stanley45/iStock via Getty Images

Age-related macular degeneration (AMD) is the most common cause of central vision loss and blindness in adults. Wet AMD comprises 25% of all cases of AMD and is characterized by new blood vessel formation in and under the retina. 75% of AMD is due to dry AMD (no new blood vessel formation). However, it can progress to wet AMD in a minority of patients.

AMD affects approximately 190 million people worldwide and is projected to increase to 250 million people by 2040. Approximately 5 million Americans have wet-AMD (more severe type). The annual incidence (new cases) of wet-AMD (more severe type) is 200,000 patients annually in the U.S. For this review, I will focus on wet AMD.

The pharmacological treatment of wet AMD is by vascular endothelial growth factor (VEGF) inhibitors. These drugs include aflibercept (Eylea) and ranibizumab (Lucentis). These drugs are administered as intravitreal injections (Eylea every eight weeks and Lucentis every four weeks) and have similar efficacy. Eylea’s annual global sales were $9.6 billion in 2022.

A $10 billion/year problem

Patients with wet AMD need frequent injections every 4 to 12 weeks (depending on the treatment regimen). Patients continue to experience a loss of vision over time with frequent injections. There is a need for newer therapies in wet AMD with less frequent injections that can maintain vision over time.

There is a lucrative global revenue opportunity of $10 billion/year for newer anti-VEGF therapies, which can offer less frequent injections in wet AMD while maintaining vision and acceptable safety.

The solution: Current developmental landscape of long-acting anti-VEGF therapies

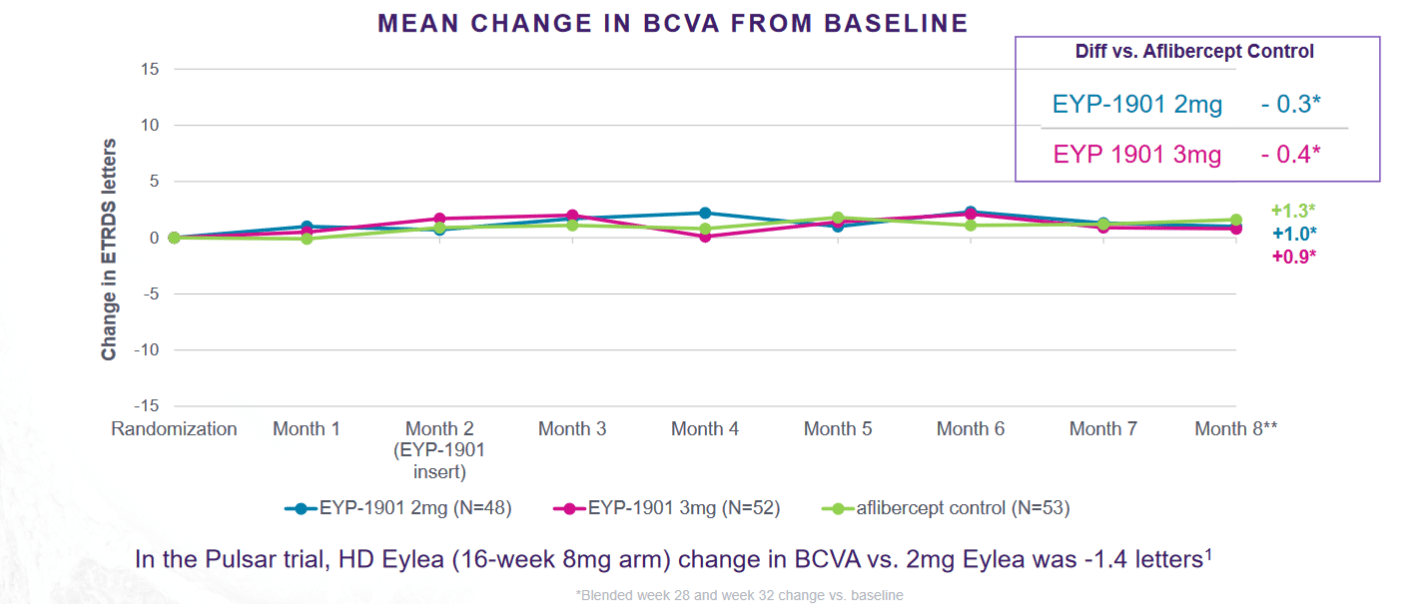

Eyepoint Pharmaceuticals (EYPT): The company is developing EYP-1901, vorolanib (tyrosine kinase inhibitor) with bioerodible Durasert, its sustained-release intravitreal drug delivery technology. Phase 2 data in controlled, previously treated wet-AMD showed statistical non-inferiority in BVCA (a measure of vision) compared to Eylea in 102 patients with up to eight months of follow-up. There was a 80% reduction in treatment burden. There were no significant treatment-related eye or systemic adverse events.

Twelve month data is expected in the second half of the year. A pivotal Phase 3 trial is expected to start in the second half of this year.

EYPT Phase 2 data in wet AMD (Investor presentation)

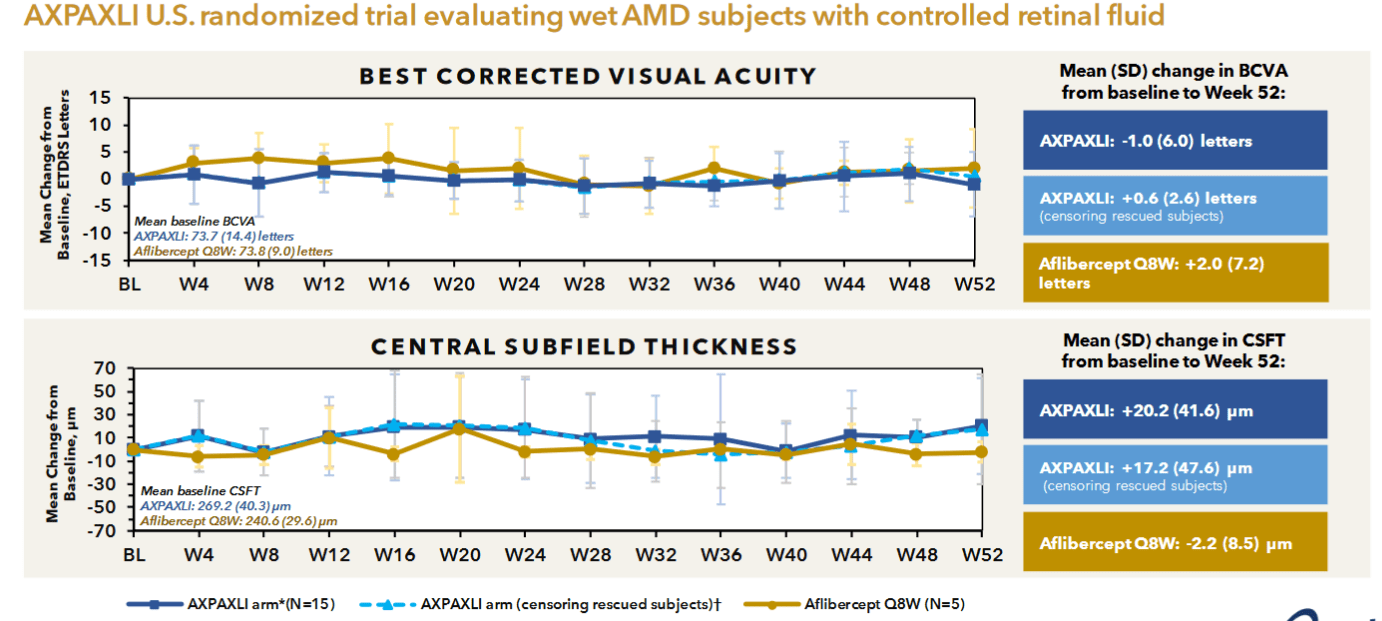

Ocular Therapeutix (OCUL): The company is developing Axpaxli, which consists of axitinib, a tyrosine kinase inhibitor in a single hydrogel implant using Elutyx technology to provide intravitreal sustained drug release.

Phase 1 U.S. randomized, controlled trial in sixteen previously treated, controlled wet AMD patients showed maintenance of vision and controlled retinal field (measured by central subfield thickness) for up to twelve months and an 89% reduction in treatment burden. There were no treatment-related ocular or systemic adverse events.

A Phase 2/3 pivotal SOL randomized, controlled trial has started screening patients for enrollment.

Axpaxli U.S. Phase 1 randomized trial results (Investor presentation)

Gene Therapy companies:

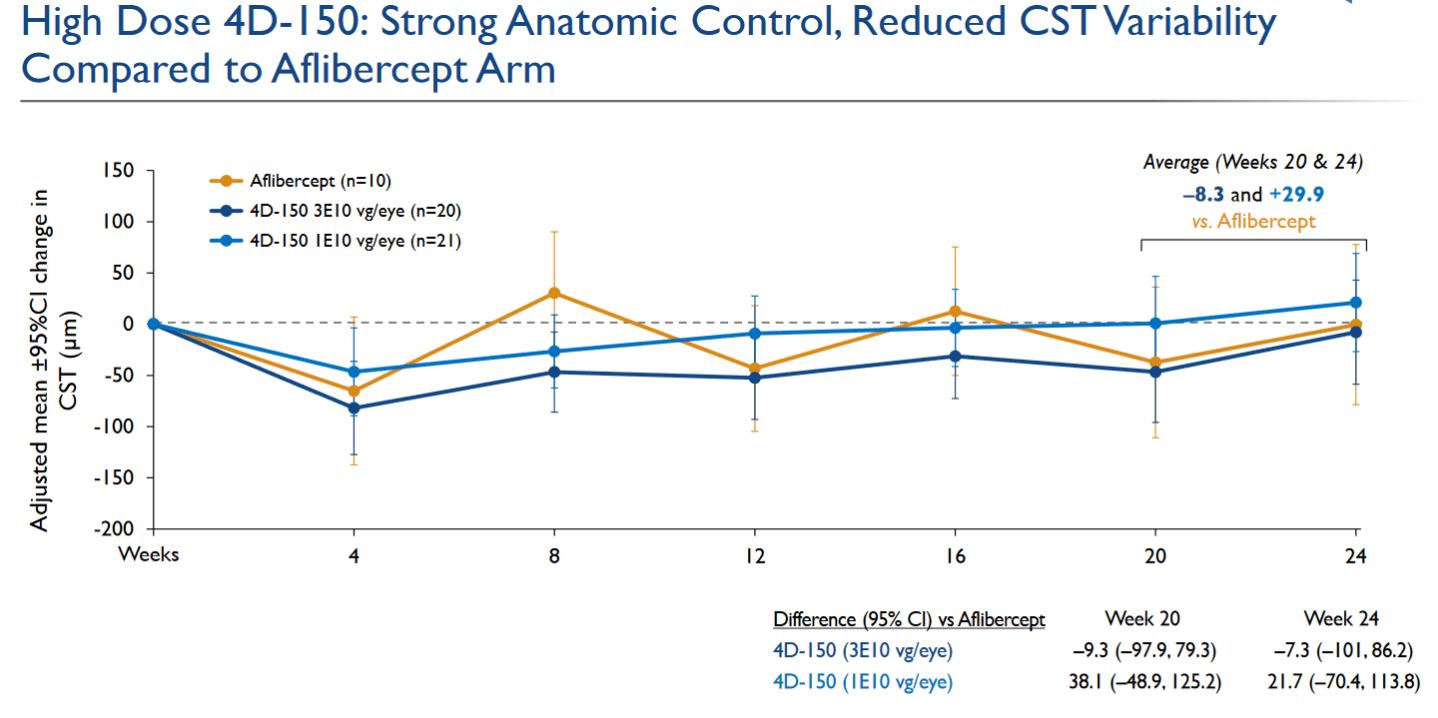

1. 4D Molecular Therapeutics (FDMT): 4D-150 is a gene therapy composed of R100 vector with a dual transgene payload consisting of Eylea and VEGF-C RNAi.

In the PRISM Phase 2 trial in 51 previously treated but uncontrolled (severe) wet-AMD patients with high treatment burden, the vision (measured by BCVA) was comparable to Eylea at six months. There was a reduction in variability in the central subfield thickness (which is linked to decreased legal blindness) and an 89% reduction in treatment burden at high doses (selected for Phase 3). 97% of patients needed treatment with prophylactic steroids, and there were no intraocular or systemic side effects like eye inflammation at high dose.

Phase 2 PRISM data in wet AMD (Investor presentation)

2. Adverum Technologies (ADVM): Ixo-vec is a gene therapy composed of AAV.7.m8 vector with a coding sequence for Eylea.

Phase 2 LUNA trial update in previously treated, high-treatment-burden patients showed maintenance of vision (measured by BCVA) in 60 patients at 26 weeks compared to Eylea. The company had issues with anterior chamber inflammation with its gene therapy in the past, needing topical steroids and is targeting to identify an optimal prophylactic regimen in the LUNA trial (which was identified). Over 90% of patients treated with the prophylaxis had no or minimum eye inflammation. The company has shown stable Eylea levels in the eye for up to 4.5 years in the OPTIC trial.

A Phase 3 trial is expected to start in the first half of 2025.

3. RegenexBio (RGNX): ABBV-RGX-314 gene therapy with NAV, AAV8 vector (partnered with AbbVie (ABBV)) administered through a suprachroidal route showed maintenance of vision (measured by BCVA) at six months compared to Eylea in previously treated, controlled patients in Phase 2 trial. There was a 80% reduction in treatment burden. There was no significant eye inflammation after a steroid prophylaxis regimen. Some treatment-related adverse events like conjunctival hemorrhage, increase in intraocular pressure, episcleritis, and conjunctival hyperemia were seen.

The above gene therapy was tested in another Phase 2 trial earlier using a subretinal route. The vision was preserved for up to six months. However, treatment-related adverse events similar to those seen above were seen.

Discussion

For longer-term sustained delivery, an intravitreal drug delivery system like those being developed by (EYPT) or (OCUL) seems to be a preferred solution. All of the above gene therapy solutions have side effects of eye inflammation and require prophylaxis with steroids. I like (FDMT) among gene therapy players due to their efficacy in uncontrolled, severe wet-AMD patients, where I believe gene therapy may have an advantage over sustained-release inserts and may find a niche justifying its high cost and need for steroid prophylaxis. (ADVM) still has around 10% of patients with eye inflammation despite steroid prophylaxis, and (RGNX) has other treatment-related eye side effects, as mentioned above.

For patients with controlled disease on Eylea injections, I like the statistical non-inferiority in the maintenance of vision compared to Eylea (shown by EYPT). Rival (OCUL) has longer-term 12-month data, and I will be interested in the 12-month data by (EYPT) in the year’s second half.

The reward for developing a safe and efficacious sustained drug delivery system as a substitute to frequent Eylea injections every eight weeks can be estimated from Lucentis, which reached $3.5 billion in global annual sales despite the need for frequent 4-weekly injections.

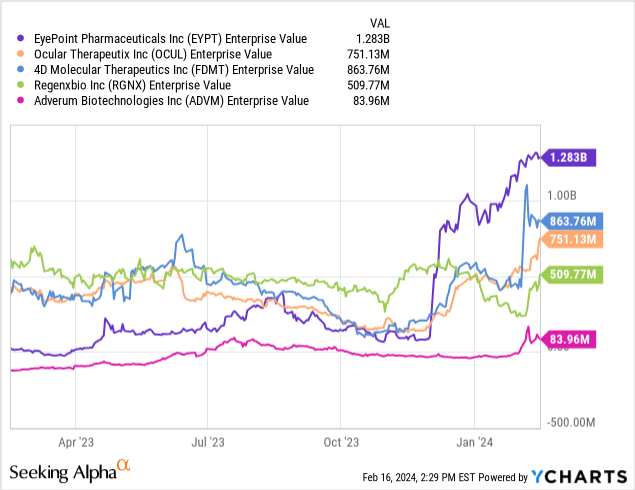

As shown in the graph below, the enterprise value of the competing companies in this field remains significantly undervalued even if we consider a target of $1 billion/year in global sales for the top-selling sustained release substitute for Eylea (biotech usually trades at enterprise value/peak sales of 6-7). Even (EYPT) which has the highest enterprise value of $1.28 billion in this group, is undervalued considering its shot at $1 billion/year in sales (where it could trade at $6 billion-7 billion enterprise value).

Q2 2024 Earnings Call Transcript")