buzbuzzer/iStock via Getty Images

Business Overview

In my opinion, Rush Enterprises, Inc. (NASDAQ:RUSHA) doesn’t get enough praise or attention from investors. This is a business that has been around since the 60s, has been public since 1996 and over the last 20 or so years, the stock has had a CAGR of 15-20% depending on entry point. Impressively, the company hasn’t shifted its business model much in the decades since being publicly traded. The high level business overview in the 1997 annual report is almost identical to that from the most recent 2023 annual report.

From the 1997 report: “Rush Enterprises operates a regional network of truck centers that provides an integrated one-stop source for the trucking needs of its customers.”

From the 2023 report: “We are a full-service, integrated retailer of commercial vehicles and related services… Through our strategically located network of Rush Truck Centers, we provide one-stop service for the needs of our commercial vehicle customers.”

This type of long-term growth has been possible for two primary reasons. One is the lack of disruption in the trucking industry. Trucks will be and have been a necessary mode of transportation, which has meant that truck centers have been necessary to support the fleets that exist. Further, the complexity of trucks is constantly increasing, which creates a larger need for skilled technicians to repair trucks, and the need for a more robust aftermarket parts channel to fill-in for the ever-increasing number of parts in trucks that can break. This has been a tailwind for Rush.

Rush has also been able to successfully integrate more truck centers over time. I am not an insider in the industry nor have I been able to speak with the management team, but they clearly have a special sauce to grow economically while taking share in the aftermarket parts industry, which is the less volatile, higher margin segment. This secret sauce seems to include hiring highly skilled technicians and maintaining a dense network of centers that can provide fast and high-quality service to their customer accounts.

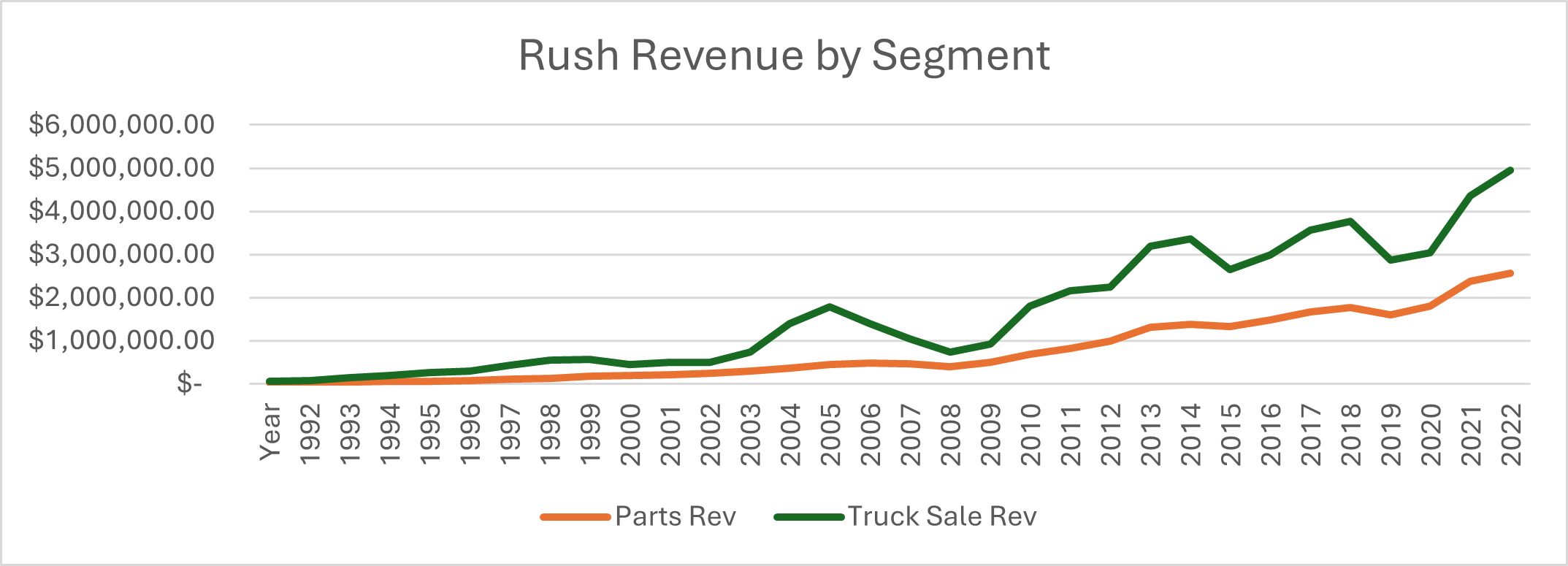

Rush focuses primarily on gaining share in the valuable aftermarket parts industry. Truck sales are extremely cyclical and are much less reliable for producing steady free cash flow. Below is a breakdown of Rush’s revenue in the aftermarket parts and truck sales segments. While both have gone up over time, parts revenue is much less lumpy than truck sales. Truck sales and aftermarket part sales go hand in hand, but the parts segment is and has been the more important segment to help Rush produce steadier free cash flow over time.

Rush Revenue by Segment (Created by Author)

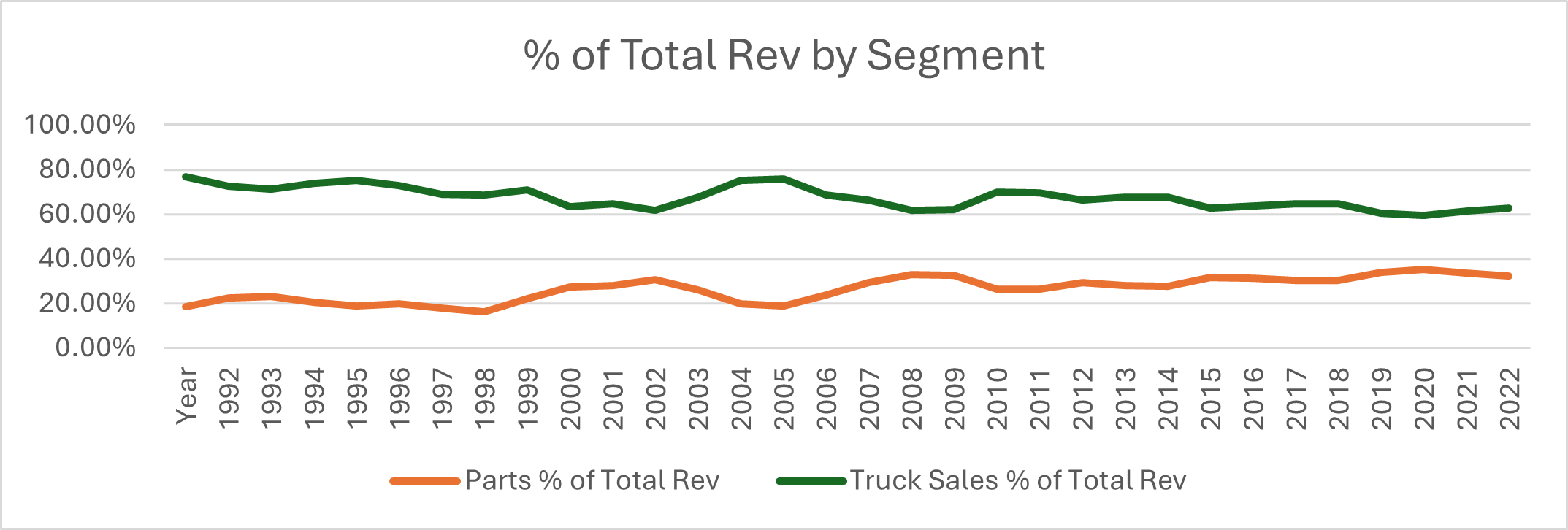

The percent of Rush’s revenue from parts and truck sales has also converged over time. The graph below shows this general trend and displays the company’s focus on gaining share in this industry.

Rush % of Total Revenue by Segment (Create by Author)

I see these trends continuing going forward because the truck dealership industry is still very fragmented, the tailwinds mentioned earlier are not going away, and economies of scale exist for Rush as it expands its network of dealerships and service centers over time.

With this in mind, I see a credible case for the stock to reach $70 over the next few years and $90 over the next 5+ years, based on my estimate of Rush’s normalized earnings over the next industry cycles.

FY2023 Results

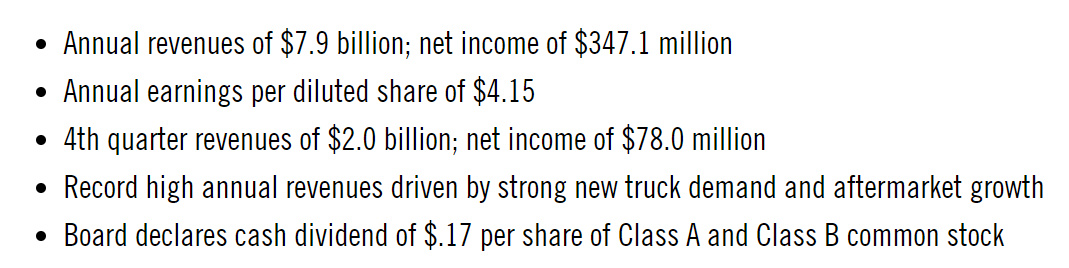

Headline Numbers from Q4 Earnings (Q4 2023 Press Release)

Rush’s FY2023 results were better than expected, as truck sales were consistently better than expected month by month as the year went on. This dynamic was due to pent-up demand from the pandemic that was finally met during the year.

The aftermarket parts segment also did well, as growth in large national accounts made up for a large decline in revenue from smaller accounts. Additionally, Rush benefitted from having customers in a variety of end markets, as certain industries such as energy and refuse offset a decline in weaker industries. These were solid results for the full year, but trends weakened in the second half of the year due to continued weakness in the freight market. This weakness will continue into 2024, but Rush is guiding for flat aftermarket parts sales in the year. Rusty Rush did comment that he hoped for low single digit to mid-single digit growth but was not putting that out as formal guidance.

Importantly, the company’s absorption ratio, calculated by the company’s aftermarket parts gross profit of a dealership divided by the overhead costs of running all of the dealership’s departments, not including the costs for the sale of trucks and the costs of holding truck inventory, remained high at 135%. For context, the company’s absorption ratio in 2005 was just over 100%.

FY2023 financial results were in line with the company’s impressive history and reflected weak freight conditions but pent-up truck demand at the same time. FY2024 will be worse when looking at headline numbers, but to understand Rush’s business value, it’s important to consider average cycle earnings and how they increase with each business cycle.

Price Target

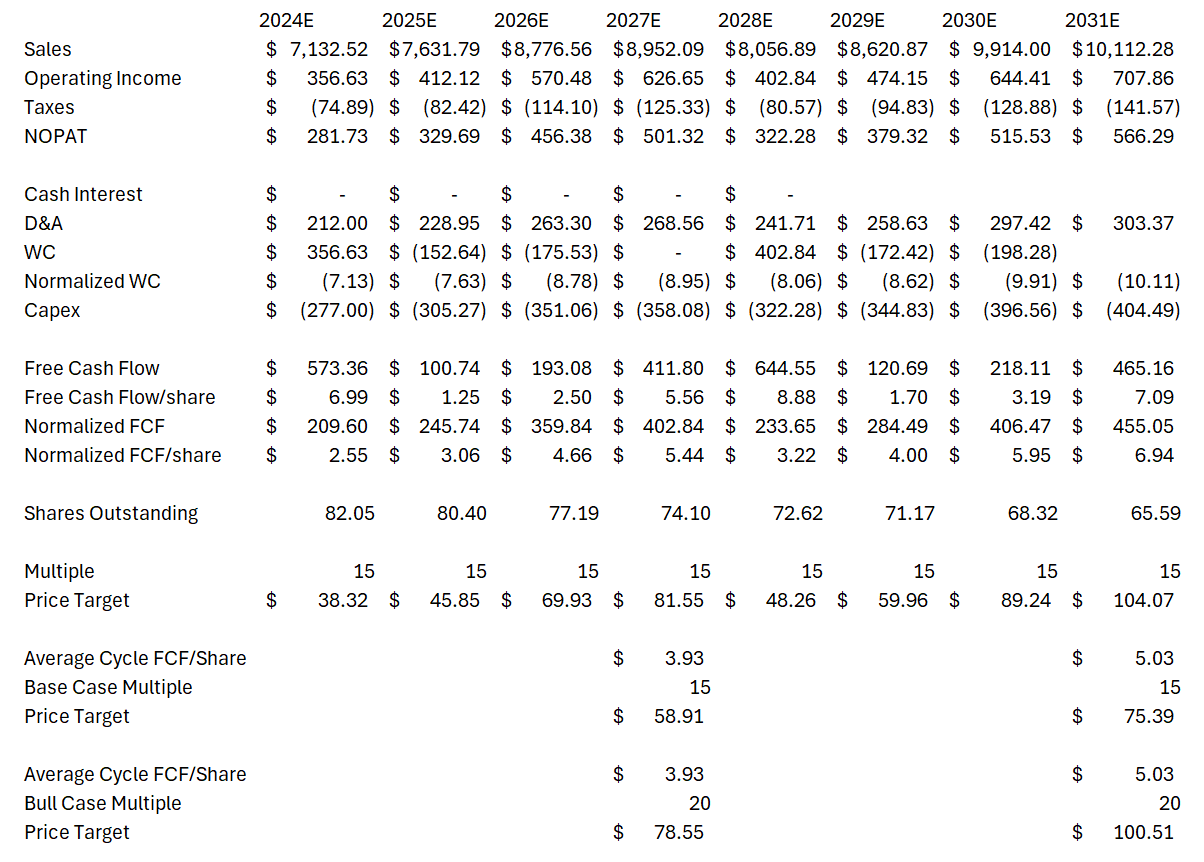

Given the cyclicality of the trucking industry, a single year’s free cash flow doesn’t provide an accurate picture of business value. Rather, estimating average earnings within a cycle gives a better idea. Many, including Rusty Rush, are expecting freight rates to trough sometime in mid to late 2024. After this, rising freight rates and EPA regulation that creates stricter emission standards that go into effect in 2027 will lead to strength in the trucking industry. This should make 2025 and 2026 strong years for the business, and 2027 a year with more muted growth, given strong growth in the prior two years. I use these assumptions in the model below, and I repeat a similar pattern to estimate what another business cycle will look like. This seems like an imperfect way to make this estimate, but there’s no perfect way to accurately predict a business cycle 5 years in the future.

As a note, I also smooth out changes in working capital to get a better picture of true earnings power by year. Large changes in inventory are common due to the number of trucks held by the company, depending on demand.

Financial Model (Create by Author)

In this upcoming cycle, I am estimating average free cash flow/share $3.93. In my base case, I am using a 15x multiple and in my bull case I am using a 20x multiple. Taking the midpoint of those multiples, I see a case for the stock to trade around $70 over the course of this cycle.

After this cycle, I estimate average free cash flow/share of $5.03. Using the same multiples for base and bull cases, I see a case for the stock to trade around $88 in 5+ years.

In general, I think it will be hard for investors to go wrong investing in a high-quality growth company at around 12x this cycle’s FCF/share, especially now that the company is more serious about repurchasing shares.

Risks

The primary risk is economic. The current freight and truck cycle has been driven by supply/demand imbalances caused by the pandemic. Aggregate economic demand has held up well in that time, but a recession with higher unemployment would obviously change the picture for this trucking cycle. However, I would expect Rush to gain market share in this situation despite worsening financial results.

Another risk is the risk of Rusty Rush retiring. He has led the company for many decades and is currently in his mid-60s. This should be a consideration for long-term investors, as a change at the top could lead to changes in business performance.

Q2 2024 Earnings Call Transcript")