EvgeniyShkolenko/iStock via Getty Images

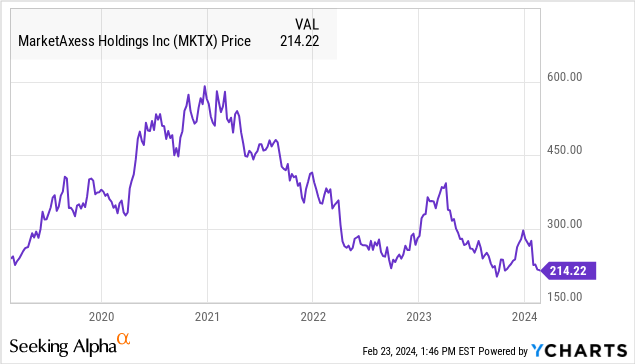

MarketAxess Holdings Inc. (NASDAQ:MKTX) reported its Q4 earnings which beat estimates although it wasn’t enough to stem a sharp selloff in shares that are down more than 25% YTD and currently near a five-year low.

We last covered the stock back in early 2022 citing what was then expected to be a “transitional year” for growth which appears to have exposed some deeper structural challenges. As we see it, the story here for the institutional-level fixed-income trading platform has been an ongoing reset of expectations compared to what was likely exuberance during a pandemic-era boom.

Recent data suggesting a decline in market share and otherwise soft profitability have worked to pressure sentiment toward the stock. The problem with MKTX in our opinion is that shares sit in a gray area as not quite delivering exceptional growth while also falling short of compelling value. We expect the volatility to continue.

MKTX Earnings Recap

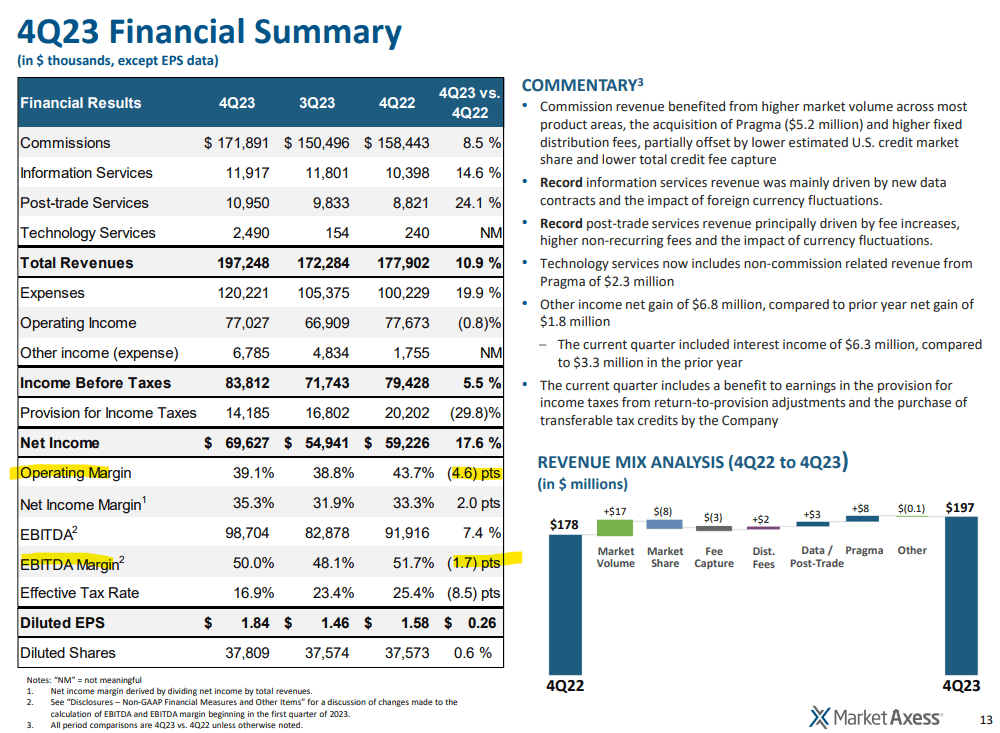

MKTX Q4 EPS of $1.84 was $0.12 above the consensus and also up 16% year-over-year. Revenue of $197 million climbed by 11% y/y benefiting from an ongoing international expansion as well as momentum from smaller segments like information services, post-trade analytics, and the technology group.

On the other hand, the core trade fee revenue growth of 8.5% in Q4, or 3.4% for the full year stands in contrast to the peak 37% growth achieved in 2020.

Keep in mind that the results this quarter also included an $8 million revenue contribution from the 2023 acquisition of “Pragma” as algorithmic trading and AI-powered execution solution. By this measure, the “organic” growth this quarter was closer to 6% y/y.

source: company IR

So while the top-line momentum has at least rebounded compared to a weaker 2022, the other side to the equation has been an ongoing increase in total expenses, up 20% y/y in Q4.

The effort to spend towards growth including adding headcount as well as on the R&D side is reflected in a lower operating margin of 39.1% in Q4, down from 43.7% in the period last year. Similarly, the EBITDA margin is also lower.

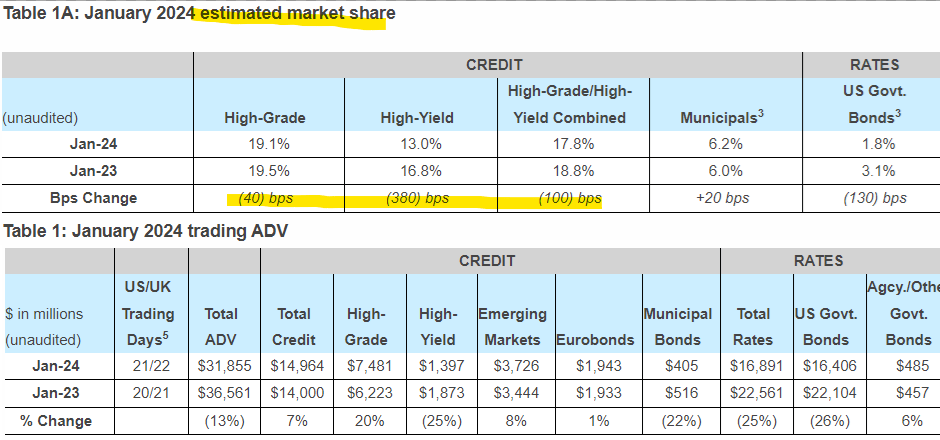

In attempting to understand the ongoing stock price weakness, the metric that stands out to us is the decline in market share with the monthly update for January into Q1 2024 showing an ongoing contraction. Within credit trading, high-grade and high-yield market share combined at 17.8% is down from 18.8% in the month last year.

Management is focusing more on “record” total average daily volume within credit as a key market segment reaching $15.0 billion, up 6.9% although the ADV for other segments is down.

source: company IR

The company believes that tighter credit spreads and reduced overall market volatility explain some of the drop, with an expectation that an eventual Fed rate cut will help improve the market backdrop.

In terms of 2024 guidance, MarketAxess is targeting full-year 2024 revenue growth of around 12% which includes a “mid-single digits” contribution from Prama. An estimate of total expenses of around $490 million for 2024, if confirmed, would represent a 12% increase y/y implying otherwise flat margins against similar growth.

source: company IR

What’s Next For MKTX?

Our takeaway when looking at MKTX is that the company is fundamentally sound with the recent operational and financial turbulence more or less reflecting growing pains in what remains a fast-moving market segment.

At the same time, it is worth looking back at some of the expectations the share price carried when the stock traded as high as $600 in late 2020 when the platform was seen as “disruptive” or a game changer compared to the industry stand where bonds, loans, and credit securities are traditionally traded over the phone.

For context, the total market cap of credit trading with data from January at 17.8% is down from as high as 19.5% in 2020. Any expectation that the company would reach a level above 30% or beyond appears increasingly unlikely in the foreseeable future. There is also a sense that the competitive landscape has worked to pressure fees and a headwind on profitability.

Players in this segment include Tradeweb Markets Inc. (TW), as well as “Bloomberg” and S&P Global Inc. (SPGI) which each over alternatives with strengths and weaknesses in certain categories. Our interpretation is that the industry has moved to implement many of the features that made MarketAxess stand out four or five years ago.

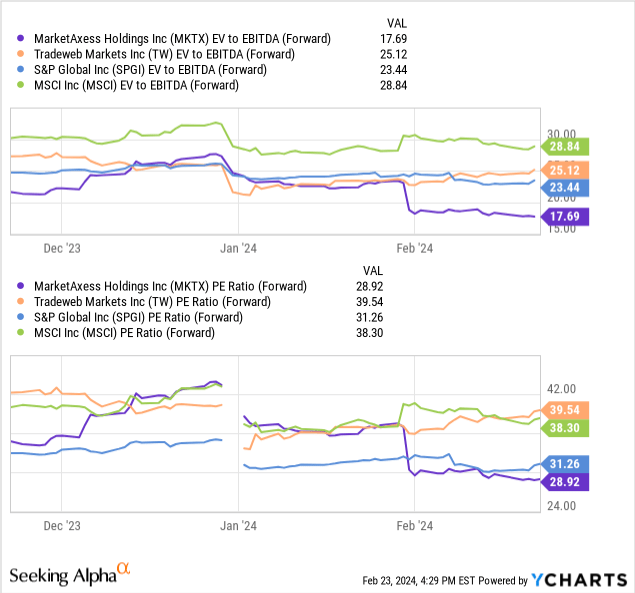

Shares trading at an 18x EV to forward EBITDA multiple or 29x forward P/E are at a discount to Tradeweb and SPGI, as a financial data leader, which we believe is justified given the recent trends.

The bullish case for MKTX is that the company can manage a re-acceleration of organic growth while also showing signs of stabilizing or gaining market share. The risk is that the data continues to underperform and the stock could face a re-pricing lower as the market reassesses the long-term opportunity.

Final Thoughts

2024 will be a critical year for MarketAxess to deliver a turnaround with an eye on financial efficiency and stronger operating momentum. The good news is that the company remains profitable with otherwise solid free cash flow that at least buys it time to make the platform work.

While leaning bearish, we’ll rate shares as a hold, balancing what we believe to be ongoing challenges while also recognizing that the steep selloff has likely already incorporated many of the negatives. A break in the stock below $200 would signal a more concerning deterioration of the outlook that shareholders should keep an eye on. Our base case is for volatility to continue.

Q2 2024 Earnings Call Transcript")