Anton Petrus/Moment via Getty Images

We get the love for tower REITs in general and SBA Communications (NASDAQ:SBAC) in particular. A strong growth story with sticky customers and one that gives you a big diversifier over the traditional brick and mortar REITs. There is little to make a strong bear case on. While we did not make a bear case on these, we refused to buy the bull story. We go over the fundamentals today, the trade we suggested last year, and update our buy point.

Current Setup

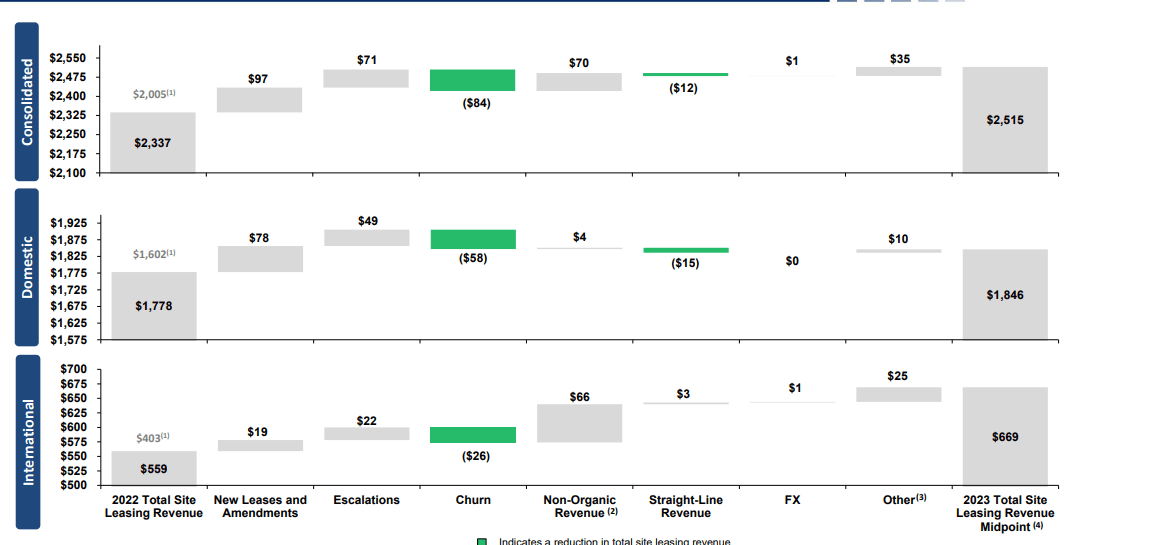

The last earnings were released some time back, and we are almost due for Q4-2023 numbers. SBAC delivered solid results, with a good beat on funds from operations (FFO) and a small one on revenues. The guidance was good and SBAC continues to show solid growth domestically and abroad.

SBAC Q3-2023 Presentation

If you were looking for weakness in any channel, you did not find it.

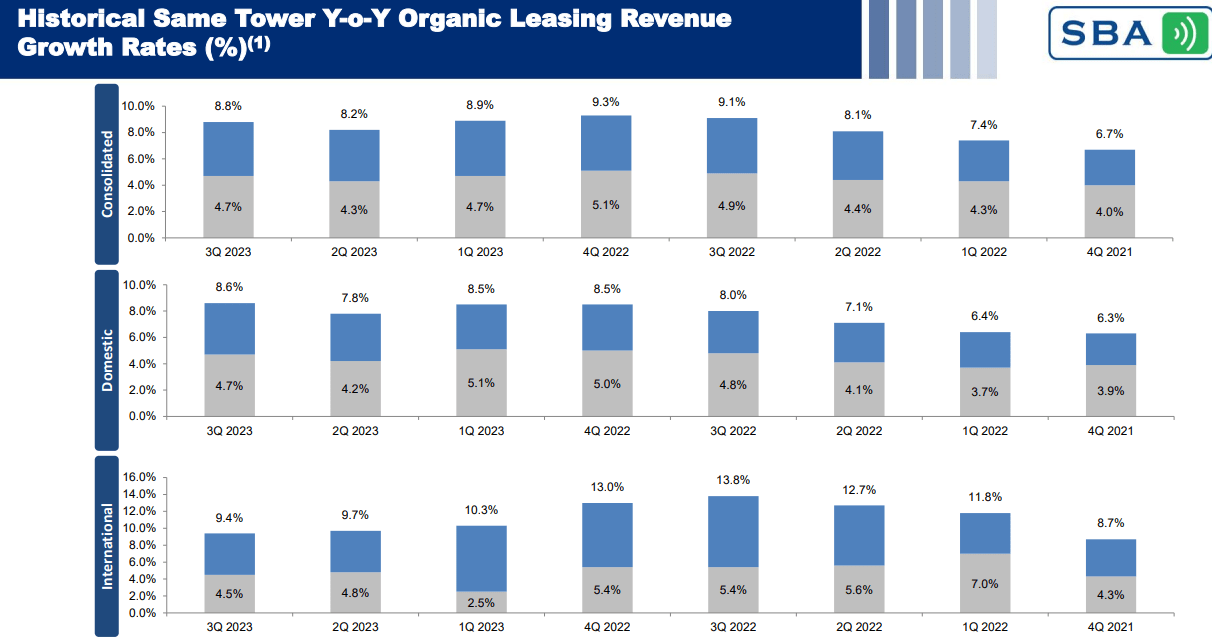

SBAC Q3-2023 Presentation

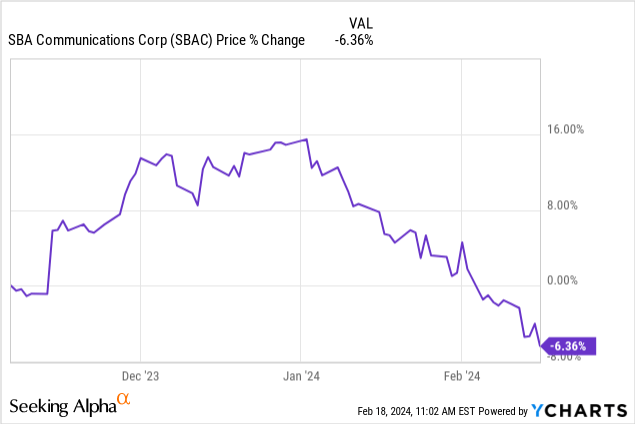

That, alongside the oversold nature of the stock, set off a rip-roaring rally. The stock has given back all of it and more.

What’s going on here?

Outlook

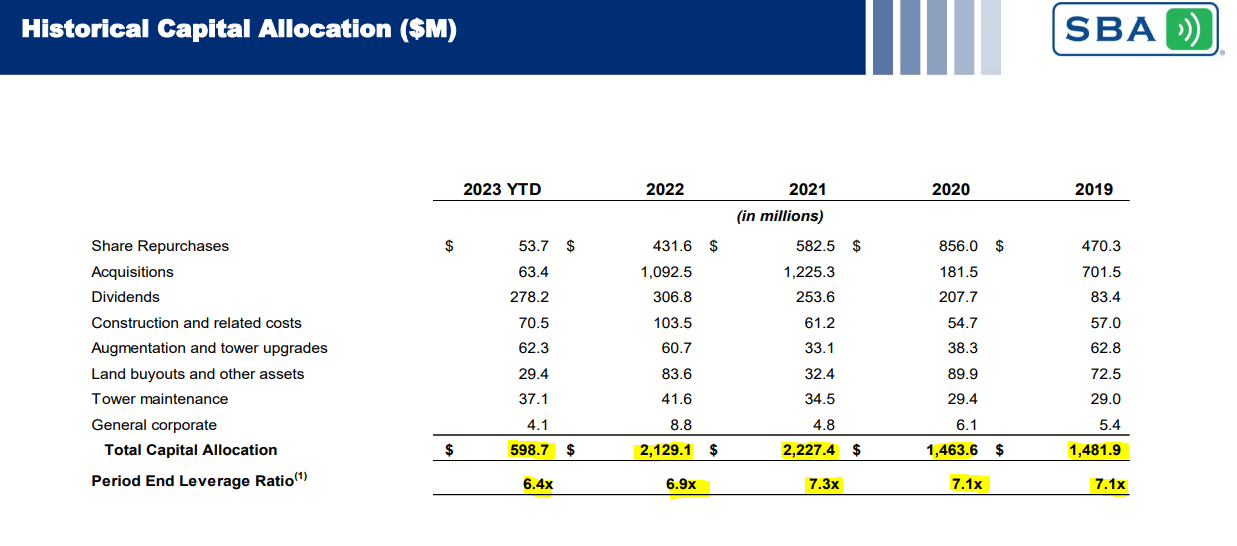

It was impossible to find fault with the capital allocation policy. You can see how SBAC was big on acquisitions in the past few years and then got that to a screeching halt in 2023.

SBAC Q3-2023 Presentation

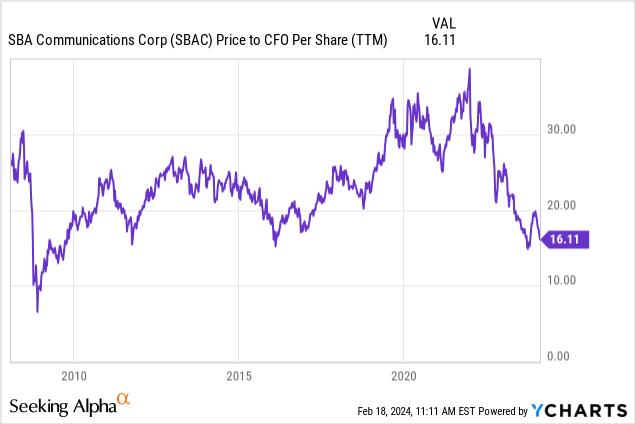

Where did the rest of the money go this year? It is clear that three quarters of the 2022 cash flow is way above the $600 odd million allocated. Well, the rest went towards debt reduction, and it shows in the period end leverage ratio. 6.4X is way better than 7.1X, which we had calculated in our May 2023 article. There had been a methodical compression of the valuation multiple as well. Price to cash flow has come down from the lofty 35X numbers, and we are now down to just 16X.

While it is easy to blame an irrational market for the valuation compression, the fact is that SBAC was possibly one of the worst priced REITs at 2021 highs. You had to see that at a 35X multiple, where the stock was well over two standard deviations over its previous 10-year average. Even now, as we compress into 16X, keep in mind that growth estimates are really winding down.

Seeking Alpha

Those are likely to prove sub inflationary growth rates. As in, CPI measures are likely to exceed these numbers. We also see substantial downside risk to these numbers. In a hard landing and our base case for a higher move in the US dollar, we think SBAC will struggle to hit these FFO estimates. The latest payroll data looked strong, but things were poor under the hood. So we would not jump to the conclusion that these numbers are written in stone.

SBAC is also still carrying a rather massive debt load. 6.4X is not what we would consider low or even average for this company. Its weighted average debt maturity is not very impressive either. SBAC referenced this in their latest refinancing.

The Company also increased its existing Revolving Credit Facility from $1.50 billion to $1.75 billion and extended its maturity to January 2029. Amounts borrowed under the Revolving Credit Facility will accrue interest at Term SOFR (with a 0% floor) plus a margin that ranges from 112.5 basis points to 150.0 basis points, based on SBA Senior Finance II’s leverage. Pro forma for this transaction, the weighted average maturity of SBA’s total debt outstanding increased from 3.2 years to 4.1 years.

Source: SBAC

Maybe if we went back to ZIRP (zero interest rate policy). But in the absence of that, we think we would see lower price to AFFO and lower EV to EBITDA ratios in the months to come.

Previous Trade

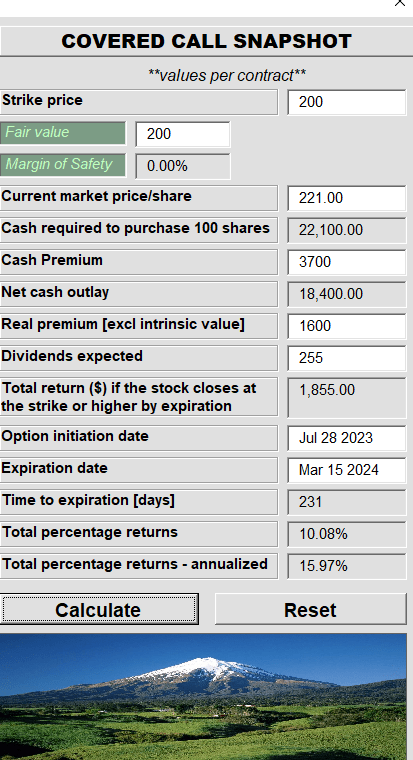

In July 2023, we had suggested investors throw out the past growth expectations and aim for modest returns via a covered call. The strike we chose was $200 and this has played out rather interestingly as we get into the March 2024.

Looking For That Buy Point, SA Article July 2023

While the stock is down about 6.5% since then, the covered call is up as the call premium has compressed from $37.00 to $11.50. Your gain on the option, plus the dividends, have offset the stock decline. At this point, we think the risks are high that the option buffer may not hold until the March expiration. We would strongly consider rolling this to December 2024 for the same strike. We estimate that this could give you $19.00 of net credit. If you did that, you would improve your net cost basis from $184.00 at the start of this trade, all the way to $165.00. We think that is a price we can get behind.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

Q2 2024 Earnings Call Transcript")