SOPA Images/LightRocket via Getty Images

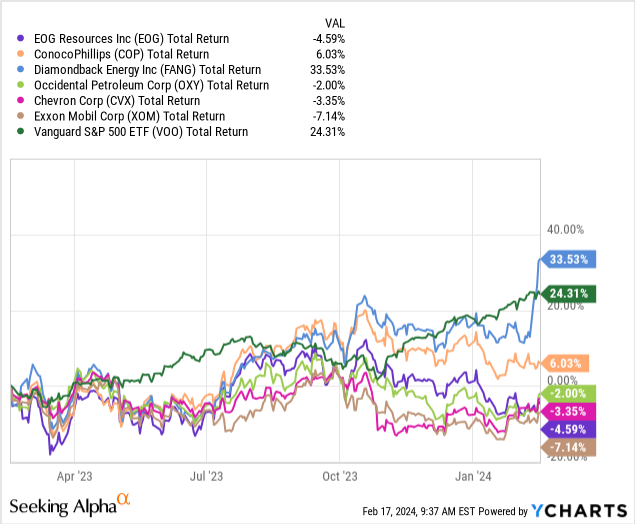

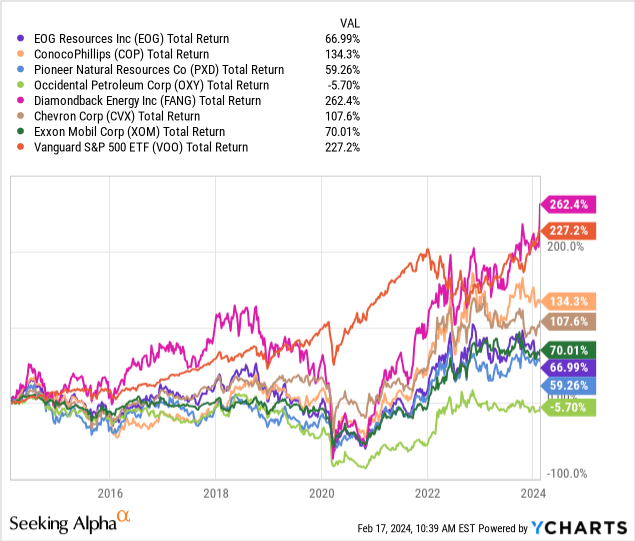

In my last Seeking Alpha article on EOG Resources (NYSE:EOG) I rated the company a HOLD because I did not see any near-term catalyst to propel the shares higher and expect O&G prices to decline (see EOG: Quiet Accumulation Vs. Splashy M&A). Shares are down 10.6% since that article was published – mostly due to the price of WTI weakening. Over the past year, EOG has been an under-performing company as compared to its peer group (see the graphic below). The company is scheduled to report Q4 and full-year 2023 earnings this coming Friday (Feb. 23rd) and today I will give a preview of that report and explain why I am upgrading EOG from a HOLD to a BUY.

Investment Thesis

As you can see from the above graphic, EOG has trailed all of the O&G companies selected in the comparison, other than Exxon (XOM). Of note is that all the O&G companies with the exception of Diamondback Energy (FANG) – due to its recent blockbuster Endeavor acquisition announcement – have significantly trailed the broad market returns as measured by the Vanguard S&P 500 ETF (VOO). This relative under-performance despite excellent operational and financial returns is one reason I now favor the stock.

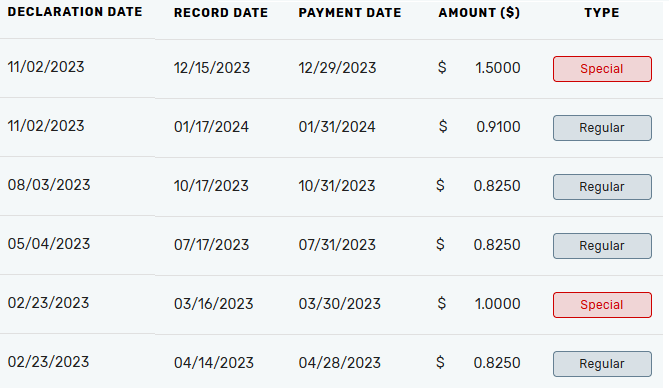

Another reason is that EOG’s dividend income and base-dividend growth (10.3%) over the past 12-months has been excellent:

EOG Resources

As you can see from the graphic, base-dividend payments, plus $2.50 in two special dividends, totaled $5.885/share. At Friday’s close of $113.56, that equates to a very attractive TTM yield of 5.18%.

From a return of capital perspective, during the Q3 conference call EOG CEO Ezra Yacob said:

In addition to announcing third quarter results yesterday, we demonstrated our confidence in the outlook for our business by increasing the regular dividend 10%, announcing a $1.50 per share special dividend and raising our cash return commitment to shareholders beginning in 2024, to a minimum of 70% of annual free cash flow.

Now, the regular dividend only amounts to ~$2.1 billion, and EOG could easily generate an estimated $6.2 to $6.4 billion in FCF in 2024 (based off of $1.5 billion of FCF generated in Q3). 70% of the midpoint of that estimate equates to ~$4.4 billion, which implies – in addition to the base dividend – another $2.3 billion for special dividends and/or share buybacks.

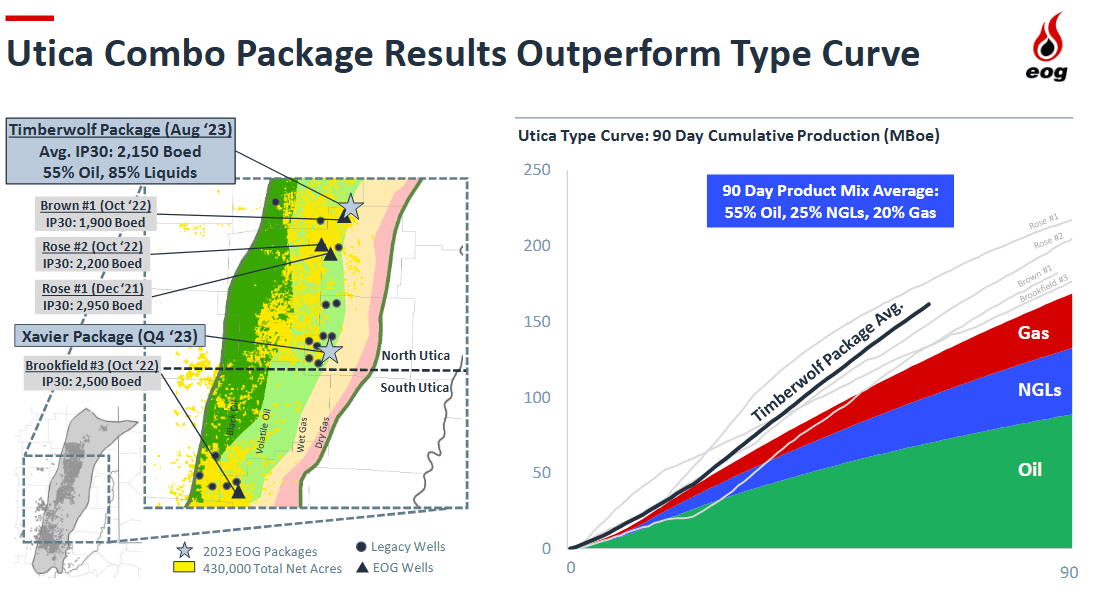

In the previous article referenced above, I explained how EOG had quietly assembled significant leaseholds in two emerging shale plays: the Utica Combo (430,000 net acres) in Appalachia and the Dorado gas-play (1,250 premium well locations) in South Texas. A slide from the Q3 presentation shows excellent results from the company’s recent “Timberwolf” wells:

EOG Resources

Another advantage of EOG’s Utica leasehold is that 90% of the acreage is already held by production. The point here is that EOG can take its time exploiting the play until it has optimized its completions recipes prior to going into a larger-scale “manufacturing mode”.

Meantime, over in the Permian, EOG reports continued improvement in the company’s Wolfcamp wells – raising production from 33 boe/ft in 2021 to an estimated 36+ boe/ft in 2023. This is more than 50% higher than the 23 boe/ft the company estimates it would take to achieve a 30% ROR with WTI at $40/bbl (let alone the current $79/bbl). And, don’t forget – EOG is one of the largest producers in the Eagle Ford and has an extensive position in the Bakken as well.

The point here is that EOG has long been considered one of the best and most well-respected shale operators and I see nothing to indicate anything has changed in that regard.

Q4 Earnings

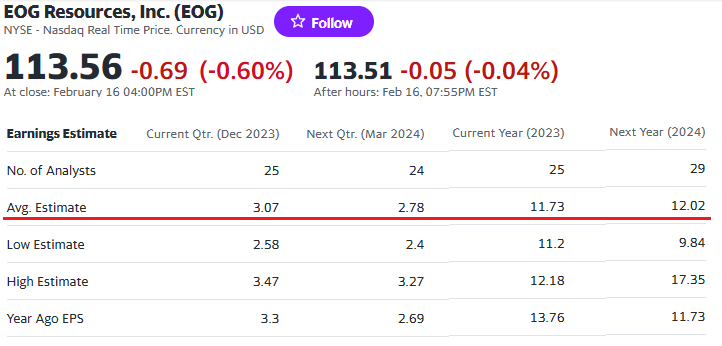

Consensus earnings estimates for EOG in Q4 are shown below per Yahoo Finance:

Yahoo Finance

As you can see, the weak prices of oil & gas (especially gas) has the Q4 consensus estimate at $3.07/share – down $0.23 from Q3 of 2022 (-7% yoy) – as quarterly revenue is expected to fall to $6.2 billion (-8% yoy).

However, note that most all of EOG tier-1 L-48 shale peers beat Q4 consensus estimates. For instance, ConocoPhillips (COP) beat by $0.23/share as L-48 shale production grew to 1.09 million boe/d (750,000 boe/d in the Permian). Now, COP is not a direct read-across to EOG given its significant presence in global LNG and the timing of those distributions, but it’s a good sign nonetheless. Occidental Petroleum (OXY) – perhaps a closer peer – also beat, but not as widely as COP. Chevron (CVX) and Exxon (XOM) also beat estimates, although they are not as good of a proxy for EOG as they have strong downstream operations. But the point here is that EOG shareholders can expect the company will likely beat the $3.07/share consensus estimate shown above.

Valuation

The table below compares EOG’s market-cap, TTM P/E, base-dividend, and base-dividend yield versus some of its peers:

| Mkt.Cap | TTM P/E |

Base Dividend |

Base Dividend Yield |

|

| COP | $130.1 billion | 12.2x | $2.47 | 2.23% |

| EOG | $66.2 billion | 8.4x | $3.64 | 3.21% |

| PXD | $54.1 billion | 11.0x | $13.96 | 6.03% |

| OXY | $53.2 billion | 15.5x | $0.88 | 1.45% |

| FANG | $31.9 billion | 10.2x | $7.99 | 4.45% |

As you can see from the table, by market-cap EOG is currently the second largest upstream E&P of the group. However, Exxon will likely snap-up Pioneer and OXY is buying Crown Rock, lifting it significantly over EOG in both size and scale (especially in the Permian). Meantime, FANG’s planned acquisition of Endeavor is going to lift it into the same class as EOG, but once again – bigger in the Permian.

EOG’s lack of big Permian acquisitions is likely the primary reason why the company trades at a significant discount to others in terms of TTM P/E. I feel that the discount is somewhat irrational given EOG’s existing 10-15 year drilling inventory (depending on the rate of drilling) and its long-term track record of delivering strong financial returns (and dividend growth).

In addition, and as I reported in my last article, EOG is debt free. That is a huge advantage against a company like OXY that ended FY23 with $16.5 billion in net-debt, which is likely one big reason OXY’s dividend is so weak relative to EOG and its peers. Note OXY also has the highest TTM P/E valuation of the group. That is even more of a head-scratcher to me considering OXY has a chemicals segment that is performing very poorly. No thank you.

Rationale For Rating Upgrade

I’ve already discussed EOG stock’s under-performance against its peers and its lower valuation despite excellent operational and financial performance (and strong dividend payments). Although seemingly forgotten during the merger-mania, EOG is one of the most prolific shale oil producers in the United States.

In addition, consider that EOG is going to benefit from the big mega-mergers in the Permian despite not participating. Why you ask? Because as big companies like COP, CVX, and Exxon expand their footprints, and with the last two big private Permian producers (OXY’s $12 billion acquisition of CrownRock and FANG’s blockbuster $26 billion cash-and-stock agreement for Endeavor) being taken out, in addition to APA Corp’s (APA) takeover of Callon Petroleum (CPE), the consolidation and the size-n-scale of the remaining players means they are going to be in a much better position to control overall production from the play (which, of course, is the most important shale basin in the U.S. and arguably in the world). Over time, that should lead to higher prices, and – of course – EOG will be there to cash-in.

Lastly, although many refineries shut-down during the “shoulder season” for maintenance, soon following that is the summer driving season. With near record-low unemployment, a strong consumer, and lower gasoline prices, I expect relatively strong demand this summer. And, of course, the wildcard is the unstable Middle East … where anything can happen these days and I won’t even guess as to what that could be (but likely not good, unless you own some oil companies). What I do know is that unless there is an actual production outage, the global oil market looks relatively well-supplied and the current price environment (relatively strong oil, but very weak natural gas prices) will likely continue for months to come.

Summary & Conclusion

EOG has under-performed peers over the past year and is significantly undervalued in my opinion. To reach a TTM P/E of only 10x (a valuation that is still below its peers), the stock would have to trade up to $135 (+19%). Add in the 3.21% dividend yield and – in my opinion – you’ve got the potential for a relatively low-risk 20%+ return by investing in one of the best and most well-respected shale operators. EOG is a BUY, and could easily trade-up to $150 even if WTI only stayed in its current range ($75-$80).

I’ll end with a 10-year total returns chart of EOG versus some of its peers:

Note that all of these O&G companies – with the exception of Diamondback Energy – significantly under-performed the S&P500 as measured by the VOO ETF. This is why in all my portfolio management articles I stress the need for energy investors not to go massively over-weight the sector (which, from the comments I see on my O&G articles, appears to typically be the case …) and to, instead, build their portfolios on a foundation of the S&P500. Note also that on a total returns basis, both COP and Chevron have significantly outperformed EOG – and, amazingly, so too has even Exxon. It’s time for EOG to catch-up a bit … otherwise, it my find itself becoming an acquisition target.

Q2 2024 Earnings Call Transcript")