FG Trade Latin/E+ via Getty Images

Introduction

West Pharmaceutical Services, Inc. (NYSE:WST) is a market leader in the injectables market, benefitting from long-term tailwinds as more biologics get introduced to the market and healthcare spending ramps up. On February 15, the company announced its Q4 2023 results (which were pretty mixed) and provided guidance and outlook for 2024. In this article, I’ll delve deeper into the company’s results and provide a rationale for why I’m not buying the company’s shares after a drop in its share price post-results.

Background

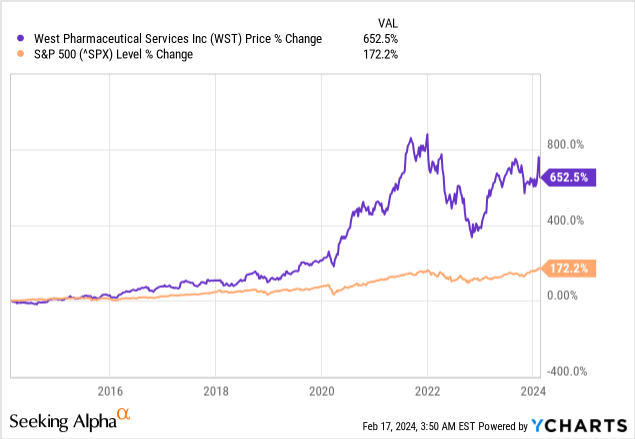

Over the last ten years, shares of West Pharmaceutical have put up very respectable returns to investors with a total return of 652.5% over the period compared to the S&P 500’s return of 172.2%. With a 652.5% total return in the last 10 years, this equates to a compounded annual return of 22.4%.

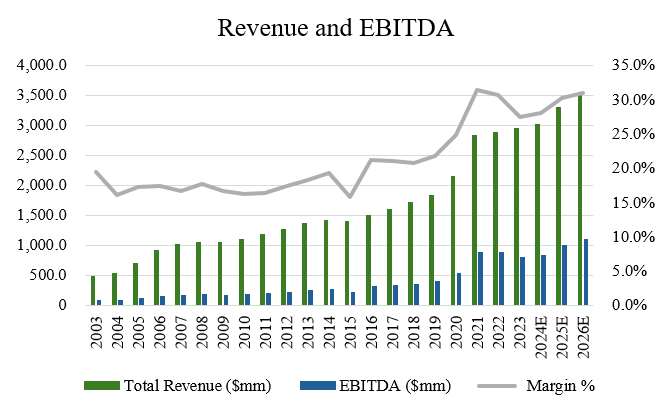

With a strong record of outperformance, it’s important to look at what’s driving this, particularly in the company’s financials. Over the last 20 years, West Pharmaceutical has had growth in revenues and EBITDA at CAGRs of 9.5% and 11.4%, respectively. Over the last 10 years, it’s grown revenues and EBITDA at CAGRs of 8.0% and 12.5% (source: S&P Capital IQ). With the share count increasing 27.4% over the last two decades, we can conclude that the rest of the growth leading us to a compounded annual return of 22.4% for the share price has been as a result of multiple expansion.

Author, based on S&P Capital IQ

Recent Results

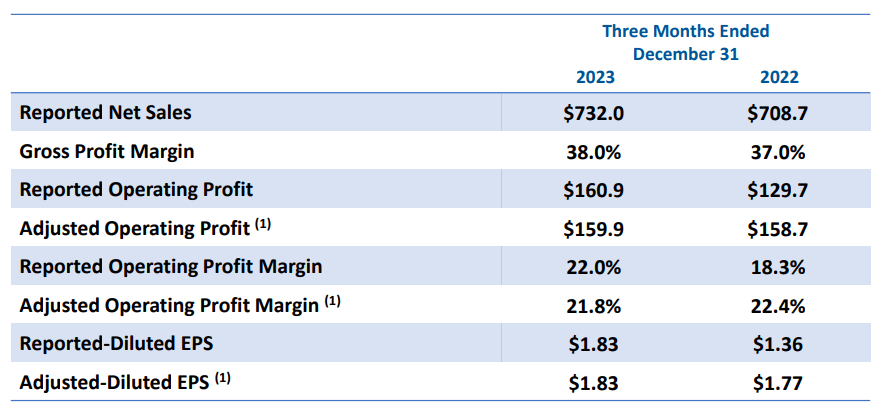

When looking at the Q4 2023 results that were announced on February 15, West Pharmaceutical had revenues of $732 million, which was up 3.3% year over year. While the company reported a beat on EPS by $0.05 to $1.83 per share, the company missed on its revenue target by $7.52 million and organic net sales growth was pretty flat at 1.4%.

At first glance, this seemed like a pretty good quarter for the company. Revenue was up, EPS was up, and margins expanded nicely with gross profit margins expanding 100 basis points and adjusted operating profit margin up 370 basis points.

Investor Presentation

During 2023, West Pharmaceutical had a number of major highlights I think are noteworthy. For example, the company introduced its Vial2Bag Advanced 13mm admixture device, which is being used for in drug preparation and delivery. Generally speaking, West Pharmaceutical has somewhat of a competitive advantage in the injectable drug delivery market, which has high barriers to entry.

Why is that relevant? Because it gives the company an intangible moat around the business, protecting its high margins and its new competition from entering the market. According to IBIS World, the injectables market is growing about 6% a year and so as a major player in the industry, it would seem that West Pharmaceutical should benefit, especially with a near 70% market share in the market for elastomer components for injectable drugs.

Looking out into 2024 and beyond, management is expecting between $3.0 billion and $3.025 billion, with adjusted EPS in the $7.50 to $7.75 range. That EPS range would be a nice improvement (and suggest pretty good margin expansion), so why the forecast for only ~2% growth in 2024?

Well, West Pharmaceutical anticipates some challenges ahead, with a few factors that are expected to put downwards pressure on growth in the near future. For example, with guidance of just 2% to 3% in 2024, this is lower by about 6 percentage points from the company’s preliminary outlook.

Driven by macro factors, like destocking from customers, overhang from COVID-19, and the timing of new HVP device capacity, West Pharmaceutical looks like it’s going to have a pretty mediocre year.

I generally like to invest in companies that have a good outlook, with catalysts to have even better results. But in the case of West Pharmaceutical, I’m concerned that the risks to the investment thesis and outlook outweigh the catalysts. On the one hand, there’s an argument to be made that most of these issues are transitory. Eventually, once customers are done destocking, demand would likely pick up again and the company can likely continue growing in the high-single digits, back to the 7-8% revenue CAGR the company has been consistently growing at over the last decade or so.

On the other hand, the risks I see here are that capex has more than quadrupled in the last five years, as the company focuses more on investing in efficiency and automation. That doesn’t hurt EPS and net income for 2024, but it will certainly show up in the cash flow statement. The other risk I see for the company is on its rich valuation, which I’ll discuss at length in the next section.

Valuation

Based on the 4 sell-side analysts who cover West Pharmaceutical’s stock, there are 3 ‘buy’ ratings and 1 ‘hold’ rating with an average price target of $417.00, a high estimate of $470.00, and a low estimate of $375.00 (source: TD Estimates). From the current price to the average target price one-year out, this implies potential upside of 15.2%, not including the company’s 0.2% dividend yield. With total return potential of 15.4% over the next year, it would seem that analysts are fairly bullish on the near-term upside potential for the company.

However, when looking at the future growth of the company and current multiple, I would disagree with the analysts’ take here and suggest that shares are likely quite overvalued at the current price.

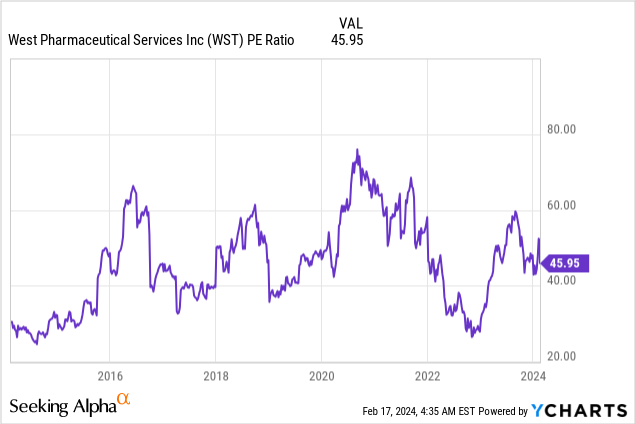

When looking at the current valuation of West Pharmaceutical, the company trades at a forward multiple of 46.0x, which seems pretty high to me. Why? Because for a company growing in the single-digits, it seems that the market is valuing this as a high-growth company, despite indications that West Pharmaceutical is only expected to grow 2.0% in 2024 and 9.2% in 2025.

Using forward P/E multiples doesn’t give me much more comfort in the valuation, either. West Pharmaceutical is still trading at 44.5x 2024 earnings and 40.1x 2025 earnings; a high multiple by any measure.

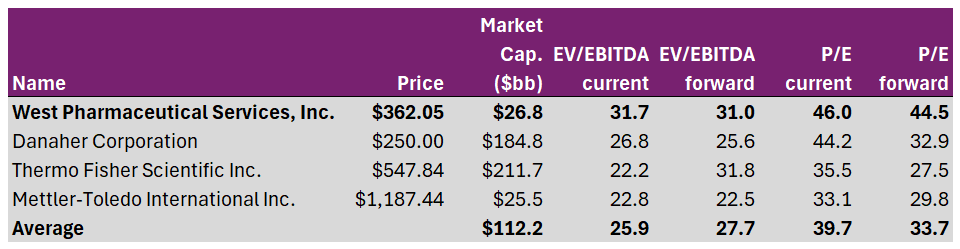

And when comparing West Pharmaceutical to its peers, it continues to look expensive. Looking at the comps table below, West Pharmaceutical comes in ahead of the pack on every metric. I chose to compare West Pharmaceutical to companies that also manufacture healthcare-related products, have strong competitive advantages but also exhibit similar growth profiles. While all their multiples are above-market multiples (S&P 500 P/E ratio is 26.0x), West Pharmaceutical seems to be expensive at today’s prices relative to its peers.

Author, based on data from S&P Capital IQ

Say what you want about business quality, but I think it’s very hard to justify such lofty multiples for a company that won’t be able to produce above-average growth for its shareholders on a per share basis.

Conclusion

While West Pharmaceutical has benefitted and is poised to benefit from long-term, secular tailwinds in the injectables market with a dominant market share, I think the recent results and guidance paint a meaningful picture for some challenging times ahead for the company. With my concerns over its near-term growth constraints, elevated capital expenditures, and a rich valuation, I’m doubtful of the company’s ability to sustain such high multiples, especially when an analysis of the peer group valuations reveals a very lofty price today. I think despite the drop post-results, there seems to be a potential disconnection between expectations and fundamentals. So with that said, I’m not comfortable buying today.

Q2 2024 Earnings Call Transcript")