Marvin Samuel Tolentino Pineda

Investment Thesis: I take the view that Bank of Montreal does not have strong growth prospects at this time owing to lack of growth across non-interest revenue, higher provisions for credit losses, as well as a lack of certainty regarding the future interest rate trajectory in Canada. As a result, I continue to rate the stock as a Hold at this time.

In a previous article back in October 2023, I made the argument that Bank of Montreal (NYSE:BMO) had little prospect of upside in the short to medium-term, owing to a continued drop in non-interest revenue, along with modest growth in net interest income.

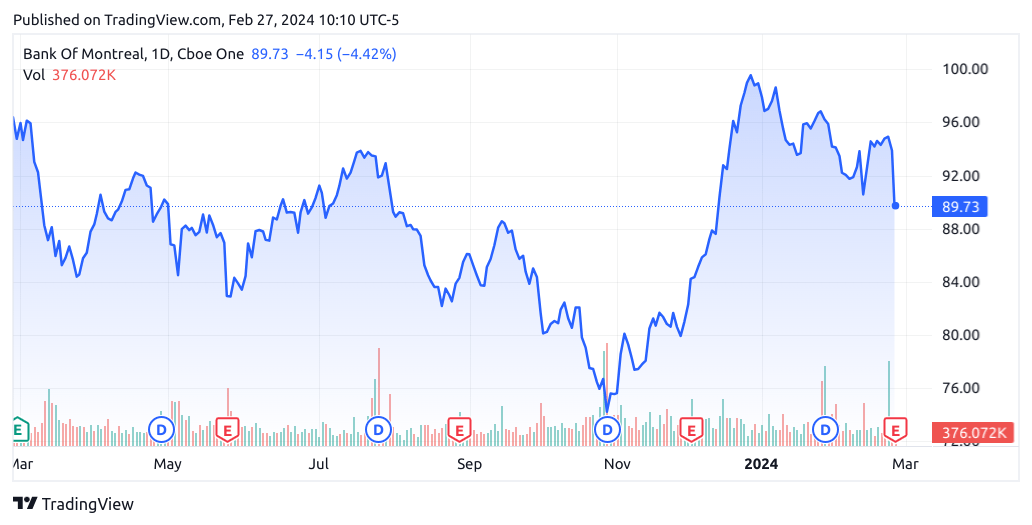

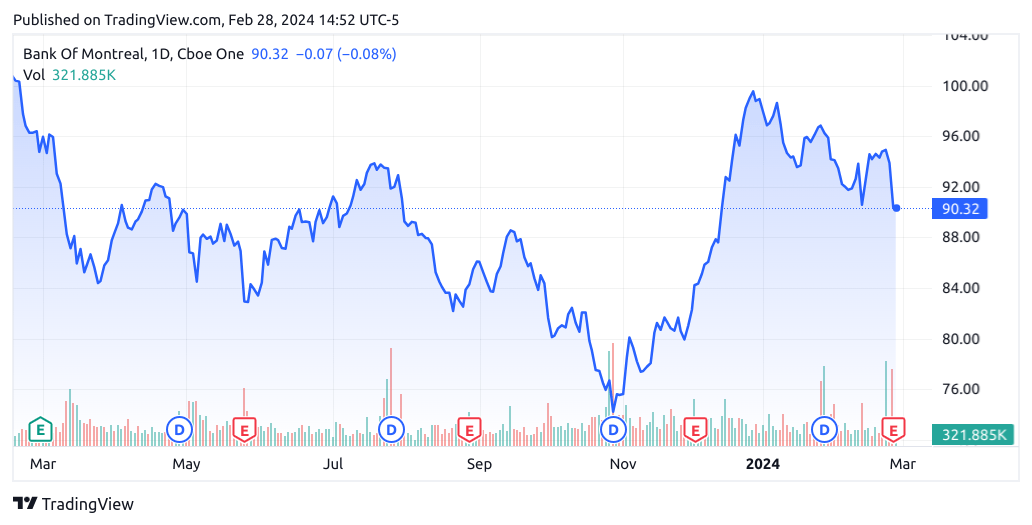

However, the stock has ascended to a price of $89.73 at the time of writing – albeit having seen a sharp drop from $94 upon its earnings release:

TradingView.com

The purpose of this article is to assess whether Bank of Montreal has the capacity to see further growth going forward.

Performance

When looking at the most recent earnings results for Bank of Montreal reported on Feb. 27th, we can see that on an adjusted basis – both net interest income and non-interest revenue have seen strong growth from that of the prior year quarter.

BMO Financial Group Reports First Quarter 2024 Results

However, we see that diluted EPS is down to $2.56 per share in Q1 2024 as compared to $3.06 in the prior year quarter. Analysts had expected diluted EPS to come in at $3.02 for this quarter – with provision for credit losses of $627 million, exceeding analyst expectations of $508 million.

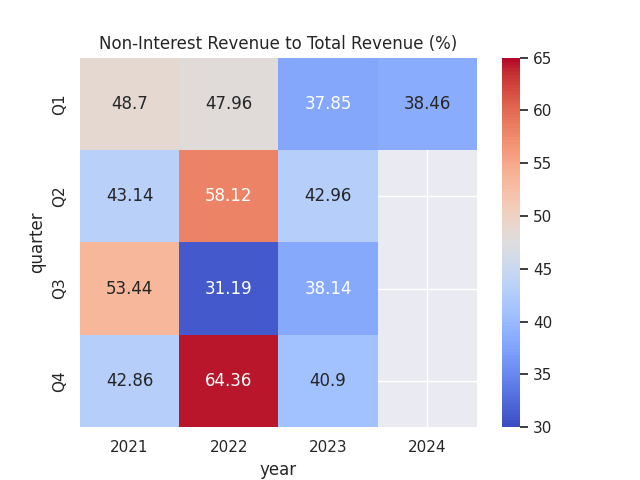

In addition, we can also see that the ratio of non-interest revenue to total revenue has remained at virtually the same level as that of the prior year quarter. Given the revenue growth we have seen from that of last year – this indicates that interest-related revenue has been responsible for a significant portion of overall revenue growth.

Non-interest revenue and revenue figures sourced from historical Bank of Montreal quarterly financial reports. Percentages calculated by author. Heatmap generated by author using Python’s seaborn visualisation library.

My prior reservation regarding Bank of Montreal was that the bank would have to set aside further provisions across both performing and impaired loans – and an increase in provision for credit losses could hinder growth going forward. We have seen this to be the case on the basis of recent results.

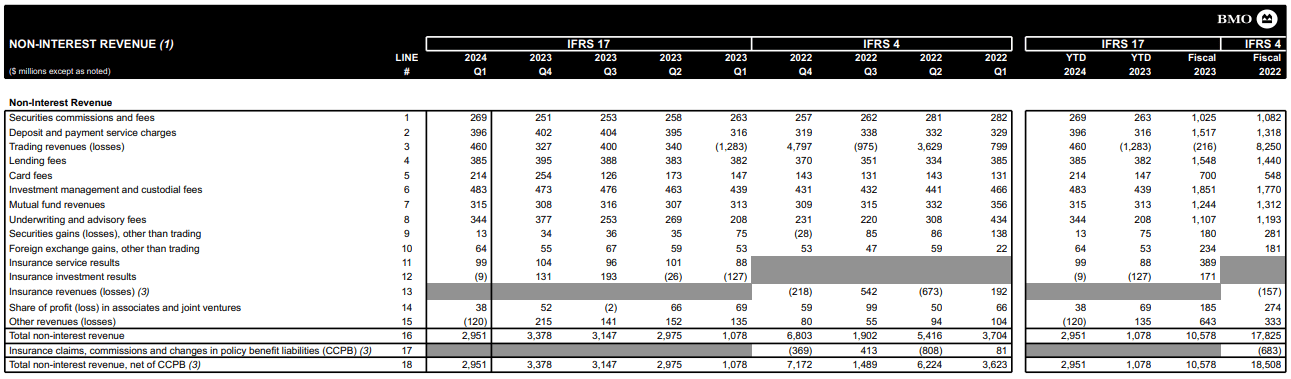

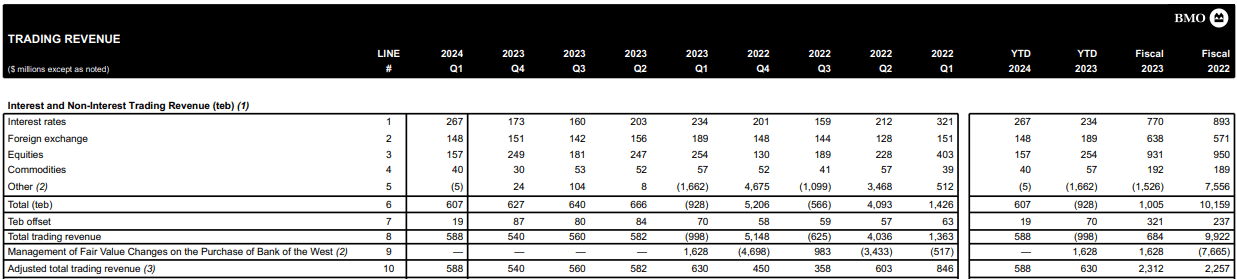

When looking at Bank of Montreal’s Supplementary Financial Information for this quarter ended, we see that while trading revenues are still lower than that of the $799 million seen in Q1 2022 – this quarter saw a rebound to $460 million in trading revenues, which was up sharply from a loss of -$1.283 billion in the prior year quarter.

BMO Financial Group: Supplementary Financial Information For The Quarter Ended January 31, 2024

However, this comes with a caveat. We see that when taking a deeper look at the breakdown in trading revenues, revenues across the segment for Other non-interest trading revenue, the sharp reversal from a loss of -$1.662 billion in Q1 2023 was related to fair value changes on the purchase of Bank of the West.

BMO Financial Group: Supplementary Financial Information For The Quarter Ended January 31, 2024

When examining further, we see that while interest-related trading revenue is up by 14% from the prior year quarter, revenues across the foreign exchange, equities and commodities have seen a drop over the same period.

In this regard, while the growth in interest-related trading revenue has remained encouraging – we have seen that non-interest segments have still come under pressure.

Balance Sheet

From a balance sheet standpoint, it is notable that in spite of rising interest rates – loan demand has continued to see growth – with a deposits to loans ratio of 1.41 as compared to 1.46 in Q1 2022.

| Quarter | Average deposits | Average gross loans and acceptances | Deposits to loans ratio |

| Q1 2022 | 720713 | 493895 | 1.46 |

| Q2 2022 | 707601 | 506082 | 1.40 |

| Q3 2022 | 725678 | 526150 | 1.38 |

| Q4 2022 | 763709 | 556295 | 1.37 |

| Q1 2023 | 792530 | 565953 | 1.40 |

| Q2 2023 | 883303 | 646873 | 1.37 |

| Q3 2023 | 884254 | 644672 | 1.37 |

| Q4 2023 | 905480 | 657020 | 1.38 |

| Q1 2024 | 922069 | 654957 | 1.41 |

Source: Figures sourced from Bank of Montreal Supplementary Financial Information For The Quarter Ended January 31, 2024. Deposits to loans ratio calculated by author.

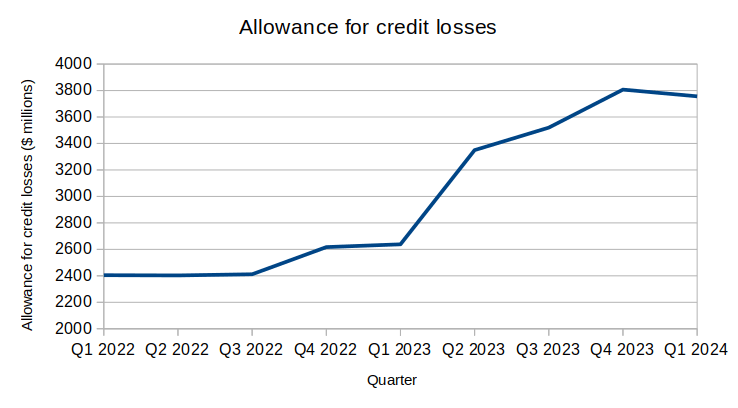

However, we have also seen that the bank has had to set aside a higher allowance for credit losses over this period – to account for the heightened risk that a greater proportion of consumers will not be able to afford to pay back these loans due to higher interest rates.

Figures sourced from Bank of Montreal Supplementary Financial Information For The Quarter Ended January 31, 2024. Graph generated by author.

As a result, we have seen a sharp increase in allowance for credit losses over the past year, which has contributed to the drop in earnings that we have been seeing for the bank. In this regard, while growth in loans has been continuing in spite of higher rates – higher allowances for credit losses have impacted the degree to which the bank can grow earnings as a result.

My Perspective and Looking Forward

As regards my take on the above results and the implications for the growth trajectory of the stock going forward, I do not see any developments that would change my view on Bank of Montreal at this time. Non-interest revenue has remained under pressure due to a decline in non-interest trading revenues, and provision for credit losses have concurrently seen an increase, which creates further uncertainty as to future growth prospects.

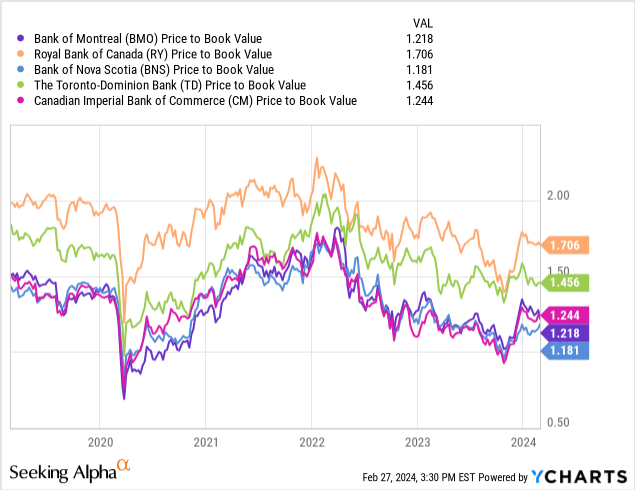

In addition, I had previously made the argument that one of the bullish signals for Bank of Montreal was the fact that at the time, the bank had been trading at the lowest price to book ratio among its peers and had demonstrated the highest return on equity.

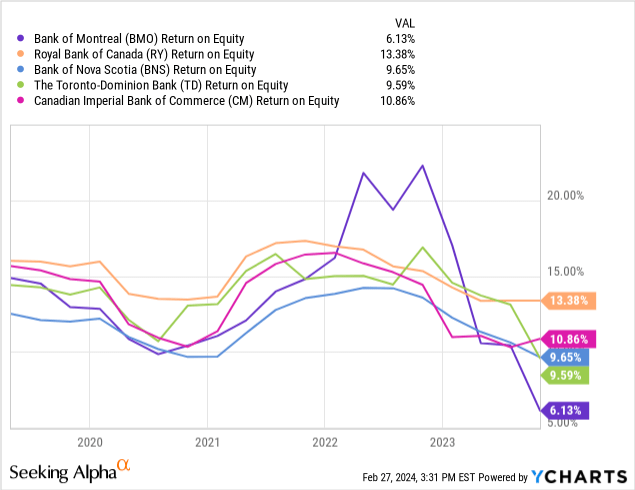

However, we see that the Bank of Nova Scotia (BNS) now trades at a lower price to book ratio than that of the Bank of Montreal, and return on equity for Bank of Montreal has nose-dived to 6.13% at the time of writing – giving it the lowest return on equity among its peers.

Price to Book

ycharts.com

Return on Equity

ycharts.com

For return on equity in particular, higher provision for credit losses have had the impact of reducing net income – and this has in turn reduced return on equity (net income/shareholder’s equity).

In this regard, I do not take a bullish view on Bank of Montreal given both a strong decline in return on equity, as well as a continued decline in non-interest related trading revenues.

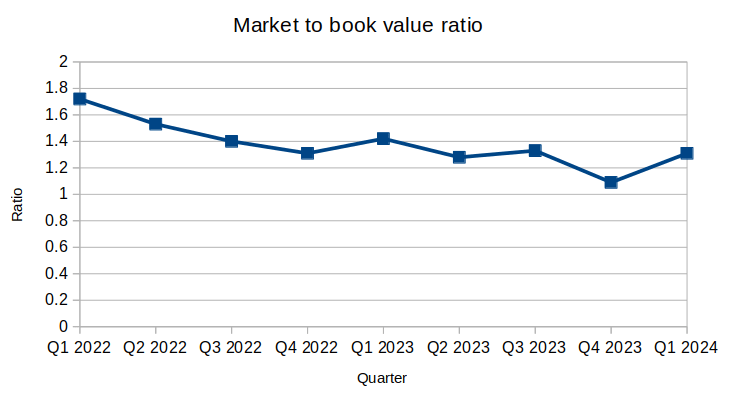

Here is an overview of Bank of Montreal’s market to book ratio on a quarterly basis:

Figures sourced from Bank of Montreal Supplementary Financial Information For The Quarter Ended January 31, 2024. Graph generated by author.

We see that the bank is trading at an almost identical market to book value ratio (1.31x) as in Q3 2023 (1.33x). When looking at a price chart, we can see that the stock was also trading within the $82-94 price range between June and August.

TradingView.com

In this regard, while the stock had previously been trading just shy of the $100 range at the end of last year – I take the view that the subsequent reversion back to $90 marks a better representation of fair value given that the market to book value ratio is back to trading at a similar level as that seen for the first three quarters of 2023. In this regard, I take the view that a range of $82-94 represents fair value for the stock at this time.

We have seen that a significant reason for a rise in provision for credit losses has been growth in interest rates. While the latter has allowed for a rise in net interest income – it has also increased the risk of bad loans, hence the bank must hold a larger financial buffer against such risk.

At this point in time, uncertainty looms in the Canadian market as to how long interest rates will remain elevated. Moreover, it is likely that potential homebuyers may choose to delay securing a mortgage until the trajectory surrounding rates becomes more clear. In particular, Bank of Montreal is now choosing to reduce its exposure to ultra-long mortgages in Canada.

While the original purpose of extending mortgages with amortization periods in excess of 30 years was to ease the monthly payment burden for customers due to higher rates – a reduction in exposure to such mortgages illustrate that the same are not financially viable for the bank in the longer-term.

Conclusion

Overall, my view is that the lack of growth across non-interest revenue, higher provisions for credit losses, as well as a lack of certainty regarding the future interest rate trajectory in Canada indicate that future growth prospects for the stock do not look strong at this time.

In this regard, while I take the view that the stock is trading in its fair value range and does not have too great a risk of further downside at this time, I do not envisage significant growth in the stock until such time that we see a significant reduction in provision for credit losses and the interest rate trajectory across the Canadian market as a whole becomes more clear. I continue to rate the stock as a Hold at this time.

Q2 2024 Earnings Call Transcript")