Westend61/Westend61 via Getty Images

Stratasys (NASDAQ:SSYS) is an Israeli-US company among the leading global manufacturers of 3D printers and consumables used in the additive manufacturing industry. If interested in the industry, here are my previous articles on Materialise NV (MTLS), 3D Systems Corporation (DDD), Proto Labs (PRLB), Xometry (XMTR), and The 3D Printing ETF (PRNT). Over the past 3 years, the company has faced several unfavorable economic factors, including the high-interest rate environment limiting demand for 3D printers, new product development, and experimentation with new manufacturing processes. In addition, I believe the conflict in Israel is an important risk factor to consider given the high number of employees and assets the company has in the Jewish state. Nevertheless, Stratasys remains one of the leaders in the industry, with particular specialization in polymer-based processes. In 2024, SSYS began selling the new F3300 3D printer, printing twice as fast as currently existing models, receiving the attention of giants such as Toyota, among the first buyers of this product. In addition, starting in 2023 the company launched the GrabCAD Print Pro platform, a subscription-based service facilitating the printing process for FDM and SLA 3D printers. I believe that these 2 elements, combined with the growth in the consumables business unit, can represent a turning point for the company, allowing it to emerge from this economically adverse moment. What’s more, recent M&A deals involving Stratasys indicate a perceived undervaluation of the stock, also confirmed by my analysis of multiples yielding a target price of $16.7, c.a. 30% above the current price. Please appreciate that such multiples analysis was limited to the EV/sales ratio due to the non-profitability of SSYS. Overall, I rated SSYS stock as a Hold, as the potential return is sizable, but given the current risks involved, it could not be suitable for the most risk-averse investors. In the following sections, I will look at SSYS’s business units, new interesting initiatives, recent M&A bidding, and financial performance, to provide an insightful justification for my outlook on the stock.

Consumables segment as a catalyst for growth

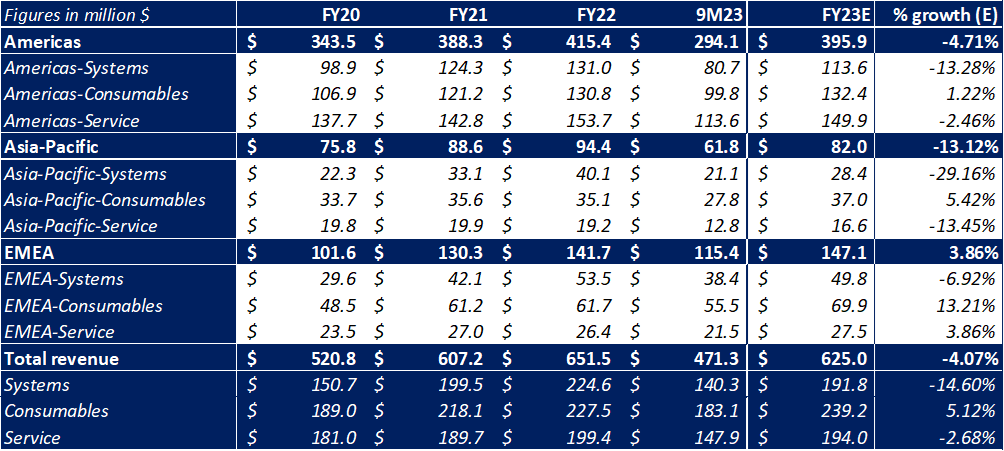

Stratasys’ activities are mainly structured around three business units: Systems, Consumables, and Service. Below you will find a breakdown of historical and expected revenues, a brief description by individual BU, and my views.

SSYS SEC Filings and Author’s Analysis

Systems is engaged in developing and selling, also through resellers, a wide range of 3D printers with a focus on thermoplastic polymer-based processes such as FDM and SLA. The business unit, after the trough in revenues in FY20 due to the pandemic, rebounded in FY21 and FY22, but in FY23 still experienced a weakening in both revenue and operating results due to the high interest rate levels limiting business investment. I anticipate that the launch of the new F3300 will have a positive effect on sales in both FY24 and 2025, especially in the event of declining interest rates that would encourage more investment by companies in the major end-markets that SSYS refers to.

Consumables is engaged in the sale of consumables such as filaments or powders that are used in 3D printing processes. Between FY20 and FY23, it grew in each of the fiscal years and in each of the geographic regions in which Stratasys operates, reaching a CAGR of 8.1%. I believe this Business Unit could be the best growth driver in the short and medium term. That is because the new printer models just released will make the Additive Manufacturing processes increasingly efficient, intensifying the use of this technology by many industries and in healthcare. The sale of more 3D printers will increase the amount of production consumables required, thereby facilitating the achievement of economies of scale in the production of these materials (especially polymers). Furthermore, the new faster printers require a higher amount of material per unit of time, having a further expansive effect on the sale of consumables used in production processes.

Service offers non-binding 3D printer maintenance services, contracted after the warranty period expires, which lasts from 90 to 365 days. On-demand manufacturing services and GrabCAD subscriptions are provided as well, services that are more capable of generating recurring revenue compared with the other two Business Units. It experienced a growing trend between FY20 and FY22, then a slight decline in FY23. In my opinion, it could become one of the key areas to drive margins to positiveness in the next 3 years. However, it must be stressed that there remain risks, starting with the competition that is strong in both software and on-demand manufacturing with companies such as Proto Labs, Materialise, and Xometry among the main competitors.

Some interesting healthcare initiatives

Stratasys is also active in the healthcare sector, where in addition to selling 3D printers, it has launched two new product lines, for a total market of several billion according to estimates in the Q3 2023 presentation.

TrueDent is a patented and FDA-approved (Class II) resin developed for the 3D printing of temporary dentures, crowns, and bridges. Soon, the technology may also be approved by the European regulatory body, further aiding the company’s expansion possibilities in a great economic potential sector. The aging population in developed countries may indeed favor further enlargement of this $5B market, again according to Stratasys management estimates.

Through Go Orthotics, SSYS is planning to manufacture custom orthopedic insoles using the SLA process, to provide complete product customization for the end customer.

These two initiatives highlight SSYS’s commitment to healthcare, a factor that I believe is very positive due to the high margins associated with this sector compared to those achievable with sectors such as automotive or aerospace.

M&A transactions signal value

Stratasys was recently the subject of several takeover and merger offers from competitors such as Nano Dimension (NNDM), Desktop Metal (DM), and 3D Systems which also involved spending about $17.3m on hostile takeover defense activities.

In March 2023, Nano Dimension submitted a cash offer of $18 per share, that was repeatedly raised and always rejected by shareholders. In July and September 2023, 3D Systems made two different offers: the first $7.5 cash per share and the remaining newly issued shares for a total price of $23.6 a share; the second $7 cash per share and the remaining newly issued shares for a total price of $15.3. Both offers were again rejected by shareholders and deemed financially risky by management, given the negative financial results of any combination of the two companies. In 2023 SSYS has also been proposed to merge with Desktop Metal, an offer that was welcomed by the CEOs of both parties but rejected by a 78.6% majority at the extraordinary meeting of Stratasys shareholders. Finally, in December 2023, Nano Dimension proposed a preliminary offer of $16.5 cash per share, a 30% premium over the current price, a proposal for which no response has yet been received from SSYS. In my opinion, an acquisition by third-party companies is difficult, especially considering that more attractive offers have been turned down in recent months.

The numerous M&A proposals are indicative of the intrinsic value of Stratasys. Offers in cash, rather than in stock, are another factor symptomatic of the quality of the company’s assets as they carry greater financial risk for the acquirer, especially considering that these bids are submitted by companies equal in size or smaller than SSYS. Furthermore, the proposals directly involve companies with in-depth knowledge of the Additive Manufacturing industry. I believe that an M&A deal between Stratasys and a peer could be an excellent opportunity for achieving the economies of scale and synergies needed to turn a profit. However, there are multiple risks involved in this process and, in my view, the current bids would result in an extremely indebted and negative margin company even in the event of a partial purchase through stocks. This combination of factors would lead to a high need for capital before the cost synergies are visible economically, resulting in further capital increases or more debt.

Risks

The Additive Manufacturing industry is characterized by growing competition, driven by the increasing use of this technology. This, to date, has resulted in negative operating performance for almost all of the companies involved, including Stratasys. Only an increase in sales and the ability to achieve economies of scale can enable profitability and not necessarily M&A deals are the answer, given the increased solvency risk they would bring.

Stratasys customers are mainly companies in the industrial, automotive, aerospace, and healthcare sectors looking for an improvement in production processes through the investment in 3D printers. These investments are costly and take time to lead to efficient production, a reason why the current high-interest rates environment is limiting investments. The future level of interest rates may therefore be a key element to consider.

The events of October 7, 2023, “is a reminder of Israel’s peril and the growing risk to U.S. allies.” This is a major risk factor to consider, as Stratasys has 25% Israeli employees within its workforce, and 69% ($130.6m) of tangible assets are located in Israel; in particular, the headquarters and the second-largest production site are located 45 km and 20 km from the Gaza Strip border, respectively. For these reasons, a prolonged situation could lead to economic disadvantages for Stratasys.

SSYS FY22 Annual Report

Commentary on financial data

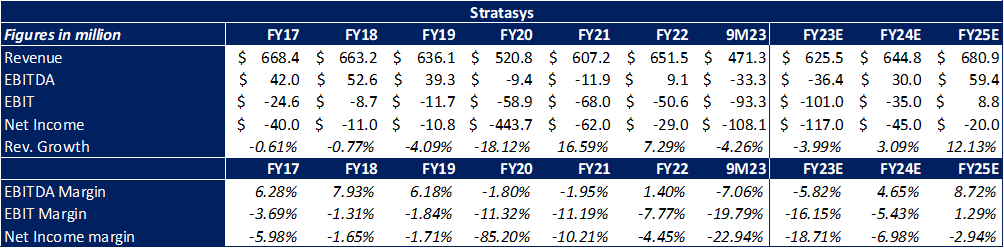

The FY23 estimate, as sourced by Refinitiv Eikon, confirms the weak momentum in the Additive Manufacturing market, with Stratasys forecasted to experience a 4% decline in revenues to $625m. The operating margins are contracting as well, reaching a historic low due to one-off costs of $17m for takeover defense and increased administrative costs. I believe that a FY23 EBITDA Margin of -5.8% (vs +1.4% in FY21) is a reasonable estimate.

The sales of the new F3300 printer, the offering of the GrabCAD Print Pro subscription platform, as well as a potential decrease in interest rates will have a positive effect on revenues, driving an expected growth by 3.1% and 12.1% in FY24 and FY25, respectively. Cost restructuring and improving sales are expected to boost marginality as well, with EBITDA margin expected to reach 8.7% in FY25.

SSYS SEC Filings, Refinitiv Eikon, and Author’s Analysis

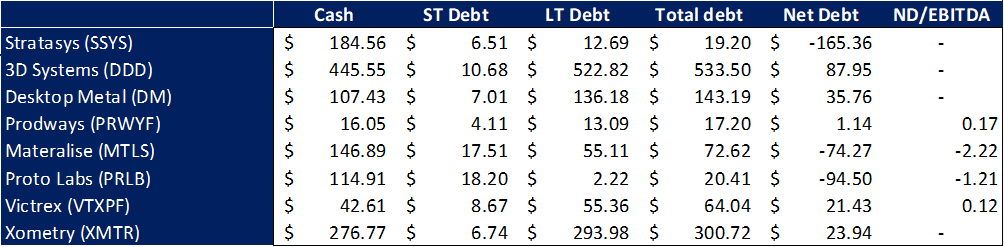

As of Sep23, the SSYS inventory is worth 31.5% of total assets, a high value but in line with other peers such as 3D Systems and Desktop Metal. The liquidity is under control both in the short term, with a quick ratio of 1.93x, and in the medium term, with a net cash position of $165m. This liquidity mainly comes from the capital increase implemented in March 2021 that raised $230m. Stratasys has indeed very low operating cash flows, insufficient to cover CAPEX and acquisitions, leading to $143m of cash burned in 9M23. Although I believe that by FY25 the company will be able to produce positive OCFs, I think it is unlikely they are sufficient to cover the investments needed for financing growth. I therefore anticipate more debt in the coming years, especially if interest rates fall. I also think new capital increases are unlikely as long as the share price remains at these levels, barring any M&A operations.

Companies SEC Filings and Author’s analysis

Valuation

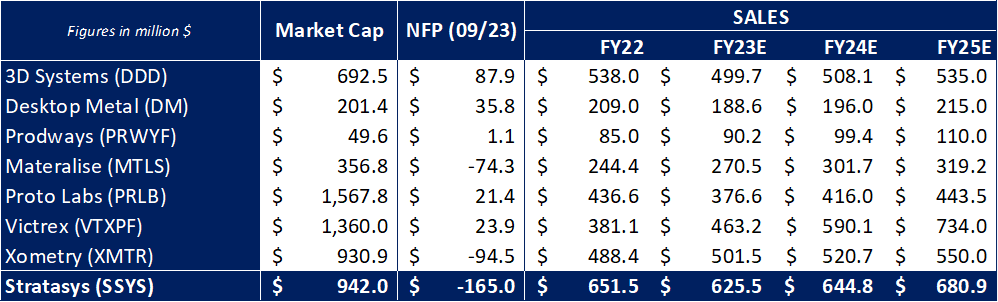

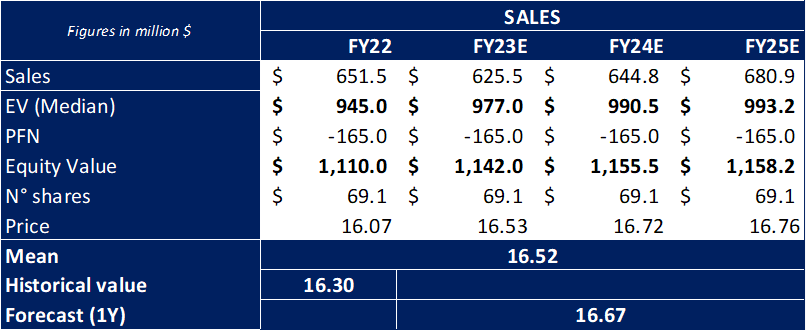

Due to Stratasys’s current unprofitable state, I was not able to perform either a DCF analysis or a multiples analysis with conventional earnings-based ratios. I obtained therefore an indicative target price solely through the EV/Sales analysis of the companies in the sample. The analysis was performed using FY22 and FY23 as historical data and FY23 (most of the sample has yet to provide the actual ones), FY24, and FY25 as perspective years (sourced from Refinitiv Eikon). The result is a share value of $16.7, c.a. 30% above the current price and in line with Nano Dimension’s recent offering.

Companies SEC Filings, Refinitiv Eikon, and Author’s analysis Companies SEC Filings, Refinitiv Eikon, and Author’s analysis

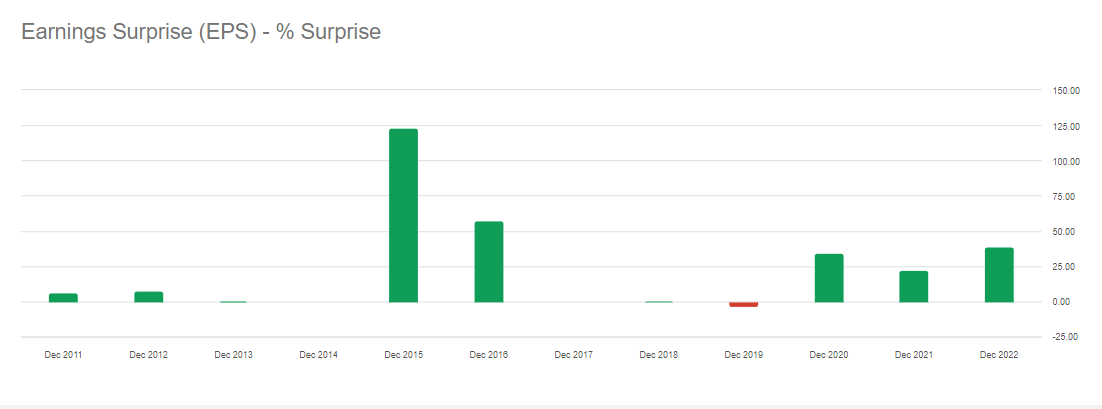

Upcoming Q4 Results

Stratasys has not yet officially announced the release date of Q4 2023 results, which are expected to be 2/27/2024. In the past three years, the year-end release has always brought an earning % surprise greater than 20%, peaking at 39% in FY22. Moreover, in the last 12 years only in FY19, the surprise was negative (-3.40%). If the recent geopolitical events had not taken an economic toll on the company, I think management may have thought of a year-end gift again this year.

seekingalpha.com

Conclusion

In my view, Stratasys is a good choice to invest in the 3D printer OEMs market, with good long-term prospects, although not supported by current results. The Consumables Business Unit could be the main driver of revenue growth, whereas GrabCAD Print Pro software and healthcare initiatives represent the key areas for improved marginality in the long run. The intertwining of M&A proposals confirms my view and may offer the opportunity for an investor to generate profits in the short term through arbitrage transactions, taking advantage of the premium of a possible takeover. However, I believe it is difficult for shareholders to accept an offer at this time after rejecting more advantageous proposals in the past year and considering the negative moment the industry is facing.

Stratasys also has multiple risks, including significant ties to Israel and a continuation of high-interest rates in the U.S. economy. For these reasons, SSYS seems suitable only for investors who believe in the industry and are willing to hold the position over a lengthy period. My EV/Sales multiple analysis resulted in a share value of $16.7, c.a. 30% above the current price, although the analysis is limited to a single ratio because of Stratasys’s current unprofitable state. Overall, I rated SSYS stock as a Hold, as the potential return is sizable, but given the risks involved, it could only be suitable for the most risk-averse investors.

Q2 2024 Earnings Call Transcript")