metamorworks

Stellus Capital Investment Corporation (NYSE:SCM) is a well-managed business development company with a focus on middle-market companies.

The BDC just released earnings for the last quarter which showed that the dividend remained well-covered by core net investment income.

The BDC still profits from a higher-rate environment, thanks to an aggressive floating-rate posture, and Stellus Capital Investment has seen a rather substantial jump in net investment income in 2023.

Stellus Capital Investment’s stock presently pays a 12% yield, but I do see very constrained re-rating potential in 2024 as the BDC’s floating-rate exposure should weigh on its net investment income growth.

My Rating History

My analysis of Stellus Capital Investment concluded in a Hold rating in December because of the company’s large floating-rate debt investment portfolio that was poised to throw off lower net investment income in a rising rate environment.

The inflation trend up until then indicated that the central bank was probably bringing the rate-hiking cycle to a definitive end in 2024. This looks to have changed as January inflation was hotter-than-anticipated which may extend the central bank’s rate cut timeline.

Portfolio Review, Credit Quality And NII Upsurge

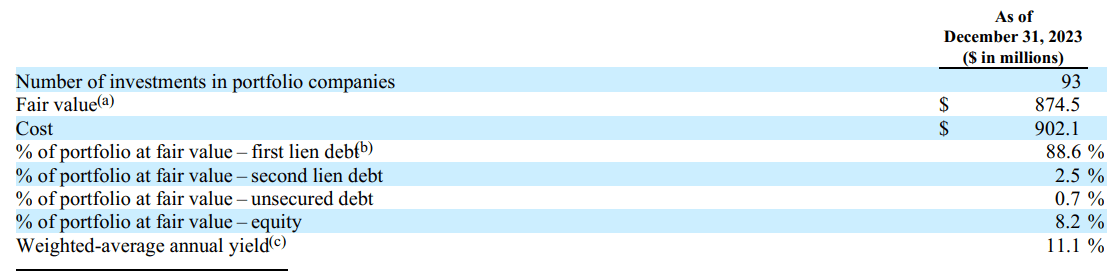

Stellus Capital Investment is a rather small BDC with a fair value of its investments of only $875 million. The BDC is focused on the lower-middle market and originates primarily First Lien Debt which accounted for 88.6% of investments at the end of the fourth quarter.

In total, Stellus Capital Investment’s portfolio was comprised of 93 investments in a range of industries.

Investments Portfolio (Stellus Capital Investment Corp)

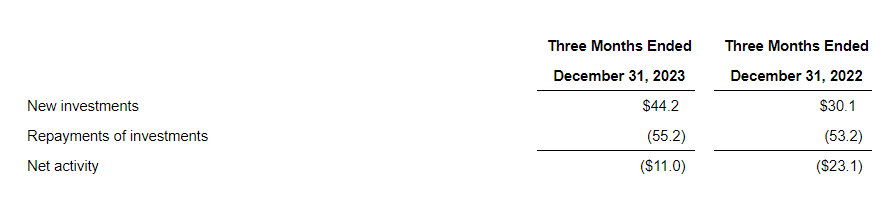

In terms of new investment activity, Stellus Capital Investment’s repayments of $55.2 million overshadowed the company’s new investments of $44.2 million. On a full year basis, however, the BDC’s portfolio gained $49.7 million. I anticipate higher originations in a lower-rate environment, so I think that Stellus Capital Investment’s portfolio has a reasonable shot to grow in 2024.

New Investments (Stellus Capital Investment Corp)

The non-accrual ratio as of December 31, 2023 was 1.3% at fair value, down from 2.3% at the end of 2022 and down from 1.6% at the end of 3Q-23.

Presently, there are four portfolio companies on non-accrual. Stellus Capital’s portfolio quality therefore is quite good and, together with the stable pay-out ratio, I think the dividend may be safer than I thought in December.

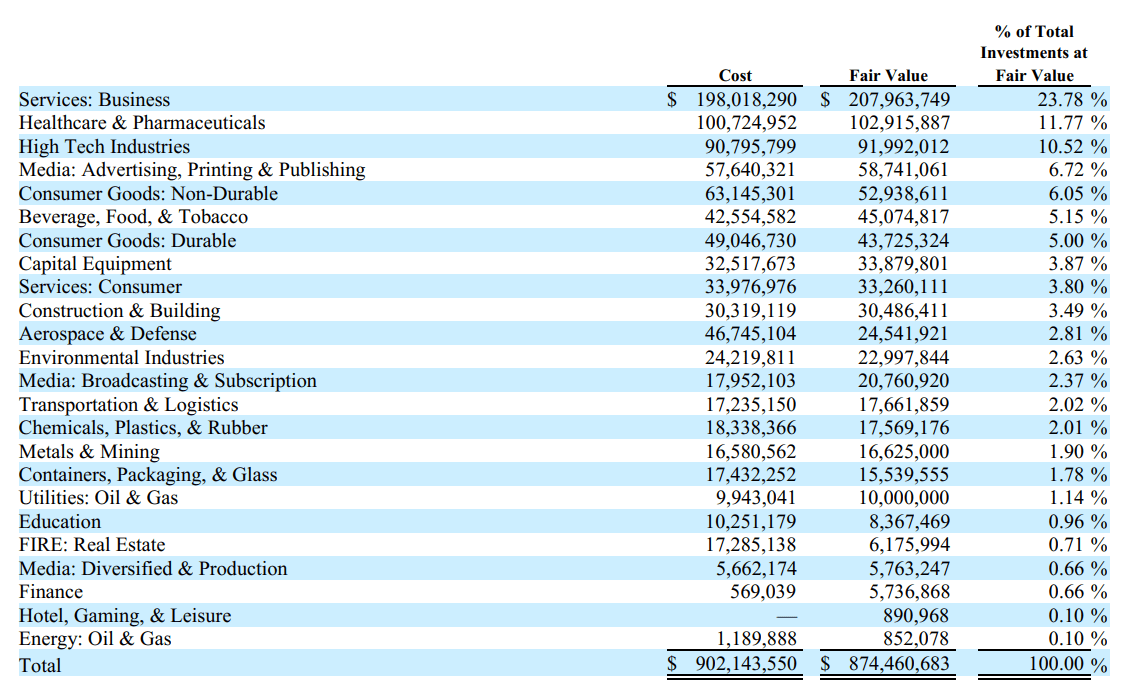

As far as Stellus Capital Investment’s diversification is concerned, the BDC remained overweight Business Services, Healthcare and High Tech Industries in the fourth quarter which provides the company with stable, recurring cash flow. The portfolio breakdown as of the latest quarter, is reproduced from the BDC’s latest annual filing with the SEC.

Portfolio Overview (Stellus Capital Investment Corp)

Stellus Capital Investment is primarily a floating-rate oriented BDC with approximately 98% of loans requiring floating-rate payments. This exposure benefited the BDC substantially in the last three years as the central bank embarked on one of its most aggressive rate-hiking cycles in recent history.

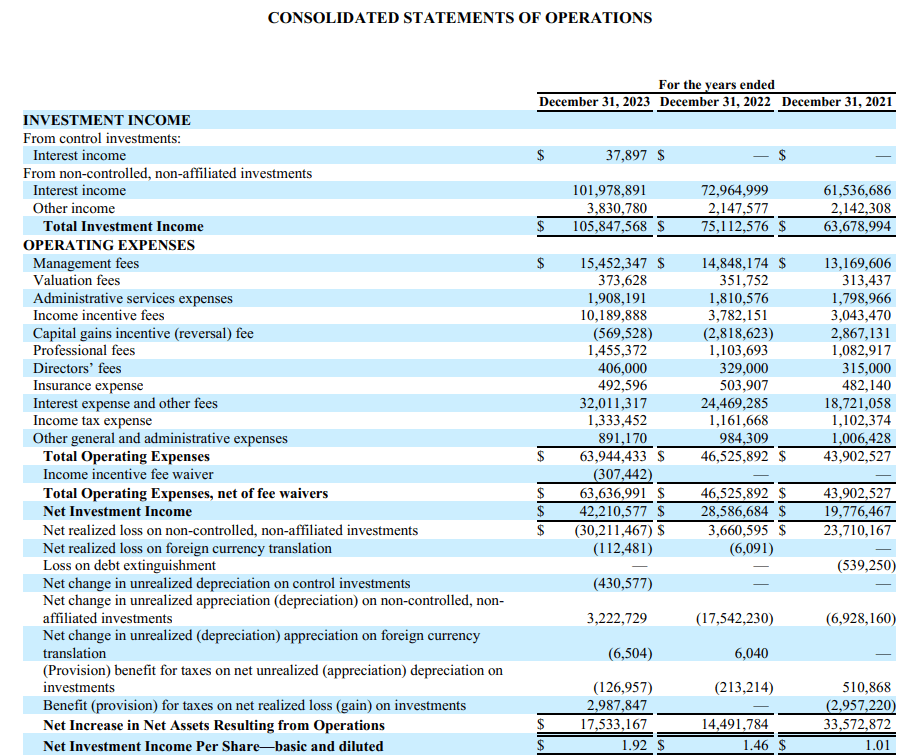

Stellus Capital Investment’s net investment income rose to $42.2 million in 2023, up 48% YoY. This growth was catalyzed primarily by a growing investment portfolio as well as floating-rate investments which triggered a big jump in interest income in 2023. On a per share basis, Stellus Capital Investment’s net investment income skyrocketed 32% YoY.

Consolidated Statements Of Operations (Stellus Capital Investment Corp)

Stable Dividend Coverage QoQ

I reduced my exposure to BDCs in 4Q-23 that have made a high number of floating-rate investment loans in their portfolios. I explained last time that I did this because I anticipated the central bank to lower short-term interest rates this year which should result in headwinds to net investment income growth.

With that being said, interest rates for now remain high and if inflation remains around 3%, the central bank might continue to delay its first rate cut of the interest rate cycle which benefits Stellus Capital Investment.

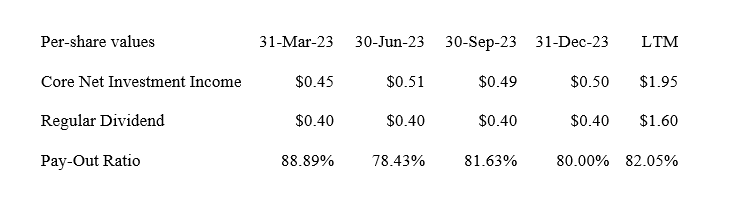

In the most recent quarter the BDC earned $0.50 per share in core net investment income which equated, based on a $0.40 per share per quarter dividend, to a dividend pay-out ratio of 80%. The dividend pay-out ratio has proven to be rather stable and the dividend itself therefore still has a high margin of safety.

Dividend (Author Created Table Using BDC Information)

SCM Is Probably Selling At Intrinsic Value

I don’t see a major competitive advantage in Stellus Capital Management’s portfolio posture or strategy and therefore rank the BDC has an average BDC.

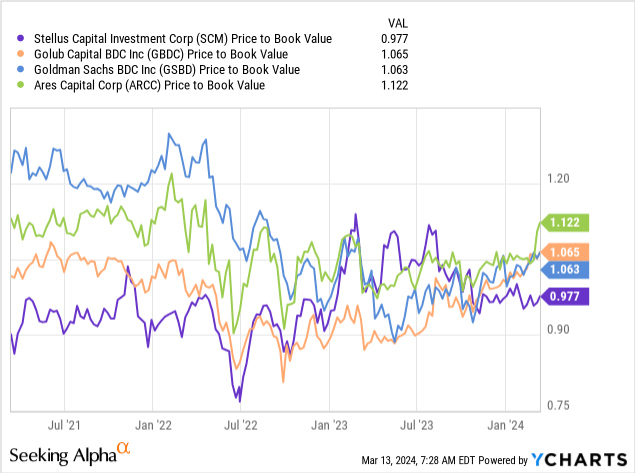

Stellus Capital Management is aggressively geared towards floating-rate loans, but the BDC is hardly alone in this regard. Stellus Capital Management’s stock is presently selling for a 2% implied discount to the latest net asset value which is $13.26 per share (my intrinsic value estimate), up $0.07 per share QoQ.

Other BDCs with similarly-positioned floating-rate investment portfolios like Goldman Sachs BDC Inc. (GSBD) or Golub Capital BDC Inc. (GBDC) are selling at similar NAV multiples.

Why The Investment Thesis May Not Play Out As Anticipated

I have adopted a much more cautious stance on floating-rate heavy BDCs in 4Q-23 due to the anticipated headwinds discussed in this article.

However, inflation may see a sporadic upsurge in 2024 in which case the central bank might further want to delay monetary easing measures.

I think this could be supportive of Stellus Capital Investment’s net investment income, though I do not see a whole lot of re-rating potential in 2024.

My Conclusion

Stellus Capital Investment’s fourth results, released last week, support my Hold rating for now. The central bank has not been as forthcoming with respect to rate cuts as I anticipated and interest rates, for now, remain high which supports Stellus Capital Investment’s NII and dividend.

With that being said, though, Stellus Capital Investment, and other floating-rate BDCs for that matter, are unlikely to see a similarly substantial YoY increase in net investment income moving forward as NII tailwinds, provided by the central bank, tail off.

I think a Hold rating can continue to be justified when taking into account Stellus Capital Investment’s rather stable pay-out ratio QoQ, but I stand by my assertion that the BDC is probably going to see NII pressure moving forward.

Q2 2024 Earnings Call Transcript")