Slaven Vlasic

About the Company

The Cigna Group (NYSE:CI) is comprised of two segments, Cigna Healthcare and Evernorth Health Services (previously Express Scripts). Cigna and Express Scripts merged a few years ago and created a vertically integrated company where Cigna Healthcare is focused on health insurance for individuals, employers, and parts of the government, while the Evernorth piece of the company is a pharmacy benefits manager.

Transactions and their Effects

In recent years, Cigna Group has sold multiple parts of the company to focus on its core business. One example occurred in 2020 when Cigna sold off its group life, accident, and disability insurance to New York Life for more than $6 billion. Additionally, in just the past month, Health Care Service Corporation acquired Cigna’s Medicare business in a deal valued at around $3.3 billion and is expected to close in 2025.

Following up on the most recent divestiture, I think it’s important to investigate why they exited said market. The Medicare Advantage transaction, which has yet to close, is interesting especially considering what was stated by Humana’s (HUM) CEO, Bruce Broussard, during their fourth quarter earnings call, “The Medicare Advantage sector is navigating a complex and dynamic period of change as we are all working through specific regulatory changes, while also absorbing unprecedented increases in medical cost trends.” In the same paragraph, he goes on to state, “The increase in utilization that emerged late in the fourth quarter was a significant deviation from an already elevated level impacting the industry.” Along those same lines, after Cigna sold off the Medicare Advantage portion of their company the CEO stated, “His company still sees Medicare as an attractive market, but that business required a focus and resources that were “disproportionate to their size” within the company’s portfolio.” All in all, both CEOs are not necessarily sounding the alarm, but are shedding light on this area of the market and that it is costing these companies more than it ever has before. Humana apparently has accepted the increased costs, at least in the short term, while Cigna cut ties with the Medicare Advantage program altogether.

Financial Metrics

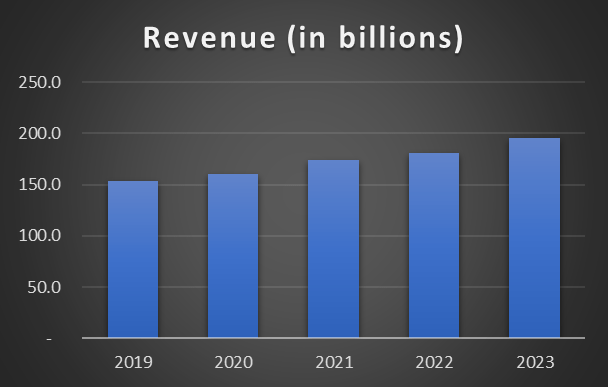

As you can see from the chart below, Cigna has been steadily increasing their revenue over the past five years. The biggest increase was seen from 2020 to 2021 when revenue expanded by about 8.5%. Cigna’s revenue has a compound annual growth rate of a little more than 6% since 2019. In Cigna’s recent 2023 fourth quarter earnings presentation, 2024 revenue guidance was provided, and the company projects revenue will top at least $235 billion in 2024, a more than 20% increase from their 2023 revenue of $196 billion.

Author created, using data from CI annual reports

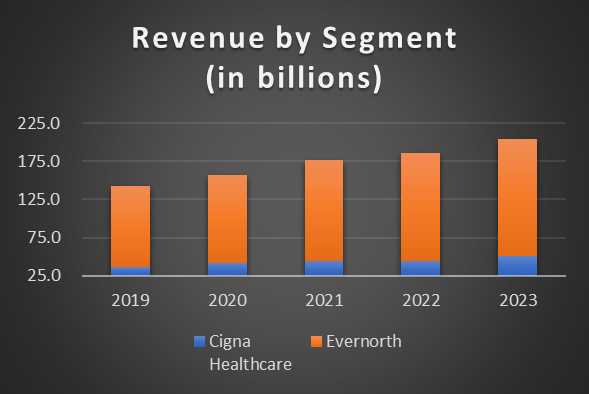

Given that Cigna has more than one segment to the company, I always find it useful to break out the revenue to see if there are any significant trends and to see which areas are growing and at what rate. First, the healthcare portion of the company has grown revenue at a respectable 7.4% annually over the past 5 years, with the largest increase occurring between 2022 and 2023 when revenue increased by almost 14%. On the other hand, the Evernorth part of the company has seen more consistent revenue growth, ranging from 6.3 to 13.4 percent annually since 2019. Further, Evernorth’s revenue has had a compound annual growth rate of almost 10%, a few percentage points better than the Healthcare segment. Overall, it is encouraging to see both segments growing in the high single digits, and I see no reason this pattern should not continue.

Author created, using data from CI annual reports

Cigna has also done a stellar job increasing their earnings per share. Over the past five years, earnings per share have grown at a compound annual growth rate of more than 10 percent, with the highest increase coming between 2021 and 2022 where earnings per share jumped 14.1 percent. Furthermore, Cigna has projected 2024 earnings per share to be at least $28.25 per share, which equates to an increase of more than 12.5%. Lastly, Cigna has been able to grow earnings per share through share repurchases; over the past three years, the company has managed to repurchase on average a net of 6.76% of outstanding shares annually.

Author created, using data from CI annual reports

The last financial metric I’d like to focus on is Cigna’s operating margin, which has struggled over the past five years. In 2019, the company had an operating margin of about 5.25%, it has since dropped to 4.37% in the most recent fiscal year. A company’s ability to increase or at least maintain its operating margin is important, which makes Cigna’s chart below somewhat concerning. This metric is definitely worth keeping an eye on if you are considering a position in Cigna or already hold one.

Author created, using data from CI annual reports

The Dividend

Cigna has only paid a meaningful dividend since March 2021 ($1.00), prior to that, the company paid an annual dividend of just $0.04. Seeking Alpha Quant, rates Cigna’s dividend safety an “A+”, with its payout ratio hovering around 20-25% over the past few years, which is in-line with management’s goal of around 20%. Additionally, Cigna has one of the better forward yields when compared to its peers, at 1.68%. Conversely, UnitedHealth (UNH) has a 1.54% yield, Elevance Health (ELV) sports a 1.31% yield and Humana brings up the rear at just 1.01%. It is probably a little too early in determining whether Cigna will become a dividend growth stock since it only began growing its dividend recently; however, all signs point to that coming to fruition.

Valuation

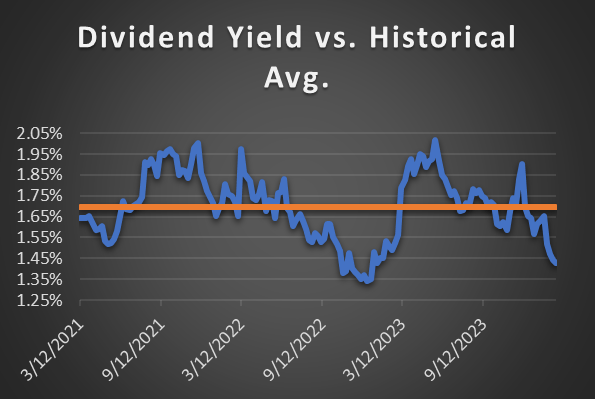

To determine if a stock is possibly over or undervalued, I use two methods. The first is dividend yield theory, which is based on the premise that if the current yield is higher than its historical yield, the company is undervalued, and vice versa if the yield is lower. The other more common method is the price to earnings ratio, which is calculated by dividing the current price by the earnings per share for the prior twelve months. While neither is an exact science, both are a quick way to see if a company is worthy of further research.

As you can see from the chart below, Cigna’s trailing dividend yield is well below its three-year average. Typically, I would prefer to look at at least four years, but as mentioned above, they didn’t pay a significant dividend until 2021. The company’s yield has fluctuated quite a bit over the past few years, briefly topping 2% in late 2021, and it did not reach that number again until mid-2023. On the other hand, its lowest point was around 1.3% and occurred in late 2022.

Author created, using data from Zacks.com

The price to earnings ratio has also fluctuated quite a bit over the past four years when compared to its average. Near the beginning of the timeframe, you can see the company’s p/e ratio was quite low at just above 8 and fluctuated significantly due to the covid effect. However, about a year after it reached that low, the p/e ratio topped 14, marking the second highest point on the chart, it was slightly higher in December 2022. Cigna’s four-year average p/e ratio as of today is 11.81, combined with its trailing twelve-month earnings per share of $25.09 gives it an approximate value of $300, this implies the company is potentially overvalued by about 10% at current levels.

Author created, using data from Zacks.com

Risks

The main areas of concern could really be lumped into one as they both revolve around government policy changes within the healthcare industry. During the previous presidential election cycle universal healthcare was discussed ad nauseum which, if it were to ever occur, could have a significant effect on Cigna’s business and income. I’d almost view universal healthcare as making health insurance companies like a utility, in the sense that it would be heavily regulated with minimal room for material growth in the future. The second risk is the lack of transparency in drug prices, which would affect its Evernorth segment. The Evernorth part of the company negotiates drug prices with manufacturers; however, drug price costs were also under significant scrutiny during the last election cycle as well, for either being too high or just unknown altogether. With the next presidential race almost in full swing, it’s very possible both topics become major points of contention again, especially as the government looks to lower healthcare costs, which would have an obvious detrimental effect on Cigna and its peers.

Final Thoughts

Cigna has already seen a sizeable run up this year, gaining a little more than 12% in the first two months and causing the stock to become slightly overvalued, in my opinion. However, over the past few years, the company has trimmed some of the “fat” and exited out of slower growing markets. I believe this has and will allow the company to focus on the faster growing aspects of its business such as commercial healthcare. Barring any significant government intervention, the company is well positioned financially and should offer solid stock price appreciation and dividend growth for the foreseeable future. I currently rate this company as a hold and if it were to drop closer to $300 I would be a buyer.

Q2 2024 Earnings Call Transcript")