LaylaBird

National Vision Holdings (NASDAQ:EYE) is an optical retailer in the United States. It provides contact lenses and accessory products and also provides eye exams. EYE recently announced Q4 FY23 and FY23 results. I will analyze its results and technical chart in this report. After analyzing all factors, I am assigning a hold rating on EYE.

Financial Analysis

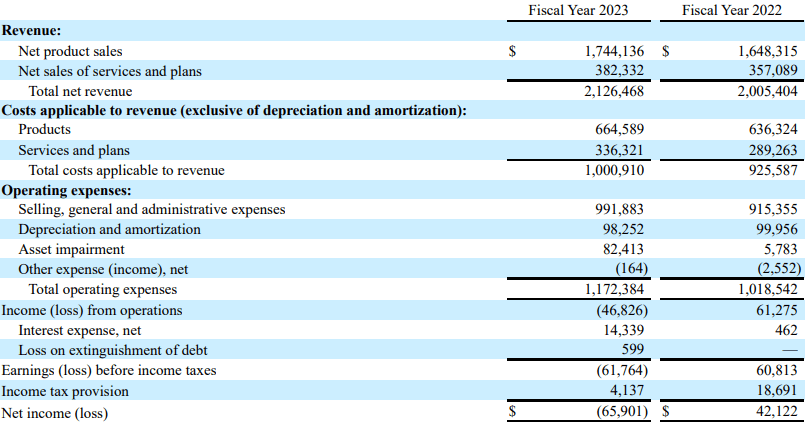

EYE recently posted Q4 FY23 and FY23 results. The total net revenue for FY23 was $2.1 billion, a rise of 6% compared to FY22. The major reason for the rise was strong demand for its AC lens business. Its comparable store sales growth in FY23 was 3.1% compared to FY22, reflecting higher average tickets. Its operating income margin for FY23 was 3.4%, which was 4.3% in FY23. The main reason for the decline was a rise in optometrist-related costs. The net loss for FY23 was $65.9 million compared to an income of $42.1 million. In FY23, it faced an impairment charge of $79.7 million and $7 million related to the termination of the partnership with Walmart.

Seeking Alpha

Now, looking at quarterly numbers. The revenues were up 8% in Q4 FY23 compared to Q4 FY22. The adjusted net loss in Q4 FY23 was $11.1 million, which was $9.3 million in Q4 FY22. Despite the inconsistent purchase cycle due to COVID-19 disruptions, it has been performing well. The revenue growth was positive, and I believe once the purchase cycle becomes consistent, then the revenue growth might get a boost. Additionally, the median age in the U.S. was around 38.9 in 2022. So, the growing age is a tailwind for the company, and the company’s continued focus on store digitalization can also be beneficial going forward. They plan to open around 70 new stores in FY24, most of which will be in America’s Best. Now, looking at margins, although margins were lower in FY23. I believe we might see higher margins in FY24 because of the exit from the low-margin Walmart business, ending the outsourced lab business from China, which will reduce its costs, and converting its 20 stores into America’s Best in order to improve profitability and efficiencies. Hence, the outlook for FY24 looks positive, in my opinion.

Technical Analysis

Trading View

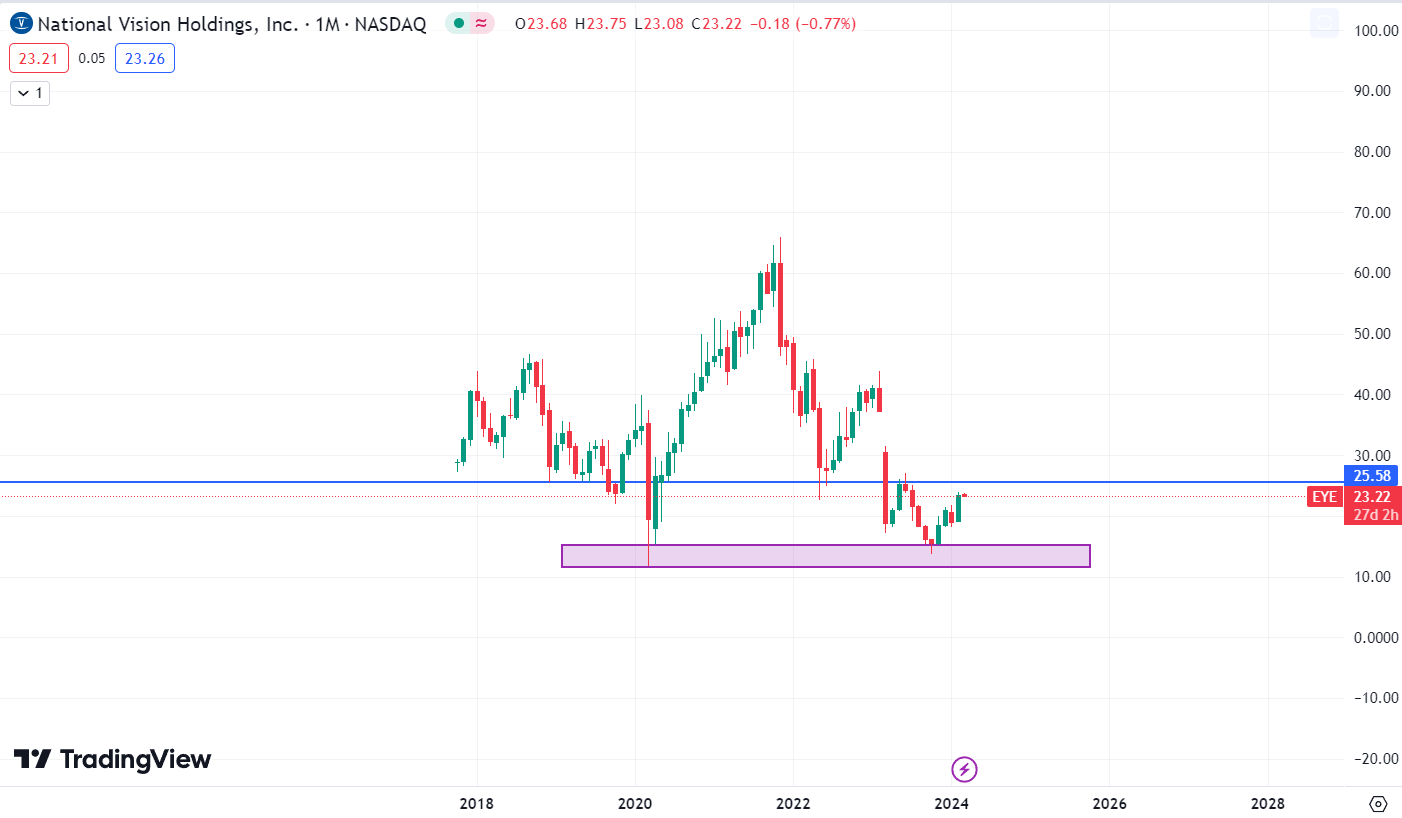

EYE is trading at $23.1. After falling about 50% in 2023, it is recovering in 2024. The stock took support from the same zone that it took in 2020 at the time of the COVID-19 crash. The stock has risen well in the last four months. But I believe one has to be cautious here because the stock is approaching an important level of $25.5. The $25.5 level is a resistance level, and the last time the stock touched it, it fell around 45%. So, the stock price is approaching $25.5, and if it creates a red candle near the resistance level, then the stock might reverse. Hence, buying it at the current level can be risky. In my opinion, one should only consider buying it once it crosses $25.5 and sustains above it for at least two weeks. Only then might we see a reversal in this stock. So until it happens, I would advise to avoid it.

Should One Invest In EYE?

First, look at EYE’s valuation. EYE is trading at an EV / Sales [TTM] ratio of 1.23x, which is lower than the sector median of 1.28x, and is trading at a P/E [FWD] ratio of 39.64x, which is lower than its five-year average of 57.33x. Its valuation looks good, and the expectations of FY24 are also positive, in my opinion. But despite these positives, I am not assigning a buy rating on it because its stock price is nearing an important resistance zone. I believe one should only consider buying once it crosses the $25.5 level because it might give us a confirmation of a trend reversal. Hence, I am assigning a hold rating on EYE for now.

Risk

In the past, their operations of 225 Vision Centers, in particular, Walmart stores until February 2024, 29 Vista Optical locations within particular Fred Meyer stores, and 54 Vista Optical locations on particular military bases have generated revenues and operating cash flows for them. These relationships were established as of December 30, 2023. See “The end of their collaboration with Walmart, including the phase of transition, have a significant impact on their business, and cash flows, which impact could be material.” Their company, financial condition, and operational performance, including the impairment of their intangible assets, could be negatively impacted by the termination or expiration of their host agreements, which might reduce their revenues and operating cash flows. This reduction could be considerable.

Furthermore, losing their Vista Optical locations may make it harder for them to recruit and hire management and retail staff, compete for managed vision care contracts, get advantageous terms from optical vendors like rebates and discounts, and make enough money to pay off debt and fund their operations.

Bottom Line

EYE posted decent results. The margins were down, but I expect it to recover in the coming quarters, and some tailwinds might boost its sales growth. The valuation also looks good. However, its share price is currently heading towards an important resistance level. So, I think one should wait for the breakout. So, I assign a hold rating on EYE.

Q2 2024 Earnings Call Transcript")