e-crow

SM Energy Company (NYSE:SM) has managed to reduce its net debt below $1 billion, and now has $616 million in cash on hand (at the end of 2023) in addition to $1.585 billion in outstanding notes. I project that SM will generate $491 million in free cash flow in 2024 at current strip prices.

SM increased its dividend by 20% and now offers a $0.18 per share quarterly dividend. This should leave over $400 million of its 2024 free cash flow remaining for share repurchases, acquisitions, and/or further debt reduction.

SM’s production and cost outlook for 2024 is largely similar to how I modeled its 2024 results back in October. SM’s 2024 capex budget is around 5% higher than what I modeled it at before, but it is also expecting 2024 to have a slightly higher oil cut than its late 2023 production.

SM’s production is around 39% natural gas though, and the relatively weak natural gas prices (combined with lower oil prices) have reduced its projected free cash flow (compared to my October look). Thus, I am now estimating SM’s value at approximately $46 per share.

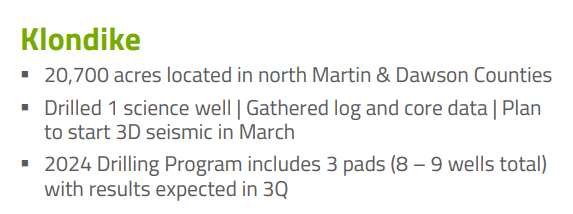

Klondike Development

SM is starting development on its Klondike asset, which it acquired in mid-2023 for approximately $94 million. Klondike is located in Dawson and northern Martin counties, and had production of 1,250 BOEPD (90% oil) at the time of the acquisition.

SM anticipates drilling 8 to 9 Klondike wells in 2024 and expects to have results available in Q3 2023. SM previously indicated that it expected an oil breakeven point of $50 or less (based on a 10% discount rate) for Klondike. That was based on capital costs at the time, and SM is modeling 10% year-over-year deflation for its 2024 development program now.

Klondike Development (sm-energy.com (Q4 2023 Presentation))

2024 Outlook

SM is expecting to average approximately 157,000 BOEPD (44% oil) in 2024 production at its guidance midpoint. This is similar to what I had modeled in October, but with a 1% higher oil cut than what I had modeled.

SM notes that its 2024 guidance calls for an approximately 6% increase in oil production and a 3% to 4% increase in total production compared to 2023.

The current strip for 2024 includes $76 to $77 WTI oil and approximately $2.40 NYMEX gas. SM is projected to generate $2.419 billion in oil and gas revenue during 2024 while its 2024 hedges add $37 million in value.

| Type | Barrels/Mcf | $ Per Barrel/Mcf | $ Million |

| Oil | 25,214,200 | $75.50 | $1,904 |

| NGLs | 9,948,148 | $23.00 | $229 |

| Gas | 132,855,912 | $2.15 | $286 |

| Hedge Value | $37 | ||

| Total | $2,456 |

SM expects its 2024 capex budget to be approximately $1.14 billion to $1.18 billion, excluding any spending for acquisitions (and excluding capitalized interest). I have chosen to include all interest costs (capitalized and non-capitalized) as a separate line item. SM’s net cash interest costs are expected to be around $80 million for 2024 as it is also generating a decent amount of interest income with over $600 million in cash on hand.

Around $40 million of SM’s capex budget is for facilities. SM is devoting 60% of its D&C capex to the Midland Basin and 40% to its South Texas assets.

SM is thus projected to generate $491 million in free cash flow in 2024 at current strip prices, including the impact of cash taxes. SM noted in its Q4 2023 earnings call that its cash taxes benefit from R&D credits related to its well optimization efforts. Cash taxes for 2024 are expected to be approximately $10 million and the credits are expected to carry over into 2025 as well.

| $ Million | |

| Lease Operating | $312 |

| Transportation | $135 |

| Production and Ad Valorem Taxes | $163 |

| Cash G&A | $105 |

| Net Cash Interest | $80 |

| Capex | $1,160 |

| Cash Taxes | $10 |

| Total | $1,965 |

Uses Of Cash

SM increased its quarterly dividend from $0.15 per share to $0.18 per share recently. SM had a bit under 116 million outstanding shares at last report, resulting in $83 million in projected 2024 dividends with that number of shares.

This would leave $408 million (of SM’s projected 2024 free cash flow) for other purposes.

SM had $616 million in cash on hand and $1.585 billion in outstanding notes at the end of 2023. Of those notes, $349 million mature in 2025, so SM may decide to call those in 2024. However, since the interest rate on the 2025 notes is only 5.625%, redeeming those notes will only have a minor impact on SM’s interest costs (net of interest income).

SM also has $215 million still available for share repurchases under its current $500 million share repurchase program. SM repurchased approximately 7.2 million shares under this program for $228 million during 2023.

Valuation Estimates

SM is now expected to generate around $4.25 per share in free cash flow in 2024. This should increase a bit in future years with improved natural gas prices.

I currently estimate SM’s value at $46 per share, assuming long-term prices (after 2024) of $75 WTI oil and $3.75 NYMEX gas. This is around $2 per share lower than my prior estimate of SM’s value, which was at a time when SM was expected to generate $700+ million in 2024 free cash flow (with low-$80s oil and $3.50 gas for 2024 strip).

Conclusion

SM Energy is now projected to generate close to $500 million in free cash flow in 2024 at current strip prices. SM’s guidance for 2024 is largely in-line with my previous expectations, but lower near-term commodity prices have reduced my 2024 free cash flow estimates by over $200 million since I looked at it in October 2023.

SM’s balance sheet appears to be good, with its net debt reduced to under $1 billion. It appears capable of redeeming its upcoming debt maturities via a combination of cash on hand and free cash flow generation.

I estimate SM’s value at $46 per share at long-term (after 2024) $75 WTI oil and $3.75 NYMEX gas now.

Q2 2024 Earnings Call Transcript")