deepblue4you

Co-produced by Austin Rogers.

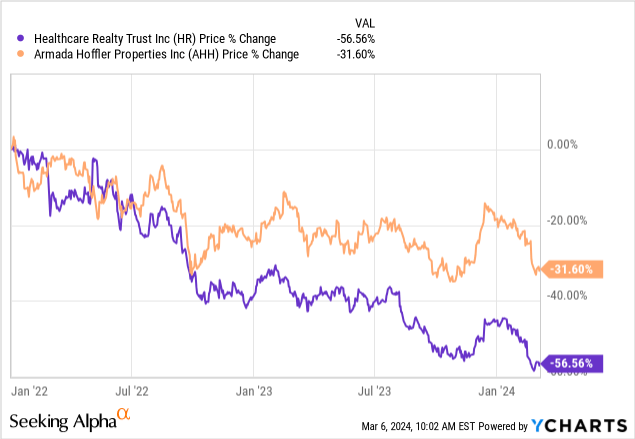

After rallying in late 2023, REITs have sold off again and given up a good portion of their gains. Some of them are down back to where they were in the Fall of 2023 and are down up to 50% in total:

It appears that the high hopes of near-term cuts to interest rates have faded away in recent months.

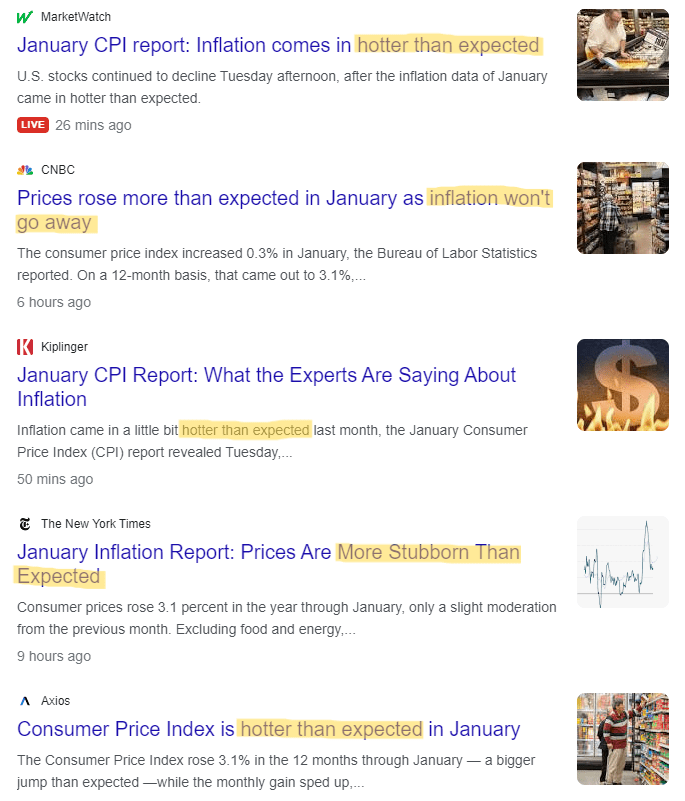

This is likely because the most recent CPI report which came in mid-February put the REIT market in a tizzy. The common theme of the news headlines was that inflation was “hotter than expected.”

Google Search

This reinforces the narrative that inflation is and will remain “sticky” at rates above the Fed’s 2% target, which in turn means that the Fed will have to hold their key policy rate at its current level for longer.

Hence, the selloff in stocks, especially rate-sensitive sectors like REITs (VNQ), but also utilities (XLU), and regional banks (KRE).

But I am here to warn you.

The trajectory of inflation continues, and interest rates are still downward and therefore, I think that this opportunity to buy REITs at such low prices will be short-lived.

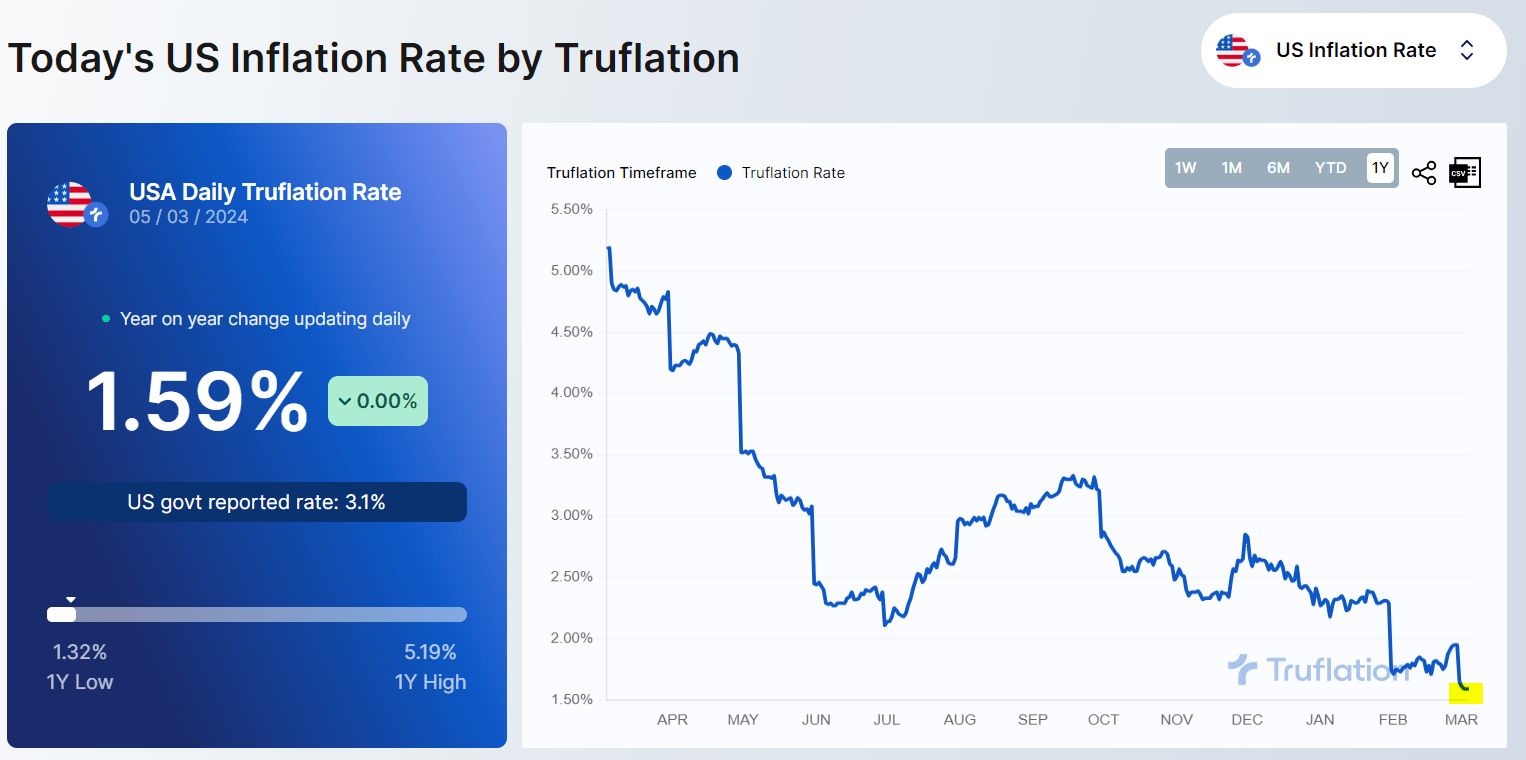

For example, look at Truflation, which we believe is a better representation of real-time inflation than the Bureau of Labor Statistics’ CPI metrics.

Truflation

Compared to the CPI’s reported 3.1% YoY inflation, Truflation reports a mere 1.59%!

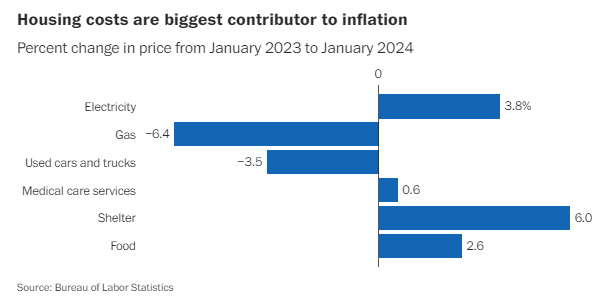

The single largest contributor to the increase in the CPI in January was the “shelter” component, accounting for over 2/3rds of the increase. In January, the CPI reported a year-over-year shelter price increase of 6%.

Bureau of Labor Statistics via Washington Post

The CPI’s shelter component is made up primarily of “rent of primary residence” and “owners’ equivalent rent.”

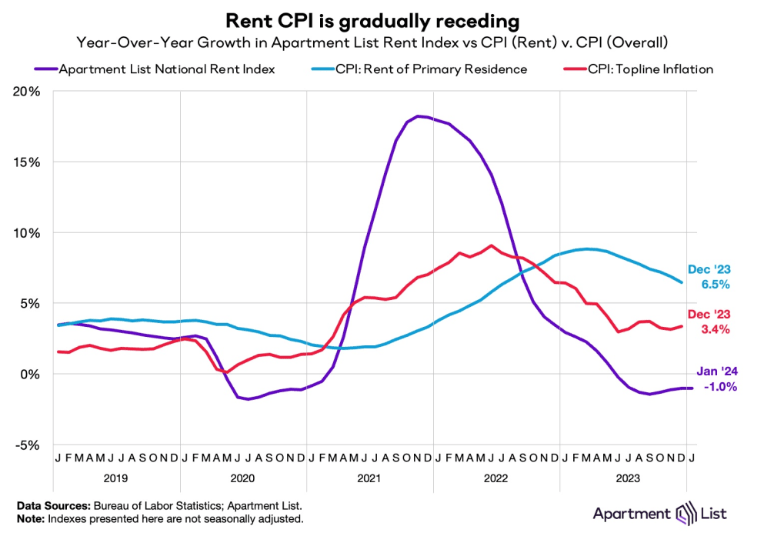

In January 2024, the CPI showed “rent of primary residence” still up 6.1% YoY. Compare that to Apartment List’s -1.0%, Redfin’s 1.1%, and Zillow’s 3.4%.

Apartment List

If you average the rent indices of Apartment List, Redfin, and Zillow, you get 1.2% YoY rent growth for January. That is a far cry from the CPI’s reported 6.1% YoY rent growth!

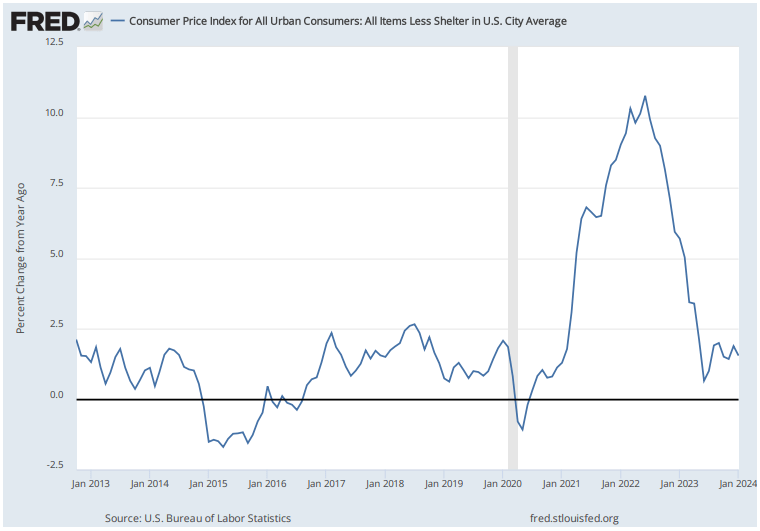

To illustrate what a huge difference shelter is making in the CPI right now, consider that the overall CPI rate excluding shelter would have been 1.54%.

CPI Ex Shelter YoY:

St Louis Fed

This was the 8th consecutive month that CPI ex-shelter was below 2%.

If instead of the CPI’s shelter metrics you plugged in the above-average of real-time rent changes of 1.2%, January’s headline CPI rate would fall to 1.4%.

As you can see in the Apartment List chart above, CPI rent (as well as owners’ equivalent rent) is now on the downward slide, but they have been falling at an arduously slow, gradual pace.

Of course, home prices have rebounded to about 5% YoY, but the CPI (rightfully) does not take home prices into account. People do not buy homes every month, or even on a somewhat regular basis. It is a rare, extremely big-ticket purchase that is almost always financed by debt or some other “OPM” (other people’s money) like a gift from family members.

The actual monthly cost of homebuying has to incorporate mortgage rates, which have declined considerably in recent months.

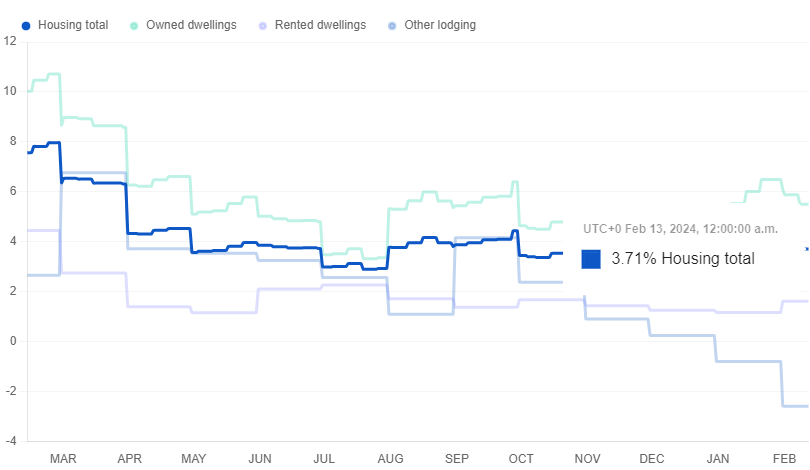

Truflation’s housing inflation data attempts to get at the true, real-time costs of both homeownership and renting (as well as “other lodging” which includes Airbnb and certain hotels).

Truflation

Again, if instead of the CPI’s 6% YoY increase for shelter you plugged in Truflation’s 3.7% number, the headline CPI would be 2.2%.

Given the fact that the shelter component of the CPI lags real-time rent changes by about a year, we should expect YoY shelter CPI growth to continue its gradual, downward slide for the next 6 months or so. It will likely bottom sometime this Summer or Fall.

Our guesstimate is that it will bottom around 1.5% for the overall shelter component and about 1.75% to 2% for the “rent of primary residence” item. But, given the fact that real-time rent growth is expected to remain muted this year due to the large amount of supply coming to market, YoY shelter CPI should likewise remain muted for an extended period thereafter.

We have made this point many times now, but we will repeat it again:

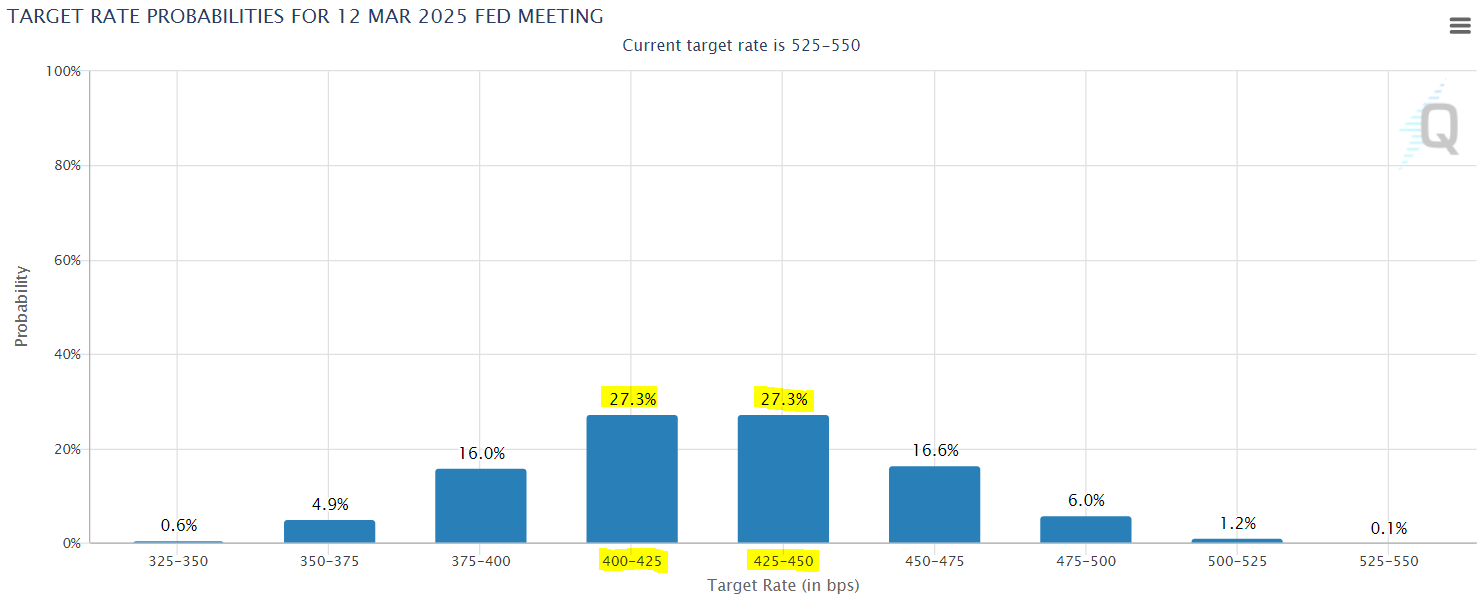

Unless non-shelter inflation makes a resurgence, both headline and core inflation should continue to decline over the course of 2024. With lower inflation, the Fed will have the room to cut rates, and this why FedWatch is still predicting that interest rates will be >100 basis points lower a year from now:

FedWatch

This bodes very well for REITs!

They crashed due to the steep rise in interest rates, and therefore, I expect them to recover just as fast as they dropped once it becomes clear to the market that interest rates are headed lower.

It will kill the narrative of “higher for longer” and as a result of this, I expect investors will rush back to REITs to secure their high and growing yields.

Today, there are plenty of high-quality REITs that offer 6-8% dividend yields that are not only sustainable, but also growing. Just to give you a few quick examples:

- EPR Properties (EPR) offers an 8.3% dividend yield, and it just hiked its dividend by 3.6%.

- NewLake Capital Partners (OTCQX:NLCP) offers a 10% dividend yield and it just hiked its dividend by 2.6%.

- Getty Realty (GTY) offers a 6.8% dividend yield, and it just hiked its dividend by 4.8%.

These are just 3 examples, but there are many others.

They offer you >10% annual total returns from their yield and growth alone, and then on top of that, they offer substantial upside potential as they reprice to a lower interest rate world.

You need to remember that REITs also retain a big chunk of their cash flow to reinvest in growth. Therefore, the real cash flow yields are actually a lot higher than the dividend yields. To take the example of EPR Properties, it is today priced at 8.4x FFO, which is the equivalent of a 12% cash flow yield.

If it simply repriced at an 8% cash flow yield, its share price would need to rise by about 50%, and I think that this is very realistic. Even at an 8% cash flow yield, the company would still be priced at a historically low valuation and offer good return prospects from its yield and growth.

So don’t miss this chance to buy the dip. Between the yield, the growth, and the upside, the total return prospects are today exceptional, especially given that most of these REITs are relatively safe investments when compared to Tech stocks (QQQ) and other popular investments.

Bottom Line

The “hotter than expected” CPI number certainly roiled the markets and caused a sharp selloff in many REITs. This is always disappointing to see play out.

But remember that this is a short-term phenomenon. Our long-term view remains that disinflation will continue over the course of 2024, even if that disinflation is coming painfully slowly.

With disinflation should come multiple Fed rate cuts, which should in turn fuel a strong rally in REITs for the balance of 2024.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")