Douglas Sacha/Moment via Getty Images

The SPDR Portfolio High Yield Bond ETF (NYSEARCA:SPHY) and the iShares Fallen Angels USD Bond ETF (NASDAQ:FALN) are my top two high-yield corporate bond ETFs. Both offer investors strong yields, dividend growth, and total return track-records, and could see moderate capital gains as interest rates stabilize. I’ve covered both in the past, and they generally have performed quite well. Owing to the strong, but similar, value proposition of both funds, I thought a comparison was in order.

Both funds invest in high-yield corporate bonds. SPHY is a simple, broad-based index fund targeting these securities. FALN focuses on bonds downgraded from investment-grade to non-investment grade ratings.

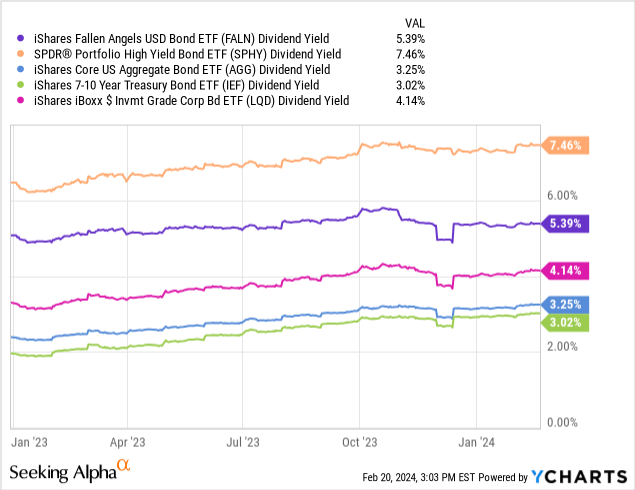

Both funds have above-average yields compared to broader bond and equity funds. SPHY yields quite a bit more, with a 7.5% yield compared to 5.4% for FALN, due to greater investments in the riskiest bonds.

Both funds have above-average total return track-records. FALN’s past returns are stronger, as the fund’s downgraded bonds have outperformed in the past. I believe that they will continue to do so moving forward as well.

Both funds focus on high-yield bonds, and so have high credit risk. SPHY is a bit riskier, but that has yet to be reflected in the fund’s performance.

Both funds have below-average interest rate risk and duration. FALN is a bit riskier in this regard, due to focusing on bonds with longer maturities.

In my opinion, both SPHY and FALN are strong investment opportunities, and buys. On net, I believe FALN to be the stronger choice, due to its proven investment strategy and performance track-record. SPHY does yield quite a bit more, an important consideration for many investors.

Strategy and Holdings Comparison

FALN – Fallen Angel Index ETF

FALN invests in fallen angels, or bonds downgraded from investment-grade to non-investment grade. As an example, a bond with a BBB rating downgraded to BB would qualify as a fallen angel.

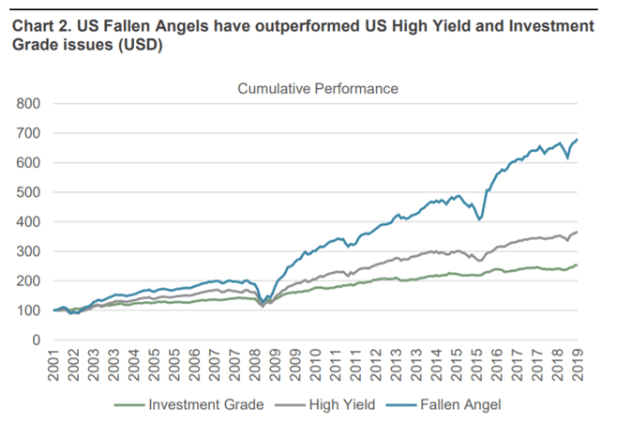

Fallen angels tend to outperform due to structural issues with bond markets and bond investors. Some large institutional investors are constrained from holding non-investment grade bonds in their portfolios, including most of the larger bond ETFs, like the Vanguard Total Bond Market Index Fund ETF Shares (NASDAQ: BND). These investors are forced into selling their fallen angel holdings soon after their downgrade. Forced selling leads to abnormally low prices and high yields for these securities, which leads to outperformance as conditions settle.

Considering the above, fallen angels should outperform broader high-yield indexes, as has been the case for the past two decades.

FTSE Russell

FALN’s more targeted portfolio means lower diversification, but higher potential total returns. The investment rationale behind fallen angels seems strong, in theory and in practice.

SPHY – Simple High-Yield Corporate Bond Index ETF

SPHY is a simple high-yield corporate bond ETF. It does not target a specific niche within this asset class, unlike FALN.

SPHY’s broader portfolio means higher diversification, somewhat reducing risk, but also limiting the possibility of significant, outsized gains.

On net, FALN’s strategy and holdings seem stronger, but comparing strategies is not straightforward, and some investors might prefer the greater simplicity and diversification of SPHY.

Risk Comparison

Diversification

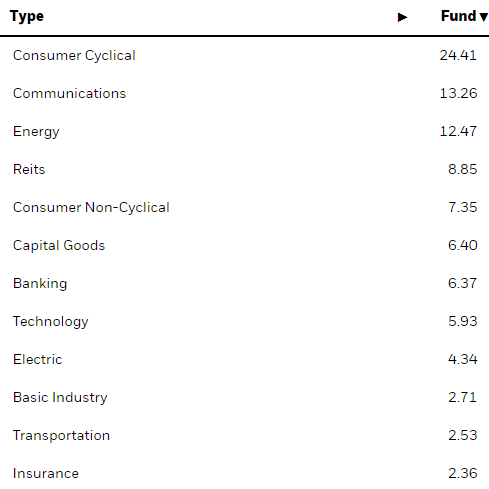

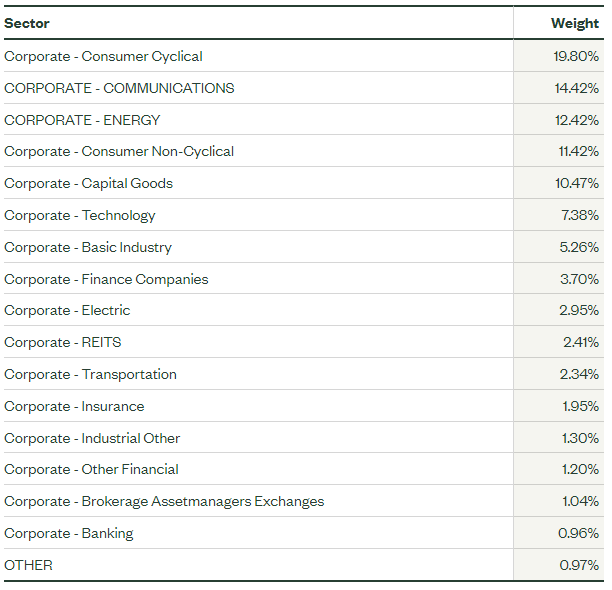

SPHY is a much broader fund, investing in high-yield corporate bonds of most types, unlike FALN, which only invests in a sliver of these. Due to this, SPHY holds many more bonds, 1,890 versus 204 for FALN. On the other hand, industry weights seem comparable, and balanced, for both funds. Weights for FALN:

FALN

Weights for SPHY:

SPHY

SPHYs broader, more diversified portfolio decreases risks somewhat, but FALN does seem diversified enough regardless.

Credit Risk

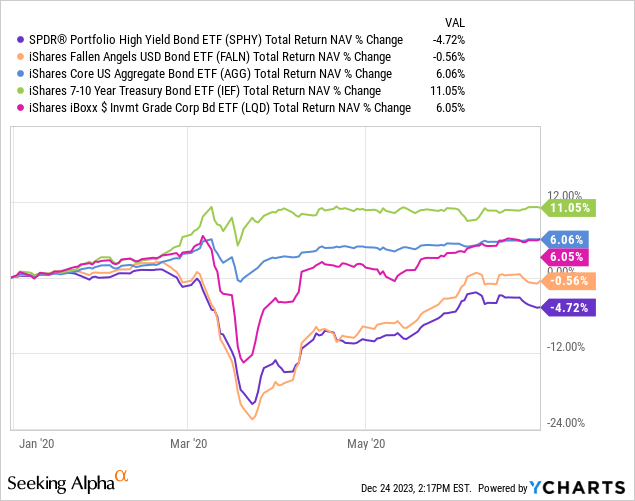

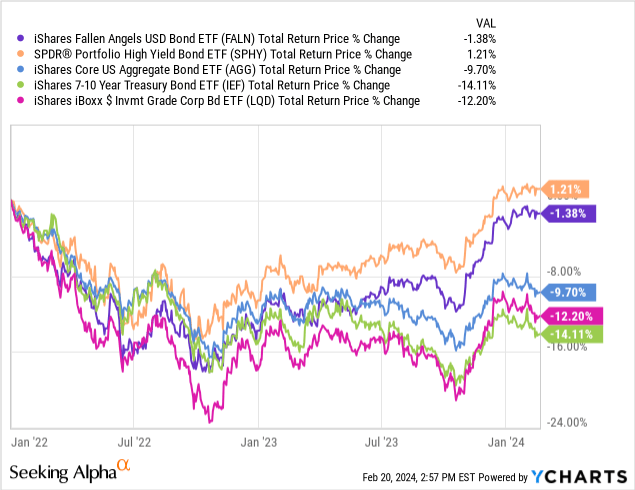

Both funds focus on non-investment grade corporate bonds with weak credit ratings and subpar performance during downturns and recessions. Both funds underperformed broader investment-grade bond indexes during the most recent recession, early 2020, as expected.

Data by YCharts

Notwithstanding the above, there are some differences in credit quality and risk between the funds.

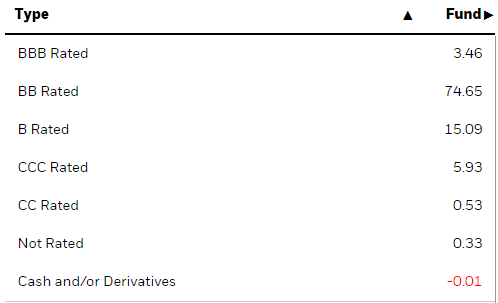

SPHY invests in high-yield corporate bonds of all credit qualities, focusing on BB an B-rated bonds, but with sizable investments in those rated CCC.

SPHY – Table by Author

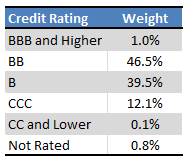

FALN focuses much more strongly on bonds rated BB, as this is the highest non-investment grade rating, and fallen angels rarely fall so low. It does hold sizable investments in BB and CCC-rated bonds, but weights are much lower than those of SPHY.

FALN

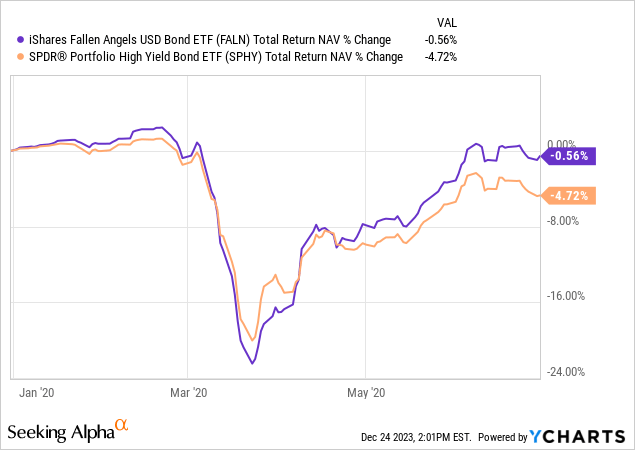

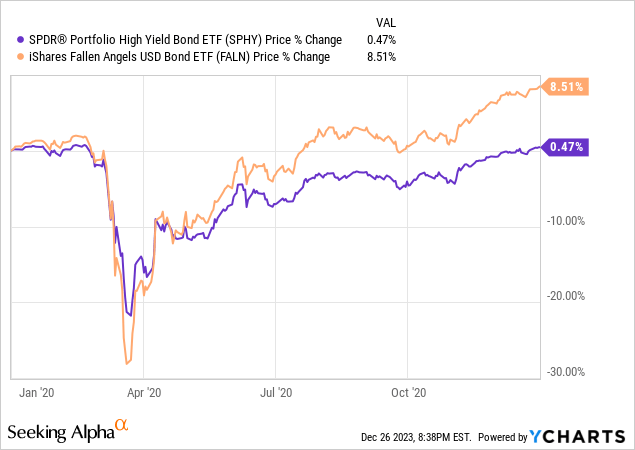

Although both funds have high credit risk, FALN focuses on bonds with somewhat higher credit quality, and so has moderately less credit risk than SPHY. Due to this, FALN should outperform SPHY during downturns and recessions. FALN saw a somewhat higher drawdown during early 2020, the most recent recession, but recovered somewhat faster from these. Results were a bit worse than expected, but still broadly positive.

Data by YCharts

FALN’s moderately lower credit risk reduces risk, volatility, and losses during downturns, an important advantage of the fund versus SPHY.

Interest Rate Risk or Exposure

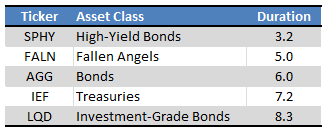

Both funds focus on non-investment grade bonds, which tend to have short maturities as investors are wary of extending long-term credit to riskier issuers. Both funds have below-average duration and hence interest rate exposure, as expected. SPHY invests a bit more heavily in bonds with particularly weak credit ratings, so its duration is a bit lower than that of FALN.

Fund Filings – Table by Author

Due to the above, both funds should outperform most bonds and bond sub-asset classes when interest rates rise, as has been the case since early 2022. SPHY slightly outperformed FALN, due to its lower duration.

On the flipside, both funds should underperform when interest rates decrease. Market interest rates have decreased since October, as investors turn dovish on Fed guidance. Neither fund has underperformed, however, due to their strong yields, and narrowing credit spreads. I still expect both funds to underperform during a period of significantly and rapidly decreasing rates, even though neither underperformed these past few months. Due bear in mind, rates have not significantly, nor rapidly, decreased.

On net, I believe that the lower interest rate risk or exposure of both funds is a positive, as it decreases long-term portfolio risk and volatility. More dovish investors might disagree.

Overall Risk Assessment

Overall, both funds have broadly similar levels of risk and volatility. SPHY has a bit more credit risk, FALN a bit more rate risk, but these are small differences, all things considered.

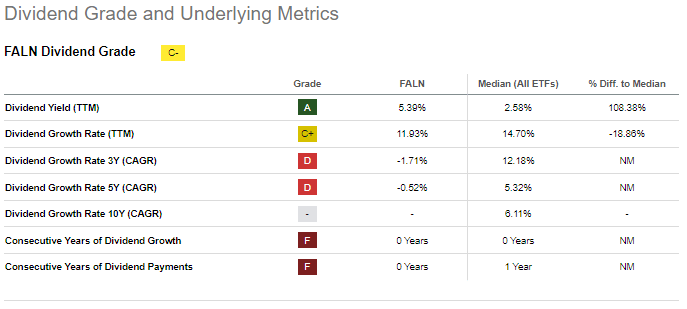

Dividend Comparison – SPHY Clear Winner

Both funds focus on non-investment grade corporate bonds, with above-average yields. On the other hand, SPHY invests more heavily in riskier, higher-yielding bonds with particularly weak credit ratings, and so yields quite a bit more than FALN.

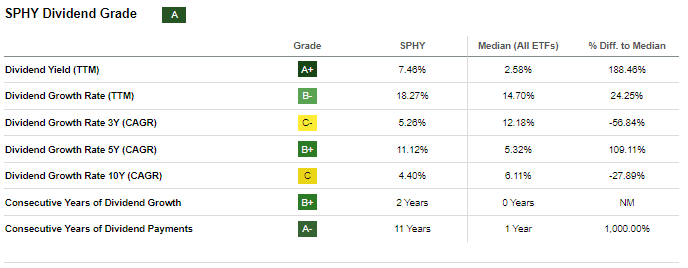

SPHY’s dividend growth track-record is also quite a bit stronger, and longer, than that of FALN. Lots of volatility in these figures, however.

Seeking Alpha

Seeking Alpha

SPHY’s strong, growing 7.5% yield is the fund’s most important benefit and advantage relative to FALN.

Capital Gains Comparison – FALN Slight Winner

Bonds are income vehicles, so returns for both funds should mostly consist of dividends. Nevertheless, right now both funds could see minor, perhaps moderate, capital gains due to prior rate hikes. These caused bond market prices to drop, but bonds must always be paid back, in full, at maturity. As this occurs both funds should see some capital gains.

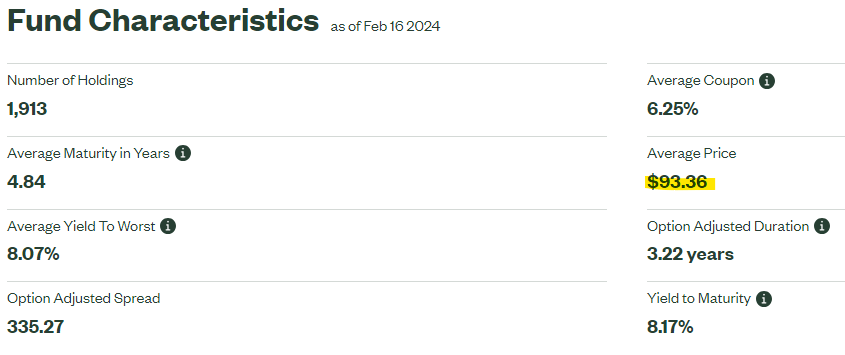

As an example, right now SPHY’s underlying bonds trade with an average price of $93.40. When these mature, the fund should receive $100, for 7.0-8.0% in potential capital gains.

SPHY

As per my calculations, FALN’s underlying bonds trade with a price of $91.80, for 8.0-9.0% in potential capital gains.

Both funds could see even further capital gains from narrowing credit spreads and credit upgrades. Gains are generally permanent or semi-permanent when bonds are upgraded to investment-grade, as high-yield bond funds must divest themselves from these, locking-in gains. This is particularly common for fallen angels, so FALN’s gains could conceivably be higher than those of SPHY. As an example, the fund’s share price increased 8.5% during 2022, in large part due to these issues.

Data by YCharts

Although both funds are mostly income vehicles, investors could see some capital gains from each. FALN’s gains could be somewhat higher, an advantage relative to SPHY.

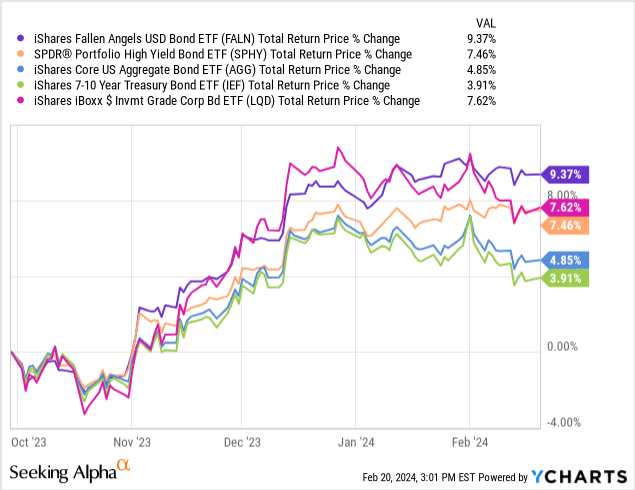

Performance Comparison – FALN Clear Winner

Both funds outperform most bond and bond sub-asset classes consistently, due to focusing on non-investment grade bonds with above-average yields.

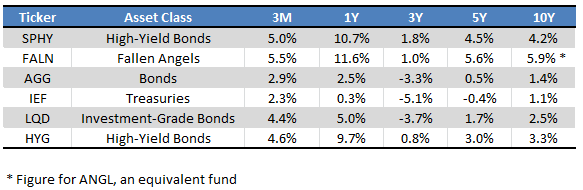

On the other hand, FALN’s performance is quite a bit stronger than that of SPHY, due to focusing on fallen angels, the best-performing bond sub-asset class. Long-term, FALN’s annual returns have been about 1.5-2.0% higher than those of SPHY, an important spread.

Seeking Alpha – Table by Author

In my opinion, FALN’s outperformance was due to structural market issues leading to fallen angel outperformance and will likely continue long-term. This is FALN’s most important benefit, and advantage relative to SPHY.

Conclusion

SPHY and FALN are two strong high-yield corporate bond ETFs, and my top two picks in the space. In my opinion, choosing between these two funds is relatively simple.

Investors can choose SPHY’s higher yield, FALN’s stronger returns, or some combination of both. I would personally go for FALN, but some investors might prefer SPHY’s higher yield.

Q2 2024 Earnings Call Transcript")