Vladimirovic

Note:

I have covered Helix Energy Solutions Group, Inc. (NYSE:HLX) previously, so investors should view this as an update to my earlier coverage of the company.

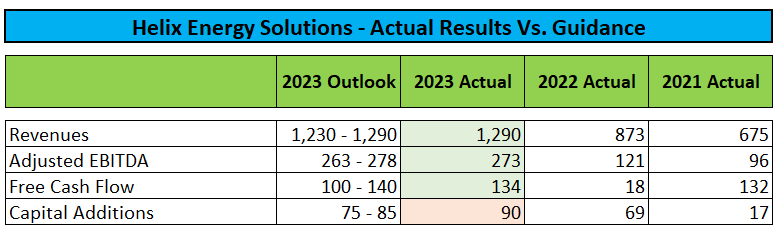

After the close of Tuesday’s session, leading offshore energy specialty services provider Helix Energy Solutions Group, Inc., or “Helix,” reported fourth quarter and full year 2023 results mostly within the ranges provided by management in the Q3 presentation:

Company Presentations

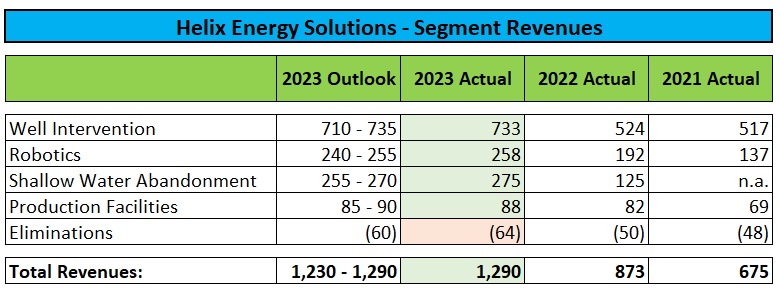

In fact, each of the company’s three major service segments (Well Intervention, Robotics and Shallow Water Abandonment) performed at or above the high end of guidance:

Company Presentations

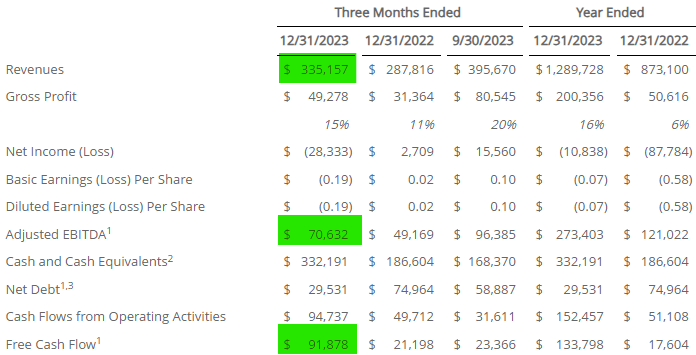

Adjusted for one-time charges, both Q4 revenues and profitability came in ahead of analyst expectations. In addition, the company generated almost $92 million in free cash flow, the highest level in more than a decade.

Company Press Release

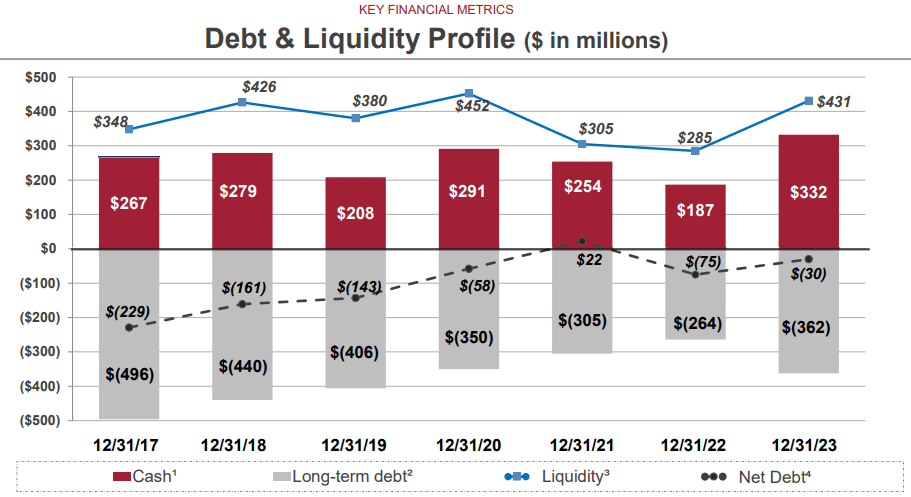

Helix finished the year with liquidity of $431 million, $332 million in cash and cash equivalents and just $30 million in net debt:

Company Presentation

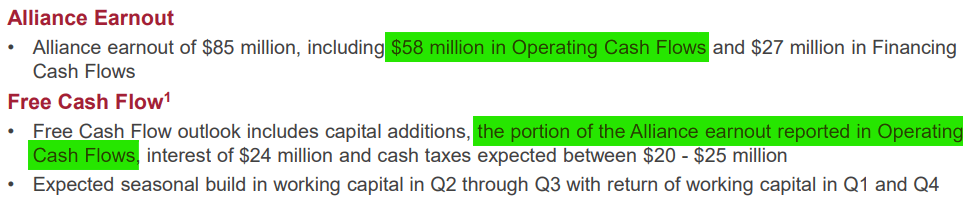

However, the company’s cash position is expected to take a temporary hit in the first half due to an $85 million earnout payment related to the acquisition of the Helix Alliance shallow water abandonment operations in 2022.

Moreover, the company expects to use an additional $40 million to redeem the remainder of its 6.75% convertible notes.

Furthermore, Helix expects to utilize between $20 million and $30 million for share repurchases this year.

Total funded debt is expected to decrease to approximately $324 million at the end of this year.

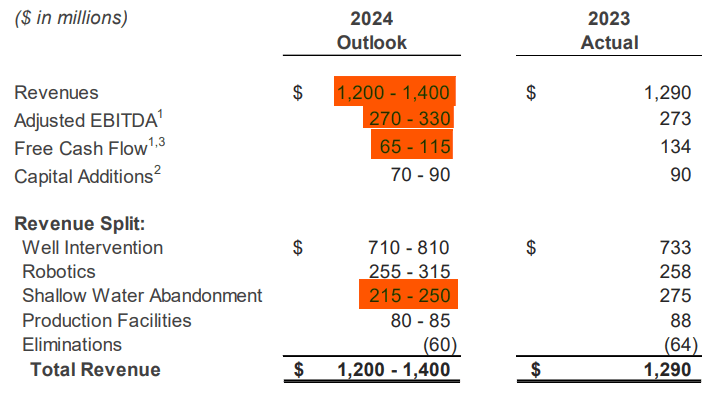

While the company’s Q4 and full-year 2023 results came in at the upper end of expectations, Helix Energy Solutions’ 2024 outlook was nothing to write home about:

Company Presentation

At the mid-point of the provided top-line range, revenues would be essentially flat, while Adjusted EBITDA would be up by approximately 10%.

Free cash flow guidance of $65 million to $115 million looks even worse, but please note that this number includes an estimated $58 million related to the above discussed earnout payment:

Company Presentation

But even adjusted for the earnout payment, free cash flow is not likely to improve meaningfully from the $134 million number reported for 2023.

With analyst expectations calling for revenues at the high end of the provided range and a very substantial increase in profitability, I would expect 2024 estimates to be revised lower.

Perhaps the most disappointing part of the company’s 2024 outlook was the expectation for the recently acquired Shallow Water Abandonment segment to show a material year-over-year decline just shortly after the end of the earnout period.

On the conference call, management admitted to some temporarily decreased demand in the Gulf of Mexico but expected the pullback to be short-lived:

We’re forecasting the Shallow Water market to generate similar EBITDA levels that we guided to for 2023, which is a meaningful reduction in EBITDA contribution year-over-year. However, we do expect a meaningful increase from there in 2025 and believe there’ll be a strong Shallow Water market in the Gulf of Mexico for years to come.

In addition to an anticipated recovery in the Gulf of Mexico, the company’s 2025 performance will also benefit from a number of high-specification well intervention assets (Siem Helix 1, Siem Helix 2 and Q7000) moving from low-margin legacy contracts to prevailing charter rates with a projected year-over-year EBITDA benefit of more than $75 million.

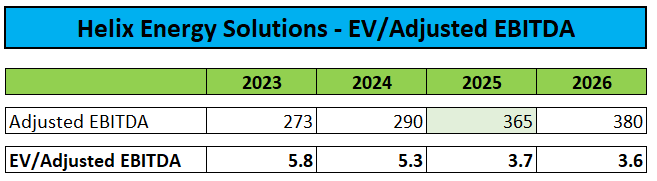

However, following the rather disappointing guidance for this year, I have lowered my 2025 adjusted EBITDA expectation slightly from $375 million to $365 million:

Company Presentation / Author’s Estimates

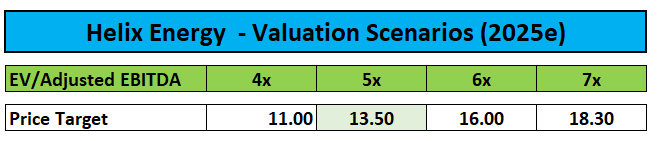

Assigning a multiple of 5x my 2025 EV/Adjusted EBITDA estimate would yield a $13.50 price target for the shares (down from $14.20 previously) thus providing for approximately 50% upside following Tuesday’s sell-off.

Author’s Estimates

Consequently, I am reiterating my “Buy” rating on the stock.

Key Risk Factor

Please note that offshore drilling and specialty services stocks remain heavily correlated to oil prices (CL1:COM), so any sustained down move in the commodity would almost certainly result in Helix Energy Solutions’ shares taking another hit.

Bottom Line

While Helix Energy Solutions reported decent fourth quarter results, the company’s outlook for 2024 fell short of expectations, thus causing the shares to sell off by more than 10% on Tuesday.

However, with 2025 still likely to be a year of major earnings inflection, I am reiterating my “Buy” rating on the shares while lowering my price target slightly to $13.50.

Q2 2024 Earnings Call Transcript")