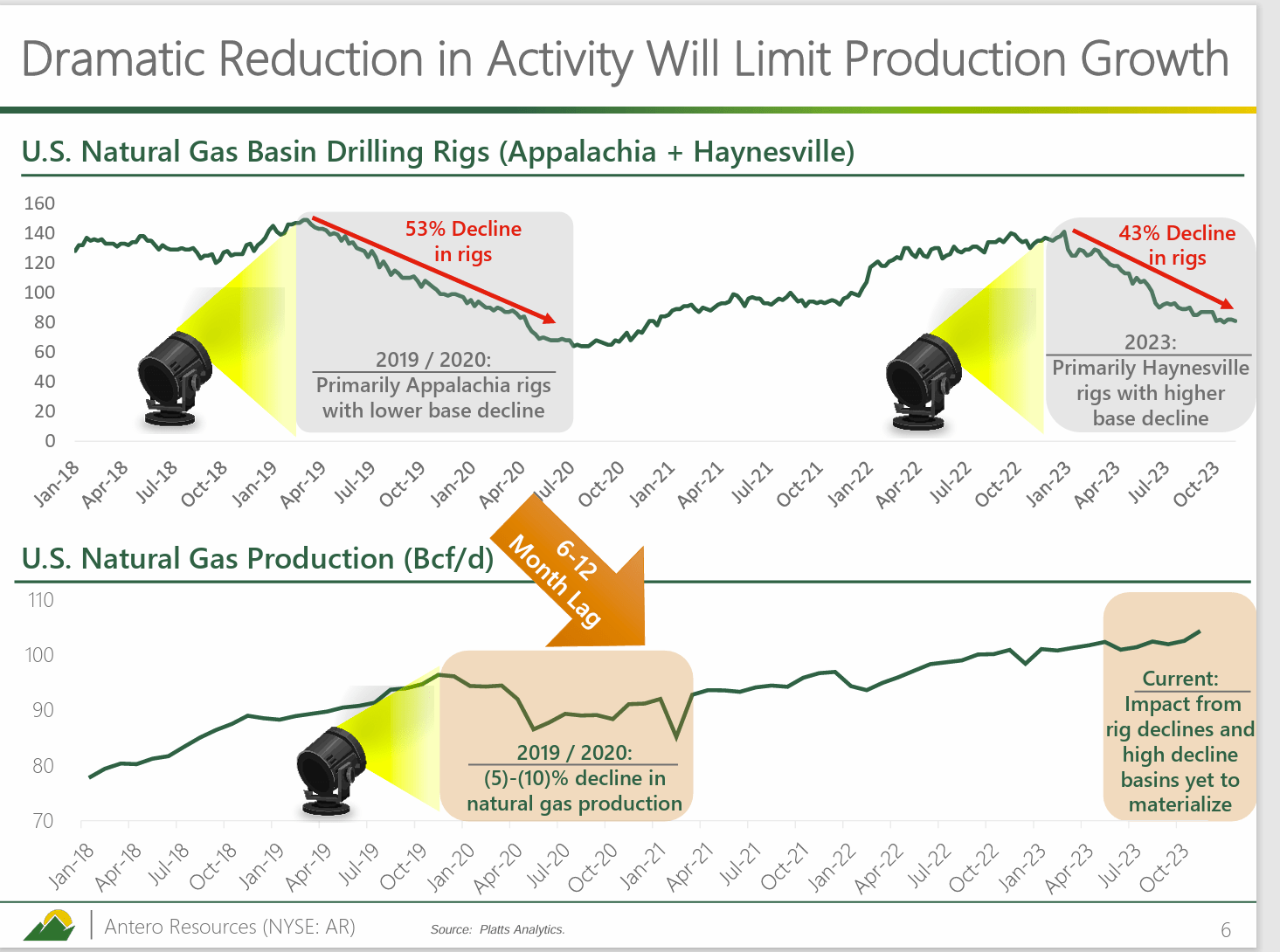

Antero Resources Presentation Of Rig Activity Decline Related To Natural Gas Production (Antero Resources Natural Gas Price Fundamentals Update November 2023)

As Antero Resources (AR) management has repeatedly noted, the rig count shown in the latest presentation on natural gas fundamentals will continue to decline until production and demand come into a balance that causes the natural gas prices to begin to recover.

The key thing to note is that the rig decline is already mostly where it was last time. Management made sure to note during the conference call that there is typically a nine-to-twelve-month lag between the start of a declining rig count until natural gas prices respond. It could, of course, go somewhat longer due to things like warm winters and cool summers. But the process in place will not stop until there is a pricing recovery.

That scenario throws considerable doubt about natural gas being in oversupply for the long term. It also means that when there are a lot of forecasts about cheap natural gas “forever”, then a contrarian investment opportunity likely exists because an investor “knows” the rig count will keep dropping.

It is beginning to look like there will be a natural gas pricing recovering this fiscal year. In fact, it will probably begin within six months. But the weather can easily change that forecast.

Low Location Cost

Jerry Jones is the major shareholder here. He invested back when this company was looking like a good candidate for the hereafter. He put roughly $1 billion of his own money in the company. Then the company went shopping. The Covey Park merger was announced in 2019. This announcement followed several in 2018 (an example).

The company was purchasing natural gas assets at the same time I was trying to convince investors that the industry and particular companies would not go broke because there would be a pricing turnaround at some point.

However, Jerry Jones, as a major shareholder of Comstock Resources, was one of the few people interested in natural gas assets after a very long decline in natural gas prices due to the rapid growth of the unconventional industry.

Now, that rapid growth is over. Therefore, it is very likely that natural gas will resume its normal cyclical behavior. But there appears to be considerable market expectations that natural gas will repeat the depressing down slide that happened during the rapid unconventional business growth that caused repeated natural gas oversupply. In that case, a lot of natural gas entered the market as a result of a lot of oil production coming online. There is no sign of that happening this time around. Now, should oil production happen to resume rapid growth, then the assumption would change.

In the meantime, Comstock Resources purchased acreage for a relatively cheap price using natural gas pricing assumptions that were far less than the acquisitions currently being done.

Location cost is therefore extremely low and very likely to be at least $1 million (per well) less than many competitors. Most companies do not report location costs to shareholders because it is not part of the “drill or not drill” decision-making process (and rightfully so). But since location cost is a cost, it will affect company profitability.

Even though Comstock Resources likely has similar “drill or not drill” decisions to the rest of the basin, it very likely has a very different profitability cycle from others that acquired acreage far later using higher future pricing assumptions.

Profitability

Management did report profits in the latest quarter. But they also reported that two rigs will idle. The fact that the company still made money at the current prices is a fairly decent accomplishment in a “swing basin” because there are likely to be a number of competitors both private and public that are losing money.

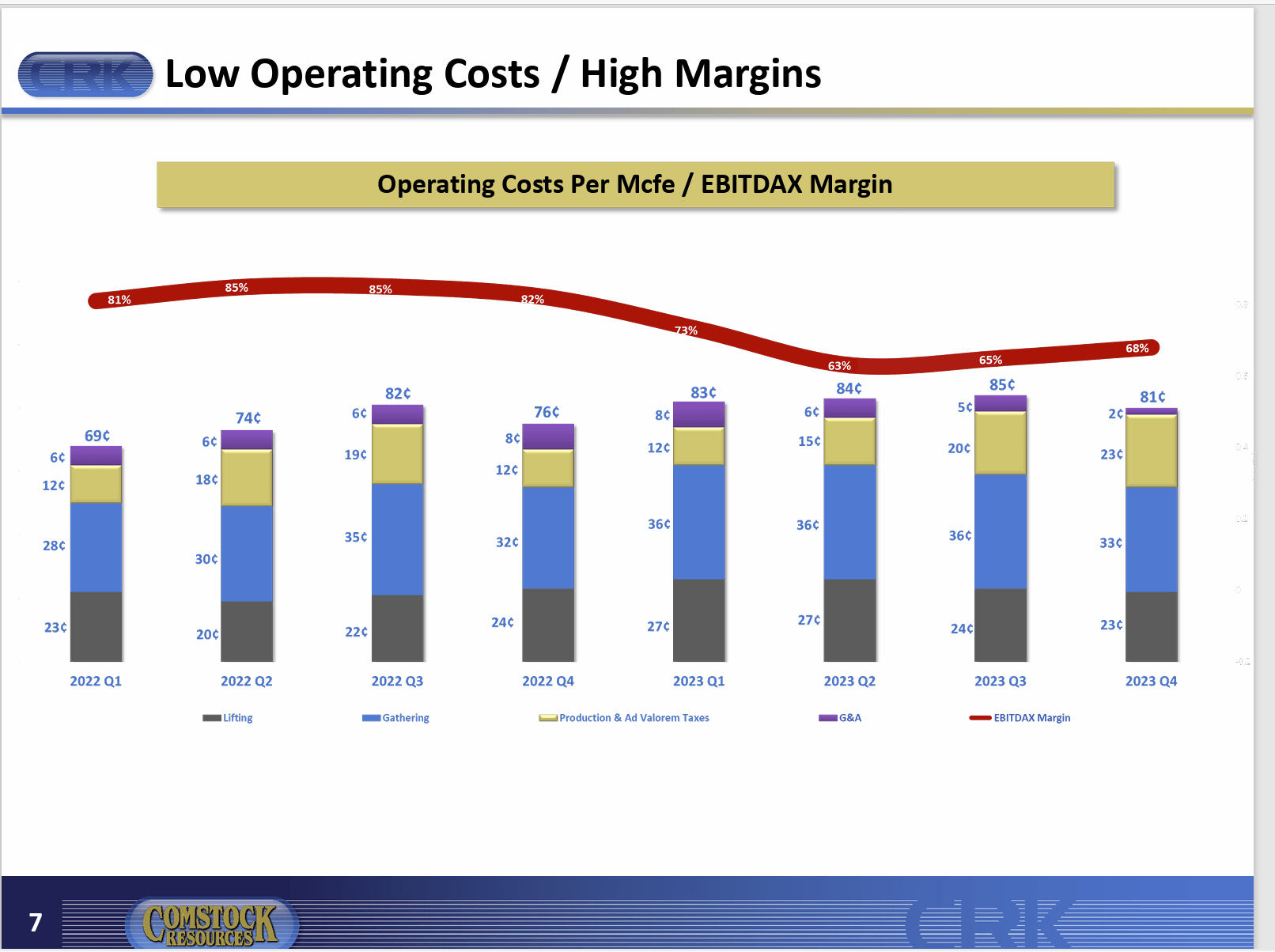

Comstock Resources Cash Operating Costs By Quarter (Comstock Resources Earnings Conference Call Slides Fourth Quarter 2023)

The operating costs, shown above, assure a decent cash flow unless natural gas prices decline quite a bit from current levels and stay declined. That is highly unlikely since rig counts are dropping in dry gas areas of production.

The combination of drilling costs and flow rates for these large wells allows for decent cash flow. But it also constrains well profitability to the extent that the basin is the “swing basin” when prices are low. These are big wells and have the total cost of big wells. But that also allows for depreciation to protect cash flow during cyclical downturns.

Summary

The Haynesville Basin may have higher costs than other dry gas areas like the Marcellus, but Comstock Resources has cheap acreage to offset at least some of that high cost. It may well be the lowest cost producer in the basin. Now whether that total cost beats producers in other basins is another question as the company is making decisions consistent with the Antero Resources presentation of swing basin producers.

The key difference is that location costs influence company profitability. That can be hard for shareholders to see because management never discusses location cost. Land does not depreciate. Therefore, location cost is not an obvious cost to the market. Nonetheless, any cost is part of the company profitability somewhere. In this case, it is likely to show up as part of return on equity (for starters) throughout the business cycle.

That means this company will likely be a good deal more profitable than the average Haynesville producer because it purchased acreage towards the end of a very long period of natural gas pricing declines when everyone was sure natural gas producers would go broke in large numbers.

Instead, that period began a natural gas price recovery that led to the huge prices for natural gas in fiscal year 2022.

Now, natural gas producers are looking at sizable increases in exporting capabilities, with the likely result that natural gas will join (the usually) far stronger world pricing market. Fiscal year 2024 and 2025 could therefore mark the transition from an oversupplied North American market to an undersupplied world market (most of the time).

Risks

The world market is heavily influenced by China, which currently has some daunting economic challenges. This may or may not change the currently optimistic industry view as it resolves itself.

The natural gas pricing outlook is always heavily dependent upon the weather. That makes the outlook extremely low visibility and very volatile.

Antero Resources management reported a roughly 30% decline in the cost of new wells. This can cause a further adjustment in competitive positions and profitability, depending upon how this is spreading throughout the industry.

Conclusion

This company remains a strong buy based upon the recovery of natural gas prices to better levels than is currently the case. Any management like this one that purchased acreage when no one else was buying is worth watching and considering as an investment.

Long-term, an investor like Jerry Jones sees a chance to make a lot of money to offset the risk he took. On the last cycle, he nearly tripled his cost of getting in. Therefore, investors can best believe that as a major shareholder, he sees even better times ahead, or he might have sold (or attempted to sell) the company during the last business cycle when the stock headed to $20 in fiscal year 2022.

This stock is not for risk-averse investors. However, for those income investors with a speculative part of the portfolio, a current investment could yield a good income return once the natural gas pricing recovery unfolds.

Q2 2024 Earnings Call Transcript")