SOPA Images/LightRocket via Getty Images

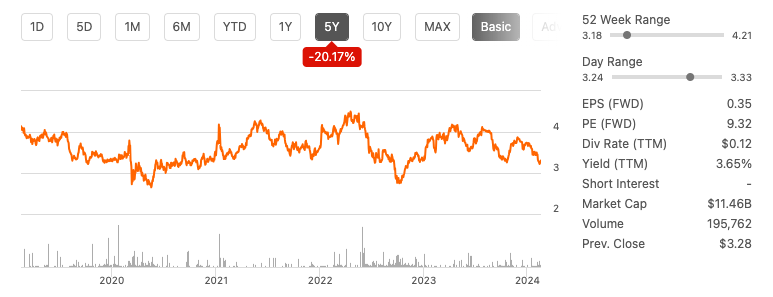

When you first look at Carrefour SA (OTCPK:CRRFY), it might seem like an attractive investment. The company has been growing its financials since FY2021, showing consistent increases in its top and bottom lines. It has a strong market position in France, Brazil and Spain. Furthermore, with an increase in levered free cash flow, share buybacks, and a FWD price-to-earnings ratio of 9.32, Carrefour seems to be undervalued compared to its supermarket and retail industry peers. However, the stock has seen little movement over the last five years and has lost 54.38% in value over the last ten years.

Five year stock trend (Seeking Alpha)

Since the 2008 financial crisis, it’s been a bumpy ride for the company, which claimed the world’s second-largest supermarket position in the 90s and early 2000s. The company failed to keep up with digital trends and growing competition and inadequately invested in adapting its business model to changing consumer demands, resulting in a number of monumental and costly failures across many of its international markets. In 2021, Carrefour announced what was a much-needed Digital Strategy 2026, in which it committed $3 billion to tech investments. However, past failures, diminished markets, and a loss of market share in France, its home front and biggest revenue generator, are reasons to remain concerned. Therefore, I do not believe it is compelling enough to give the stock a hold rating.

Company overview

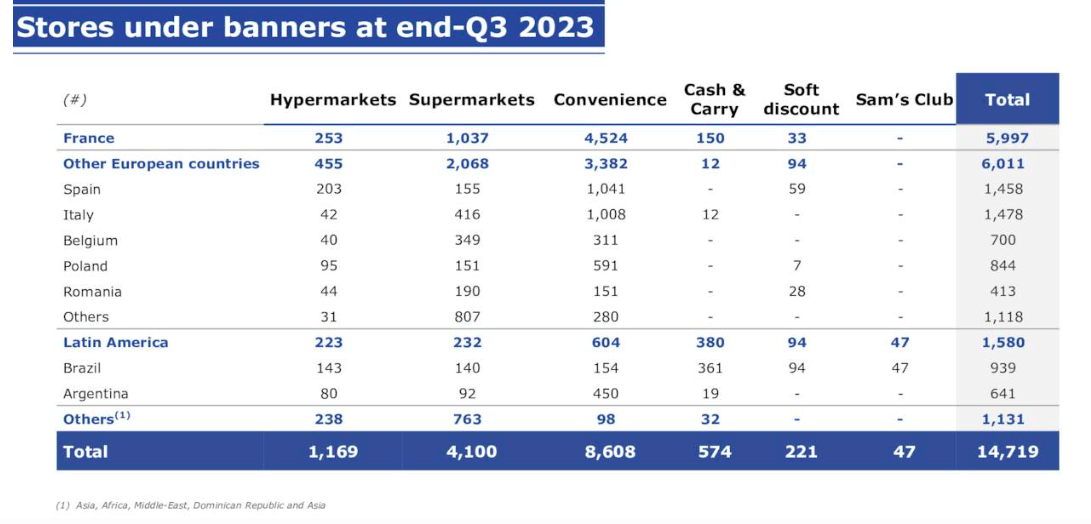

Carrefour, established in 1959, was a front-runner in the retail industry with its hypermarkets and own-brand products. The strategic acquisition of Promodes SA in the 2000s positioned Carrefour as the world’s second-largest supermarket chain, after Walmart (WMT). However, the 2008 financial crisis marked a downturn, with declining profitability and market share. The company responded by restructuring and decreasing the number of markets it was actively focused on.

Stores across regions (Investor presentation 2023)

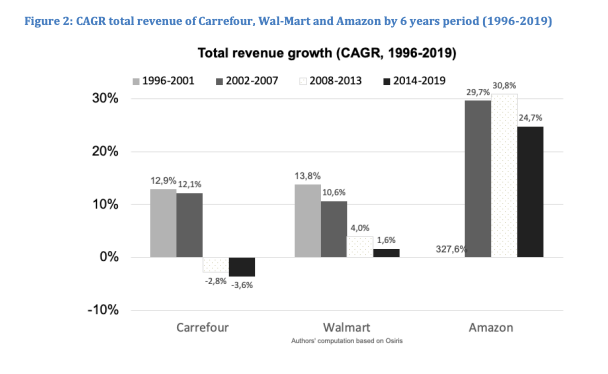

However, its lack of investment in digitalisation led to obsolescence in rapidly digitising markets, notably China. Despite being an early entrant in 1995, Carrefour struggled to adapt to China’s digital economy from 2010 onwards. A significant indicator of the importance of investing in digital capabilities within the supermarket industry is by following Carrefour and Walmart’s growth paths, which were paralleled until 2008. However, Carrefour’s lack of technology investment led to its fall to the fifteenth position in terms of market cap, while Walmart became the world’s largest supermarket chain.

Total revenue growth versus Walmart and Amazon (ResearchGate)

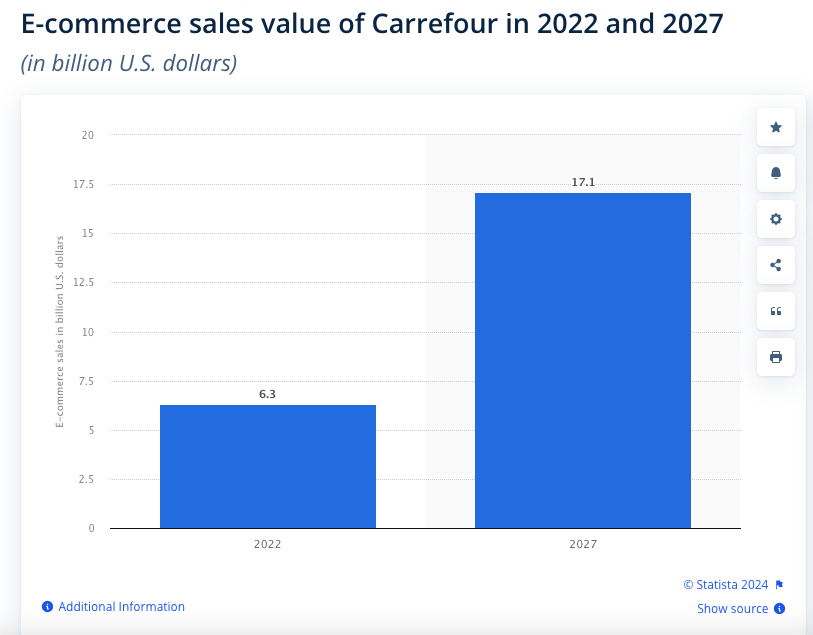

The company now aims to establish an omnichannel business model by 2026. Recognising the importance of digitalisation, Carrefour increased ICT spending to $1.9 billion in 2023, focusing on cloud technologies and partnerships with IBM and Google. The company expects to increase its online market position through its digital investments, expecting e-commerce sales to reach $17.1 billion in 2027.

E-commerce growth goals (Statista)

However, Carrefour’s long-term growth remains uncertain in an increasingly competitive retail environment. Its focus is largely on mature European markets, with Brazil as its only real major growth driver.

Market position and competition

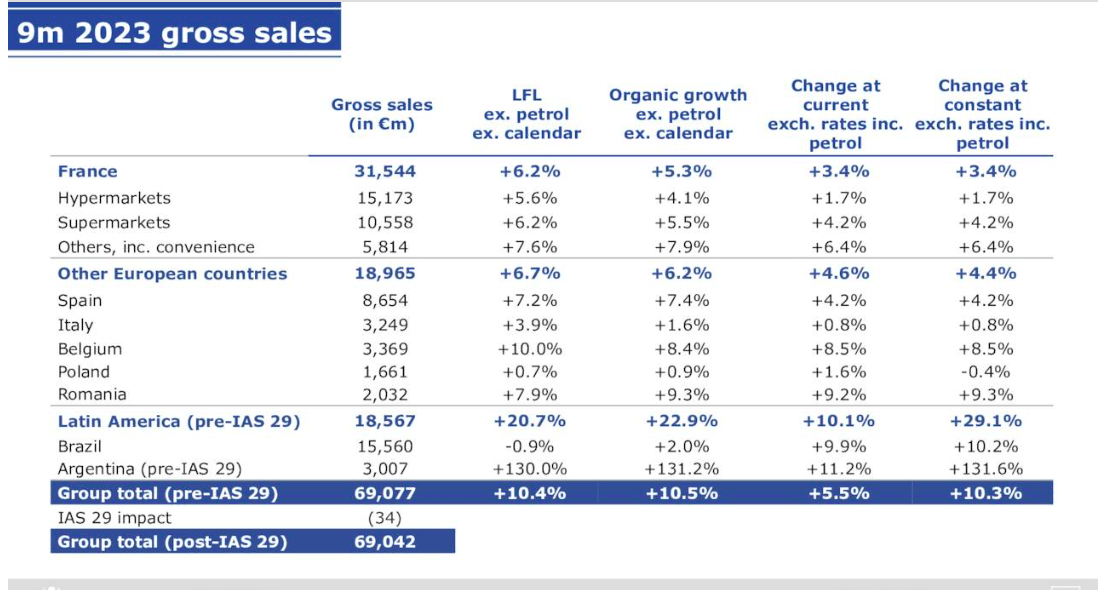

Carrefour’s largest revenue generator is France, followed by Brazil and Spain if we look at the first nine months of FY2023.

9 month revenue performance across regions 2023 (Investor presentation 2023)

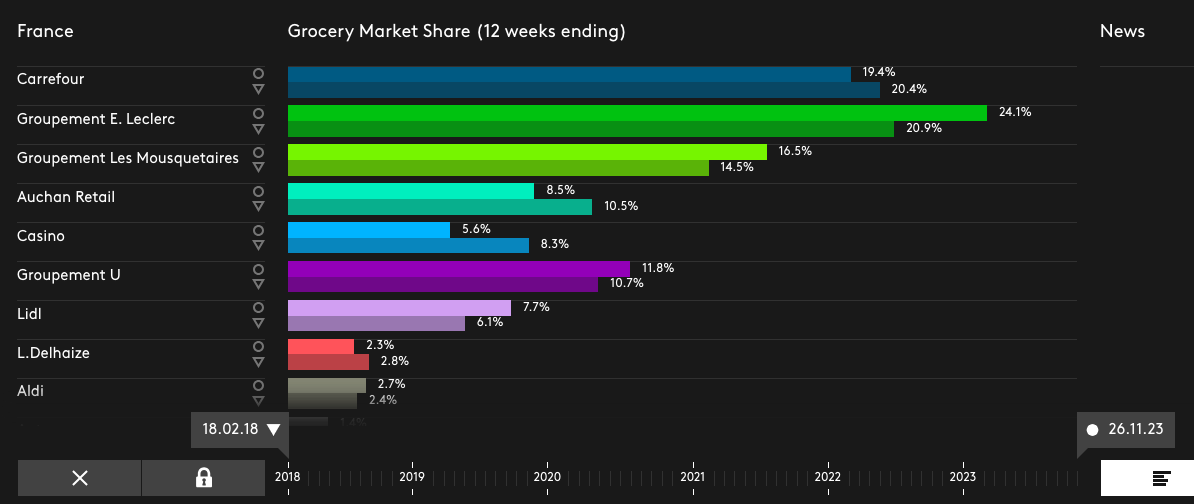

It is the second-largest grocery chain after E. Leclerc in France, with a roughly 19% market share. We can see that over five years, it has been losing market share as more competition enters the market. This is a concerning trend in the homefront business.

Grocery market share in France 2018 versus 2023 (Kantar Worldpanel)

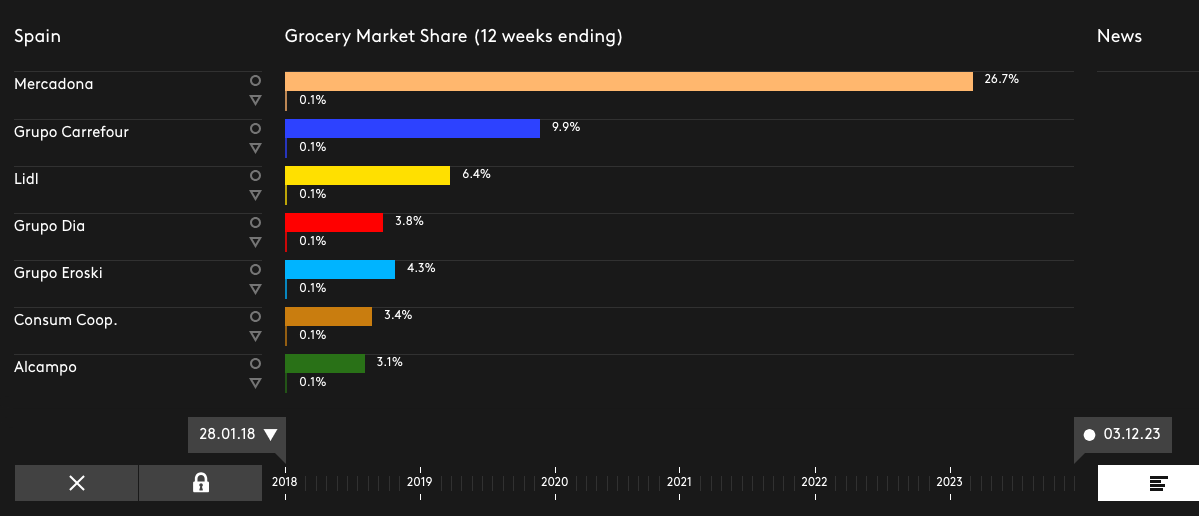

In Spain, it holds the second-largest position and has increased its market share over the past five years despite operating in a mature market.

Grocery market share Spain (Kantar Worldpanel)

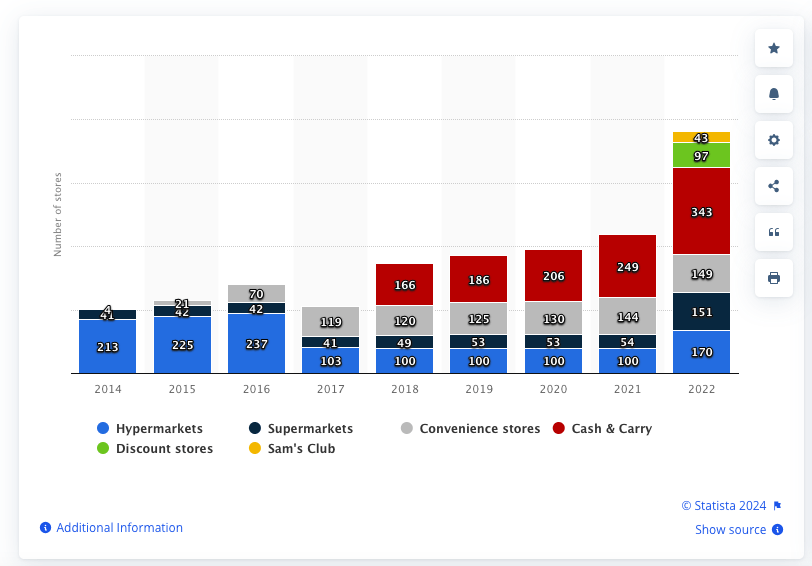

Currently, Brazil appears to be the market with the greatest growth potential. The company is one of the leading retailers in Brazil and has been investing in the growth momentum, as seen by the annual increase in stores.

Number of Carrefour stores in Brazil from 2014 to 2022, by store format (Statista)

The company expects to increase its online market position through its digital investments, expecting e-commerce sales to reach $17.1 billion in 2027.

E-commerce growth goals (Statista)

Financial position

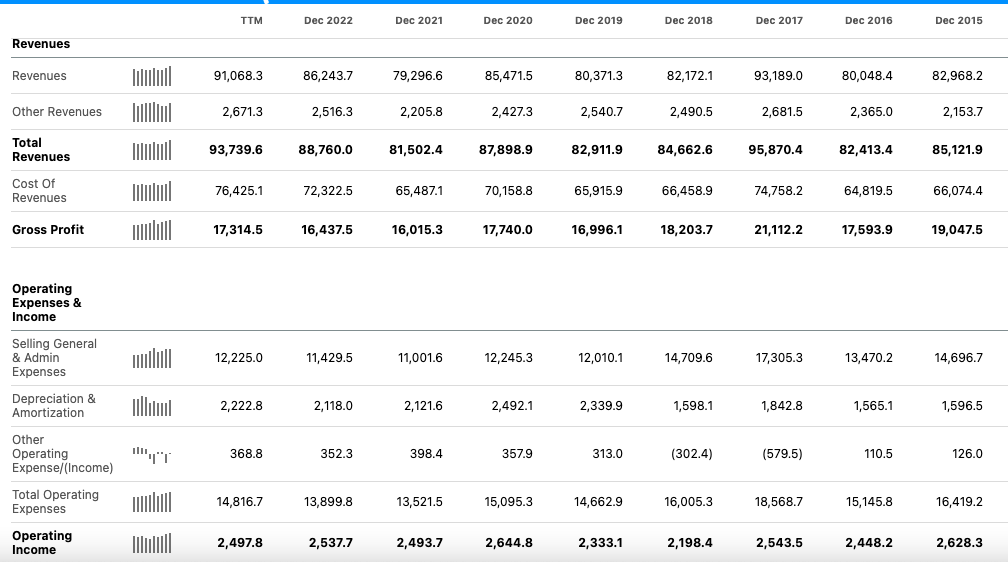

Carrefour has been improving its top and bottom lines since FY2021. Revenue growth is driven by sales in France, Brazil and Spain, which make up 80% of its total revenue. Although the company has seen an improvement in its bottom line, we can see that the profit margin has been downward trending over the past seven financial years due to an increase in competition and rising operational costs.

Annual revenue, gross profit and operating income (Seeking Alpha)

Annual net income (Seeking Alpha)

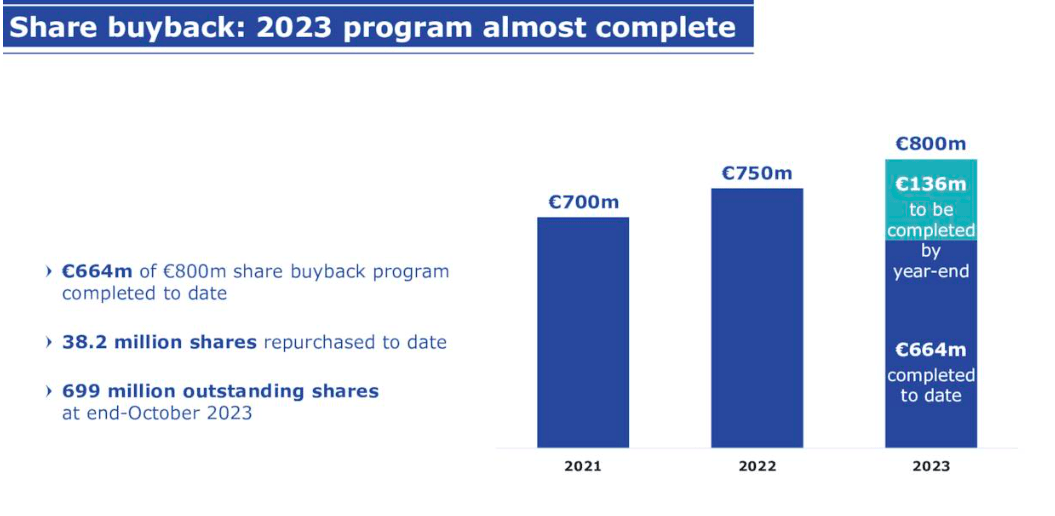

If we look at the levered free cash flow, we can see that it is positive at $555.3 million TTM. However, levered free cash flow has been inconsistent over the years, with serious cash burn since FY2021. Furthermore, the company’s levered free cash flow margin is 0.59%, which is very low for such a large-scale business. To show confidence in the business, the company has also been buying back shares.

Annual levered free cash flow (Seeking Alpha)

Share buyback since 2021 (Investor presentation 2023)

Shares outstanding (Seeking Alpha)

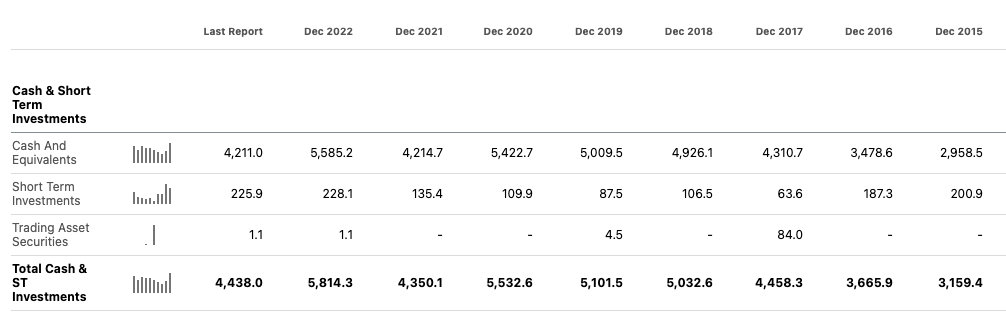

Looking at the company’s balance sheet, we can see that its annual debt intake has been increasing. Additionally, there has been a decline in total cash, indicating cash burn. While levered free cash flow has seen a YoY improvement, it’s at a very low margin. This could be a concern as we see a company that is struggling with its profit margins, taking on more debt and decreasing in total cash within a very competitive and fast-paced industry.

Annual debt intake (Seeking Alpha)

Total Cash and short term investments (Seeking Alpha)

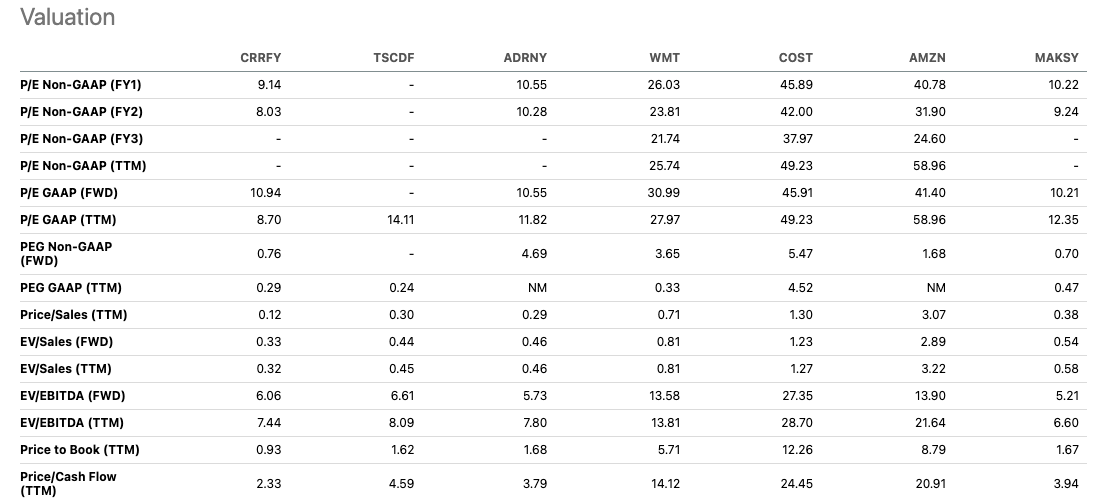

Valuation

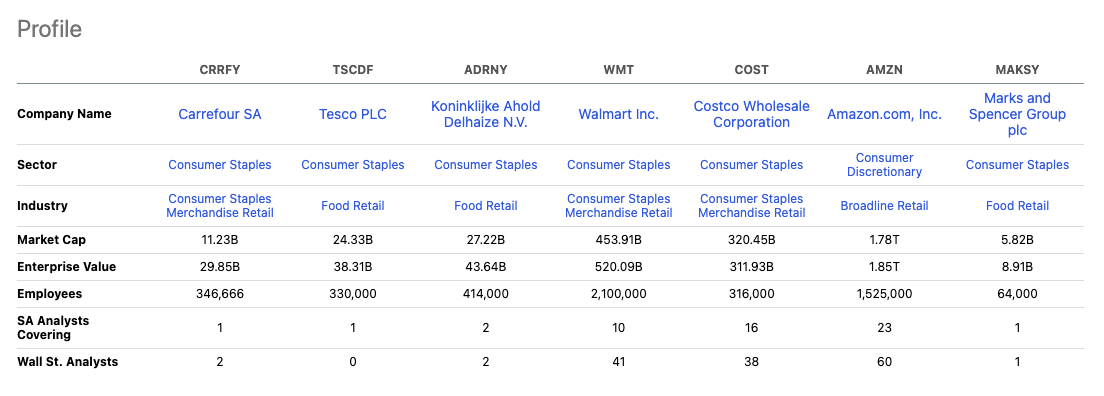

After comparing Carrefour with its peers in the retail and supermarket industries, it becomes apparent that the company’s forward price-to-earnings ratio is one of the lowest, standing at 10.94. However, upon closer inspection, it is revealed that Carrefour has one of the lowest five-year CAGR at 2.27%, coupled with the lowest EBIT margin at 2.66%. The company is also facing increased competition within the European market and is reducing its footprint in other markets to cut costs. These factors raise concerns about the company’s future performance. Therefore, I recommend waiting for clearer indications of a successful turnaround before taking a position in the stock.

Carrefour versus peers (Seeking Alpha)

Relative peer valuation (Seeking Alpha)

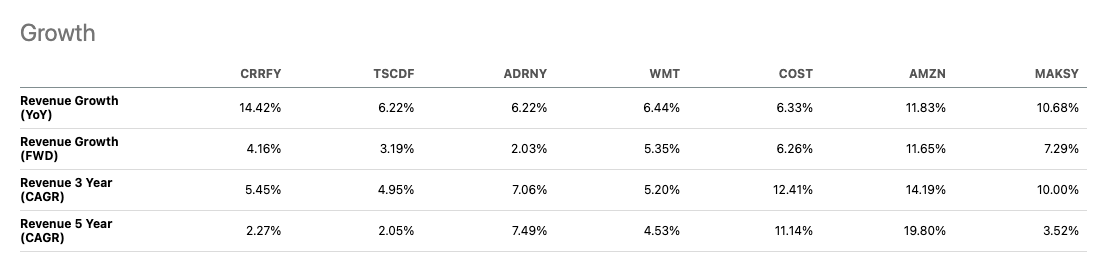

Growth versus peers (Seeking Alpha)

Profitability versus peers (Seeking Alpha)

Final thoughts

Carrefour has improved its top and bottom line since FY2021. However, the company’s significant failures in large international markets and its inability to meet changing consumer demands have left a bad taste in the mouths of many investors. The company has an attractive price-to-earnings ratio relative to many of its peers, but it generates the majority of its revenue from slow-growth mature markets. Carrefour is considered the world’s fifteenth-largest supermarket chain in terms of its market cap. It is aware of the importance of an omnichannel sales position, is investing in this, and has ambitiously worked on a 2026 plan. But for a company that has seen little stock growth in the last five years and lacks major growth drivers, I do not recommend investing and giving it a hold position.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")