PeopleImages/iStock via Getty Images

We previously covered Digital Realty Trust (NYSE:NYSE:DLR) in December 2023, discussing why we maintained our Buy rating for the stock, thanks to its improved monetization rate and impressive generative AI tailwinds through 2027.

Combined with the announced Data Center partnership with Realty Income (O)/ Blackstone (BX), we believed that DLR remained well capitalized to grow profitably moving forward.

In this article, we shall discuss why DLR’s prudent growth strategy has been misunderstood, with the supposedly underwhelming FY2024 guidance attributed to the diversification of capital resources and eventually, balance sheet management.

With the REIT expected to remain profitable in FY2024, we believe that the recent pullback offers interested investors with the chance to dollar cost average.

The DLR Investment Thesis Remains Attractive, Thanks To The Prudent FY2024 Guidance

For now, DLR has reported a decent FQ4’23 earnings call, with revenues of $1.36B (-2.8% QoQ/ +10.5% YoY), core FFO per share of $1.63 (+0.6% QoQ/ -1.2% YoY), and AFFO per share of $1.30 (-7.1% QoQ/ +0.7% YoY), with FY2023 numbers of $5.47B (+16.6% YoY), $6.59 (-1.6% YoY), and $5.84 (-2.6% YoY), respectively.

At the same time, the REIT reported an excellent same-capital cash NOI growth of +9.9% (+0.5 points QoQ/ +15.7 YoY) by the latest quarter, further underscoring the success of its data center portfolios thus far.

While these numbers appear to be promising, DLR has unfortunately offered an underwhelming FY2024 revenue guidance of $5.6B (+2.3% YoY) and core FFO per share guidance of $6.67 (+1.5% YoY) at the midpoint.

This is compared to the consensus estimates of $5.84B (+6.7% YoY) and $6.83 (+3.9% YoY), respectively, implying a drastic deceleration in the top-line growth from FY2023 levels.

It is apparent that DLR’s risk diversification efforts by giving up partnership interests to others, such as O and BX, have inadvertently resulted in the slower projected growth for the top/ bottom lines, especially since the former only commands 20% stakes in these joint ventures.

However, we maintain our belief that DLR’s partnerships have been very prudent, attributed to the ballooning debt-to-EBITDA-ratio of 7.24x by FQ4’23, compared to 6.78x in FQ3’23, 7.62x in FQ4’22, and 5.59x in FY2019.

This is based on the REIT’s long-term debts of $16.44B (+3.9% QoQ/ inline YoY/ +62.4% from FY2019 levels of $10.12B) and adj EBITDA of $568.75M (-2.7% QoQ/ +4.9% YoY/ +25.4% from FY2019 levels of $1.81B).

When we compare DLR’s leverage ratio compared to the REIT specialty average ratio of 5.81x and its Data Center REIT peers, such as Equinix (EQIX) at 4.60x, Iron Mountain (IRM) at 6.49x, and American Tower (AMT) at 5.09x, it is apparent that the former’s leverage may be temporarily getting out of hand.

Despite the higher fixed interest rate weightage of 85.3% (+4.3 points YoY) and relatively low effective interest rate of 2.89% (+0.38 points YoY), the accelerated debt growth and slower adj EBITDA growth have directly contributed to DLR’s slower bottom line expansions.

For context, the REIT reported a top line expansion at a CAGR of +14.4% between FY2016 and FY2023, with the AFFO per share growth underwhelmingly stagnant at +1.4% and Dividend per share growth at +4.8%, partly attributed to the doubled share count over the same period.

Combined with the reduced capex obligations, we can understand why the DLR management has opted for its recent partnerships, especially since $2.12B of its debts are due through 2025, implying the importance of near-term capital preservation as the management works toward a leverage target of around 5.5x.

If anything, much of the JV projects are expected to come online by 2025, with much of the additional capacity expected to be accretive to its bottom lines then, thanks to the growing backlog and strong pricing power.

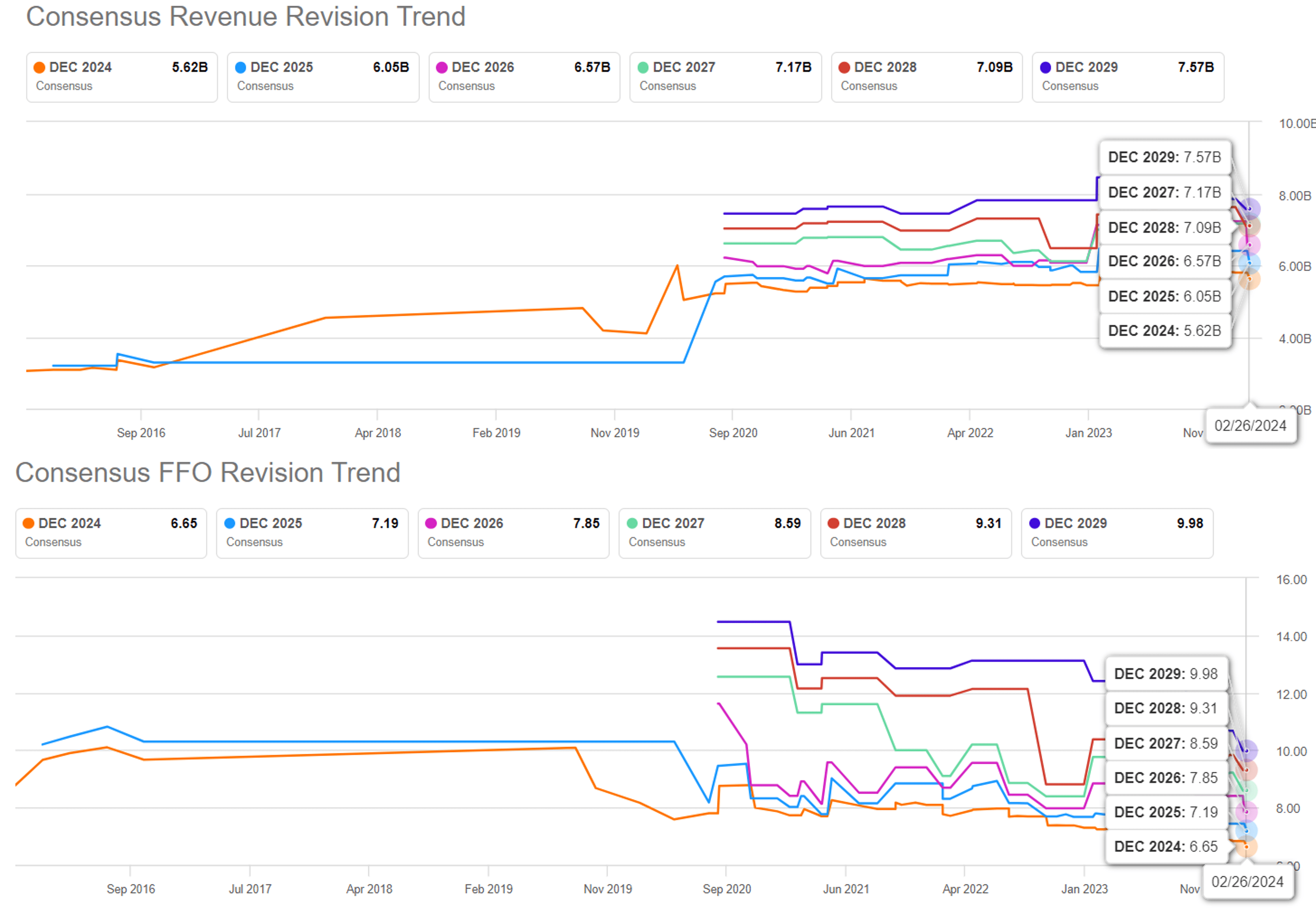

The Consensus Forward Estimates

Seeking Alpha

For now, the same downgrade has also been observed in the consensus forward estimates, with DLR expected to generate a top/ bottom line growth at a CAGR of +6.2%/ +8.4% through FY2026.

This is compared to the previous estimates of +11%/ +11.2%, though still expanded from the historical growth at +14.4%/ -1.4% between FY2016 and FY2026, respectively.

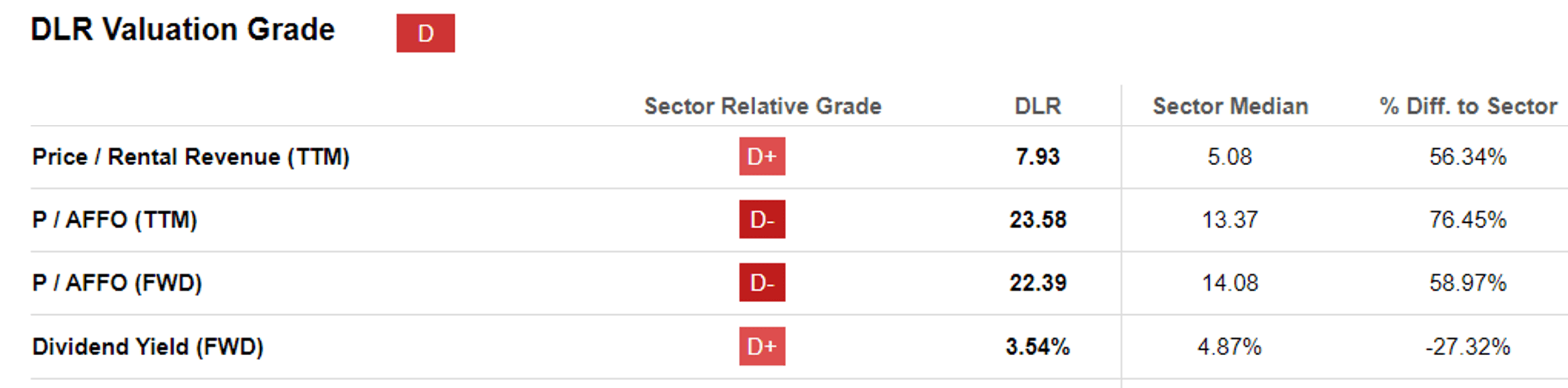

DLR Valuations

Seeking Alpha

Despite so, the DLR stock continues to trade at a relatively reasonable FWD Price/ Rental Revenues valuation of 7.93x and FWD Price/ AFFO per share valuation of 22.39x. This is compared to the 1Y mean of 6.23x/ 18.93x, 3Y pre-pandemic mean of 7.55x/ 19.19x, and sector median of 5.08x/ 14.08x, respectively.

We believe that the growing premium over the REIT sector median is warranted indeed, thanks to the generative AI tailwinds. This is especially since DLR’s valuations are also near its Data Center peers, such as EQIX at 8.38X/ 23.32x, IRM at 3.06x/ 14.80x, and AMT at 8.02x/ 19.30x, respectively.

This is further aided by the fact that DLR’s projected top/ bottom line growth may not pale in comparison to EQIX at +8.9%/ +8.8%, IRM at +9.4%/ +9.8%, and AMT at +4.4%/ +10.5% over the same period of time, while expanded compared to the historical means.

As a result of its decently profitable growth guidance in FY2024, we believe that DLR has been prudent in “diversifying their capital sources through the formation of two new development joint ventures,” since it also directly correlates to the balance sheet’s future improvement.

So, Is DLR Stock A Buy, Sell, or Hold?

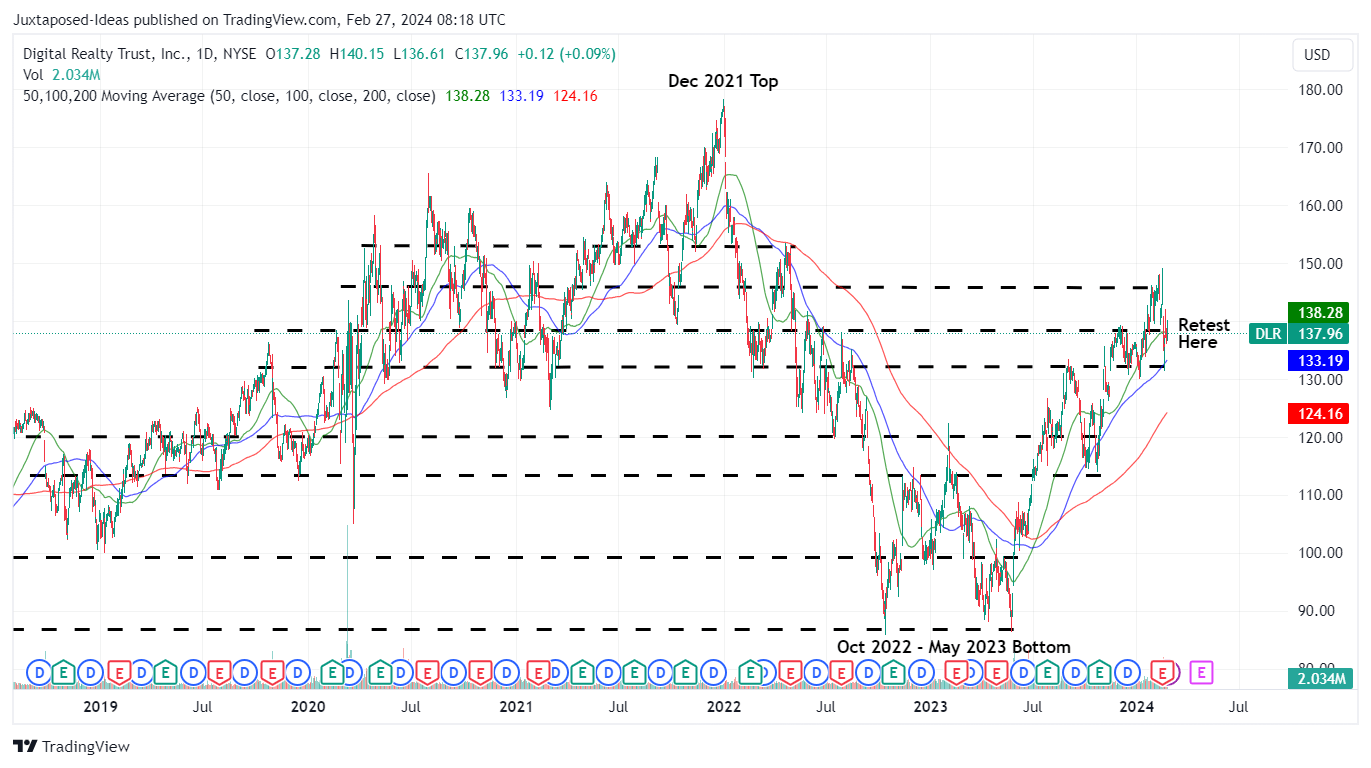

DLR 5Y Stock Price

Trading View

For now, DLR has retraced dramatically after the recent FQ4’23 earnings call, with the stock losing -9.1% of its value at its worst. However, with bullish support also swopping in at $135, it is also apparent that long-term investors are not concerned about the underwhelming forward guidance.

Despite the stagnant dividend payouts since the last hike in March 2022, the data center REIT continues to offer a decent forward dividend yield of 3.54%, in line with its peers, such as EQIX at 1.94%, IRM at 3.45%, and AMT at 3.62%.

Despite the inherent underperformance compared to the overall REIT sector median of 4.87%, we maintain our conviction that DLR remains a more than decent dividend stock.

This is especially aided by the fact that DLR now trades nearer to our fair value estimate of $130.70, based on the FY2023 AFFO per share of $5.84 and the FWD Price/ AFFO of 22.39x, thanks to the recent pullback.

Based on the consensus FY2026 AFFO estimates of $7.43, there seems to be an excellent upside potential of +20.3% to our long-term price target of $166.30 as well.

As a result of its (prospective) dual pronged returns, we maintain our Buy rating for the DLR stock.

Q2 2024 Earnings Call Transcript")