Gary Hershorn/Corbis News via Getty Images![]()

Investment Thesis

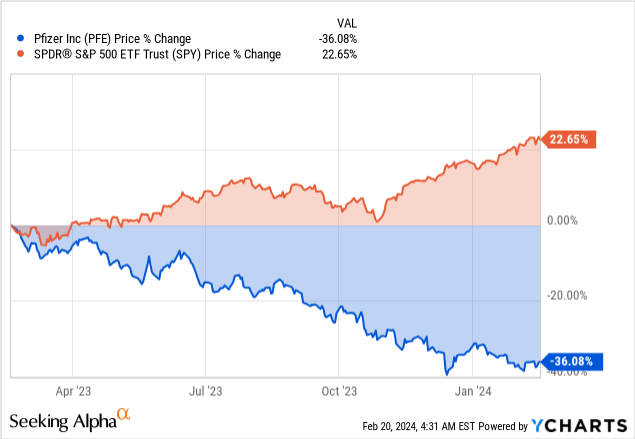

Pfizer Inc. (NYSE:PFE) experienced a significant decline in its revenue, primarily due to a sharp decrease in sales from its COVID-19-related products and vaccines. This downturn led to a 36% drop in the company’s share price since its 52-week highs, positioning it as one of the most underperforming stocks in the market.

This stark contrast was even more pronounced as the S&P 500 Index (SP500) recovered, closing the year with a 23% gain. Pfizer stock is trading close to its lowest point in a decade, highlighting an urgent need for the company to identify and leverage new growth drivers to recover its market position.

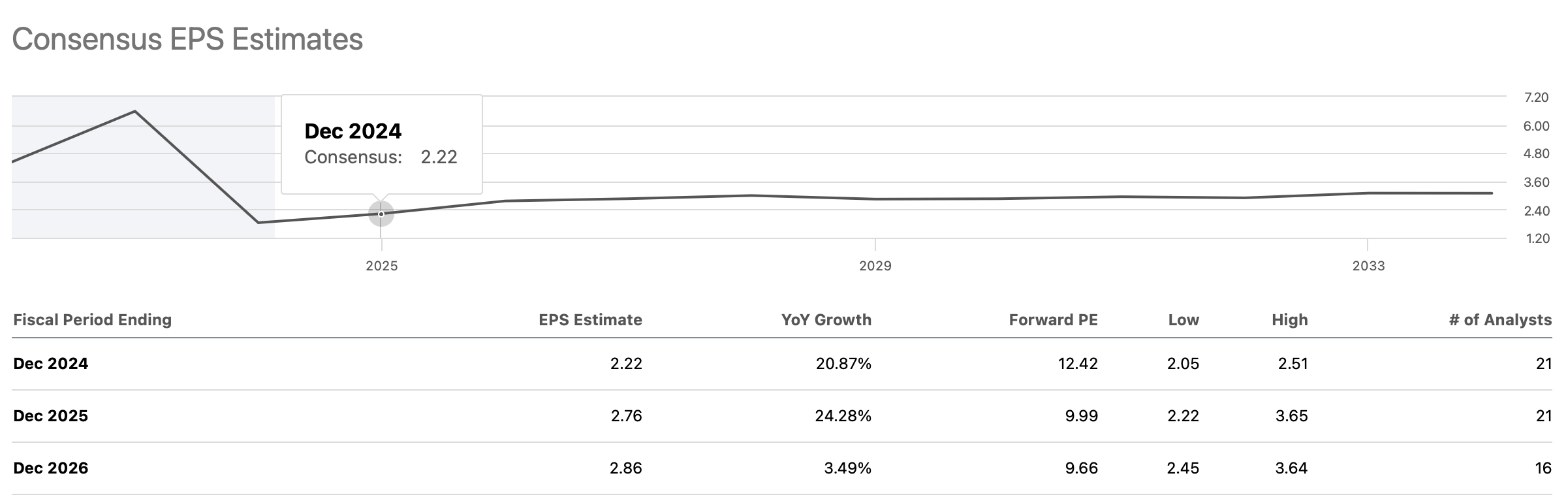

Analysts expect the company to grow by 4% and 5% this year. In contrast, Moody’s estimate shows that the entire healthcare industry will grow by about 4%, signaling that the company is still firing on all angles despite its struggles on the COVID-19 front, supporting Pfizer’s outlook.

Finally, the company boasts an impressive track record in returning value to shareholders through its 14-year dividend growth stream backed by a yield of 6%, earning the buy rating.

From Pandemic Peak to Pressing Challenges and the Path to Revival

The underperformance in recent months comes at the backdrop of the company’s earnings and stock price being artificially inflated at the height of the COVID-19 pandemic. The pandemic triggered strong demand for the company’s vaccines and other related products. Earnings grew by over 196% in two years as COVID-19 vaccine Comirnaty brought in $38 billion in peak annual sales.

However, with demand for booster shots declining dramatically, the company has felt the full brunt of the market in response to the dramatic drop in earnings. With the COVID-19 portfolio bringing in less than $8 billion in revenues in recent years, the stock would always come under pressure.

A slowdown in COVID-19 business is not the only headwind that has significantly affected the stock’s sentiments and performance in the market. Pfizer has been experiencing a significant slowdown in its international business. The situation is compounded by the prospect of the company’s essential drug patents expiring, putting it at risk of facing generic competition.

Debt is another significant issue that could affect the company’s margins and performance in the future. The drugmaker took in significant debt that had risen to $63.60 billion as of Q3 2023 as it sought to accelerate its research and development efforts. The high-interest rate environment already significantly challenges interest expenditure, increasing significantly. Nevertheless, the company has a solid balance sheet to navigate the tumultuous macro environment with over $40 billion in cash and short-term investments

However, it is not all doom and gloom for the giant drugmaker. The company still has underlying solid fundamentals that could offer support in future years. An experienced talent pool supplemented by a competitive edge in research and development affirms the company’s long-term prospects. For instance, the company secured crucial Food and Drugs Administration approvals for new drugs.

Finally, embarking on aggressive cost cuts is one of the options on the table as the drugmaker seeks to trim its operational costs and bolster its profit margins.

Navigating Post-Pandemic Challenges Toward a Resilient Future

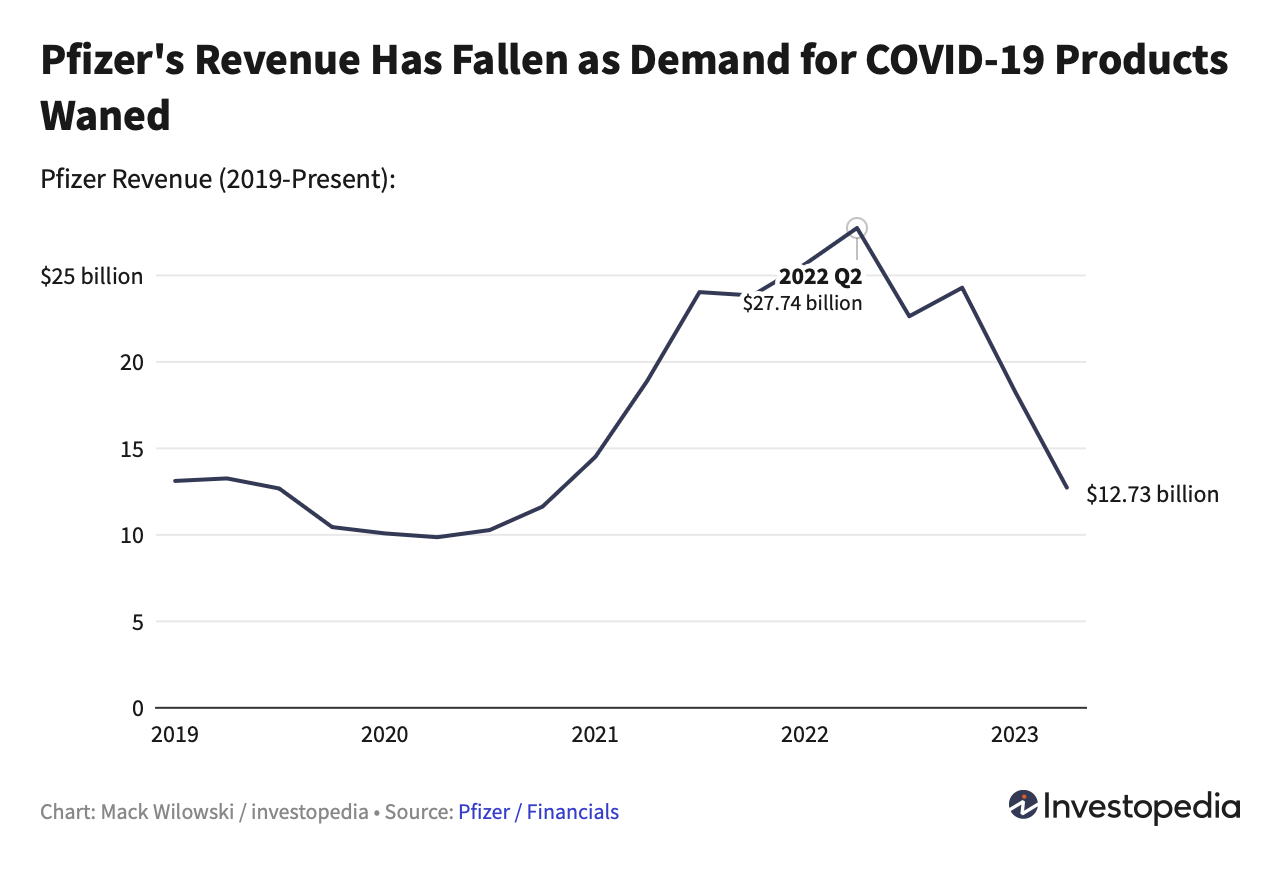

A decline in revenues has been a concern for Pfizer. In the third quarter of last year, the drugmaker struggled with stockpiles of COVID-19 treatment Paxlovid and dwindling demand for the same illness vaccine. As a result, the company plunged into a net loss of $2.38 billion or 42 cents a share, hurt by falling revenues. The net loss came as the earnings took a hit from $5.6 billion of non-cash inventory write-off as the company took back millions of unused Paxlovid doses from the government.

The revenue decline in 2023 came as Paxlovid sales fell by over 90% and Comirnaty sales fell by over 70%. The plunge further reiterated that the days of COVID-19 fueled demand were over. With only 7% of the US population receiving booster shots as of the third quarter, Pfizer warned that demand would continue to drop. Consequently, the company was forced to lower its 2023 guidance as demand for COVID-19 products waned and weighed significantly on results.

After the disappointing Q3 2023 financial results, Pfizer announced plans to adjust the COVID-19 landscape. Part of the plan entailed cost cuts through a series of layoffs. The company also closed select facilities as it sought to reduce its operating costs. Thus, the cost cuts are expected to save the company up to $1 billion in 2023 and as much as $2.5 billion in 2024.

Pfizer’s declining revenues (Investopedia)

The efforts appear to be bearing fruits, as the drugmaker bounced to a surprise profit in the fourth quarter as it delivered results that toppled analysts’ expirations. The US drugmaker delivered a profit of 10 cents a share. In contrast, analysts expected the company to plunge into a loss of 22 cents a share.

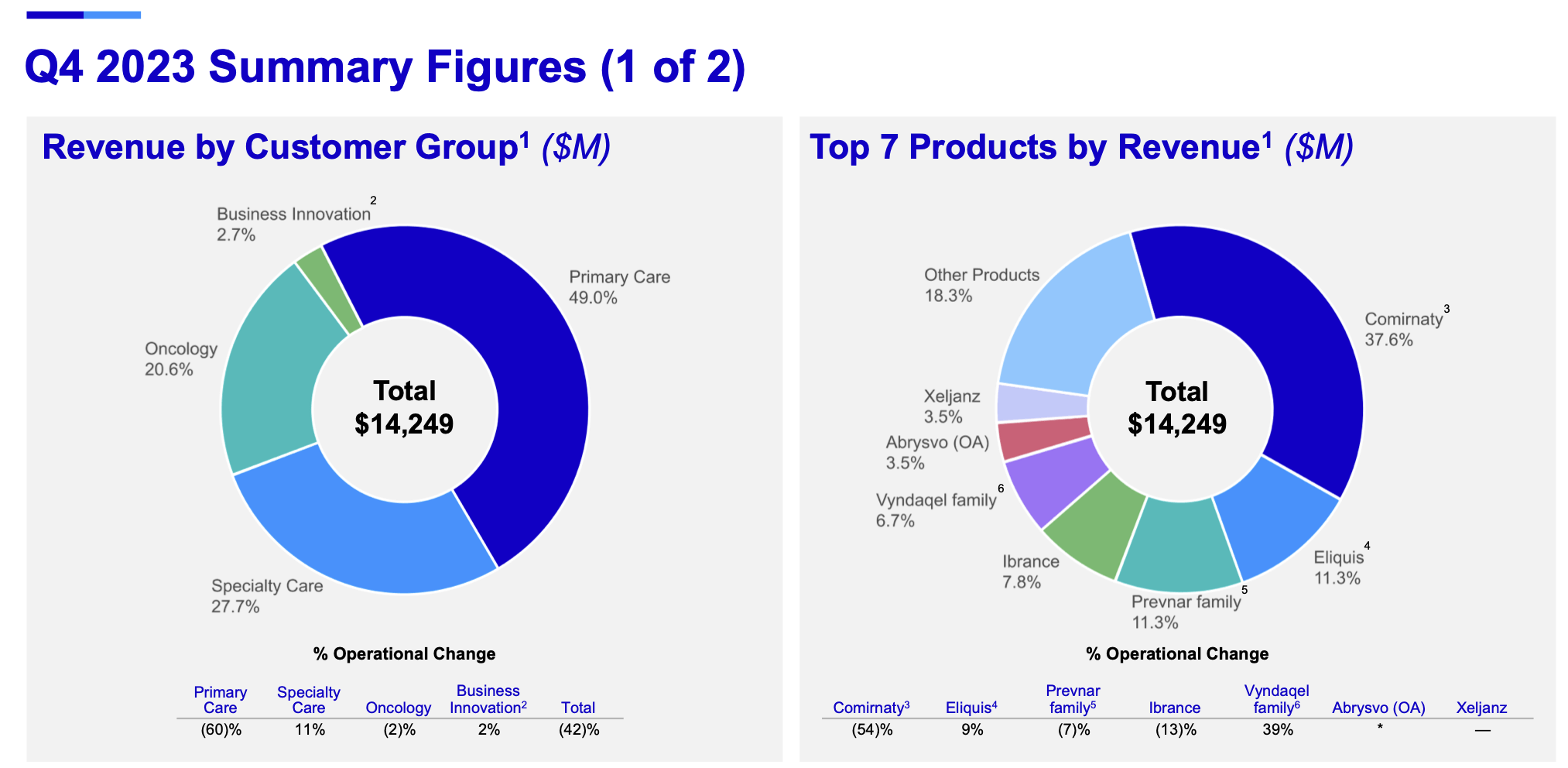

Revenue in Q4 2023 totaled $14.25 billion, down 41% year over year, falling short of analysts’ estimates of $14.42 billion. Pfizer struggled to beat analysts’ estimates on revenues as sales from its COVID-19 products, led by antiviral treatment Paxlovid and COVID-19 vaccine Comirnaty, came in at $12.5 billion, down 78% from their $57 billion peak in 2022.

Seeking Alpha

Pfizer is already looking into the future as it looks to reduce its reliance on COVID-19 products. While the company is focused on returning to profitability through a $4 billion cost-cut program, it’s also strengthened its pipeline of drugs and vaccines. The company plans to grow its revenue base through its $43 billion acquisition of cancer drugmaker Seagen and its new RSV vaccine.

Excluding COVID-19 products, Pfizer’s fourth quarter revenue was up 8%, fuelled by a string of new vaccine agents’ respiratory syncytial virus that entered the market in the third quarter. Abrysvo is one of the new products that Pfizer relies on to strengthen its revenue streams. The vaccine was developed and approved to help protect older adults and infants through maternal immunization, and it’s currently approved for use in the U.S. and the EU. Hence, the respiratory shot generated $515 million in revenue from the company in the fourth quarter.

Pfizer

Supported by the impressive Abrysvo sales, Pfizer has set out to increase the RSV market share. It plans to establish vaccination as a year-round discussion while expanding its ritual contracting offerings. Vyndaqel drugs, a set of treatments for cardiomyopathy and heart muscle disease, also strengthen Pfizer’s revenue streams beyond COVID-19 products. The drugs recorded a 41% increase in sales in Q4 to $961 million. The company’s blood thinner drugs, led by Eliquis, continue to drive growth, having recorded a 9% increase in sales in Q4 to $1.61 billion.

Additionally, the company has secured regulatory approval for using Velsipity to treat moderate to severe active ulcerative colitis. The FDA has also approved Elrexfio, a BCMACD3-targeted bispecific antibody for relapsed/refractory multiple myeloma. Lastly, Pfizer secured regulatory approval for Litfulo, a JAK3 inhibitor for treating severe alopecia areata, as a weak pediatric growth hormone deficiency treatment.

Mergers and Acquisitions Fueling New Growth Horizons

With the slowing COVID-19 business, Pfizer is turning to business deals to revitalize its growth metrics that have taken a significant hit. The company has set sights on mergers and acquisitions that it hopes will strengthen its product pipeline and give way to a new frontier for sales growth.

Completing the Arena Pharmaceutical acquisition for $6.7 billion was part of the new growth strategy. With the acquisition, the company has strengthened its portfolio with exposure to various treatments for several inflammatory diseases.

Moreover, Arena Pharmaceuticals adds to Pfizer’s pipeline a portfolio of promising development-stage candidates in key areas of cardiology and dermatology. The wide portfolio of drugs that comes with the acquisition should enhance the company’s ability to target various medical conditions, including ulcerative colitis.

In addition, the $43 billion acquisition of Seagen underscores how Pfizer remains focused on strengthening its competitive edge in the drug-making business, as it now has access to over 60 programs. This was the largest deal in over four years, following the acquisition of Allergan for a $63 billion acquisition.

Pfizer

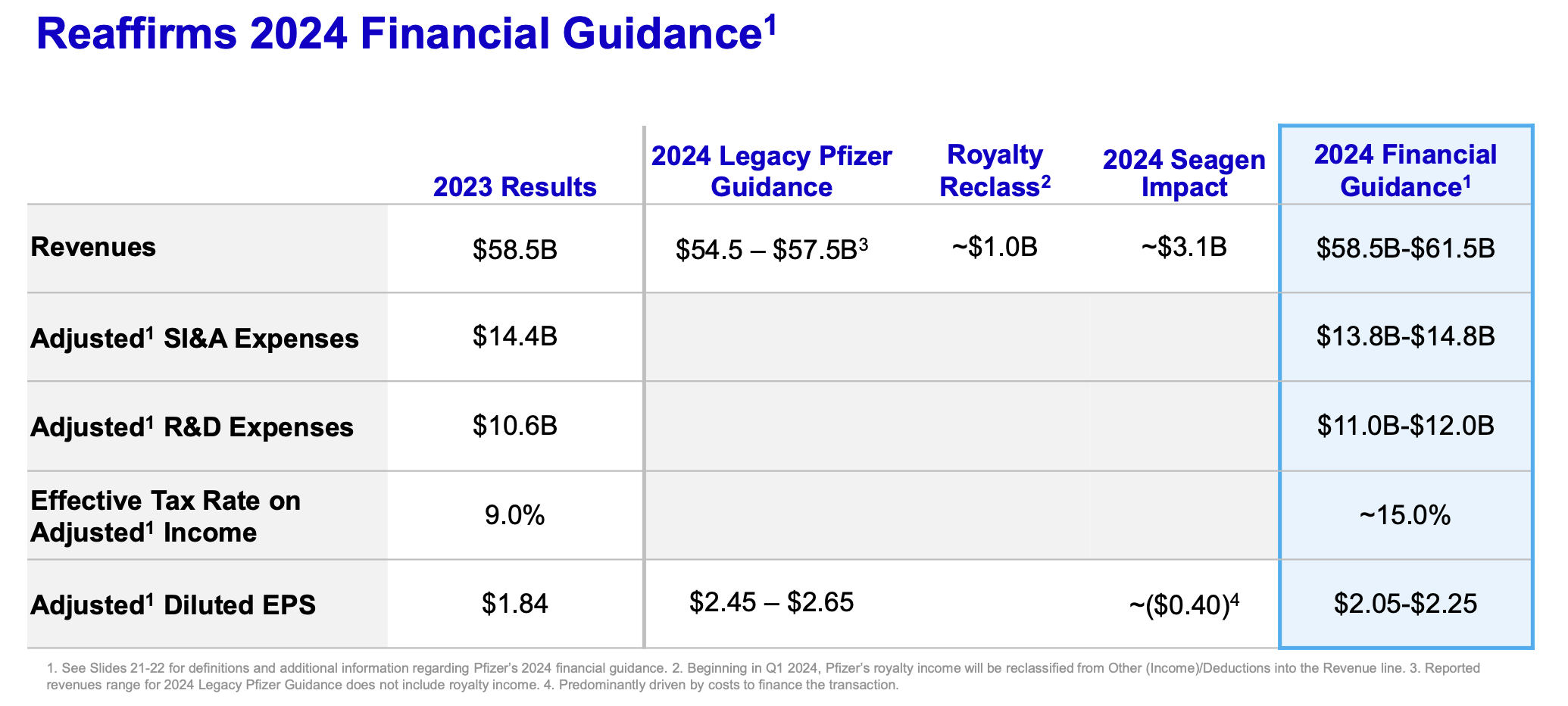

The Seagen acquisition not only strengthens Pfizer’s pipeline of oncology medications but is also expected to bolster financial growth prospects. Pfizer has already reaffirmed its 2024 guidance, whereby it expects revenue to average between $58.5 billion and $61.5 billion. Seagen should contribute about $3.1 billion in revenues this year and could rise to over $10 billion by 2030. The company expects COVID-19 products to contribute $8 billion in sales.

While factoring in the company’s other products and its series of acquisitions, COVID-19 revenue could skyrocket to over $74 billion on a compound annual growth rate of 10% from 2025 to 2030. In addition to the business deals, Pfizer plans to launch a combined coronavirus influenza vaccine to counter the COVID-19 revenue slowdown. Thus, the new product could be of great interest and use to people who go for an annual flu shot, which is nearly half of the US population.

Weighing Integration Risks Against Growth Potential

The biggest risk standing in the way of Pfizer bouncing back and generating robust growth is failure to integrate the new businesses fully. Integration of the $43 billion acquisition of Seagen is a challenge, making it impossible for the company to generate optimum value from it.

Integrating a significant acquisition is difficult, as the company must merge different corporate cultures and research and development pipelines to generate optimum value. The fact that Pfizer paid over 22x revenues to acquire a company that is not yet profitable is somewhat concerning.

Another significant risk that could affect Pfizer’s long-term prospects is the expiration of patent protection for some essential drugs. Patent expiration would expose the company to competition from generic products that could eat into its revenue base when it faces a slowdown in revenue from COVID-related products. For example, losing the patent status of Vyndaqel, a heart medication, would be a big blow for the company. Breast cancer drug Ibrance and heart drug Eliquis are other drugs at risk of losing their patent protection status.

After a disastrous 2023 that saw Pfizer go down by over 40%, it emerged as one of the cheapest stocks in the drug-making business, with its valuation declining significantly. The deep pullback raises questions about whether the markets and investors overly reacted to the company’s struggles, pushing the stock lower.

A slowdown in the COVID-19 pandemic was always expected, as the pandemic would not have lasted for long. On the other hand, the stock appears undervalued and is trading at discounted levels. It trades with a forward P/E of 13 times, much lower than an industry average of 21.

The much lower forward P/E ratio implies investors are heavily discounting the stock. Analysts maintain an average price target of $40 on the stock, implying that the stock could gain about 48% from current levels.

Bottom Line

Pfizer is a big player in the healthcare sector, given its arsenal of products that address various medical conditions. While the stock has underperformed the past year, investors might have overreacted, given its performance at the height of the pandemic. Even though COVID-related revenues are declining at an astronomical pace, the company has all its bases covered to cover the continued weakness in the segment.

Q2 2024 Earnings Call Transcript")