shih-wei

Written by Nick Ackerman, co-produced by Stanford Chemist.

Despite the continuing global conflicts causing disruptions in key natural gas and oil-producing countries, the prices of these commodities have been resilient in the case of oil or falling in the case of natural gas. That’s put pressure on the share prices of energy companies.

In the closed-end fund space, we have the Tortoise Midstream Energy Fund (NYSE:NTG), which is invested primarily in midstream companies and focuses on natural gas. This closed-end fund also trades at a deep discount, providing another potential catalyst for returns in the future.

NTG Basics

- 1-Year Z-score: -0.62

- Discount: -17.59%

- Distribution Yield: 9.05%

- Expense Ratio: 1.98%

- Leverage: 20.30%

- Managed Assets: $270.9 million

- Structure: Perpetual

NTG’s investment objective is to seek a “high level of total return, emphasizing current distributions.” They will do this by investing “primarily in midstream energy entities, with a focus on natural gas infrastructure companies.”

The fund is leveraged, and that always increases volatility and risks. However, it can also potentially increase the positive total returns. In this case, the fund utilizes a few sources of borrowings. This is through a credit facility, senior notes and preferred.

One area in which CEFs have been getting hit is because their borrowing costs are rising. For NTG, they noted that just over 80% of their borrowings are based on a fixed rate. That means they haven’t been feeling the impact of higher costs of leverage at this point.

At year-end, the fund was in compliance with applicable coverage ratios, 80.2% of the leverage cost was fixed, the weighted-average maturity was 3.7 years and the weighted-average annual rate on leverage was 3.78%. These rates will vary in the future as a result of changing floating rates, utilization of the fund’s credit facility and as leverage matures or is redeemed. During the six month period ended November 30, 2023, $2.1 million of MRP shares and $3.0 million of Senior Notes were paid in full upon maturity.

Performance – Deep Discount

Energy overall struggled in 2023 after a solid 2021 and 2022 rebound performance. On a total NAV and share price return basis, NTG was able to put up some positive results.

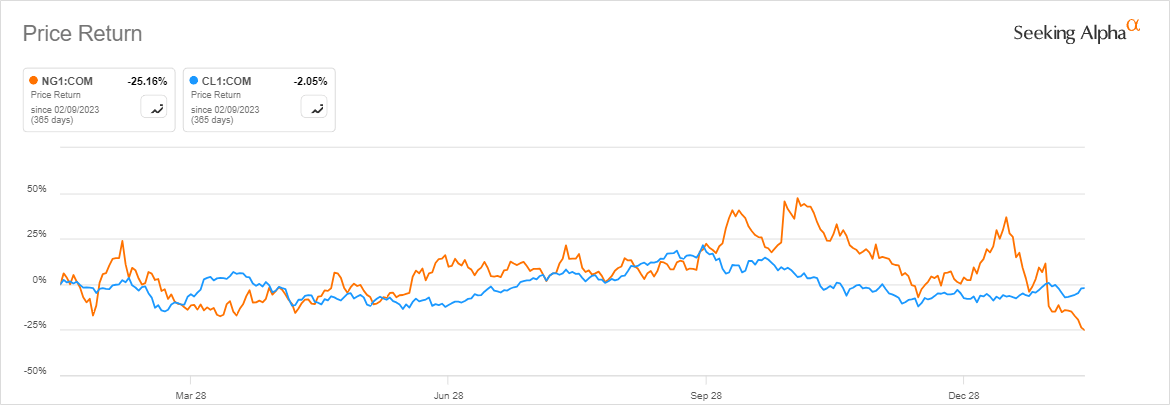

More recently, natural gas has been tumbling, and that’s putting pressure on funds like NTG. These latest declines helped to push the price down overall to over 25% in the last year. That said, we can also see that crude oil over the last year hasn’t been a standout either, as prices stay more or less stable despite ongoing global conflicts.

Natural Gas and Crude Oil Price (Seeking Alpha)

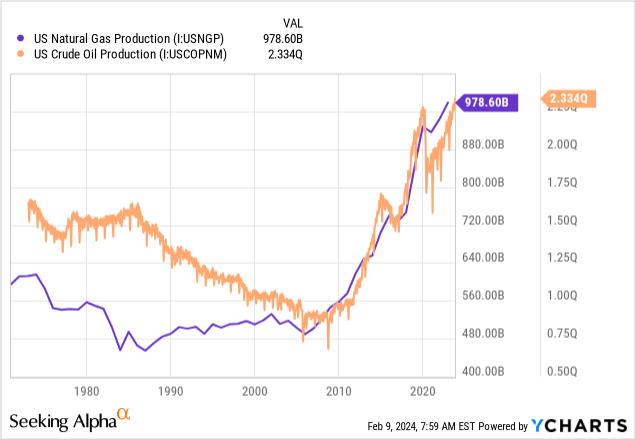

Warmer weather is certainly helping to dent demand. Another factor supporting supply and, therefore, helping to keep prices down is that the U.S. is producing more oil and natural gas at a record pace. We’ve now breached the levels that we saw prior to the Covid pandemic.

Ycharts

With all that being said, there are some opportunities here. The prices of these commodities are down now, and that’s impacting the share or unit prices of some of these midstream C-corps and MLPs in NTG’s underlying portfolio. Thus pushing the price of NTG’s own shares down as it loosely follows its NAV lower.

However, the underlying cash flows should be relatively protected for these midstream operations as they usually have long-term, fee-based contracts in place.

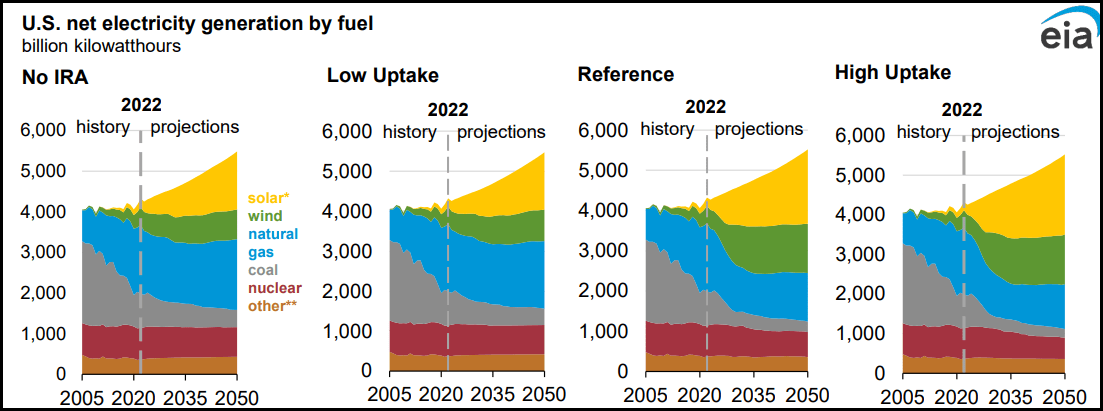

Natural gas and oil make the world go around and will be necessary for decades and even centuries to come – despite a push for more renewable sources of producing energy. That’s no matter what forecasted renewable uptake the EIA has provided in their annual energy outlook from 2023.

Electricity Generation by Fuel Projections (EIA)

Therefore, we know that demand will be there over the long term and that the reliance on these fossil fuels isn’t going anywhere. While NTG is down now, over the long run, the fund will likely survive and, barring a significant crash, likely to recover.

We know in 2020, the fund crashed and did not recover, but that was a black swan event. They went into 2020 as a highly leveraged fund at the time, and that caused permanent damage to the fund.

Today, they are still leveraged but much more modestly at a leverage ratio of around 20%. Heading into 2020, the fund had a combination of credit facility borrowings, senior notes, and preferred issuances that totaled $462.6 million. That put their effective leverage ratio at nearly double, pushing it toward 41%. Shortly after the Covid collapse, the fund implemented a 1-for-10 reverse split.

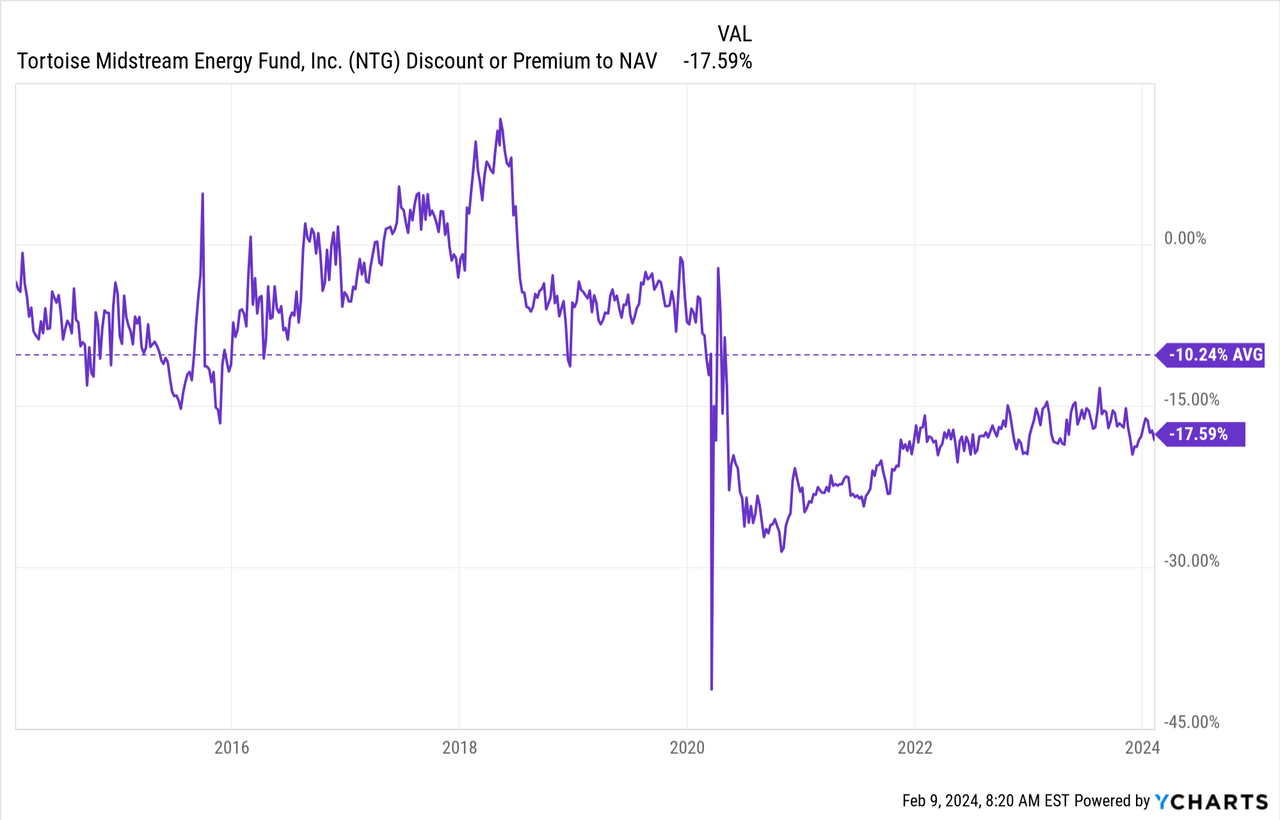

Also relevant today is that the fund is trading at a substantial discount. What made the fall even more dramatic for shareholders pre-Covid was the fact that the fund was only at a rather shallow discount. However, to be fair to those investors, the fund had been trading at a premium prior to that.

Ycharts

So, at that time, a 5% discount was relatively attractive, and most probably wouldn’t have assumed a sudden drop to a dramatic 30% discount was on the horizon. The discount since then has gradually narrowed since those 2020 lows. Even still, due to this higher valuation, the fund’s average discount over the last decade still comes in at around 10%. That’s even though the fund has been trading at well over double-digit discount levels since Covid.

Clearly, if there is another black swan event, there is no telling how far the discount could drop again. That’s always a general risk when investing in closed-end funds, regardless of the category.

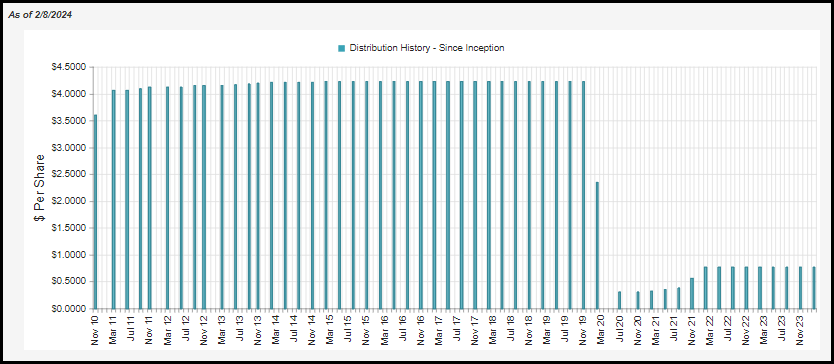

Elevated Distribution Thanks To Significant Discount

Naturally, when you lease three-quarters of assets in your fund nearly overnight in a black swan event, your distribution will be whacked as well.

NTG Distribution History (CEFConnect)

Today, it has clawed some of that back with a few distribution boosts. However, there will unlikely ever be a full recovery since the deleveraging was so aggressive, causing permanent damage to the fund. Said another way, just like the NAV will never reach pre-Covid levels – at least it is highly improbable – the distribution will never either.

The fund has a distribution policy to fall in the range of 7 to 10% annually based on the average week-ending NAV of the fund. Therefore, it would have to surmount a meaningful distribution rate before spilling over to see appreciation in the fund’s assets.

That said, another one of the main perks of a deep discount on CEFs is that it gives a boost to what investors receive in terms of distribution. In this case, the distribution rate for investors comes to 9.05%. At the same time, the NAV yield of the fund is more modest at 7.45%. This is on the lower end of their range, but given the discount, the actual rate investors receive is on the higher end.

As we know, though, a CEF can pay out what they’d like for as long as they like – assuming NAV doesn’t go to zero. That’s why looking at distribution coverage can actually be important because funds frequently pay out over what they earn.

Historically, for equity funds, we’d look at NAV over periods of time to make a rough estimate as to whether the fund is earning its payout. If NAV is rising, it could be considered earning the payout through income and appreciation. If it is declining, then it would be considered not to be earning its distribution. In the case of NTG, we know that any period of time prior to Covid or even the energy bust in 2015/2016 is going to look rough (i.e., distribution not being covered because NAV is down.)

That said, with their latest report, we can dive into the numbers of the last year. For the last fiscal year, 2023, the fund has a net investment income of $1,547,634, working out to $0.29 per share. They paid out $16,305,009 in distributions to investors for the year, which works out to around 9.5%. That’s consistent with the $3.08 annualized current distribution, which would put NII coverage at a light 9.4%. The fund had a tender offer and has been repurchasing shares in an effort to reduce the fund’s discount. That will have an impact on coverage going forward relative to where the last FY landed.

However, given the fund’s significant holdings in midstream and MLP-related investments, the fund collects significant returns of capital distributions. These ROC distributions to the fund are subtracted from the fund’s total investment income to arrive at the net investment income. So, it is cash flows the fund is receiving that should be recurring fairly regularly, assuming we don’t see mass distribution cuts in the underlying portfolio. Therefore, for this fund, we would look at distributable cash flow or (“DCF”) coverage as a more proper coverage metric.

The fund listed $8,057,534 in ROC distributions from its underlying portfolio. Adding that to the NII would push the figure up to $9,605,165. That puts DCF coverage at nearly 60%, a significantly better coverage ratio when looking at what should be relatively regular recurring cash flows. This isn’t out of line with other equity funds either, as they almost always require sizeable capital gains to cover their distributions fully.

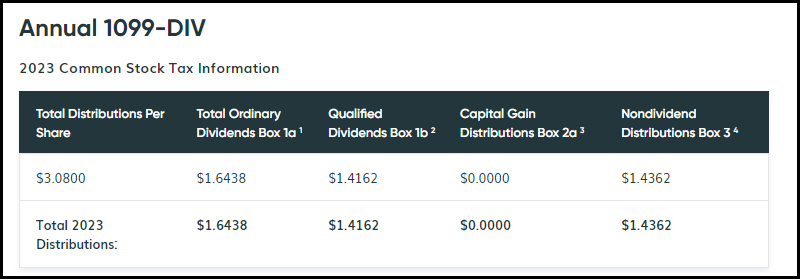

Given the significant amount of ROC distributions the fund receives, it’s likely we could continually see ROC distributions that it pays out itself. The 2023 distribution reflects this, with a significant portion classified as non-dividend distributions (another name for return of capital.)

NTG Distribution Tax Classification (Tortoise)

However, it should also be noted that the fund was previously structured as a C-corp. Going through 2023, the fund was transitioning to comply as a regulated investment company (“RIC”).

That meant at the fund level, they could be on the hook for taxes, but it also impacted the distribution classifications of the fund. This is because a RIC can generally pass through the tax classifications of what it receives itself. This means that if it receives distributions based primarily on the return of capital, capital gains, or qualified dividends, that can translate into its own distribution being classified similarly.

NTG’s Portfolio

NTG’s management team is fairly active. The latest fiscal year shows around 56% portfolio turnover. That was down from nearly 73% in 2022 but up from the ~58.5% listed in 2021. Currently, natural gas infrastructure is the largest allocation of the fund’s assets by far. Of course, that’s consistent with the fund’s investment policy.

NTG Asset Allocation (Tortoise)

Despite not having a specific renewable focus mandated for the fund, the fund does carry some renewable exposure. Having that greater flexibility, I believe, is a positive for the fund. They can dynamically shift the allocation over time depending on the adoption pace for renewables. Any fund that invests in energy infrastructure is naturally going to be exposed to a renewable shift based on regulations nudging in that direction.

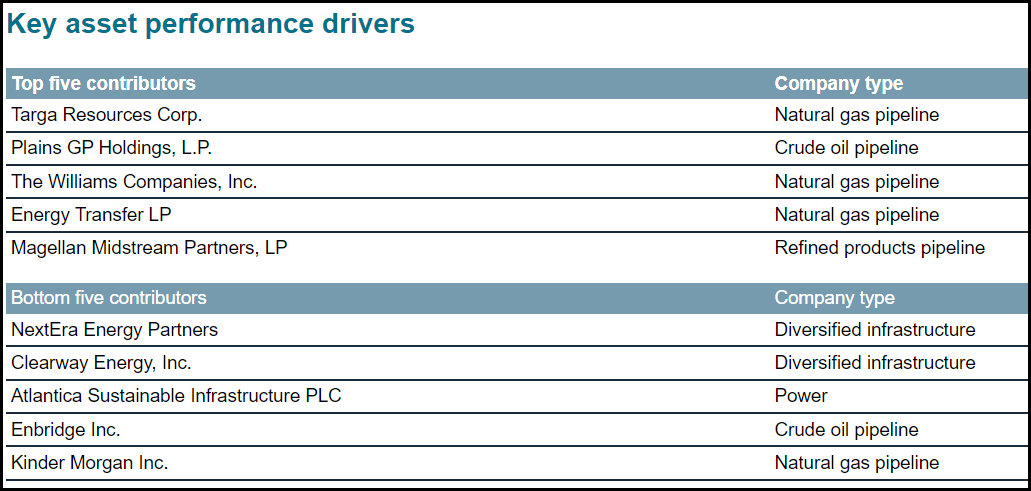

That said, the worst performers for NTG in the last year were those specifically tied to the renewable focus. That includes NextEra Energy Partners (NEP), Clearway Energy (CWEN) and Atlantic Sustainable Infrastructure (AY).

NTG Top And Bottom Performers (Tortoise)

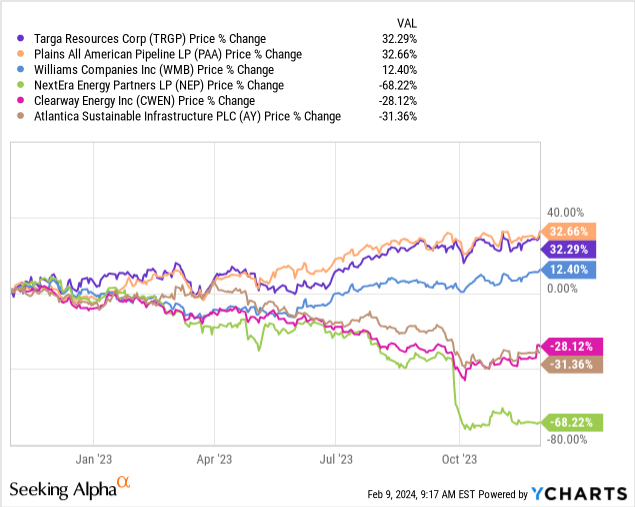

While there was a very noticeable drop in the share/unit prices of these renewables during October, the space had just been planning to underperform their fossil counterparts throughout the NTG FY 2023.

Ycharts

Significantly higher costs for funding debt are putting pressure on the space. Cheap debt was fueling these renewable operations, and now they are paying hefty distributions while running up against these higher borrowing costs. While government policies are pushing for more renewables, the funding through subsidies for these pushes has to be considered when deficits are ballooning and national debt levels are piling up. Fossil fuels are also subsidized globally, which isn’t projected to change much in the years to come. It would seem that the push against renewables is more debated as it’s a hotter political topic. That keeps the topic front and center and likely where funding cuts would come, if at all.

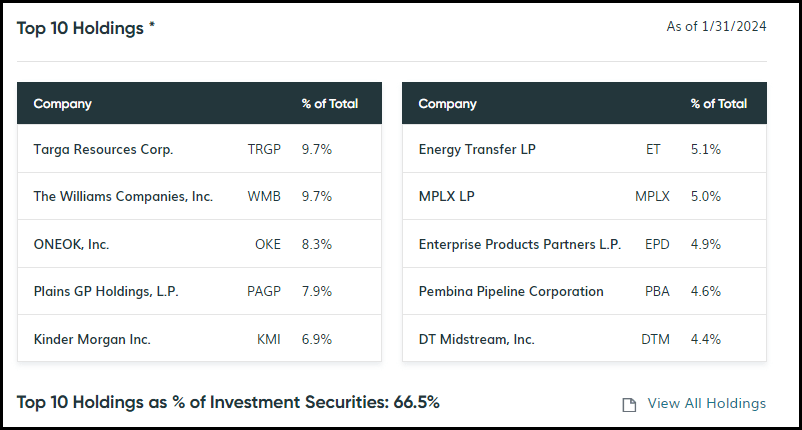

Looking more specifically at NTG’s top ten, we should also note the relatively high concentration of investments. The top ten account for over 66% of the fund’s total investments. The total holdings list comes to 25 when excluding cash.

NTG Top Ten Holdings (Tortoise)

This isn’t completely unheard of in the infrastructure fund space, but even more so when a fund is focused on midstreams more specifically. There are only so many midstreams/MLPs to invest in, and if you’re going to be discerning, that narrows what is worth investing in overall, too.

An important consideration for running a narrow portfolio is that you are more reliant on individual companies performing well. That is, the management team has to have a higher success rate of picking winners when there is less diversification. As a non-diversified fund focused specifically in one industry, this can be even more difficult when a sector in industry goes out of favor.

This could also lead to why turnover for the fund is relatively high. If you sell out of a position and replace it during the year, that one swap could account for a meaningful portion of the turnover.

Conclusion

NTG is looking like an opportunity as it comes under some pressure due to falling natural gas prices. The fund also sports a deep discount that provides another potential catalyst for upside in the future should that discount narrow. While it may not see premium pricing like it had in the past, the average discount has been slowly but surely trending to a narrower range since Covid.

Based on their last report, distribution coverage also looks strong thanks to relatively higher yields in the midstream space. This is also where a large discount can benefit shareholders because the rate paid out is meaningfully higher than what the underlying fund needs to earn to cover it.

Q2 2024 Earnings Call Transcript")