Pixelimage

Blackstone Secured Lending (NYSE:BXSL) out-earned its dividend with net investment income in the fourth quarter which in turn led to the BDC reporting a 1% QoQ increase in its net asset value per share.

The BDC’s large floating-rate debt portfolio is still producing top results for Blackstone Secured Lending and BXSL is a rare BDC that I am willing to pay a premium for.

New investment commitments roared higher in 4Q-23 and the BDC has very good credit quality, particularly when compared to the credit trends we have seen for other BDCs this earnings season. Buy.

My Rating History

Re-accelerating inflation rates in the fourth quarter and Blackstone Secured Lending’s large floating-rate loan portfolio culminated in a Buy stock classification in October.

Blackstone Secured Lending continued to surpass its dividend pay-out with net investment income in 4Q-23, which was boosted by higher interest rates.

Given the amount of excess dividend coverage, I anticipate another dividend raise in 2024.

Portfolio And Credit Quality

Two of my passive income BDC holdings have quite seriously disappointed lately: Oaktree Specialty Lending Corporation (OCSL) and FS KKR Capital Corp (FSK), both of which triggered investor stampedes after they disclosed quite substantial upticks in their non-accrual ratios for the most recent quarter.

As such, I have learned that the credit quality trend is now by far the most important metric for passive income investors to follow. Fortunately, Blackstone Secured Lending didn’t disappoint in this regard.

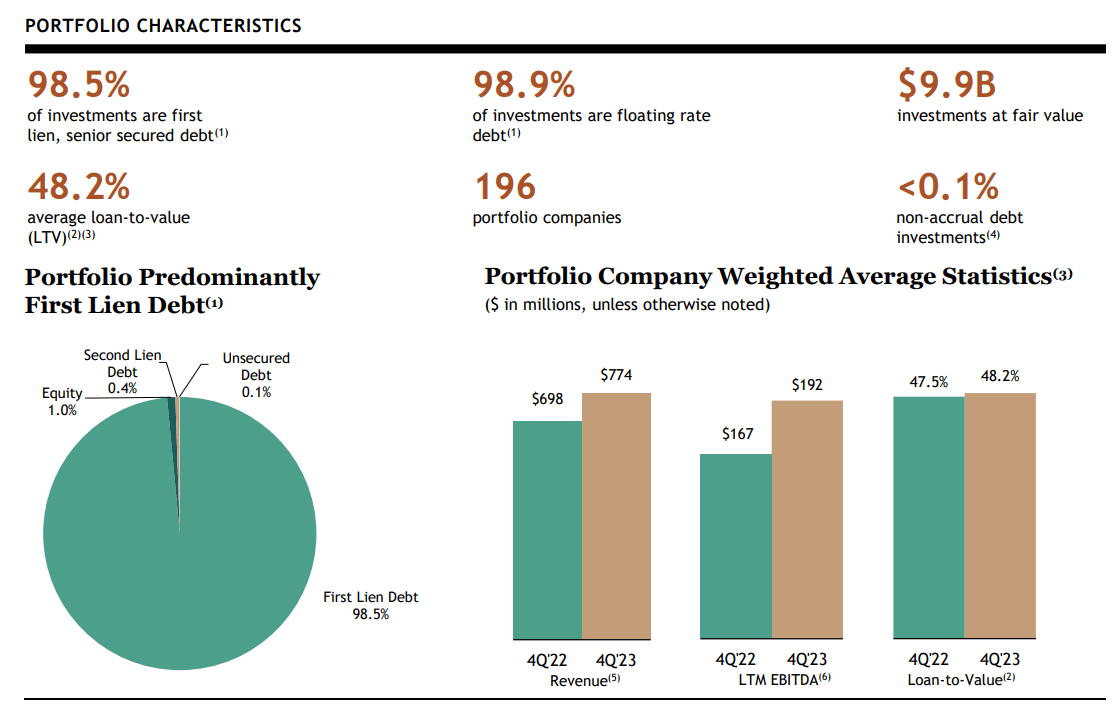

Blackstone Secured Lending is a Senior Secured Debt-focused BDC with considerable exposure to First Liens. As a matter of fact, First Liens accounted for 99% of the BDC’s portfolio investments in 4Q-23 which I think is a distinguishing characteristic for Blackstone Secured Lending.

Most BDCs that I reviewed in the last year tend to incorporate large positions of Equity, Subordinated Debt and Second Liens into their portfolio structures in order to boost their return potential. Since Blackstone Secured Lending doesn’t, the BDC stands out with a more concentrated First Lien-centric investment portfolio.

Portfolio Characteristics (Blackstone Secured Lending)

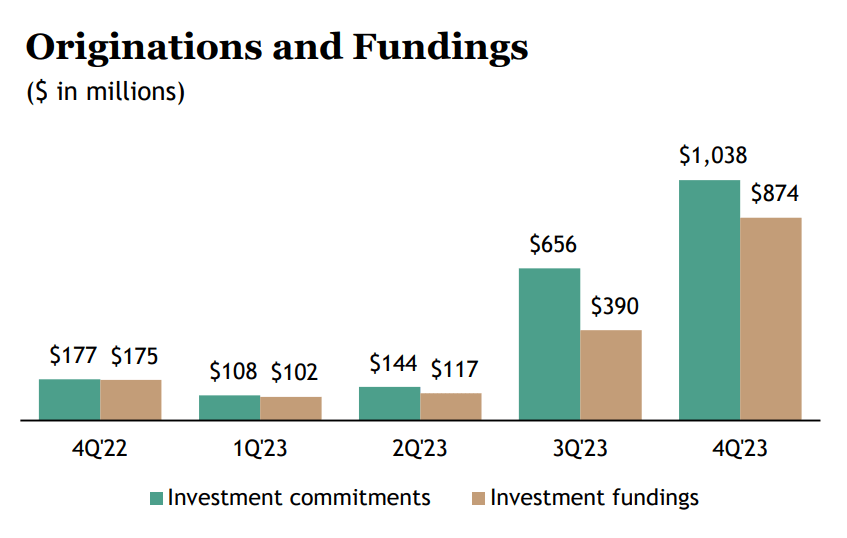

Blackstone Secured Lending’s investment commitments continued to surge in the fourth quarter, extending a trend that started in 3Q-23. Lower expected short-term interest rates, which have weighed on business spending and demand for new loans, are behind the sharp uptick in the company’s investment commitments.

Though repayments also increased, the BDC is seeing robust portfolio growth: Blackstone Secured Lending’s portfolio value as of the end of 4Q-23 was $9.9 billion, reflecting a QoQ increase of 4%.

Originations And Fundings (Blackstone Secured Lending)

As I mentioned in the introduction, credit quality is now where the music is playing, particularly after Oaktree Specialty Lending and FS KKR Capital disappointed in this regard: Oaktree Specialty Lending’s stock sold off after the company reported an idiosyncratic lending performance for its most recent quarter that led to a 4.2% non-accrual ratio. FS KKR Capital did even worse as its non-accrual ratio skyrocketed to 5.5% in 4Q-23.

But Blackstone Secured Lending shone in terms of loan performance in 4Q-23 as the BDC had only one debt investment on non-accrual status in 4Q-23. The BDC now has credit quality that rivals that of Hercules Capital, Inc. (HTGC).

Hercules Capital had perfect credit quality in the last quarter with a non-accrual ratio of 0.0% based on fair value. Blackstone Secured Lending’s non-accrual ratio of 0.1% of debt investments, thus, compares to the best in the field.

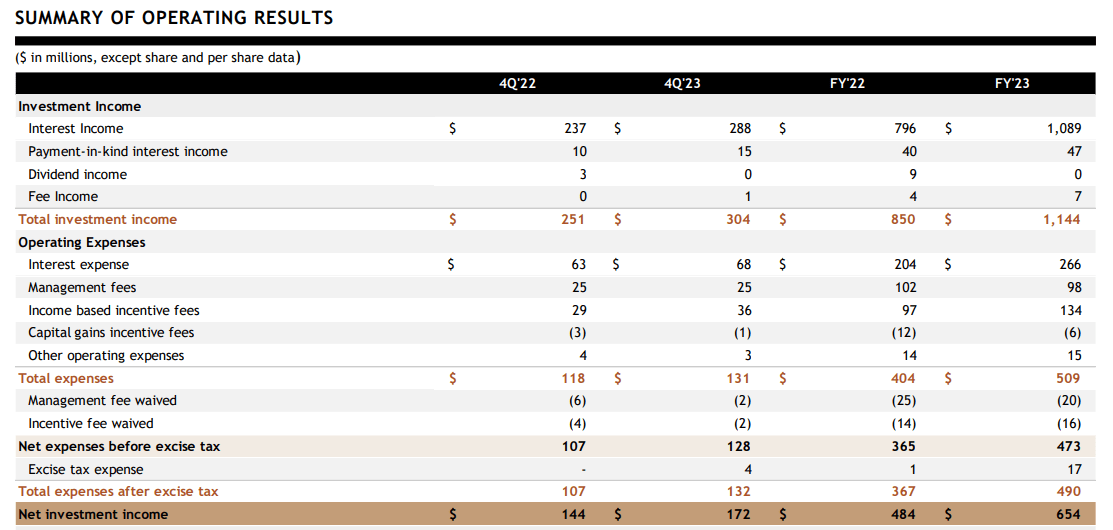

As far as Blackstone Secured Lending’s net investment income performance goes, the BDC, which is 99% floating-rate positioned, was expectantly solid. The BDC earned $288 million in interest income in 4Q-23, up 22% YoY, thanks to the central bank’s rate hikes over the course of the last year. This equated to $172 million in net investment income, up 19% YoY.

Summary Of Operating Results (Blackstone Secured Lending)

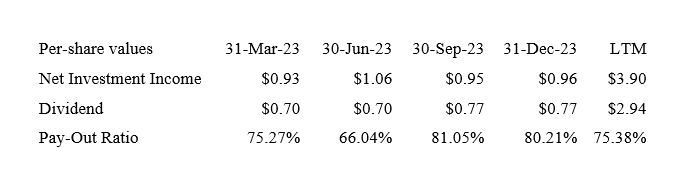

Dividend Coverage Improved QoQ, Solid Margin Of Safety Despite 10% Dividend Raise

Blackstone Secured Lending earned $0.96 per share in net investment income in 4Q-23, up 7% YoY, thanks to the BDC’s bet on higher interest rates that paid off for the BDC big time.

The net investment income tailwind allowed Blackstone Secured Lending to raise its regular dividend by a solid 10% in 3Q-23. The dividend raise explains why despite higher net investment income tied to the BDC’s floating-rate loans the dividend pay-out ratio ticked up to the low-80%-range in the third quarter. BXSL exhibited a 75% pay-out ratio in 2023 which leaves room for more dividend raises in 2024.

Dividend (Author Created Table Using BDC Information)

A Premium That Is Worth Paying

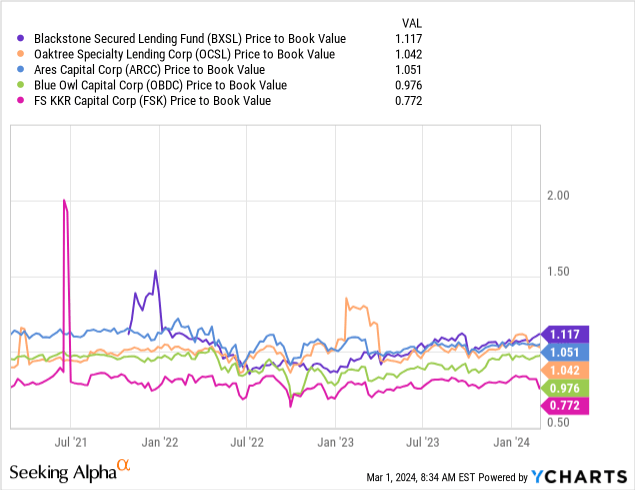

Blackstone Secured Lending rightfully sells at a premium to net asset value. The 11% premium that passive income investors presently must pay to secure a covered 10.4% dividend yield is directly tied to the BDC’s superb credit quality.

Blackstone Secured Lending’s net asset value, with the support of the factors discussed in this article, rose 1% QoQ to $26.66.

I rarely recommend a BDC that is selling at a premium to net asset value, mostly because I like to boost my total return potential through capital gains. In the case of Blackstone Secured Lending, however, I am willing to make an exception due to the BDC’s solid credit quality status and significant excess dividend coverage.

Why Blackstone Secured Lending Might See A Higher Or Lower NAV Multiple

Since the BDC’s credit quality is near-perfect, the key lever for Blackstone Secured Lending to grow its net investment income is the central bank’s rate policy.

Though the bank said that it was considering to lower short-term interest rates in 2024, a hotter-than-expected inflation report for January caused doubts about the central bank’s timeline for rate cuts.

A decline in short-term interest rates, however, would pose a net investment income challenge for Blackstone Secured Lending since it is heavily reliant on floating-rate loans to its portfolio companies.

My Conclusion

Blackstone Secured Lending’s 4Q-23 earnings were quite solid, particularly in the context of other BDCs disappointing greatly with respect to their credit trends.

The BDC covered its $0.77 per share per quarter dividend pay-out with net investment income and Blackstone Secured Lending’s net asset value rose as well, thanks to higher interest income from floating-rate investments.

Blackstone Secured Lending is now selling for an 11% premium to net asset value, a premium that I think is deserved.

Taking into account the BDC’s net investment income trend, strong non-accrual position, and covered 10% yield, I am keeping my stock classification for BXSL at Buy.

Q2 2024 Earnings Call Transcript")