Douglas Rissing

In keeping with my running commentary on bonds, thought to write an article focusing on treasuries. Since I last wrote about treasuries last year, returns have been mediocre as yields have risen. Moving forward, likely Federal Reserve cuts should put pressure on yields, which might lead to some short-term capital gains for treasuries, but lower long-term total returns.

On net, I think that treasuries are a much stronger, and reasonable, investment opportunity than last year. Settled on a hold rating, as I think there are even better investments out there, including high-quality CLO ETFs like the Janus Henderson AAA CLO ETF (NYSEARCA: JAAA) and the Alpha Architect 1-3 Month Box ETF (BATS: BOXX).

I’ll be focusing on the iShares 7-10 Year Treasury Bond ETF (NASDAQ: NASDAQ:IEF) for the remainder of this article, but everything should apply to other treasury funds and treasuries as an asset class in roughly equal measure.

Treasuries – Analysis

Dividends and Yields

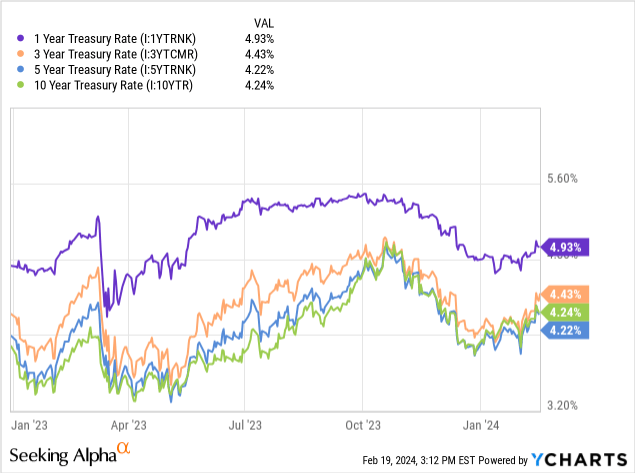

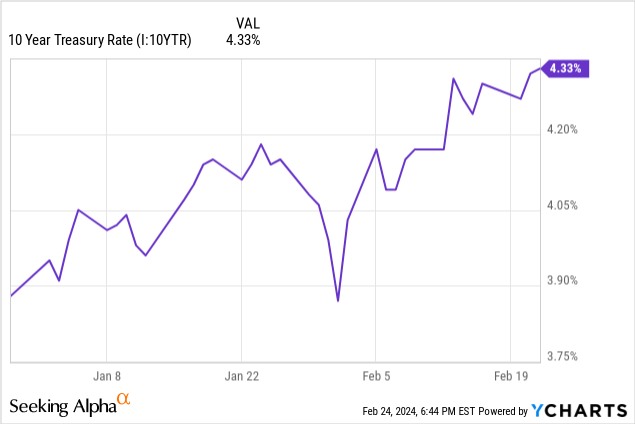

Treasury yields have risen since early 2023, with benchmark 10y treasury rates rising from 3.9% to 4.2%. Yields rose due to Federal Reserve hikes, and expectations of somewhat restrictive policy moving forward (higher for longer).

Data by YCharts

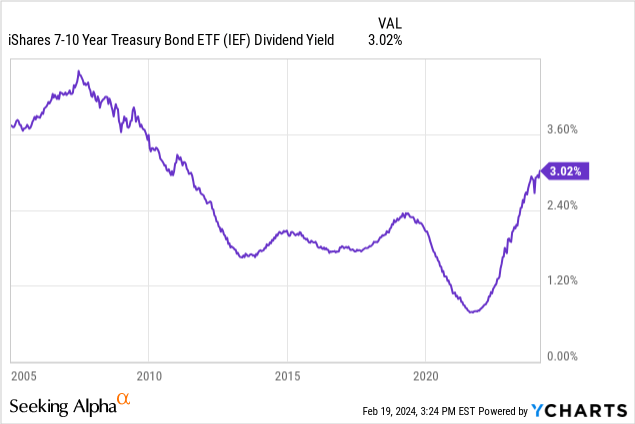

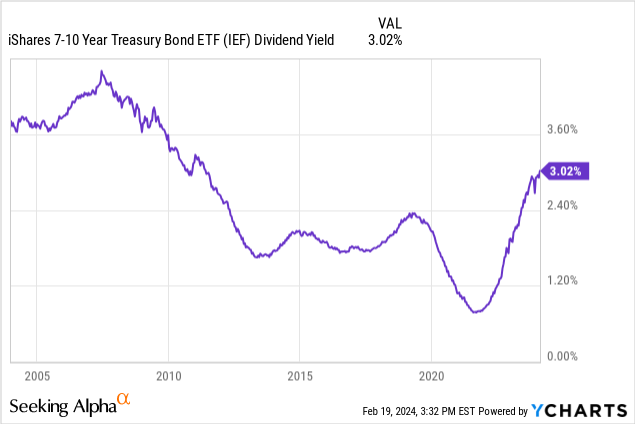

IEF itself has seen its yield increase from 2.0% to 3.0%.

Data by YCharts

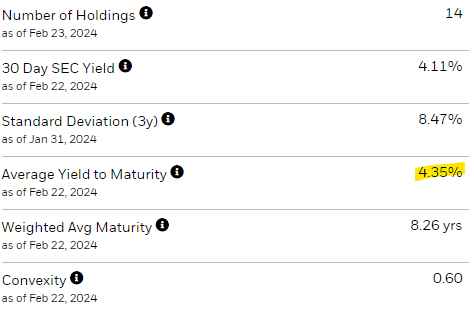

IEF’s yield remains lower than treasury rates, as the fund still contains several older treasuries with much lower coupon rates. These have lower prices, so expected total returns, including potential capital gains from treasuries maturing at par, are higher, and similar to those of treasuries themselves. IEF sports a 4.4% yield to maturity, comparable to prevailing treasury rates, as expected.

IEF

Treasury yields are at their highest levels since the financial crisis / housing bubble, but were generally higher during prior decades. Economic conditions have materially changed since, so focusing on more recent years seems appropriate.

IEF’s yield is also highest since the financial crisis, but was a bit higher during the 2000s.

Data by YCharts

Higher treasury yields will almost certainly lead to higher treasury returns long-term, an important, straightforward benefit for investors. IEF itself is a materially stronger investment opportunity now than last year, too.

Potential Federal Reserve Cuts

The Federal Reserve is guiding for three rate cuts this year. Although rate cuts are not certain, they seem incredibly likely, and most investors and analysts expect them to occur. Fed rate cuts should put pressure on treasury yields, with two important implications.

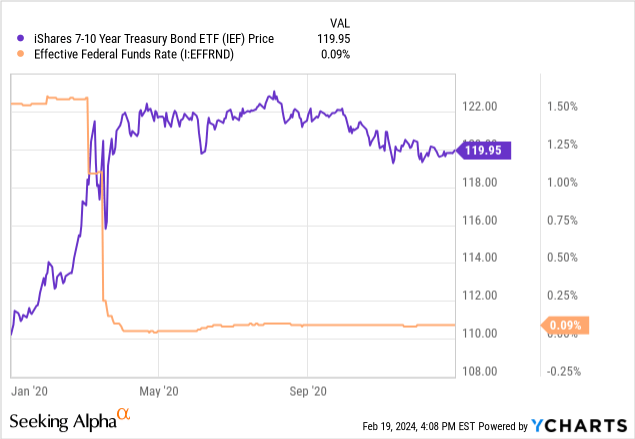

First, lower Fed rates should lead to higher treasury prices short-term. Remember, treasuries are fixed-rate investments, so Fed policy has no impact on existing treasury coupon rates. If rates go down, currently existing treasuries should continue to yield +4.0%, and those rates would start to look very attractive once Fed rates are near 2.0-3.0%. Demand for these older, higher-yielding treasuries should spike, leading to higher treasury prices. The same should be true for IEF. As an example, IEF’s share price increased from $110 to $120 during 2020, as the Fed slashed rates due to the pandemic.

Data by YCharts

Do bear in mind, the above is dependent on the magnitude and speed of any potential rate cuts. I would not expect higher treasury prices from a 0.25% rate cut in late 2025, I would expect them if rates are slashed, as during the pandemic. In practice, I expect rate cuts somewhere between these two extremes, so higher treasury prices are a somewhat uncertain possibility. Still, an important one.

The second implication of lower Fed rates is lower treasury long-term returns. Rates go down, yields decline, returns go down. Seems simple enough but, again, important to mention. Insofar as this is a possibility or concern, investors should gravitate towards investing in longer-term treasuries, to lock-in rates.

In my opinion, rates are likely to remain higher for longer, at least relative to market expectations and prices. As such, I do not think that treasury prices will significantly increase, nor potential returns decrease, in the coming months.

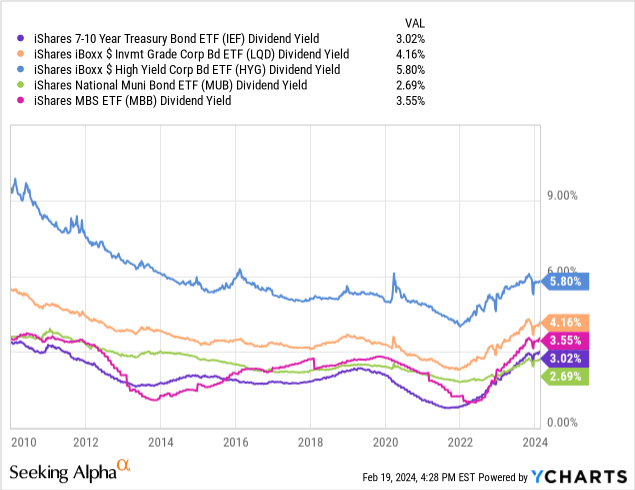

Treasury Peer Comparison

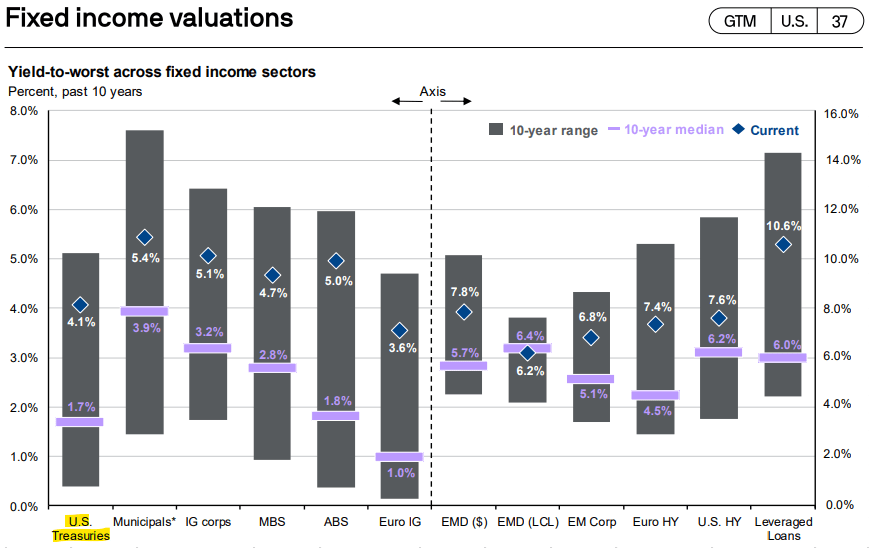

Due to recent Federal Reserve hikes, most bonds and bond sub-asset classes have seen higher yields. Treasuries are not special in that regard, although treasury yields have risen a bit higher than average, especially when compared to other investment-grade securities like municipal bonds and MBS.

JPMorgan Guide to the Markets

The same is generally true of bond funds, most of which have seen their yields rise to decades-highs. The iShares iBoxx $ High Yield Corporate Bond ETF (HYG) seems to be an exception, and I’m generally unsure why. Considering high-yield bond characteristics, the fund should be trading at a much higher yield than average. Dividends have risen since early 2022, at least.

Data by YCharts

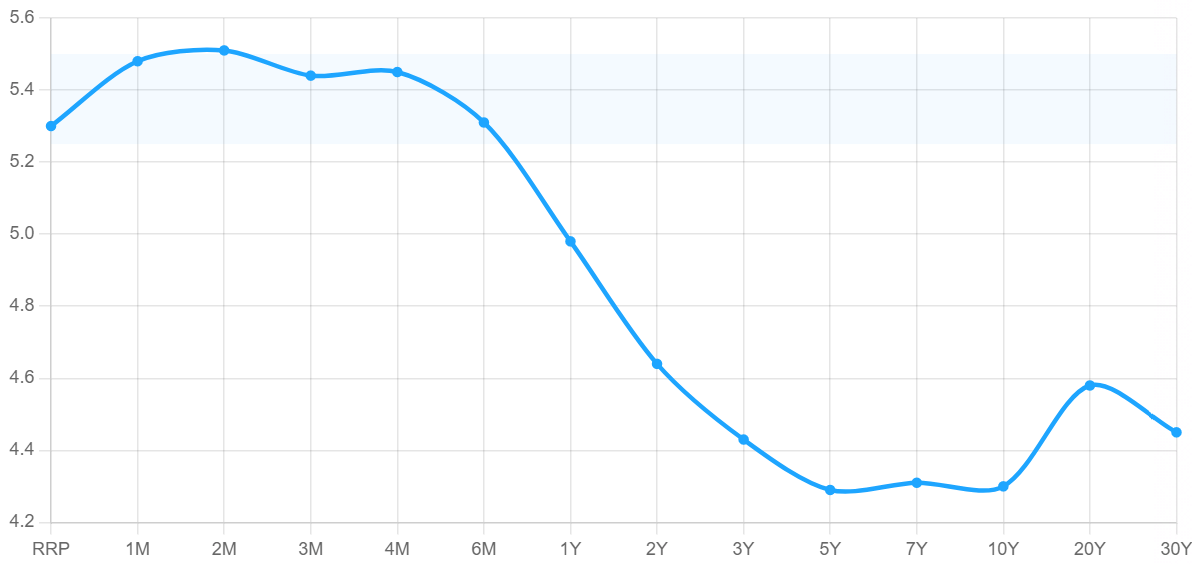

Due to expectations of near-term rate cuts and Fed guidance, the yield curve is inverted, with short-term securities generally yielding less than long-term securities. As an example, t-bills yield 5.3% right now, compared to 4.3% for 10y treasuries.

U.S. Treasury Yield Curve

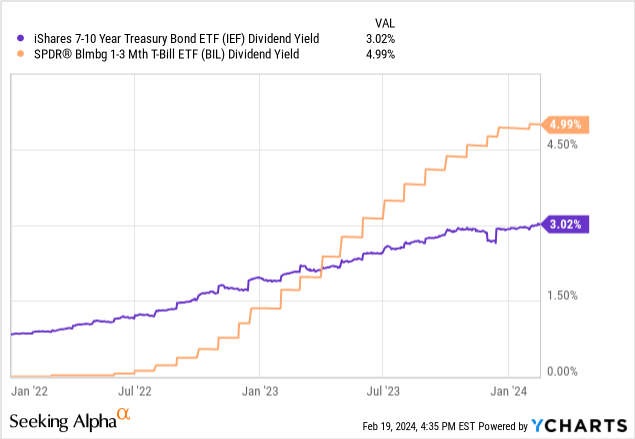

The same is true for IEF and t-bill funds.

Data by YCharts

So, treasuries are much stronger investment opportunities now than in the past, but the same is true of most bonds and bond sub-asset classes. Some of seem stronger than treasuries, too, offering higher yields or other benefits.

BOXX achieves t-bill like returns through options, providing some potential tax benefits to investors.

JAAA invests in high-quality CLO debt tranches. Risk and volatility are both extremely low, while the fund yields 6.2%.

BOXX is a short-term fund while JAAA’s underlying holdings are variable rate, so neither can be used to lock-in rates, unlike IEF or treasuries. I still prefer the pair to IEF, but that is an important difference.

Looking Back

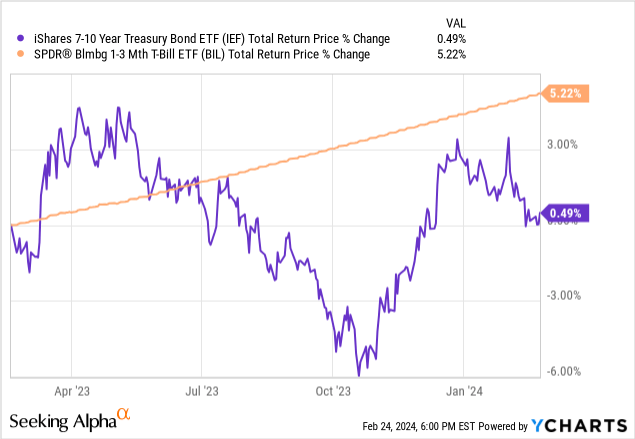

In my last article on treasuries, I argued that t-bills were a much stronger investment opportunity, due to their higher yields and lower rate risk. T-bills have outperformed since, in-line with expectations.

Data by YCharts

Since then, treasury yields have risen, inflation has eased, and the Fed seems poised to start cutting rates. As such, treasuries seem like much stronger investment opportunities now than in the past.

Conclusion

IEF’s dividend yield has risen, an important benefit for the fund and its shareholders. Lower rates might yield some short-term benefits, but the long-term impact will almost certainly be negative. Although IEF is a much stronger investment now than before, other choices look even stronger, including JAAA and BOXX.

Q2 2024 Earnings Call Transcript")