JHVEPhoto

Dear readers/followers,

Unfortunately, Novo Nordisk (NVO) goes into my 2023 bag of the companies I was very wrong about. I underestimated this company’s ability to outperform the market during an already overvalued time, and as a result, the RoR for the company was far better than the market – and I held no real stake in this company.

I’ve looked through the results and also the trends and what we may expect for the company going forward. As with most overvalued companies, I reach a conclusion here that the premium must be justified. The market seems to believe the current premium to the stock, which as of this morning is over 45-50x P/E normalized, is justified.

I do not believe this to be the case.

Novo Nordisk is expected to generate significant growth for the future as well – however, if I owned shares in this business today, I would consider them candidates for profit rotation.

Why is that?

That’s what we’ll look at in this article, where we will try to establish a likely 2024E target, and I have conviction my thesis will perform better than the thesis I established last year.

Novo Nordisk – A Crazy 2023

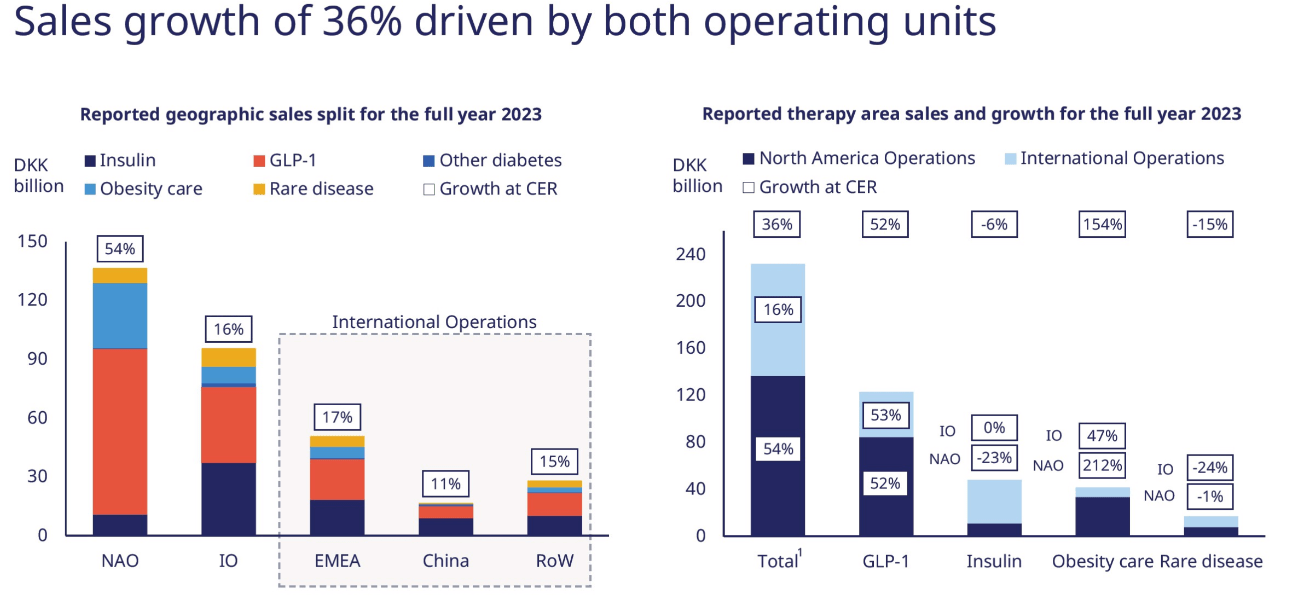

A crazy 2023 such as this one does not come without reason – and Novo Nordisk certainly has reason for such outperformance. The company saw a clear increase – and that’s an understatement, in Obesity care sales, of 154% at CER. This drove sales to 41.6B DKK in this segment alone. This also was the main reason for significant company-wide sales growth of 36% as well as a full-year operating profit growth of 44%. The company also reported full-year free cash flow of almost 69B DK.

The company reported growth from both sales units, but you can see in the specifics, that much of the growth came from the obesity care, and specifically Wegovy/Ozempic.

Novo Nordisk IR (Novo Nordisk IR)

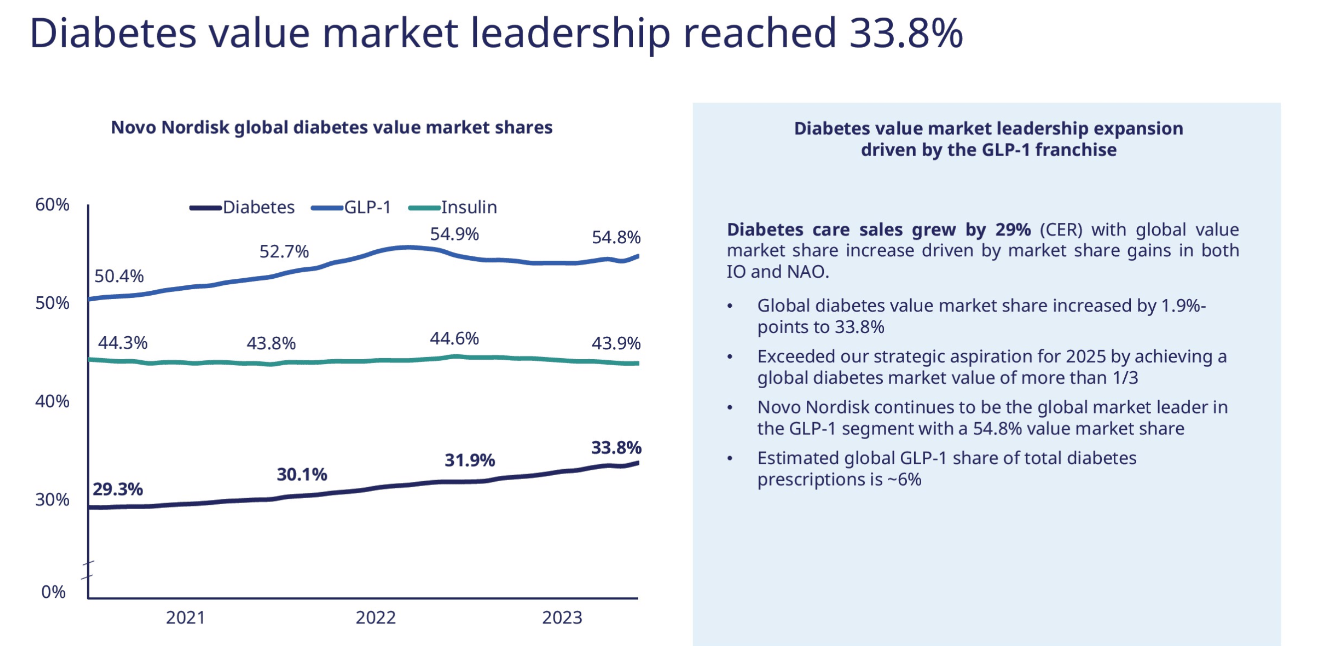

This sales increase also moved the company further up to a market leadership position of almost 34% of the entire market, which is a 1.9% increase. This exceeded the company’s own already optimistic estimates because Novo Nordisk now has over 1/3 of the global diabetes market.

Investors who held onto this stock and the shares are to be commended and lauded for their patience – I am unsure if I could have done the same in this environment.

And the obvious question here becomes – is this in any way a repeatable performance for Novo Nordisk?

Novo Nordisk IR (Novo Nordisk IR)

The main geographic driver behind that 154% increase was the US – not outside of the US.

Outside of Semaglutide, the company’s other segment performances were quite lackluster. Take the rare diseases segment, which saw a sales decline of 15% mainly in the international operations, due to inventory and manufacturing. This is likely to revert going forward.

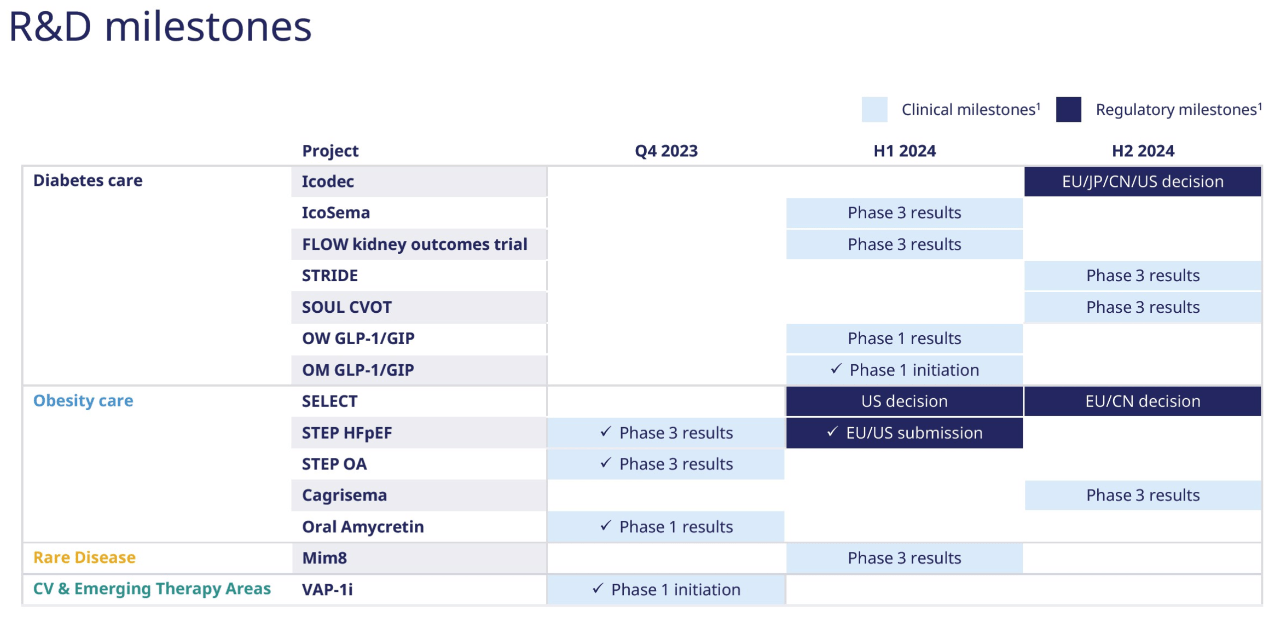

The focus, as I see it now, is for the company to try and maintain high levels of sales for its now-incredibly popular medications, while at the same time pushing R&D and its current pipeline, which currently looks like this.

Novo Nordisk IR (Novo Nordisk IR)

Novo Nordisk is moving into a heavy CapEx period, where the company seems likely to invest significantly in order to expand its manufacturing base. Amounts in excess of 45B DKK are being discussed, which are massive expansions for this company and expected to be in the low double digits of sales for the coming years. This is a significant percentage for a company that before this averaged no more than 6-9% of sales – and the question becomes if the company’s sales can keep supporting this. I think, given the popularity of the products, it’s entirely possible.

Novo Nordisk also has a very attractive capital allocation program, with a significant dividend increase of almost 52% to reflect the superb results, but also significant cash to be spent on buybacks. The company also expects to initiate another share buyback program worth 20B DKK. I view this as the wrong choice given that the company is buying their own shares at over 40x P/E, but this is something that companies other than Novo Nordisk have also done before.

Let me be clear. Not even the most optimistic Novo Nordisk estimates expect a repeat of 2023E. The company is expected, based on its own numbers, to grow its sales at 18-26% at CER, and negative 1% as reported, with reported operating profit growth around 2% lower YoY, but still managing over 60B DKK worth of FCF.

If the company manages this, the valuation might be justifiable, if they can maintain and grow on this. For certain, I do need to and will adjust my price target for the company.

However, it would be wrong to say that there aren’t risks. There obviously are, otherwise, I wouldn’t be on a “HOLD” for this company, without any intention of changing this here.

First off, am I the only analyst with this stance?

No, certainly not. My own share price/FV estimate is echoed by many analysts and services. Morningstar, as of today, has a 540 DKK FV to the company, which is close to 50% of the current share price.

Why is this the case? What are we analysts, who are more bearish on the stock, seeing that others may be “missing”?

Because obviously, let’s be clear about the upside – Wegovy is significantly expanding obesity for Novo Nordisk. It’s a very efficient and key drug and product, and I expect it to be a core for a long time to come. Novo Nordisk also has a very solid core portfolio of GLP-1 products, such as both Rybelsus and Ozempic, both of which are good products in their own right, and even injectable. The company, with its new 1/3 market share of the market, is more than prepared to give battle here and defend its overall market share.

No doubt about this.

However, the risks – they exist, and are worth considering.

Operational Risks For Novo Nordisk

The obvious risk is valuation – we’ll cover this later. Let’s look at the operational risks specifically, which I am assuming that most people interested in Novo Nordisk want to hear.

First off, Wegovy has competition. Eli Lilly (LLY) is coming out with Zepbound which is launching in 2024E. I expect the launch alone to come at the cost of the share price level for Novo Nordisk. Also, Wegovy’s launch wasn’t the best due to constraints in supply and manufacturing, giving other players like LLY the opportunity to prepare in a superior way in terms of launch.

Also, Zepbound is likely a more effective drug than Wegovy, insofar as weight loss and reductions in blood sugar (Source).

There are ups and downsides to both of these, but the simple fact that there is competition incoming will serve as a dampener on this company’s share price, as I see it.

What else? The company’s insulin products are, as I’ve mentioned in past articles on NVO; under pressure from biosimilar products, from players like (again) LLY and Sanofi (SNY). Once you dig into the medical specifics, it becomes clear that LLY and NVO are duking this one out, with LLY’s new oral GLP-1 Mounjaro being a direct competitor to Rybelsus.

In short, the upside and clarity aren’t as clear as I would like it to be for a company that demands this sort of valuation premium.

And with that, I want to show you what exactly this would mean for the company going forward – but keep in mind these numbers are not yet updated for today’s move by the company.

NVO Stock – The Valuation Is Now Excessive

I say with clarity that this valuation is absolutely excessive. With the company’s move today, we’re over 900 DKK. My last article was in January, a little less than a year ago from now, of 2023.

I gave the company what I considered to be a very generous share price target, given where it was going, at 720 DKK, and expected it to normalize closer to the 25x P/E, at which point I could be buying this great business.

Obviously, that did not happen.

Instead, we find ourselves at over 45x P/E for an AA-rated, less than 1.5% yielding medical/pharma company. Yes, the growth expectations are excessive, in excess of 15-20% per year at least for the next 2 years, if S&P Global analysts are to be believed (Source: S&P Global).

But I don’t believe this.

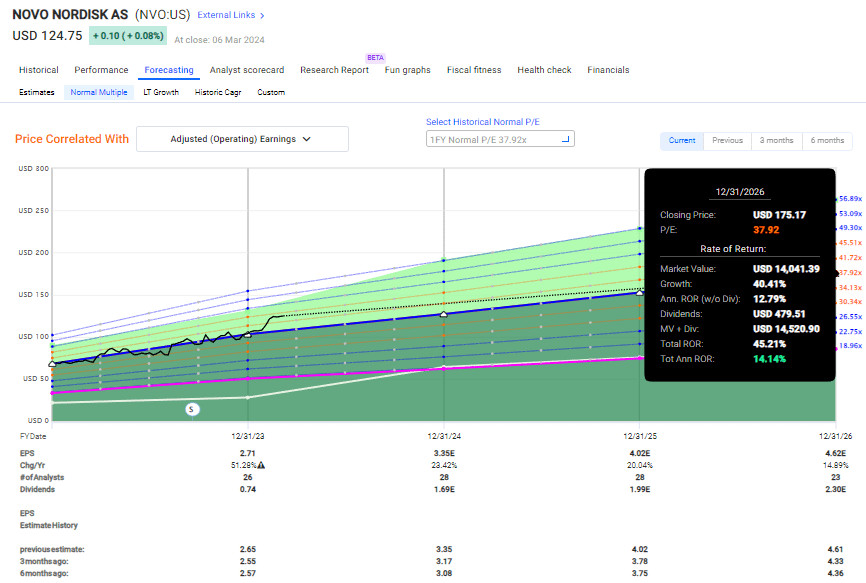

Novo Nordisk has never traded this high. It’s at an EPS yield of less than 2.5%, which means that you’re paying what I consider to be an absolutely irrational premium for an admittedly great business.

In order for this investment to generate positive returns for you, you’ll have to abandon even the idea of value investing in my view. At the 20-year normalized P/E of 24x, the company is likely to generate a negative annualized RoR of around 2.5%. let’s assume you go as short-term to valuation as you possibly can, and forecast at 38x P/E. That’s a 14% RoR in a company that has never traded this high in its lifespan.

Novo Nordisk Upside (F.A.S.T. Graphs)

Peer comparisons show both LLY and NVO riding high currently – but Novo definitely rides higher.

On the operational side, I consider the growing reliance that the company has on GLP-1 to add substantial volatility to the company’s continuing cash flow. That’s especially considering that the company, while international, is seeing a 50% sales reliance on the US market, which in addition to volatility, exposes it to US policy changes. Not an ideal situation. The company’s asset base, drugs, and products have high exposure also to Medicare changes – there is obviously talk for these negotiations to begin in the next few years, but such inclusion would obviously come with pricing changes.

On the valuation side, I consider both peer comparisons and historical comparisons to be insufficient to justify this massive premium for the company. Because of the high reliance on the US, and other valuation risk factors as shown above, I do not view the company as investable. This should not be equated to Novo Nordisk not being a good company, because it is.

I’m just saying it’s not worth close to 4T DKK.

S&P Global targets for this business are higher than most others. 25 analysts give this company a target of 140 DKK to 1000 DKK. Realize that this is the highest target variance I have ever seen. The average PT for the company is 810, so fairly close to this and higher than my previous PT, but I would remind you that the same 25 analysts gave the company an average of 440 DKK less than a year ago.

So I believe there is plenty of exuberance built into this.

I am not an exuberant investor. I maintain my view that Novo Nordisk is worth a premium, and I am willing to bump this premium to 27-28x P/E given the strength of its GLP-1 and related businesses, as well as a strong pipeline. Novo Nordisk is also an exemplary capital allocator, perhaps with the exception of the recent buyback decision, which I strongly disagree with.

Beyond that, here is my thesis for the company for 2024E.

Thesis

- Novo Nordisk is a great business that can really be bought into virtually any long-term investor’s portfolio. However, the company’s specifics dictate that you should be careful about NVO and when to buy it.

- I believe Novo Nordisk will come down from its lofty heights, and normalize closer to 27-28x P/E, at which point valuation investors, such as myself and yourself, potentially can pick it up if our portfolio allows for it.

- My target for the company is no more than 750 DKK here – so still an overvaluation in the double digits. I’m not changing my stance here, but I am upping my PT for the company.

Remember, I’m all about:

-

Buying undervalued – even if that undervaluation is slight, and not mind-numbingly massive – companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

-

If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

-

If the company doesn’t go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

-

I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them.

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

Novo Nordisk does not fulfill any of my valuation-specific criteria, and therefore cannot be anything except a “HOLD” here.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")