P A Thompson/The Image Bank via Getty Images

Introduction

Academy Sports and Outdoors (NASDAQ:ASO) is a sports, outdoor product and firearm retailer currently with 285 stores across 18 states, mostly located in the South. For people who do not live in the South, ASO is basically DICK’S Sporting Goods (DKS) but only in the South, plus they sell firearms whereas DICK’s does not.

ASO was a turnaround story when in 2018, Ken Hicks, who turned around Footlocker was hired as the CEO of ASO and was able to successfully do so again with ASO, turning a declining business into a reinvigorated franchise with a clear vision of growth beyond 2023.

Ambitiously, the company expects to reach $10 Billion in revenue in 2027, which is over 50% growth from $6.11 billion revenue TTM. Herein, I will examine the growth levers of ASO and explain how ASO will be able to reach the hefty sales target.

Growth lever 1: New ASO Stores + Excellent Store Economics

The main revenue driver in the next 5 years will be store expansion. The management expects to add another 50% of the total number of ASO stores from 2022-2027. That is about 120-140 stores over the 5-year period, and they are ramping up this effort. ASO added 9 stores in 2022, while in 2023 so far it has added 14 new stores in 2023 (first 3 quarters), and will probably finish the year adding a total of 20 new stores.

It takes new ASO stores four to five years to ramp up from about $18 million in sales in its first year to an ideal $24 million in sales. If we assume that ASO will be successfully adding 130 stores from 2022-2027, and by 2027 these new stores will have an average sale of $21 million/store, the store expansion will add $2.73 Billion in sales by 2027. In doing so, store expansion alone will bring AOS 2027 revenue to about $8.8 Billion, assuming no change to same-store sales (SSS), which is also likely to increase as I will explain later.

The store expansion plan builds on excellent store economics. ASO’s store is more profitable than its largest competitors, with ASO’s average store EBIT sitting at $4 Million vs. $2 Million for its competitors. All the ASO’s stores are profitable and the new stores self-fund their own growth, which is a testament to its high ROI. According to the management, the newly opened stores have an average ROIC of 20% and turn EBITDA positive right after the 1st year.

ASO takes the lead in store efficiency as well. For sales per sq ft, ASO stood at $340 per sq ft vs. $290 per sq ft for DICK’s. Also, for sales per store, ASO stood at $24 Million vs. 14 Million per store sale for DICK’s. Same with EBITDA per store. These strong numbers speak to ASO’s store efficiency and the effectiveness of its omnichannel strategy.

ASO vs Others in Store Productivity (ASP presentation)

Growth lever 2: Same-Store Sale (SSS) growth

The global Sporting Goods market is expected to expand at a CAGR of 3.83% from 2023 to 2031. This is not surprising given that retail sales take up a consistent portion (5.5-6%) of GDP over the years, so retail growth basically tracks GDP growth. For ASO, this will likely translate to even higher SSS because of two main reasons: 1) ASO has been gaining market shares in various retail categories. 2) It operates in the fastest GDP growth states.

Firstly, ASO has been gaining shares in the growing industry of recreational goods. From 2019-2022, it has gained market shares in most leading product categories, with Apparel gaining 44 bps, Footwear 36 bps, firearms 25 bps, team sports 10 bps, and fishing equipment 8 bps. These are the results of transformed customer experience at ASO and ASO’s restored reputation. In 2022, ASO reported its Net Promoter Score (NPS) to be 43, higher than the well-known customer-obsessive Amazon (37), and much higher than its competitor DICK’s (26).

In addition, ASO operates in states with the fastest GDP growth, especially Texas. ASO has 285 stores across 18 states in the South, with 111 stores, which is about 39% of all Academy Sports Outdoors stores in the US, located in Texas.

ASO Store location (Scrapehero)

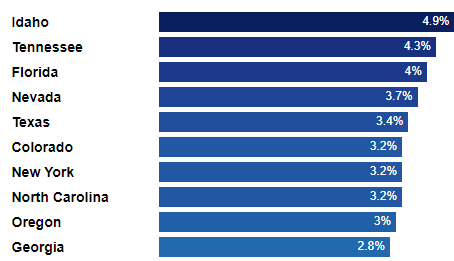

Texas is one of the fastest growing states both in terms of GDP and population. As you can see in the chart below, in the top 10 states with the fastest growing GDP, Texas ranked #5, and 6 were covered by ASO’s store locations. While in the top 10 States with the fastest growing population, Texas ranks #1, and 6 were covered by ASO’s store locations. In addition, it is beneficial to the bottom line that these states ASO operate in tend to be more business friendly from a corporate tax perspective. For example, Texas has no corporate tax rate, whereas CA has a flat 8.84% corporate tax rate.

ASO has demonstrated in the past that it is fully capable of increasing its SSS. From 2018 to 2023, its SSS had an impressive CAGR of ~4.5-4.7% (essentially the same as revenue CAGR because it had very little store expansion over the past 5 years). As the population and GDP in Texas and other key states continue to grow, and as ASO continues to gain market shares in its retail space, I expect a modest 1-2% SSS CAGR for ASO over the next 5 years When coupled with the 130 new stores expansion, SSS will contribute about $0.6-1 billion in revenue in 2027, bringing the previously projected 2027 revenue of $8.8 billion to $9.4-9.8 billion, very close to the $10 billion target.

2022 GDP Growth for Different States (World Population Review) Population growth expectations for different states (ASO presentation)

In addition, ASO’s online presence continues to expand and was able to meet its ecommerce sales goal of reaching 10% of total sales a year early, in March 2023. These are good trends that should help with the same store sales growth in the future for ASO.

Growth Lever 3: Share Buyback

The company has been aggressively buying back shares. Specifically, it spent $426.8 Million in 2021, $490.7 Million in 2022 and $306.7 Million in the past 12 months buying back shares. Since Sep. 2021, ASO has reduced the total shares outstanding from 93.5 Million to 74.15 Million, or 20.7% of total shares, which is very investor-friendly, and gives a healthy boost to its EPS.

ASO Total Shares Outstanding (YCharts)

Valuation

We look at three scenarios using the DCF model 10 years out.

1. Worst-case scenario, assuming a 10-year average net margin of 6%, 2% revenue growth rate (3% from store expansion, -1% from SSS growth) from 2026-2032, rate of return at 9% and perpetual growth at 1%, we reached a fair value of $55.56 per share, indicating ASO is overvalued today.

ASO DCF Worst case (Author)

2. Base-case scenario, assuming a 10-year average net margin of 7%, 5% revenue growth rate (4% from store expansion, 1% from SSS growth) from 2026-2032, rate of return at 9% and perpetual growth at 2%, we reached a fair value of $89.5 per share. Using today’s ASO stock price of $70.84 per share, ASO currently has a 26.3% upside.

ASO DCF Base Case (Author)

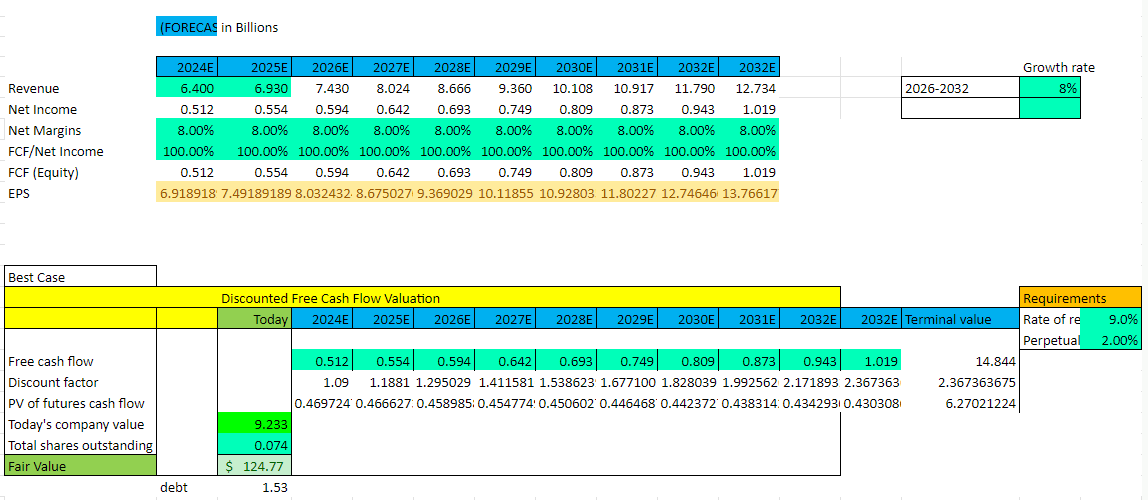

3. Best-case scenario, assuming a 10-year average net margin of 8%, 8% revenue growth rate (6% from store expansion, 2% from SSS growth) from 2026-2032, rate of return at 9% and perpetual growth at 2%, we reached a fair value of $124.77 per share, or a 76.1% upside from today.

ASO DCF Best Case (Author)

Risks And Final Remarks

The biggest unknown is the broader economy, as discretionary spending tends to drop significantly in an economic downturn. The majority of ASO’s customers are middle class, who are even more sensitive to the macro environment. Nonetheless, it is looking hopeful for a soft landing this year, and possible rate cuts later this year. All are good signs that the economy might actually reach a soft landing.

As a long-term investor, I ignore the macro noise and just look at the company itself. For ASO’s next earning report, I will be closely monitoring its SSS and I want to see a deceleration in SSS decline, as well as the store expansion plan where I will be looking for acceleration. Both are important to gauge if they are on target for $10 billion in revenue in 2027.

In summary, with ASO, I see a brilliant management team that has already turned around the sinking ship in the past 5 years and a growth story that likely will play out nicely in the next 5-10 years. As such, I give ASO a Buy rating.

Q2 2024 Earnings Call Transcript")