Yuichiro Chino/Moment via Getty Images

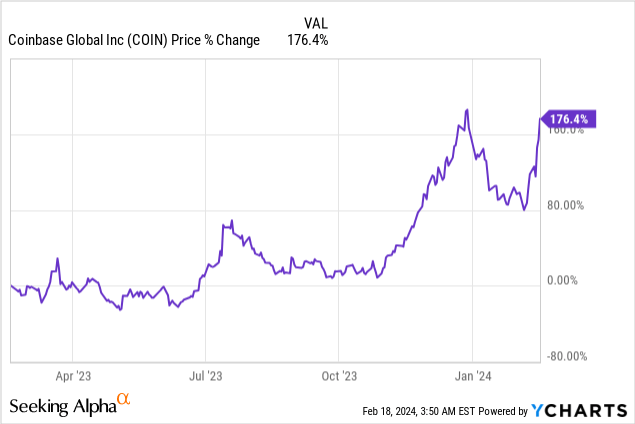

Shares of Coinbase (NASDAQ:COIN) have soared after the company submitted a much better than expected earnings sheet for the fourth-quarter on resurging trading volumes. The company’s fundamentals are improving due to a broad recovery in the cryptocurrency market. The current rally in Bitcoin (BTC-USD), driven by the SEC’s greenlighting of ETFs that trade Bitcoin, reflects growing confidence in the cryptocurrency market. Coinbase is also a more diversified bet on the crypto economy as the company is growing its non-trading related service revenues. I believe the risk profile is now much more favorable than last year and shares are a buy!

Previous rating

My last rating on the cryptocurrency marketplace was hold – The Risk Matrix Has Changed (Rating Downgrade) – as I saw a deteriorating risk profile in 2023. However, Coinbase is seeing a huge rebound in trading volumes and has cut operating expenditures aggressively last year. With Bitcoin soaring and both individual and institutional investors trading more on Coinbase’s platform, the near-term earnings outlook has drastically improved.

SEC’s Bitcoin ETF greenlighting is a catalyst for Coinbase

Coinbase delivered strong results for its fourth-quarter as well as FY 2023 with revenues soaring, driven by a recovery in the cryptocurrency market. This broad-based market recovery has been driven by improving investor sentiment, which at least in part was supported by the Securities and Exchange Commission approving the first U.S. spot bitcoin exchange-traded funds in January. This decision which has led to the creation of a number of Bitcoin ETFs has been a catalyst for Bitcoin as well as for other currencies like Ethereum (ETH-USD).

Bitcoin-focused ETFs use cash to buy Bitcoin which fundamentally boosted demand for the cryptocurrency. The SEC stamp of approval was a vote of confidence in Bitcoin especially and has led to a sharp uptick in the price of Bitcoin, other digital currency prices as well as prices of those ETFs, such as the BlackRock’s iShares Bitcoin Trust (IBIT).

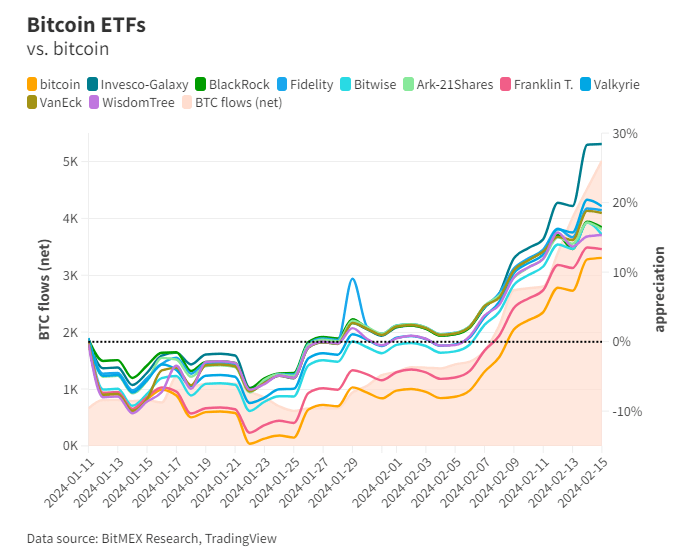

Bitmex

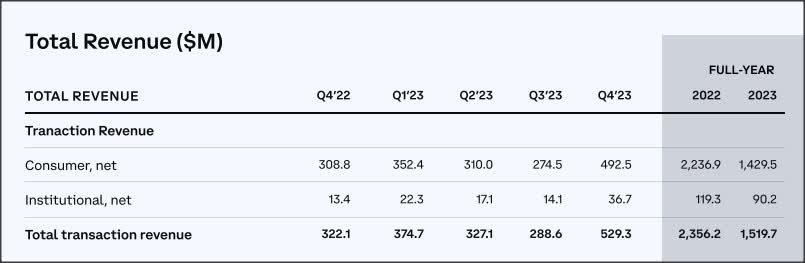

The expectation of a positive SEC decision with regard to Bitcoin ETFs has already led to a rally in cryptocurrencies in the fourth-quarter which has been reflected in Coinbase’s soaring transaction revenues. Attracted by growing prices for cryptocurrencies, traders jumped on the bandwagon, causing Coinbase’s transaction revenues to soar 64% Y/Y in Q4’23 and reach $529.3. While FY 2023 revenues came in 36% below the FY 2022 level, the Q4’23 trend and the Q1 SEC decisions are favorable tailwinds for Coinbase as well as the wider cryptocurrency market.

Coinbase

Interestingly, institutions drastically increased their trading on the Coinbase platform in Q4’23, likely in anticipation of the SEC’s decision about Bitcoin exchange-traded funds. Institutional transactions revenues increased 160% Q/Q while retail customers were responsible for a 79% Q/Q jump in transaction revenues. Retail customers still account for the overwhelming majority of 93% of all transaction revenues, however.

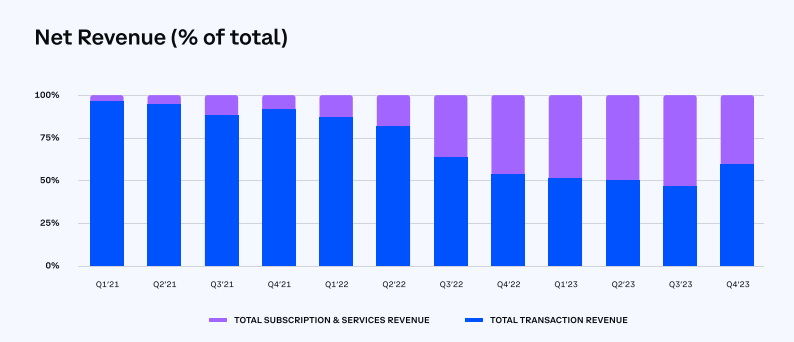

What has changed since last year is that Coinbase has become a lot more diversified in its revenue picture and has made an effort to reduce its reliance on volatile and unpredictable transaction revenues. Coinbase has grown its subscription and services revenues significantly (+78% Y/Y) to $1.4B in FY 2023 and these services include blockchain rewards, custodial services, interest income on loans to customers as well fees from issuers for stablecoins. In FY 2023, 48% of net revenues came from non-transaction related services compared to just 25% in FY 2022. This diversification serves to reduce the volatility of Coinbase’s revenues going forward and should lead to a more stable earnings profile as well.

Coinbase

Drastic cuts to operating expenditures now paying off

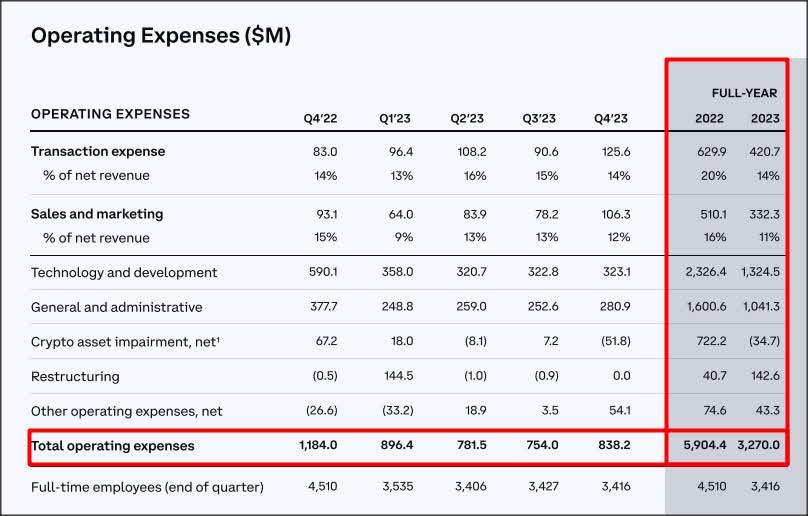

During the last cryptocurrency bear market, Coinbase laid off workers and cut back aggressively on costs which is now paying dividends for the company. Coinbase today is a much leaner company with its operating expenses declining 45% between FY 2023 and FY 2022.

Coinbase

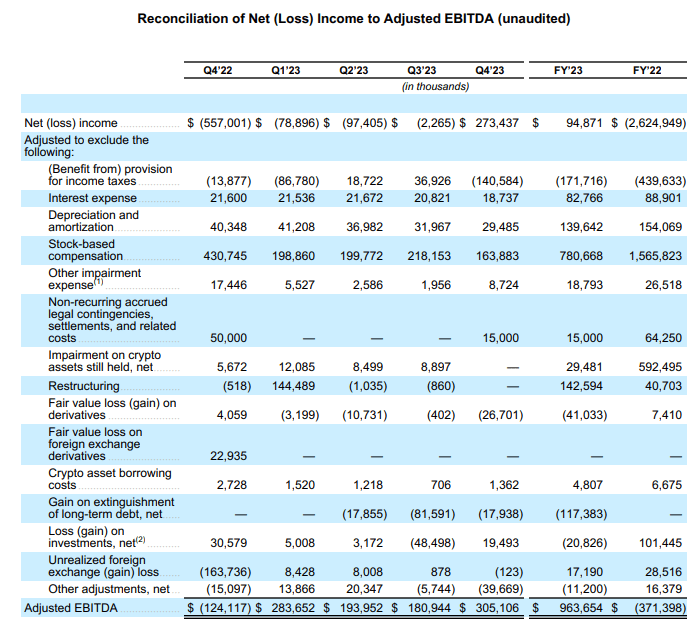

Changes in the operating expense structure combined with a surge in trading volumes as well as growth in non-trading related subscription/service revenues have pushed Coinbase into solid adjusted EBITDA territory last year. Coinbase generated $963.7M in adjusted EBITDA in FY 2023, showing a $1.3B swing relative to FY 2022. The improvement in EBITDA was mainly driven by changing trajectory with regard to Bitcoin which soared from a price below $16k in November 2022 to almost 52k as of February 18, 2024.

Coinbase

Coinbase valuation

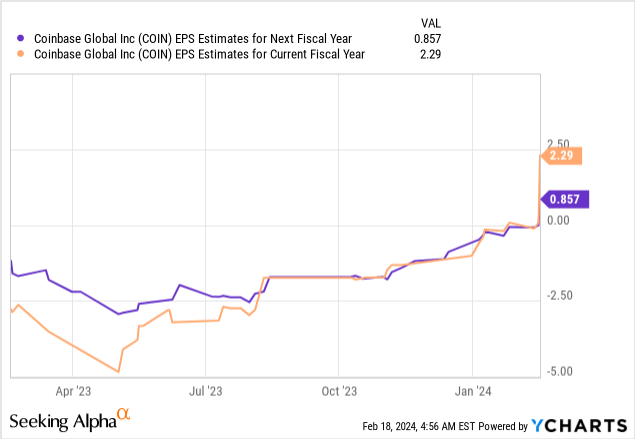

Cryptocurrency adoption is growing and the SEC’s decision to allow investment companies to start Bitcoin trading ETFs has led to an improved industry setup. This could translate into strong earnings growth for Coinbase which sits right at the nexus between the real and the digital economy. Coinbase is expected to generate $2.29 per-share in earnings this year, but earnings estimates are rising fast.

During the bull market of FY 2021, Coinbase earned $14.50 per-share, but the company is now much leaner and more diversified, and has therefore considerable earnings upside. Calculating with only $14.50 per-share in annual earnings potential, Coinbase is currently valued at a P/E ratio of 12.0X (based off on peak earnings), but has traded at P/E ratios way above 18X during the 2021 bull market. Assuming a conservative 15X P/E ratio, which I believe is fair given the massively reduced volatility in net revenues and solid platform profitability today, I see a fair value for Coinbase at ~$217.

Risks with Coinbase

Coinbase’s risks are chiefly of a regulatory nature. As far as the risk profile more generally is concerned, I believe the massive shift of net revenues toward non-trading related net revenues has reduced the risk profile for Coinbase drastically, as did the firm’s aggressive cost cuts and headcount reductions. The biggest commercial risk that I see for Coinbase is a cyclical downturn in cryptocurrency prices as well as the risk of other trading platforms falling into bankruptcy. The bankruptcy of FTX in 2022 affected investors very negatively and a similar event could seriously hurt the recovering sentiment in the cryptocurrency market again, cutting into Coinbase’s upswing in trading volumes.

Closing thoughts

I am up-grading Coinbase to buy after the company crushed fourth-quarter expectations and COIN is now a solidly profitable cryptocurrency trading platform. The SEC’s decision to allow investment companies to start their own Bitcoin trading ETF products has done a great service for the restoration of investor sentiment, further legitimized the entire crypto economy, and is a catalyst for Bitcoin trading (demand) going forward. With Coinbase now being profitable, having a leaner and optimized cost structure, and being less dependent on traders for revenues, I believe shares of Coinbase are an attractive investment vehicle for investors to bet on the overall expansion and growth of the crypto economy!

Q2 2024 Earnings Call Transcript")