If you’ve held Uber Technologies (UBER -0.57%) shares for any meaningful length of time since the beginning of last year, congratulations! You’ve almost certainly made good money on your trade. Uber stock is up more than 200% since the end of 2022. As you might imagine, however, the big run-up looks like it’s running out of steam. A handful of investors even seem to be anticipating a profit-taking pullback.

That doesn’t mean you’ve missed out on the advent of ride-hailing, though. You’ll just want to plug into it with a different name that’s not nearly as overheated and overpriced. That name is Grab Holdings (GRAB 0.32%).

Grab Holdings — the Uber of Southeast Asia

Don’t sweat it if you’ve never heard of Grab. Plenty of investors haven’t. Not only is its $12 billion market capitalization anything but head-turning, but the Singapore-based company’s service is limited to southeast Asian markets.

Still, just as they do in the western hemisphere, consumers in and all around Singapore value convenience and time-saving services. Just like Uber, Grab offers people an on-demand means of getting from one place to another, as well as quick deliveries of restaurants’ online orders. It’s even easing into non-food deliveries from conventional retailers.

Not-quite-like Uber, though, Grab also offers a variety of financial services. Online payments are part of this mix (for obvious reasons of convenience), but insurance and investing are also part of the company’s repertoire. That’s why the company now refers to its app as the “everyday everything app.”

Perhaps Grab’s top distinguishing factor, however, is its deep use of artificial intelligence. From content creation to driver management to language translation to predictive product and service suggestions, Grab’s $250 million worth of AI investments in 2019 and 2020 are making a difference — a big one.

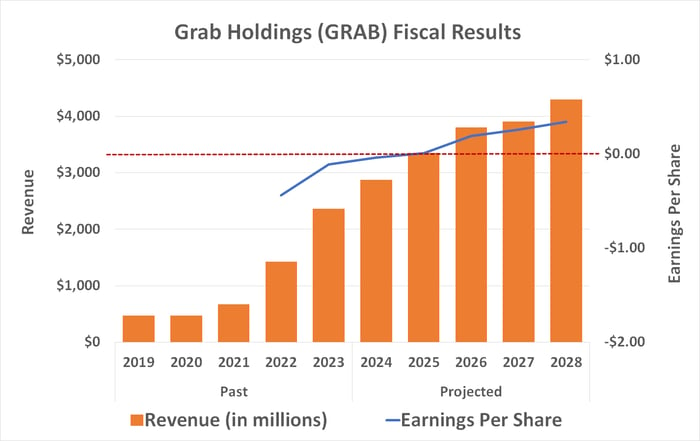

The company finally broke even in the second quarter of last year and has continued to make profit progress in the meantime. Its fourth-quarter revenue growth of 30%, to $653 million, not only led to a record-breaking profit of $11 million but preceded bullish guidance for the fiscal year now underway. The company is calling for a 2024 top line of between $2.7 billion and $2.75 billion, which is 14% to 17% better than 2023’s sales.

The kicker: With its Q4 report, Grab Holdings also announced a stock-repurchase authorization of up to $500 million.

The bullish argument investors aren’t seeing

Curiously, the strong quarterly report and news of the stock buyback didn’t help the stock. Shares actually fell quite a bit that day late last month. Why? As strong as Grab’s full-year guidance was, the market was looking for more. Consensus estimates put the ride-hailing and delivery company’s 2024 sales at $2.8 billion. Anything less, and the company’s growth rate is mathematically slowing down.

The market’s glass-half-empty perspective ignores a handful of important details, though. The first of these details is simply that it’s difficult to maintain historic growth rates. As a company grows, the comparisons to ever-rising historical results become tougher. Grab has already been around for 12 years. It’s mature, as are many of its core markets. Competition is maturing as well. Top-line growth of between 14% and 17% now is actually rather healthy.

Another crucial detail many investors appear to be ignoring is the company’s earnings before interest, taxes, depreciation, and amortization (EBITDA) guidance versus expectations. Grab’s adjusted EBITDA outlook of between $180 million and $200 million is far better than the 2024 consensus of $135.2 million. Credit the company’s savvy use of artificial intelligence, mostly.

Finally, Grab stock’s persistent weakness fails to reflect the expected growth of the ride-hailing and delivery market in the ASEAN (Philippines, Malaysia, Thailand, Singapore) region itself. Mordor Intelligence believes this area’s ride-hailing/ride-sharing market is set to grow at an annualized pace of 7.4% through 2029. Meanwhile, Mordor predicts the Asia-Pacific area’s restaurant delivery market is likely to grow by an average of 10.5% per year for the same time frame.

Given the Grab app’s popularity and its leading market share in most of these countries, the company is already better positioned than most to garner more than its fair share of this growth. Its use of AI will only make Grab even more competitive.

Not for everyone, but decidedly for some

It’s not a pick that belongs in every investor’s portfolio. There’s above-average risk here, heightened by difficulties in keeping tabs on a relatively small company that does all of its business overseas. We’ve also seen that the stock doesn’t necessarily respond well to bullish news.

Still, risk-tolerant growth investors may want to put this stock on their watchlist if not in their portfolios. This business model is being proven in the Western Hemisphere and, now, in the east. There’s more market growth in the cards, too.

Data source: StockAnalysis.com. Chart by author.

The stock is also just plain old undervalued. Analysts’ current consensus price target of $4.65 per share is more than 50% above the stock’s present price. And of the 25 analysts keeping tabs on Grab Holdings, 20 of them rate its stock as a strong buy.

If that doesn’t do it for you, this just might: While Uber stock may be too far gone to bother chasing now, one of Grab’s biggest corporate shareholders is — you guessed it — Uber Technologies. Uber previously operated its ride-hailing business in several markets where Grab does business now, in fact, ceding its share there to the company better equipped to manage it. Uber’s remaining stake in Grab speaks volumes about its potential from the perspective of one of the top names (if not the top name) in the business.

Q2 2024 Earnings Call Transcript")