Nastco

My last article on Warner Bros. Discovery (NASDAQ:WBD), written in August 2022 here, explained the debt problem facing the company, which would be hard to overcome without lower refinancing/borrowing costs. Well, since then, interest rates have risen in America, and WBD has declined -29% in price. Just as I suggested, long-term gains and any type of outperformance in owning shares have failed to materialize, vs. the S&P 500 blue-chip average advance of +21% over the same span.

Seeking Alpha – Paul Franke, Warner Bros. Discovery Article, August 9th, 2022

The bad news is, that I don’t expect much to change until debt levels and interest rates on them move dramatically lower. In fact, a recession during 2024-25 could decimate streaming sales industry-wide, as a price war may break out. While most planners at the streaming giants are projecting regular price hikes for subscriptions to continue like 2022-23, what if the opposite occurs? As a result, I am now officially moving my Hold rating to Sell on Warner Bros. Discovery, using a 12-month outlook.

Too Much Debt

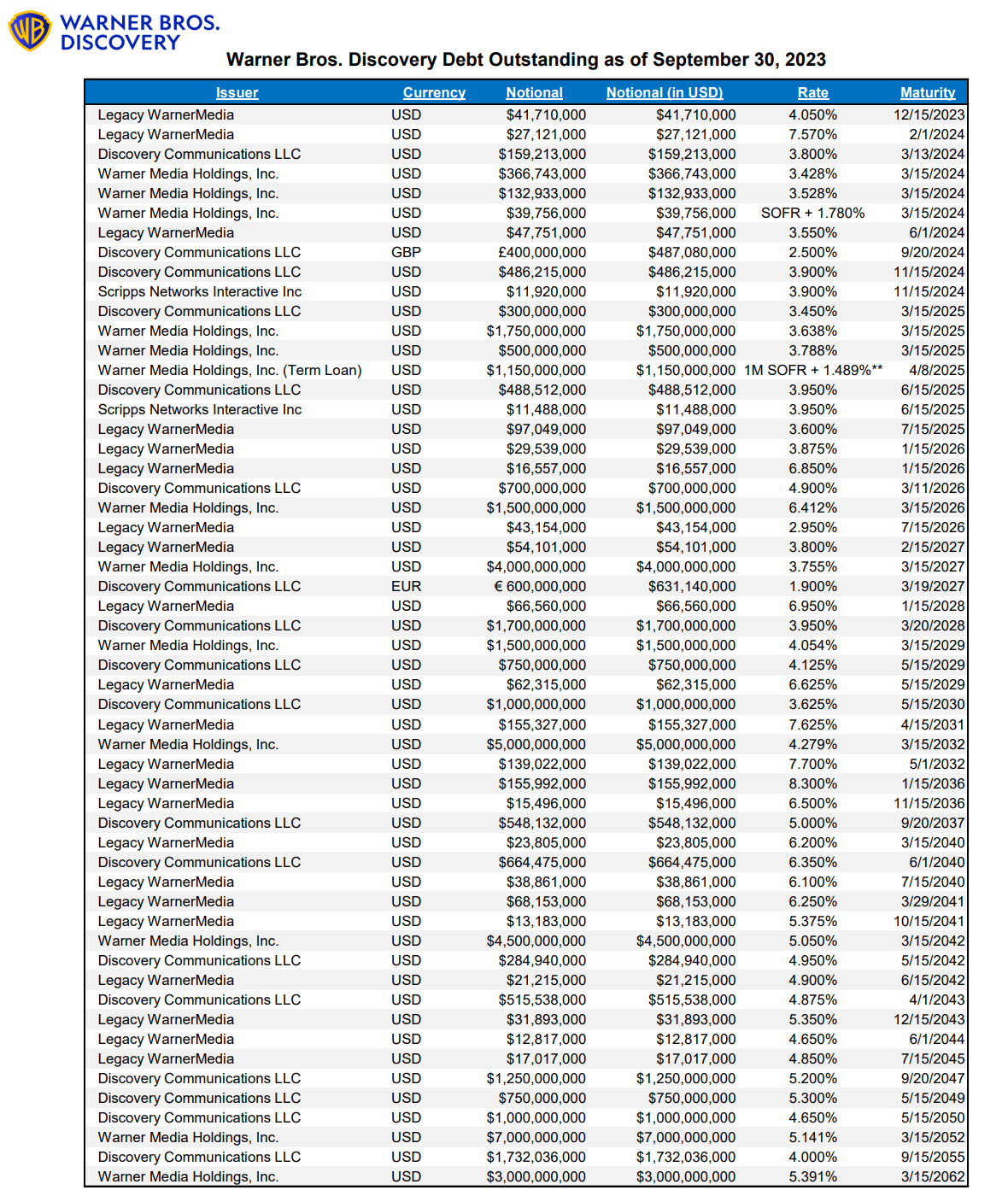

Today’s $24 billion market cap at $10 per share pales in comparison to $42.4 billion in net debt (debt minus cash on hand) owed at the end of September. The saving grace for the time being is that $27 billion matures after 2031, seven years or later from today, with rates largely fixed under 6%.

Warner Bros. Discovery – Debt Schedule, September 2024

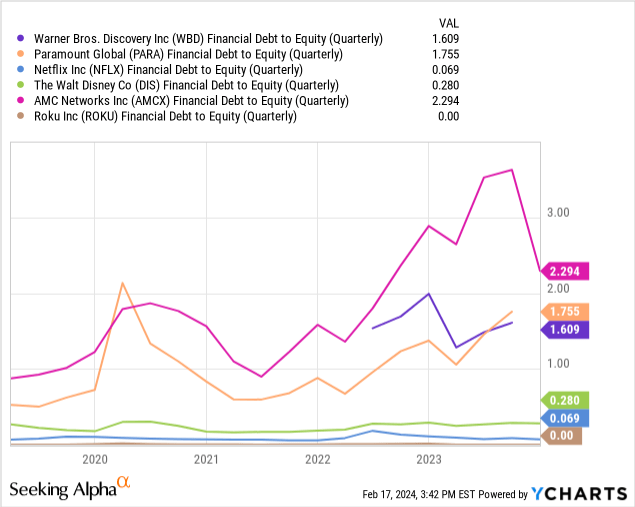

Versus peers and competitors in media production, digital entertainment and streaming delivery services, WBD’s debt is absolutely on the high end of the spectrum, getting close to unsustainable levels.

For example, the debt to equity reading of 1.6x is roughly equal to the closest cousin Paramount’s (PARA) 1.75x ratio. Only the small niche player AMC Networks (AMCX) sports a higher leverage reading at 2.3x, with questions about the solvency odds at this firm everywhere on Wall Street. In comparison, Netflix (NFLX) holds almost no debt, Disney (DIS) sits at a reasonable 0.3x, and Roku (ROKU) owes nothing with plenty of cash in the bank to expand viewership.

YCharts – Warner Bros. Discovery vs. Streaming Peers, Debt to Equity, 5 Years

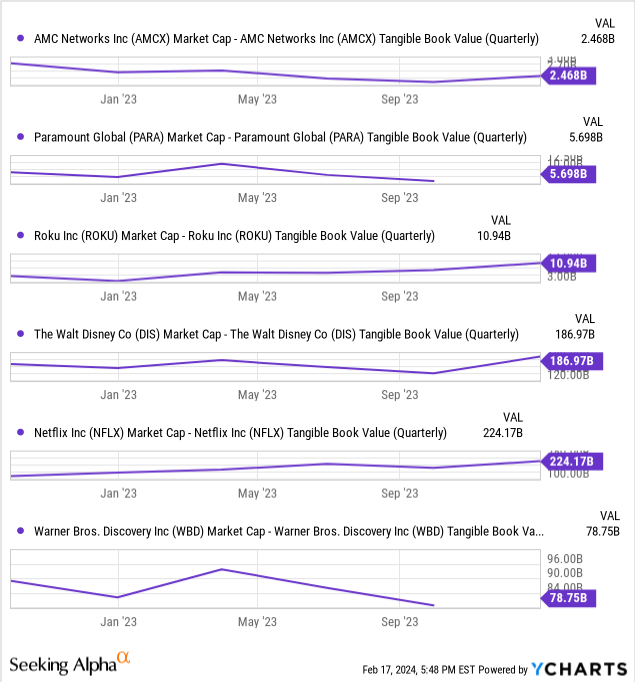

The real bummer for WBD shareholders is almost all of its assets to back “equity” totals on the balance sheet are thin-air intangibles and goodwill accounting from past acquisitions and copyrighted media content ($97 billion out of $123.7 billion in total assets reported at the end of September). So, $42+ billion in debt and almost $78 billion in total liabilities are matched against just $27 billion in hard assets, cash and investments!

When we review the distance between equity market capitalization and tangible book value readings (a hugely negative number for this company), Warner Bros. Discovery stands out as quite overvalued in the streaming industry. While the heavily indebted Paramount and AMC Networks or perpetual money-losing setup of Roku have been valued close to tangible book value in early 2024, WBD is priced at a whopping $78 billion premium. The share valuation is in the same league as the too much lower leverage, much higher profitability names of Netflix and Disney. I personally don’t believe this valuation is justifiable.

YCharts – Warner Bros. Discovery vs. Streaming Peers, Market Cap Premium to Tangible Book Value, 15 Months

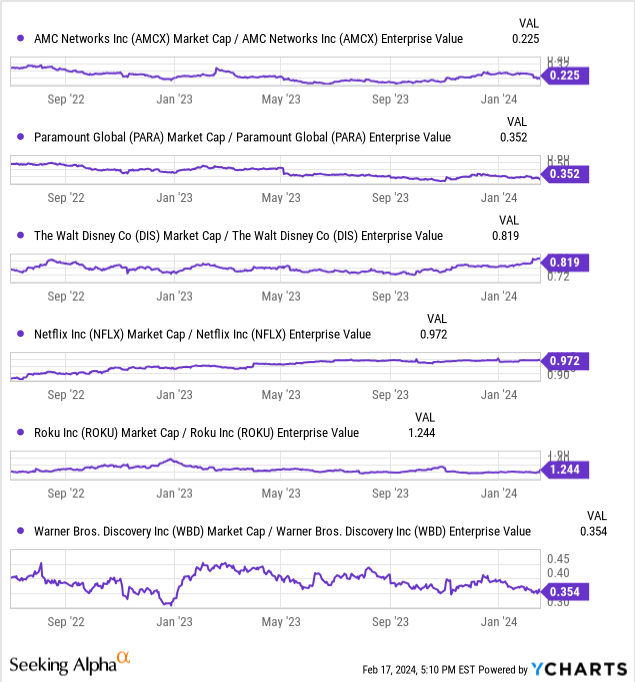

Another way to look at the balance sheet and the potential risk excessive leverage poses is… take the equity market capitalization and compare it to enterprise value. Enterprise value adds in debt and subtracts cash on hand, to get a better feel of what it would actually cost to acquire a business along with its contracted future obligations. For simplicity, companies with limited debt and/or substantial cash holdings have a Market Cap to Enterprise Value near 1.0x for a multiple.

Corporations with numbers above 1.0x have super-strong balance sheets effectively, while organizations under 0.2x are often considered at risk of bankruptcy in a recession or industry downturn (excluding bank/financial balance sheets). The typical blue-chip business traded in America sports a number well above 0.5x. WBD’s ratio of 0.35x is down from 0.5x at the time of the merger, where future share price declines in 2024 could easily push its ratio nearer the rotten AMC Networks setup.

YCharts – Warner Bros. Discovery vs. Streaming Peers, Market Cap vs. Enterprise Value, Since July 2022

Business Outlook

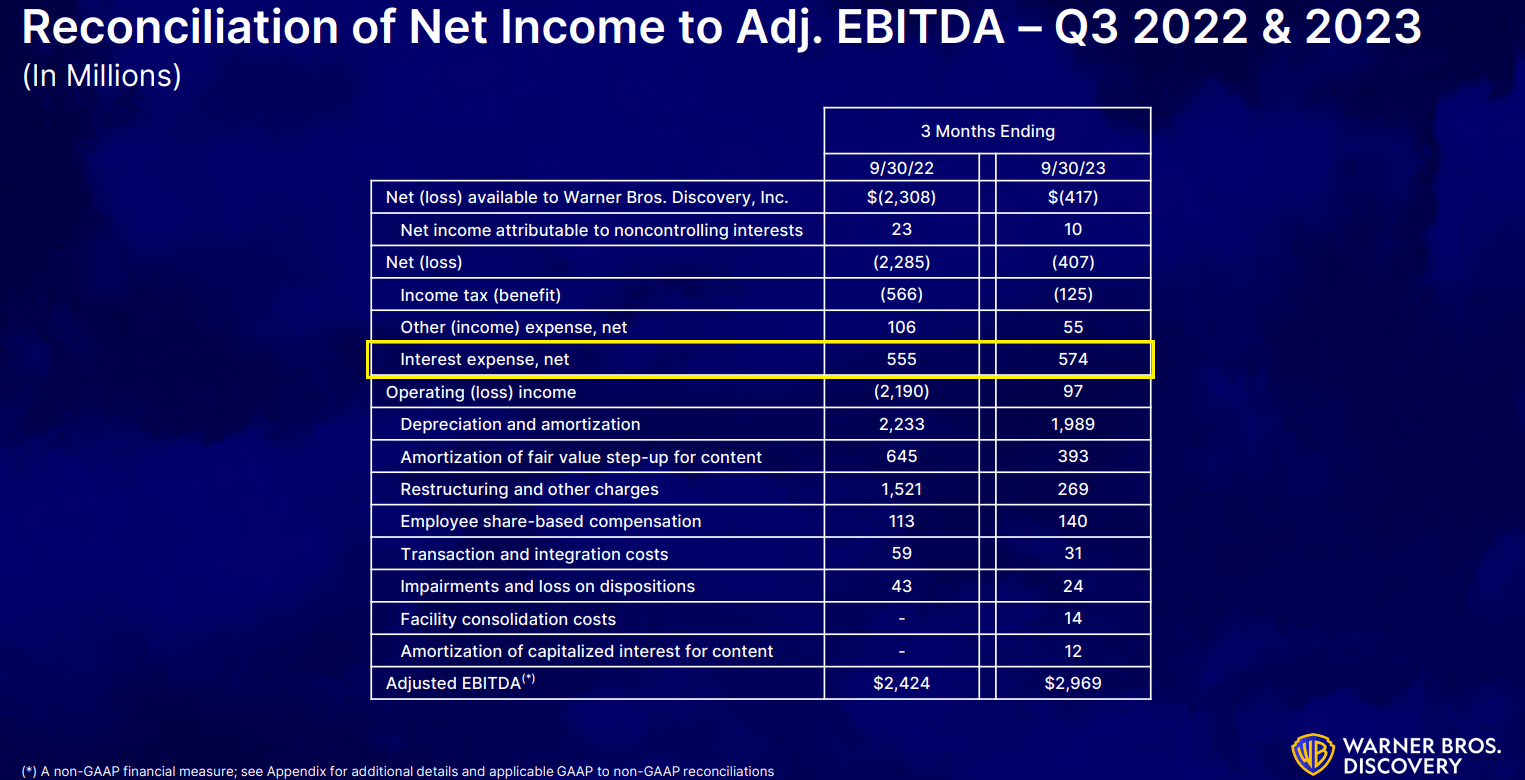

Despite $5 billion in total debt reduction over the previous 12 months, net interest expense still rose YoY (boxed in yellow below) during the September quarter, on the back of rising interest rates for new loans, variable rate contracts, and refinanced debt.

Warner Bros. Discovery – Q3 2023 Earnings Release, Results Breakdown

What WBD is facing is a classic “profit squeeze” on rising interest expenses, climbing production and labor costs, plus higher marketing and customer retention expenses to keep business in a highly competitive streaming marketplace – all in the face of potentially extreme difficulty raising monthly subscription rates in a general U.S. economic recession.

Already, Warner Bros. Discovery’s Max video-on-demand offering is struggling to grow. Last quarter, DTC online subscribers dropped to 95.1M (-0.7M net adds vs. Q2 2023). And, consumers are getting nervous about a slowing economy. A February 2, 2024 Forbes article explained the price-conscious customer views for streaming services. My concern is any economic contraction with sharply increasing unemployment trends will make regular subscription price increases next to impossible later in 2024.

Forbes – Ana Durrani, Streaming Subscribers, February 2nd, 2024 Article Forbes – Ana Durrani, Subscriber Survey on Streaming Price/Value, February 2nd, 2024 Article

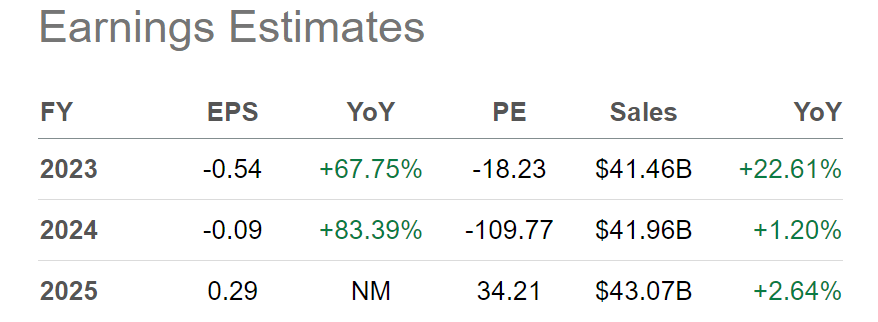

In terms of Wall Street analyst forecasts, little growth in revenue is projected for 2024-25. While cash EPS is expected to rise, the pace will not be fast, even under the assumption of moderate economic expansion in the U.S. economy. I am using the below estimate table as something of a best-case scenario. Why?

Seeking Alpha Table – Warner Bros. Discovery, Analyst Estimates for 2023-25, Made February 17th, 2024

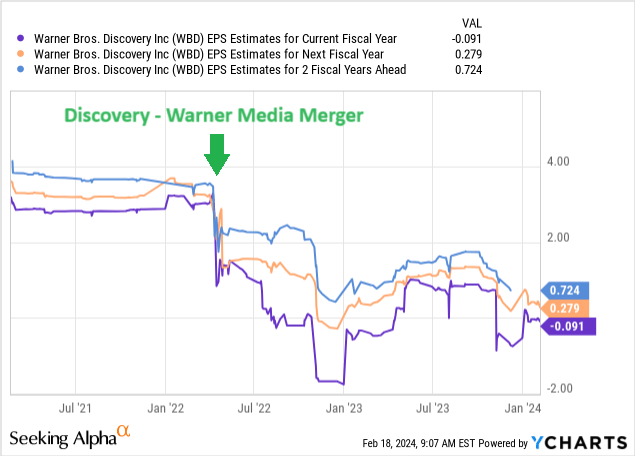

2024-26 estimates have been coming down on a routine basis since the merger was completed in May 2022. Mind you, WBD has found it difficult to meet rosy pre-merger targets BEFORE any contraction in the overall economy becomes a reality. Original Discovery shareholders before the merger have every right to be upset with how things are turning out. Falling from pre-merger Discovery EPS in the $3.00 to $3.50 range estimates well under $1 (perhaps closer to breakeven in a mild recession) are not the expectation laid out by management in the hyped run-up to this business marriage.

YCharts – Discovery & Warner Bros. Discovery, EPS Estimates for 2024-26, Since March 2021

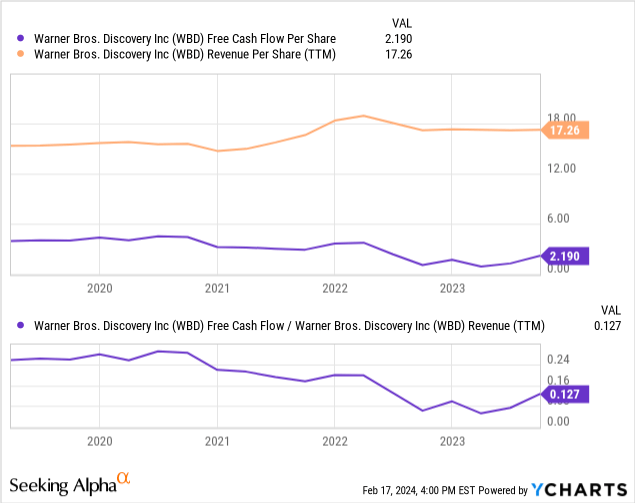

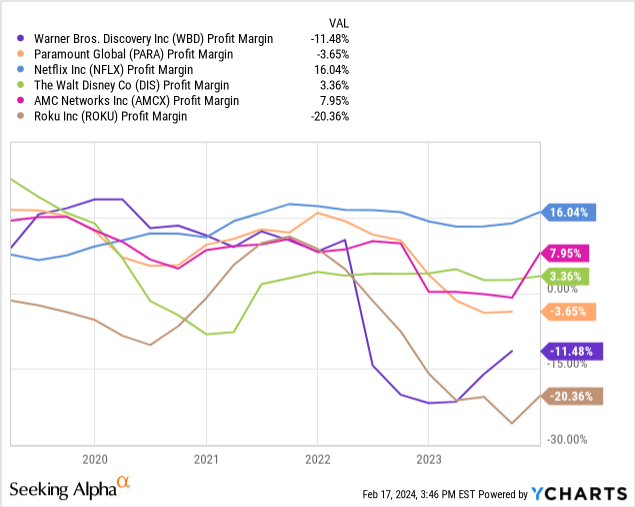

Free cash flow margins have been cut in half from the Discovery stand-alone enterprise in 2020-21, while GAAP profit margins have turned into major operating loss margins.

YCharts – Discovery & Warner Bros. Discovery vs. Streaming Peers, FCF vs. Sales Per Share, 5 Years YCharts – Discovery & Warner Bros. Discovery vs. Streaming Peers, Final Profit Margins, 5 Years

Final Thoughts

Q4 and 12-month FY 2023 operating results are due for release on February 23rd. At that point, we will get an update on subscriber growth if any, progress on debt reduction efforts, possibly some extra asset write-downs in intangible/goodwill asset values, plus management guidance for 2024. There is opportunity for both relief and disappointment by bullish stakeholders.

Talk of a possible hookup with Paramount has also made the rounds in early 2024. I personally don’t think another merger with an equally debt-laden streamer is in the cards when the last one has not added any value for shareholders. I would not view the announcement of partnerships or streaming combinations as particularly great news for WBD owners, although such a possibility exists.

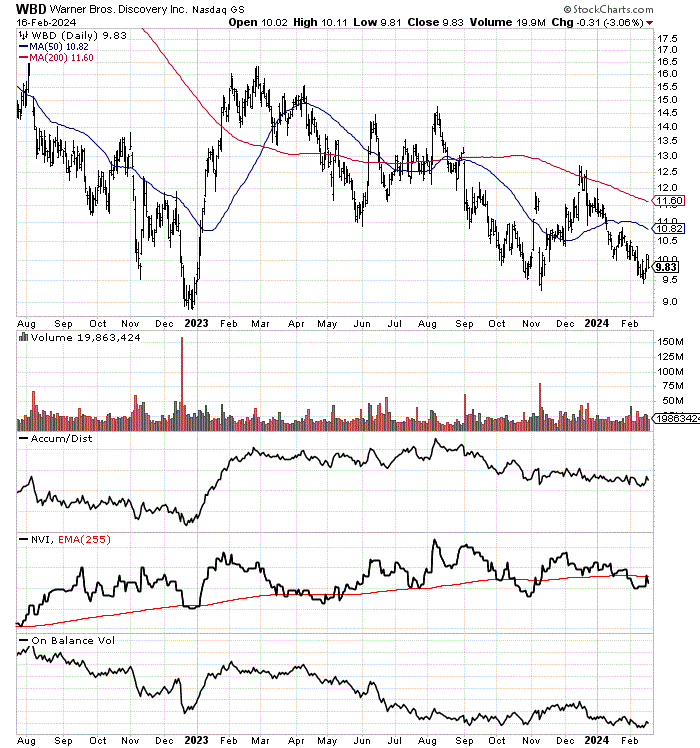

Below is a daily trading chart for Warner Bros. Discovery, back to my last article on the company. It highlights a weak chart – both in price and trading momentum patterns. Price is below its important 50-day and 200-day moving averages, not far away from a multi-year low under $9. In addition, I would categorize the Accumulation/Distribution Line, Negative Volume Index, and On Balance Volume zigzags as noncommittal to bearish in trend.

StockCharts.com – Warner Bros. Discovery, 19 Months of Daily Price & Volume Changes

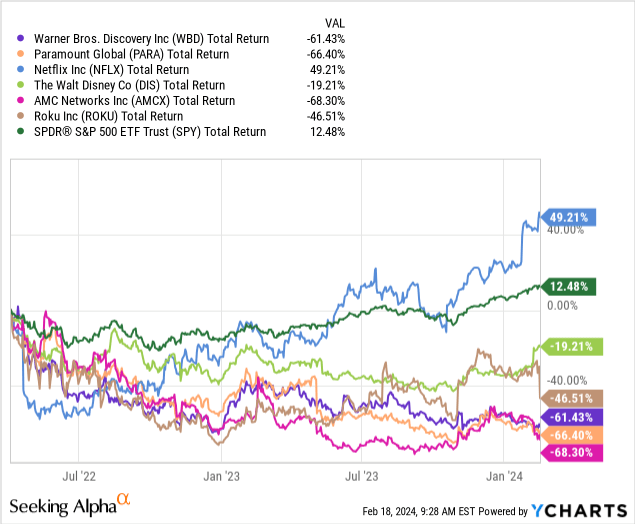

Total returns for investors measured from just before the merger have been dismal, at a -61% loss. If there’s any consolation, Paramount and AMC Networks have been just as weak, mainly from a similar overuse of leverage (too much debt in a slowing growth industry).

YCharts – Warner Bros. Discovery vs. Streaming Peers, Total Returns, Since April 2022

Ever-tightening credit conditions in the U.S. banking system (inverted Treasury yield curve and contracting total bank credit as signals), another bump higher in inflation this higher (perhaps led by rising crude oil quotes), on top of a clearly overvalued U.S. stock market (priced richly on peaking cycle earnings), all point to the real risk of a wealth and employment recession this year.

In a deep and prolonged recession, Warner Bros. Discovery does carry some bankruptcy risk, especially if a price war in the streaming industry breaks out. Under this scenario, the common shares can decline to zero in price, giving investors a potential 100% loss on whatever your purchase price/cost might be, in a worst-case scenario. Honestly, companies with stronger balance sheets like Disney and Netflix will find it difficult to go to zero for price, even in a deflationary depression.

How could WBD advance in price? You have to be rooting for falling interest rates on debt, slowing wage growth, on top of a stronger economy with greater industry-wide demand for streaming content. A Goldilocks outcome is the easy answer.

The main outlier bullish idea is that someone with deeper pockets makes a bid for the Warner Bros. Discovery library. Netflix, Apple (AAPL), Google/Alphabet (GOOG) (GOOGL), and Amazon (AMZN) would be the potential suitors. If a big fish purchased WBD to merge with their streaming offerings, paying off most to all of its $42+ billion in debt, I suppose WBD may have some value. A takeover share bid of $15 would bring a total Warner Bros. Discovery buyout value of $75 billion (including debt) while throwing off up to $3 billion in after-tax income (4% for an earnings yield). Of course, intense competition for subscription pricing would nosedive operating earnings in a recession scenario, meaning such a marriage might not work out well for the acquirer.

Even if you are bullish on Wall Street equities, I do feel the odds of WBD staying above $13 a share on a sustainable basis are low (looking at its underperformance trading history and stagnate financials), particularly if the economy weakens from early 2024.

My view is the Warner Bros. Discovery stock setup should be sold and avoided at this stage. I will re-evaluate once a recession hits and the Federal Reserve is again allowed to lower interest rates in the economy. After a watershed stock decline, a “risk-on” environment could theoretically make the stock a buy at lower levels, perhaps in the low single-digit range. For a 12-month outlook, I am downgrading my rating to Sell, with a price target under $5.

Q2 2024 Earnings Call Transcript")