JHVEPhoto

Introduction

The consumer staples sector is an interesting one, especially during times of economic and business uncertainty. Consumer staples companies offer low-volatility options as investors seek less volatile and cyclical investments. These companies, known for their stability during economic cycles, present opportunities for investors, especially when leading ones suffer from a broad market sell-off.

One company in the sector is Kraft Heinz (NASDAQ:KHC), which is trading for a low valuation and should be analyzed. I previously held shares in the company and sold them following the dividend cut. Kraft Heinz sells everyday products that consumers purchase regardless of economic conditions. Therefore, I will try to analyze whether it can offer defensive qualities. Despite the company’s valuation, this article will describe my HOLD thesis on Kraft Heinz.

Seeking Alpha’s company overview shows that:

Kraft Heinz manufactures and markets food and beverage products in North America and internationally. Its products include condiments and sauces, cheese and dairy products, meals, meats, refreshment beverages, coffee, and other grocery products under the Kraft, Oscar Mayer, Heinz, Philadelphia, Lunchables, Velveeta, Ore-Ida, Maxwell House, Kool-Aid, Jell-O, Heinz, ABC, Master, Quero, Kraft, Golden Circle, Wattie’s, Pudliszki, and Plasmon brands. It sells its products through its own sales organizations and through independent brokers, agents, and distributors to chain, wholesale, cooperative, and independent grocery accounts.

Fundamentals

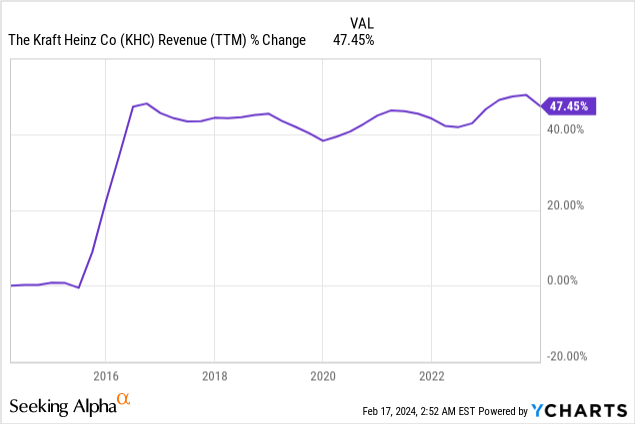

Kraft Heinz has enjoyed a 47% increase in sales over the past decade. Almost the entire increase is thanks to the merger that formed the company. Following the merger, sales growth has faced challenges with a long period of stagnation as the company struggles to grow. Analyst consensus, as seen on Seeking Alpha, predicts that Kraft Heinz will continue to grow slowly with a 1.5% annual increase in sales in the medium term.

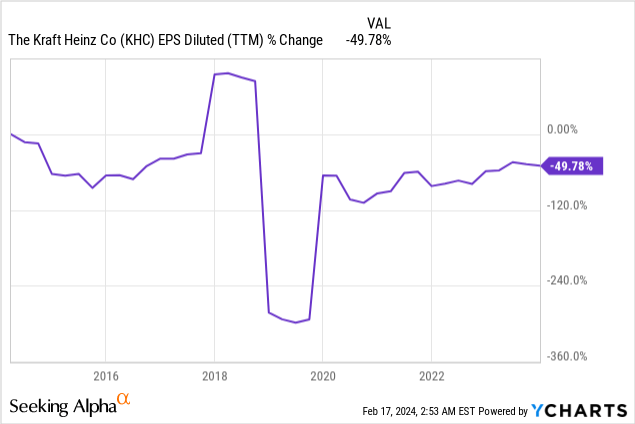

The company’s GAAP EPS (earnings per share) has seen a 50% decline over the past decade. However, the non-GAAP EPS, which excludes one-time noncash items, will look better, thus showing a 35% increase during the same period. Lower margins have played a role in the gap between sales and EPS growth and the share issuance to fund the merger. Seeking Alpha’s analyst consensus predicts that Kraft Heinz will achieve an annual EPS growth rate of 4.5% in the medium term.

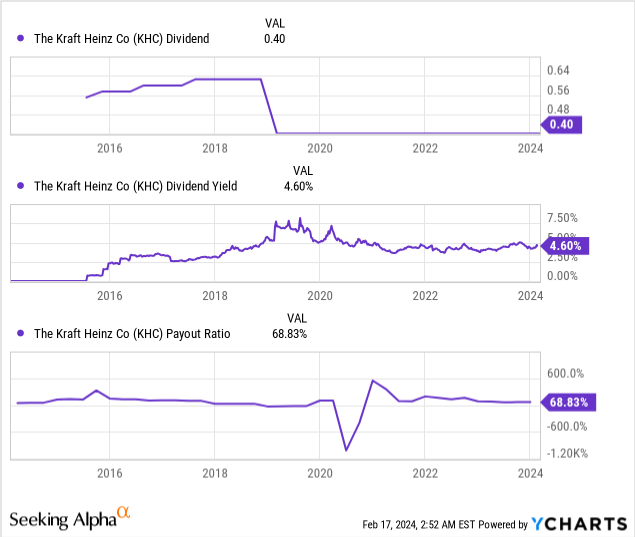

Kraft Heinz maintained its dividend payment over the last three years after a dividend cut in 2019 aimed at reducing debt load. The current annual dividend is $1.6 per share, frozen since the cut. While the payout ratio of 70% may look too high, the non-GAAP figures are better suited as they ignore noncash expenses and show a more sustainable payout ratio of around 50%. Investors should remember that further dividend increases might take time as the company works on growth initiatives and deleveraging efforts, but the current yield is attractive at 4.6%.

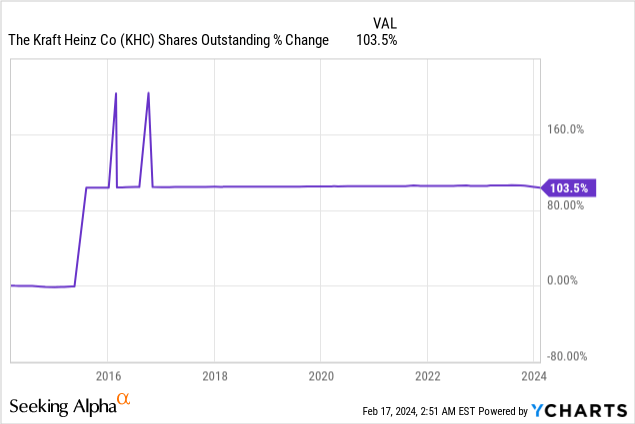

The company is not utilizing buyback in addition to dividends as many in its sector do. Kraft Heinz is focused on deleveraging and pays the other half of its EPS in dividends. The Kraft-Heinz merger has increased the share count by over 100%, and the company has brought it down by only 0.5%. When the company completes its strategic positioning and achieves growth with lower leverage, it may consider buying back stock.

Valuation

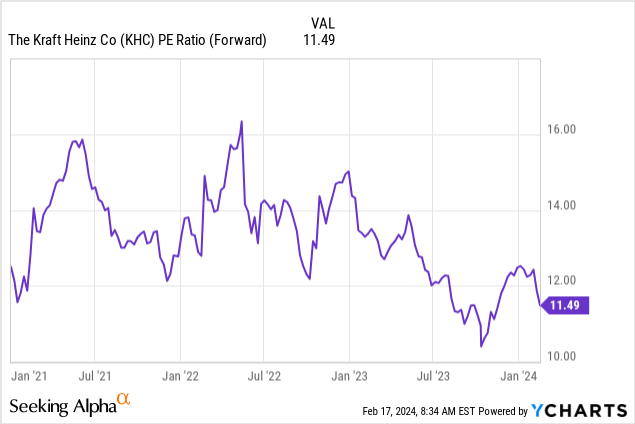

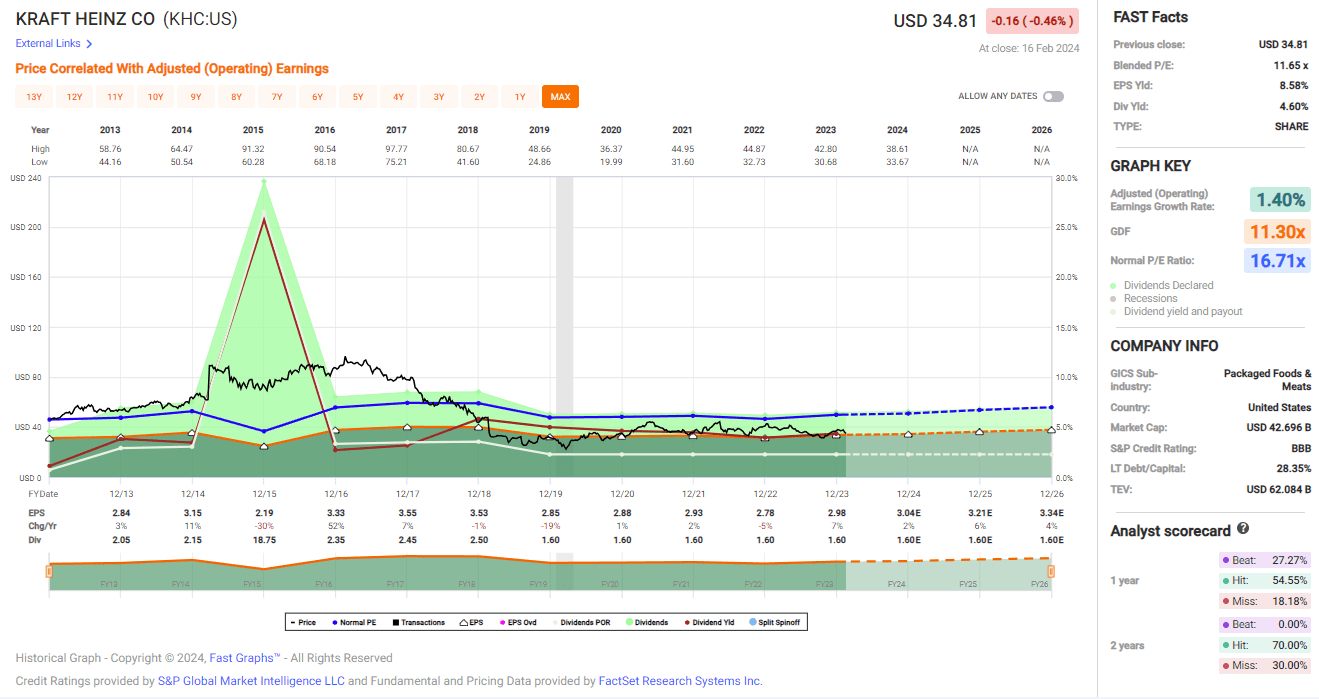

Kraft Heinz’s current P/E (price to earnings) ratio, based on the 2024 EPS estimates, is 11.5. It is much lower than we have seen over the past twelve months. The company’s anticipated growth rate of 4.5% may make the current valuation attractive. However, there is some investor skepticism due to the historical challenges of stagnation. Despite the positive growth outlook, the P/E ratio is low, thus implying that the shares are attractive if the company manages to reignite growth.

The graph below from Fast Graphs also shows the complex situation of Kraft Heinz. The average P/E ratio for the company over the last 20 years stands at 16.7. However, the current P/E ratio of 11.5 reflects a lower valuation due to the prolonged stagnation and investor skepticism. The average annual growth rate for the company over the same period is 1%, amplifying the long-term stagnation, and the current forecasted growth rate is 4.5%. Therefore, we have a lower valuation and a faster growth rate, but with skeptical investors who first want to see some growth initiatives succeeding.

Fast Graphs

Opportunities

Kraft Heinz has three main growth opportunities. They’d be the pillars of its long-term future growth. The company sees significant growth opportunities in its global Foodservice business, with a Q4 sales growth of approximately 7%. The company wants to continue this momentum, targeting new, attractive, and higher-margin channels offering restaurants and other distributors a more tailored service, such as Ketchup dispensers. The focus is on driving success in Foodservice by capitalizing on consumer trends and leveraging its portfolio to capture market share where demand meets competitive edge, making it suitable for a specialized service and offerings.

“In 2023, our Global Foodservice business delivered approximately 7% sales growth. North America Foodservice grew approximately 5%, and our international zone grew more than 10%, outpacing industry growth.”

(Carlos Abrams-Rivera, Chief Executive Officer, Q4 2023 Conference Call)

The second opportunity is the strategic focus on new markets. The company strategically focuses on double-digit growth in Emerging Markets, with a Q4 organic net sales growth of 12.3%. The company has a data-centric, go-to-market model that has successfully expanded distribution. It offers different markets different products from its portfolio, making it more efficient and precise. For 2024, the goal is to sustain this growth opportunity by leveraging this tailored model and expanding into new categories and markets, improving both volumes and prices.

“Our go-to-market model drives our strategy for growth in Emerging Markets. This data-centric, repeatable model drives distribution and is designed to capture opportunities with the right product in the right market.”

(Carlos Abrams-Rivera, Chief Executive Officer, Q4 2023 Conference Call)

The third growth opportunity is focusing on its most promising products. Kraft Heinz continues its market share improvement in U.S. Retail GROW Platforms by focusing on innovation, marketing, and resolving supply constraints. These products include organic food and cream cheese, for example. Despite industry challenges, the company has successfully executed action plans that led to share gains in these critical categories. It will continue to do so in 2024 and may add additional products as its investments in marketing succeed.

“The improvement we saw in market share performance was driven by action plans we set at the beginning of the year. We executed our joint business plans with key customers to drive shelf space and quality merchandising, with a 1.5 percentage point share of shelf expansion versus the prior year.”

(Carlos Abrams-Rivera, Chief Executive Officer, Q4 2023 Conference Call)

Risks

Kraft Heinz faces challenges from a changing consumer taste as more consumers seek value over brands. The impact of higher interest rates on consumer spending remains a risk, affecting consumer behaviors. Moreover, changes in the economic environment, like reductions in government programs like SNAP benefits, can negatively affect the company’s sales performance.

“First, the industry was more challenging than we had originally anticipated as the impact of higher interest rates continues to weigh on the consumer and the impact from lapping excess SNAP benefits in the quarter hit peak levels.”

(Carlos Abrams-Rivera, Chief Executive Officer, Q4 2023 Conference Call)

Another risk is the inventory reduction following supply chain challenges. The company experienced difficulties in Q4, including trade timing and a retailer inventory reduction, which impacted organic net sales performance. While some of these factors were anticipated to be one-time occurrences, if they happen again, it may hurt the company’s performance in critical products and decrease the credit investors give the company even more. Therefore, this risk may lead to lower revenue growth and valuation due to a lack of trust.

“The trade timing was a one-time occurrence and a function of lapping a prior year trade accrual release. With regards to the inventory deload, this is anticipated to be limited to the fourth quarter.”

(Carlos Abrams-Rivera, Chief Executive Officer, Q4 2023 Conference Call)

Third, Kraft Heinz faces uncertainties related to the economic environment, with inflation decreasing but still impacting costs. The company also has to deal with a high-interest rate environment. While the company did lower the net debt to EBITDA to 3, the higher rates will mean that future debt will carry a higher rate, thus pressuring the margins. Balancing inflationary pressures while maintaining profitability and market share poses challenges.

“Overall, the cost environment is getting better. Inflation is moderating, but on a year-over-year basis, costs are still higher. In regard to consumer health, we continue to see a pressured consumer, with a retained focus on seeking value. And at the same time, the interest rate environment remains high.”

(Andre Maciel, Executive Vice President and Global Chief Financial Officer, Q4 2023 Conference Call)

Conclusions

Kraft Heinz was created in its current form in a mega-merger in 2015. Since then, the company has stagnated. It has cut the dividend to reduce debt and failed to reignite growth. The company’s growth opportunities lie in a strategic shift, focusing on emerging markets, Foodservice, and crucial segments in the U.S. Until it shows some growth, it will likely continue to fail in building investor confidence after a dividend cut and a long stagnation period.

As investors, we must balance between the promising growth opportunities that showed a tiny glimpse of success in 2023 and the attractive valuation, with the history of execution failures, dividend cuts, and risks. Therefore, I believe the shares are a HOLD. I will consider investing in the company if the P/E ratio is 8-9 or if the company manages to achieve a mid-single digits growth rate for two years in a row (following a 7% growth in 2023, the forecast for 2024 is 1.7%).

Q2 2024 Earnings Call Transcript")