bymuratdeniz/E+ via Getty Images

Investment Overview – Why Protagonist Stock Has Been On Roller-Coaster Ride For Past 3 Years

Back in March 2021, I covered Protagonist Therapeutics (NASDAQ:PTGX) in a post for Seeking Alpha, giving the company and its stock a “Buy” recommendation, based on the potential of its lead proprietary drug, Rusfertide, to secure approval in the indication of Polycythemia Vera (“PV”), a rare form of blood cancer, and a pipeline of peptide antagonist drugs being developed in partnership with Janssen, the drug development subsidiary of Pharma giant Johnson & Johnson (JNJ), targeting the inflammatory condition psoriasis.

Nearly three years on, and on the face of it, very little has changed – Protagonist stock is priced at $27, down 8% since my note, and Rusfertide and the Janssen partnered assets remain the company’s primary focus.

With that said, I find myself breathing a heavy sigh of relief, because, although between March 2021 and August 2021 Protagonist’s share price rose from $30 per share, to $50 per share – a gain of 67% – it then dropped in value by 65% overnight, to ~$18, as the Food and Drug Agency (“FDA”) placed a clinical hold on Protagonist’s Phase 2 study of Rusfertide.

According to a Protagonist press release at the time:

The clinical hold follows Protagonist’s notification to the FDA of a recent non-clinical finding in a 26-week rasH2 transgenic mouse model study. The rasH2 model is designed to detect signals related to tumorigenicity, and benign and malignant subcutaneous skin tumors were observed in this study.

The situation was in fact resolved quickly as the FDA opted to remove the clinical hold in October 2021 – according to a Protagonist statement:

The Company provided the FDA with all requested information as the basis for a Complete Response and subsequent removal of the clinical hold. In particular, the Company provided the requested individual patient clinical safety reports, updated the investigator brochure and patient informed consent forms, performed a comprehensive review of the most recent safety database, and included new safety and stopping rules in the study protocols.

The rasH2 signal also prompted a re-examination of the four cases of cancer observed across all rusfertide clinical trials involving over 160 patients, and a comprehensive review of the safety database, including cases of suspected unexpected serious adverse reactions (SUSAR). No additional cancer cases, and no other unexpected safety signals, surfaced in this process.

By November 2021, shares had recovered to trade ~$35, but in late-April 2022, they sank in value to <$10 per share as the FDA moved to rescind the “breakthrough designation” it had given Rusfertide in 2021, again based on the nonclinical mouse data.

More bad news followed when Protagonist’s wholly-owned oral, gut-restricted, alpha-4-beta-7 (“α4β7”) specific integrin antagonist – PN-943 – flunked a Phase 2 Proof of Concept (“PoC”) study in Ulcerative Colitis (“UC”), with its 450mg twice daily dose failing to meet the pre-specified primary endpoint, although Protagonist framed the data positively.

By June 2022, Protagonist stock had reached a new low of ~$8 per share, where it remained for the rest of the year, with few share price needle catalysts in play. I had more or less written off Protagonist as a busted flush, when in March 2023, the company announced that its joint plaque psoriasis candidate JNJ-2113, met its main goal in a Phase 2 clinical study. According to a press release:

Data from the 255-patient study showed that JNJ-2113 achieved the study’s primary efficacy endpoint, with a statistically significant greater proportion of patients who received JNJ-2113 achieving PASI-75 (a 75% improvement in skin lesions as measured by the Psoriasis Area and Severity Index) responses compared to placebo at Week 16 in all five treatment groups

Shares climbed back to $30, but as I discussed in my previous note on Protagonist, auto-immune and anti-inflammatory markets are ultra-competitive, with almost every “Big Pharma” concern, and scores of smaller biotechs, attracted by the massive rewards on offer.

AbbVie’s (ABBV) Humira ruled the roost for more than a decade, commanding peak revenues of >$20bn in 2021 and 2022, before its patent protection expired last year, allowing generic competitors to flood the market.

The list of competitors today is intimidating, to say the least – UCB’s (OTCPK:UCBJY) Bimzelx, and Cimzia, Bristol Myers Squibb’s (BMY), Sotyktu, and Otezla, AbbVie’s (ABBV) Humira replacement Skyrizi, Sun Pharma’s Ilumya, Johnson & Johnson’s Tremfya, Remicade, and Stelara, Eli Lilly’s (LLY) Taltz, Amgen’s (AMGN) Enbrel – to name a few of the major players.

As such, when data was presented at the World Congress of Dermatology in Singapore, last July, comparing JNJ-2113 unfavourably with Stelara, Tremfya, and Skyrizi – whose revenues in 2023 were respectively $10.9bn, $3.1bn, and $7.2bn – Protagonist stock crashed yet again, to ~$14 per share.

Over the next few months, however Protagonist stock has once again recovered, after the company and Janssen insisted they would guide JNJ-2113 through a Phase 3 study, and as the Phase 3 study of Rusfertide continues, with full enrollment expected to be complete by the end of this quarter.

Protagonist Today – Liability, Long-Shot, Or Likely To Succeed?

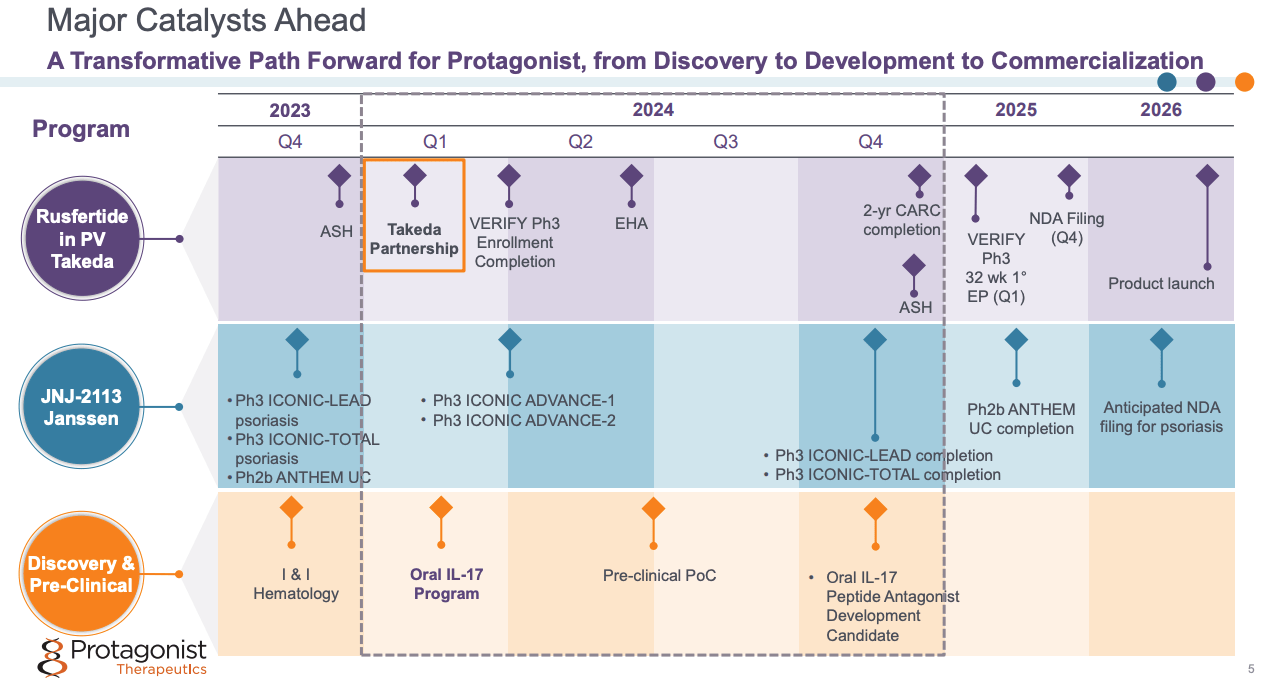

As we can see below, from a slide taken from a January corporate presentation, Protagonist has some notable catalysts in play in 2024.

Protagonist 2024 Catalysts (corporate preentation)

The Rusfertide opportunity has to an extent been derisked by a 50/50 co-development and commercialisation partnership agreed with Takeda Pharmaceuticals, the ~$46bn market cap Japanese Pharma powerhouse. According to a press release:

Under the terms of the agreement, Protagonist will receive an upfront payment of $300 million and is eligible to receive additional worldwide development and regulatory milestone payments, as well as commercial milestones and tiered royalties on ex-U.S. net sales.

Protagonist will remain responsible for research and development through the completion of the Phase 3 clinical trial and U.S. regulatory approval. Takeda has rights for ex-U.S. development and is responsible for leading global commercialization activities.

Dinesh V. Patel, Ph.D., President and CEO of Protagonist Therapeutics, commented on the deal:

As we progress towards a fully integrated pharmaceutical company, this deal mitigates the inherent execution risks of a first-time commercial launch, optimizes the timing and enhances the scope for peak potential sales of rusfertide, while still allowing us to actively participate in the commercial experience and economics with a 50:50 profit split in the U.S. market.

I suspect that Protagonist management will be delighted with this deal, which has helped its stock price climb ~25% year-to-date, giving the company a market cap valuation of ~$1.63bn at the time of writing. Protagonist also has the option to opt out of co-commercialisation, in exchange for a higher maximum milestone payout of $975m, and a higher royalty share of 29%.

As of Q3, the company had reported a near-term cash position of ~$330m, against a loss for the year to date of $106m, so there is a substantial funding runway now in place for the company.

While anti-inflammatory markets are teeming with therapies, there are only a few therapies indicated to treat PV – according to Protagonist’s 2022 10K submission / annual report:

Ruxolitinib, marketed as Jakafi®, was approved in 2014 for the treatment of adults with PV who have inadequate response to or are intolerant to HU. Approximately 5,300 PV patients are treated with Jakafi® each year. Besremi®, a ropeginterferon alfa-2b product indicated for the treatment of adults with PV, was approved with a black box warning in November 2021.

Rusfertide has a unique approach to treating PV – as I wrote back in 2021:

The excitement being generated by Rusfertide reflects its unique approach to treating PV – a disease with a prevalence of ~100k patients in the US, characterised by excessive production of red blood cells (“RBCs”) caused by myeloproliferative neoplasms (tumors), which has a median survival rate of ~20 years. PV can trigger thrombotic or cardiac events, and may progress to Myelofibrosis or Leukemia.

The key treatment paradigm for PV is to keep hematocrit (the volume percentage of red blood cells in blood) levels below 45%, which is usually done via a blood-letting procedure known as a Phlebotomy. Phlebotomies can only be carried out at hospitals or health clinics however, and do not generate sustained hematocrit levels <45%, increasing the threat of thrombotic events and disease progression. Research has suggested that patients with high hematocrit levels of 45-50% are 4x more likely to die from cardiovascular causes or major thrombotic events.

Rusfertide – an injectable treatment which can be self-administered by patients, reducing frequency of hospital visits – is able to restrict the overproduction of red blood cells by mimicking the activities of the Hepcidin hormone, which regulates the entrance of iron into the body from the intestine and the release of iron from the macrophage where it is stored throughout the body.

Back in 2020, analysts were predicting that Rusfertide could achieve peak revenues of ~$2.7bn. If that were to prove the case, and if we assume 50% of those revenues are achieved in the US, Protagonist’s share of profits would be derived from ~$675m of US revenues, and based on a 14% royalty share elsewhere, a further ~$189m of royalty payments would be available, plus development and sales related milestone payments.

If we assume a 20% profit margin, and a total revenues of $865m, Protagonist would be receiving ~$175m of revenue from Takeda, with no overheads, while I would add ~$50m per annum in milestones, for the next 5 years at least. $225m heading straight to the bottom line is a tantalising prospect for shareholders and Wall Street – a forward price to earnings ratio of ~7x, which is a ratio low enough to imply there is plenty of upside potential in Protagonist’s shares.

Looking Ahead – Milestones, & Risks To Look Out For

Of course, nothing is quite so straightforward in the biotech industry as I may have made it seem above. First of all, Protagonist still has a Phase 3 study to fully enrol, complete, and report upon – Takeda’s involvement and financial assistance does not begin until the drug is commercialised.

Given Protagonist’s past struggles with the FDA, there must be a risk that the agency will decline to approve the drug based on its adverse safety findings, although if the pivotal study data does not reveal any safety issues, Rusferide’s ability to keep patients out of the hospital will surely have significant appeal for physicians, patients, and health insurers. In its Phase 2 study, data showed that 92.3% of subjects (24/26) did not receive phlebotomy in part 2, 12-week randomisations part of the study. There was a 69% responder rate in the first part of the study, and Protagonist says that the study achieved “durable hematocrit control through 2.5 years”.

There will, however, be a long wait before a New Drug Application can be filed, and with no product launch expected until 2026 – assuming the FDA approves the drug – there is time for competing therapies to establish en entrenched market position. I am not aware of any other drugs in development with the same MoA as Rusfertide, however, which bodes well both for approval, and for growing market share as a viable alternative option to current standards of care.

Meanwhile, the ability of JNJ-2113 to compete in psoriasis markets may be impacted by its potential inferiority to current standards of care, although, as an orally available drug, it potentially has a convenience advantage over injectable drugs – most of the drugs I have mentioned that are approved to treat psoriasis are injectables. Additionally, if approved, JNJ-2113 may have a long period of patent protection, while other therapies are already facing, or will soon face, generic competition. As with Rusfertide, the biggest risk appears to the time it will take to bring the product to market – shareholders will need to be patient with Protagonist.

Concluding Thoughts – Do I Make Protagonist A Buy, Sell, Or Hold?

Aftre such a turbulent three years, and with some issues still to be resolved – the safety profile of rusfertide, the long wait for approval, what the market opportunity for rusfertide may be, the potential uncompetitiveness of JNJ-2113 – I plan to maintain a watching brief on Protagonist stock for the time being, as the damage a bad set of data or a regulatory miss-step can cause to the company valuation and share price is evident.

Protagonist’s current market cap valuation of $1.64bn is reasonably high for a company with no approved therapies, and no prospect of any until 2026 at the earliest, and I suspect there may be more volatility before we reach the approval end-game.

As such, although I do think Rusfertide can be a successful commercial product, and potentially JNJ-2113, and that Protagonist has two powerful Big Pharma partners, either of whom could make a lucrative acquisition bid for the company – I think there may be opportunities to buy into this story at lower prices, and perhaps more evidence is needed from pivotal studies before we can really judge how effective Protagonists two lead products can be.

That is why I rate Protagonist stock as a “hold” for the time being.

Q2 2024 Earnings Call Transcript")