Bloomberg/Bloomberg via Getty Images

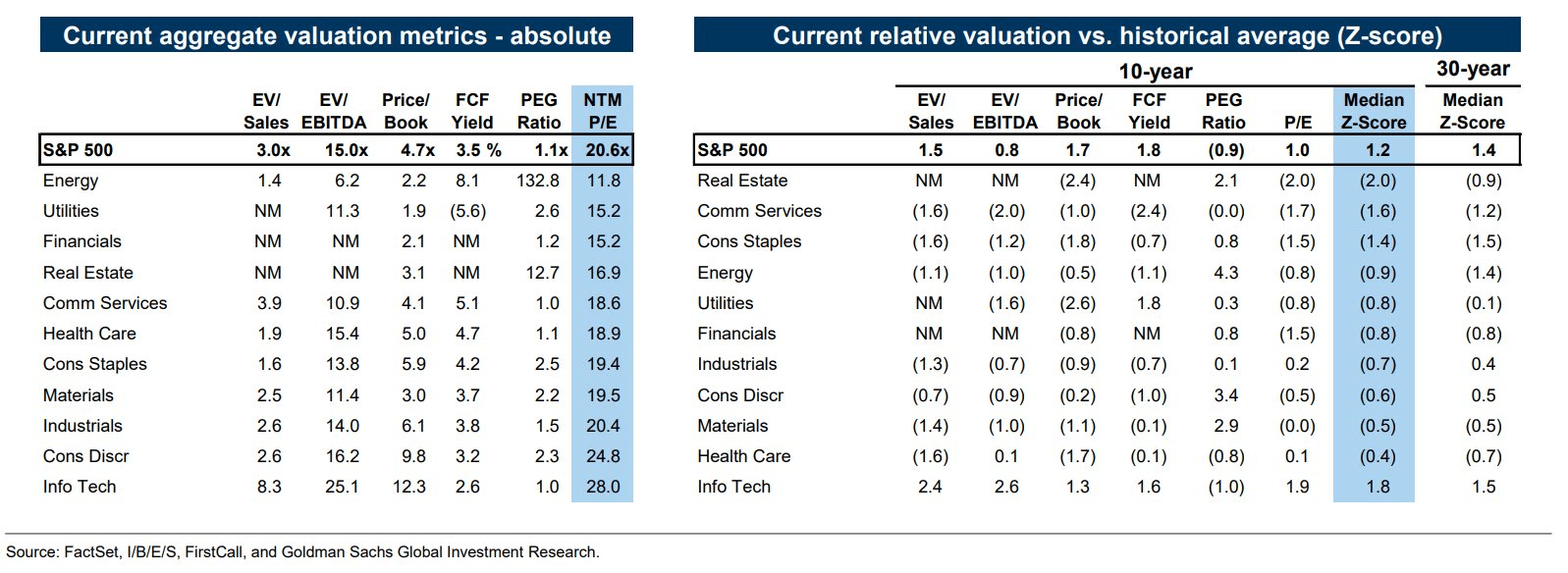

Valuations continue to turn more stretched. While the Information Technology sector is the priciest across several metrics, the Consumer Staples space sells for a lofty 19.4 times forward operating earnings estimates, according to Goldman Sachs using FactSet data. A valuation premium is often deserved for defensive earnings growers that can withstand periods of economic distress, but investors should always reflect on how much is being paid for that safety net.

I reiterate my buy rating on shares of Coca-Cola FEMSA, S.A.B. de C.V. (NYSE:KOF). The stock now trades at 18.7 times 2024 earnings estimates, but quality profit strength over the next handful of quarters, a high yield, positive free cash flow, and an uptrending chart are positives.

Staples Stocks Nearing 20x Earnings

Goldman Sachs

According to Bank of America Global Research, Coca-Cola FEMSA is the largest bottler for The Coca-Cola Company (KO) outside the US, with total sales volumes of around 4 billion unit cases, serving more than 375 million people. It manufactures and distributes Coca-Cola products in Argentina, Brazil, Colombia, Costa Rica, Guatemala, Mexico, Nicaragua, Panama, and Venezuela. KOF is controlled by FEMSA and KO, according to a shareholders’ agreement.

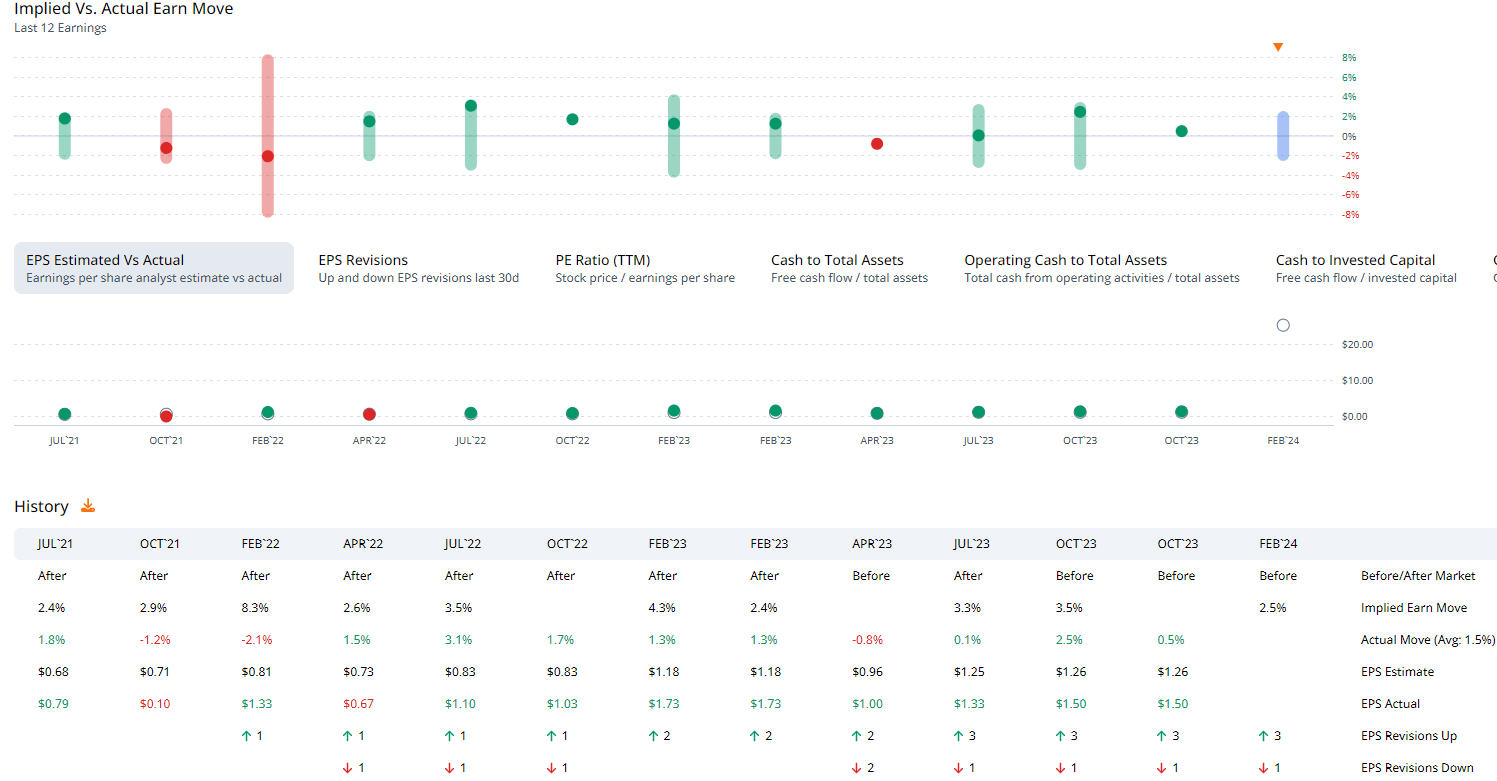

Ahead of earnings later this week, KOF trades with a moderate 24% implied volatility percentage, and the options market has priced in a very small 2.5% earnings-related stock price swing when assessing the at-the-money straddle expiring soonest after Thursday’s reporting date, according to data from Option Research & Technology Services (ORATS). Having topped EPS estimates in each of the previous eight quarters with positive share-price reactions after seven of those eight beats, there is a bullish underlying trend at play here. Seeking Alpha shows a consensus operating EPS figure of $1.62 expected to be reported this Thursday morning.

KOF: A String of EPS Beats, Positive Share-Price Reaction History

ORATS

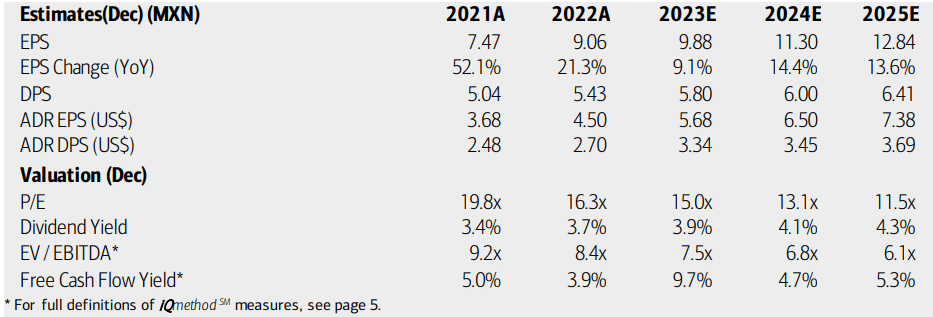

On valuation, analysts at BofA see earnings having risen more than 9% last year, while per-share profit growth is forecast to be stout in the low to mid-teens through 2025. The current consensus per Seeking Alpha reveals 14% bottom-line growth this year, with EPS advancement decelerating to 10% in the out year. Top-line growth is solid, in the mid-single-digit range in 2024 and 2025.

Dividends, meanwhile, are expected to rise commensurate with earnings growth, leading to an expected dividend yield of around 4% over the coming quarters. With an EV/EBITDA now near 9, the valuation is a bit stretched compared to the stock’s history, and the current free cash flow yield is just under 7% – an impressive number.

Coca-Cola FEMSA: Earnings, Dividend, Valuation, Free Cash Flow Forecasts

BofA Global Research

While the growth trajectory is robust, the valuation has become a risk now that shares are up by more than 40% from the October 2023 low. If we assume normalized EPS of $6.30 over the next 12 months and apply the stock’s 5-year average earnings multiple of 17.2, then shares should be priced near $108, limiting potential upside to just $8 as of the close last Friday. Thus, it’s borderline between a hold and a buy, but I will keep my buy rating for now given the yield and free cash flow strength.

Decent Valuation Metrics, But No Longer A Value Play

Seeking Alpha

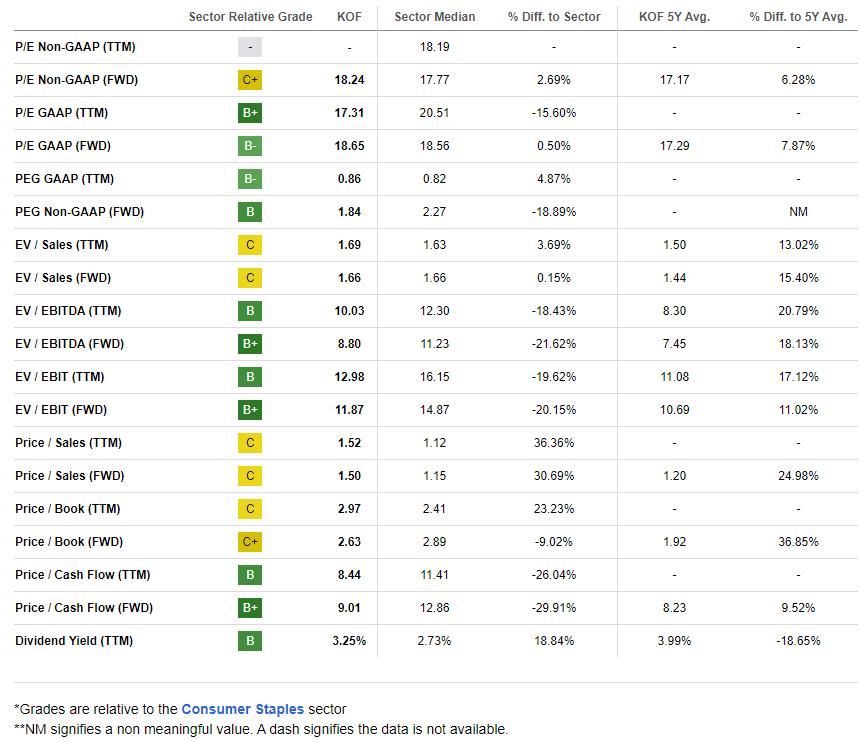

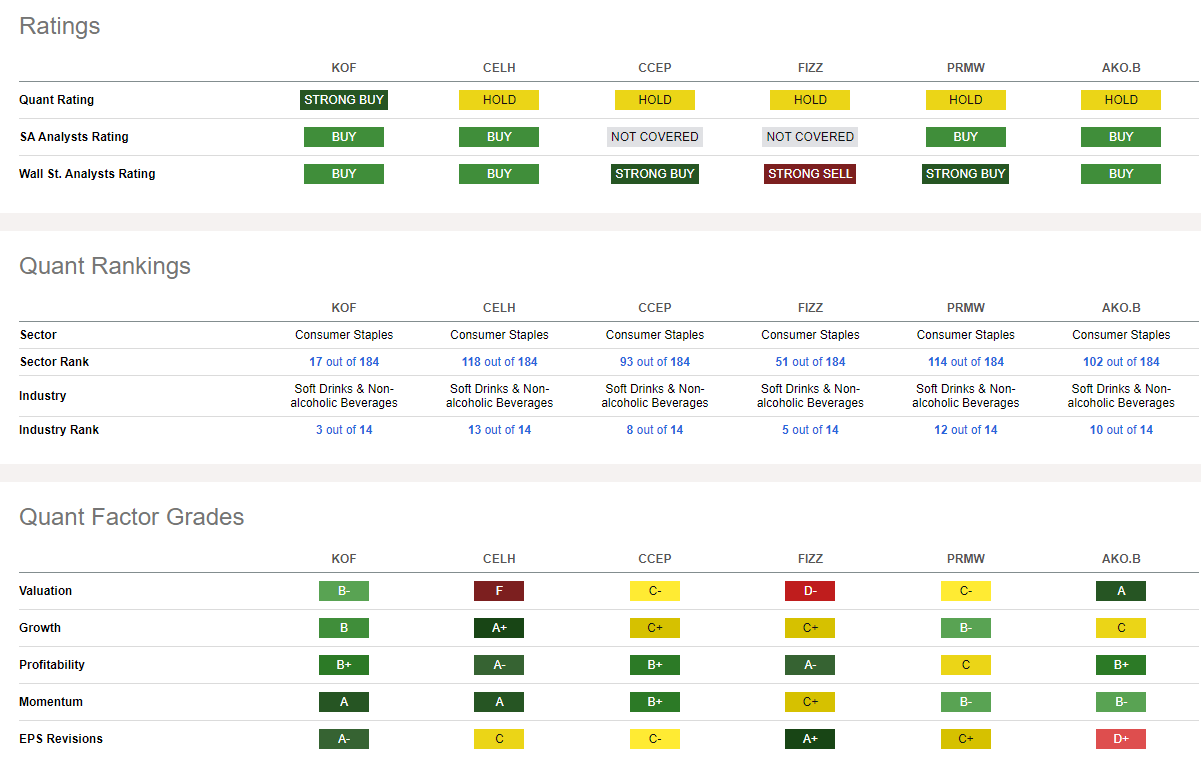

Compared to its peers, KOF features impressive quant factor ratings. The valuation, while by no means a deep value play, is sound while the growth arc is very strong. Profitability trends are impressive, as are technical factors, including share-price momentum – I will detail key price levels on the chart to monitor later in the article. Finally, EPS revisions have been starkly on the good side in the last three months – there have been four earnings upgrades and just a single downgrade.

Competitor Analysis

Seeking Alpha

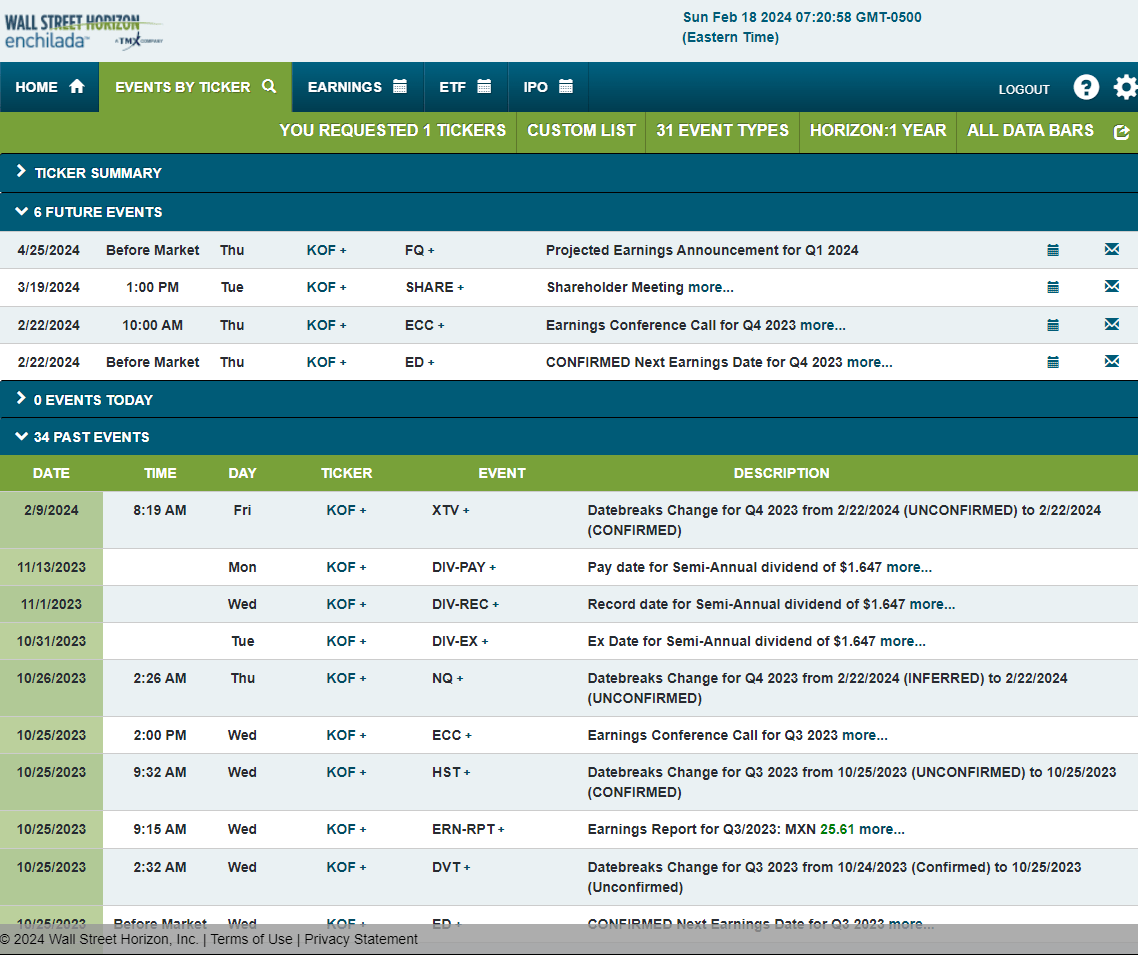

Looking ahead, corporate event data provided by Wall Street Horizon shows a confirmed Q4 2023 earnings date of Thursday, February 22 BMO with a conference call later that morning. You can listen live here. Also keep March 19, 2024, on your calendar as a potential volatility catalyst, as that is when the firm holds its virtual shareholders’ meeting.

Corporate Event Risk Calendar

Wall Street Horizon

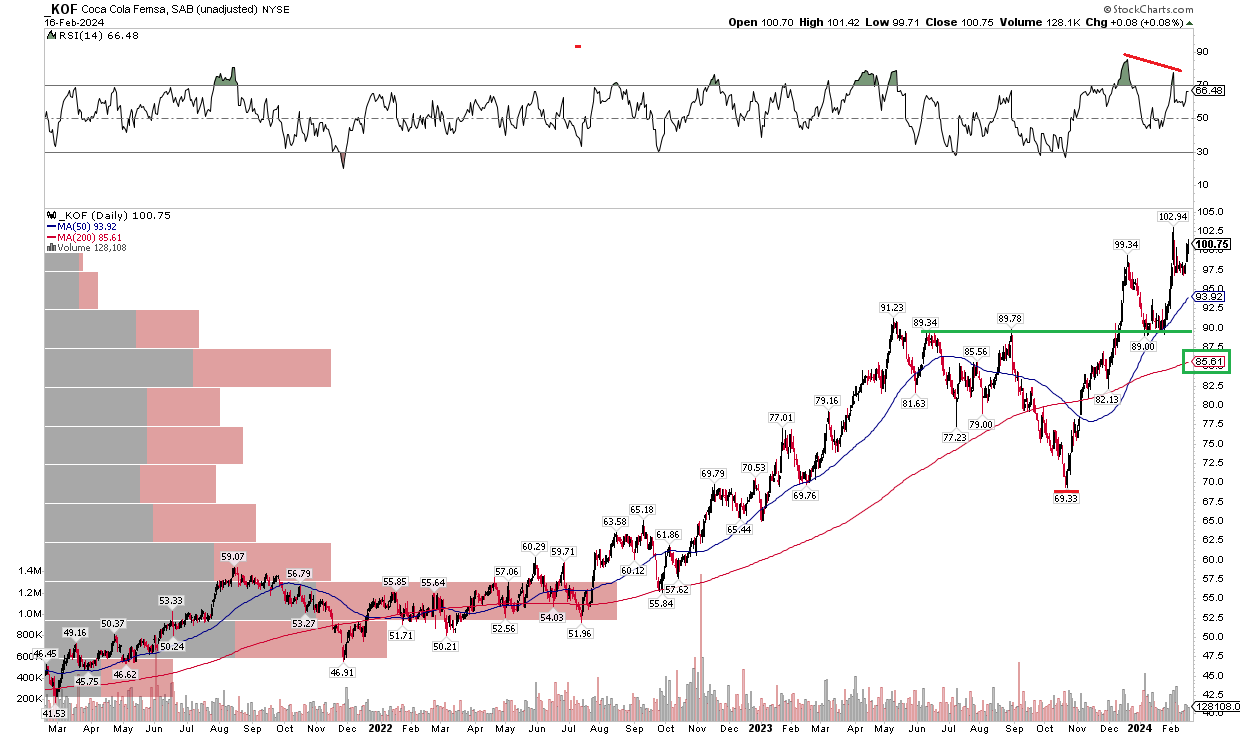

The Technical Take

With a solid valuation and healthy growth trends, the technical picture is generally positive, but there are risks to consider. Notice in the chart below that shares recently rose to a fresh 10-year high of $103. That move came alongside negative RSI momentum divergence, though. It’s thought among technicians that when price advances to a new high without the confirmation of a new high in the RSI, then there is the bearish chance that shares could falter.

Where might they dip? I see key support in the $89 to $91 zone – that was a key area of polarity – a battleground between the bulls and bears – from May 2023 through this past January. But with a rising long-term 200-day moving average, and a 200dma that is below the shorter-term 50dma, the bulls appear to be in control of the trend. We could even peel back the chart to see a long-term bearish to bullish reversal that has a technical upside measured move price target to near $145.

Overall, the trend is positive, and I would be a buyer on a pullback to the low $90s if we get such an opportunity post-earnings this week.

KOF: Bearish RSI Divergence, Broader Uptrend In Place, $90 Support

Stockcharts.com

The Bottom Line

I reiterate my buy rating on Coca-Cola FEMSA, S.A.B. de C.V. Shares are modest to the cheap side while the technical trend is sound for the most part. Still, if we do see a selloff over the latter half of the first quarter, buying on a dip into the low $90s appears as a reasonable risk/reward play.

Q2 2024 Earnings Call Transcript")