Alan Schein/The Image Bank via Getty Images

Thesis

The Manitowoc Company (NYSE:MTW) is currently experiencing headwinds from its EURAF segment due to softening demand in the European region, however, the robust growth in the MEAP segment and Americas segment is supporting the overall revenue and margin growth of the company. I anticipate that the company’s long term outlook is good due to strong backlog levels and continued healthy demand in the MEAP segment driven by a robust pipeline of Giga projects in Saudi. Also, the Americas segment looks good as it continue to increase its aftermarket service business and gain market share, which should drive the company’s top line in the coming years.

The company’s stock is currently available at a really attractive price point, and while the company’s long term prospects look decent, this should be a great opportunity to invest in this stock at the current levels.

Business Overview

The Manitowoc company (MTW) is among the leaders in providing engineered lifting solutions across the globe. The company with the help of its owned subsidiaries, designs, manufactures, distributes, and supports a large no of products including mobile hydraulic cranes, boom trucks, lattice-boom crawler cranes, tower cranes, and many other related products. The company operates under three major segments with a geographic reporting structure:

- Americas

- Europe and Africa (EURAF)

- Middle East, Australia, and Asia Pacific (MEAP)

The company’s products serve various industries, including construction, energy production/distribution, petrochemical and industrial, and infrastructure.

Last quarter performance

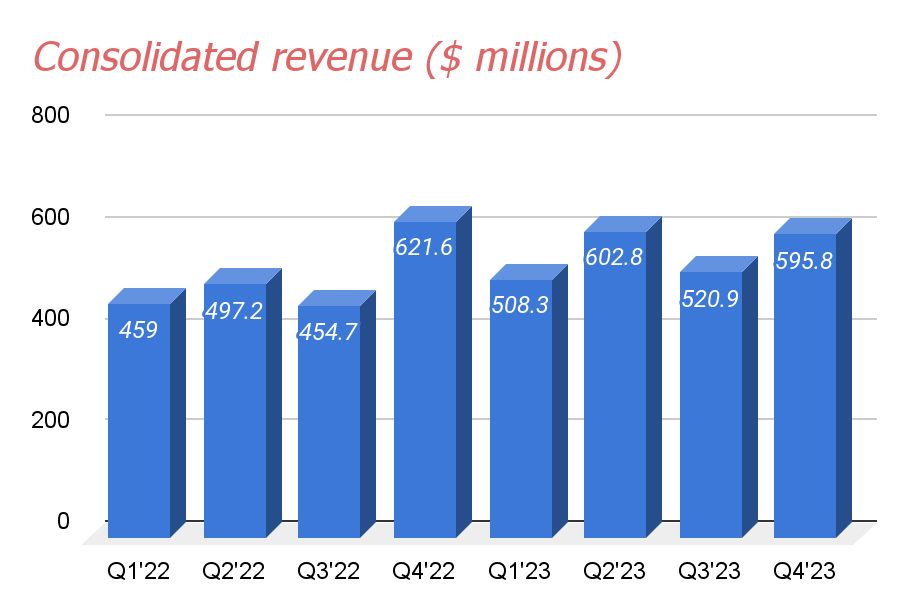

In the last quarter of 2023, the company reported its consolidated revenue at $595.8 million, beating the estimates by approximately $12.5 million. However, the revenue was down by 4.2% versus $621.6 million in the prior year quarter. This decline comes after consecutive double-digit growth in the company’s topline throughout 2023, as the demand in the Europe region continues to experience headwinds primarily in the tower cranes, due to a higher interest rate environment, which more than offset the benefits from global pricing efforts in the Americas segment. The Consolidated adjusted EBITDA margin also contracted by 220 bps to 6.1% during the quarter due to lower sales volume and an unfavorable product mix.

MTW historical revenue (consolidated) (Research Wise)

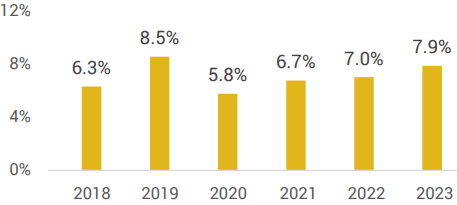

For the full year of 2023, the company’s top line grew 9.6% to $2.23 billion, thanks to a year of robust growth in both the Americas and MEAP segments and progress of the company’s CRANES+50 strategy. Margins for FY23 on the other hand expanded 90 bps to 7.9% versus FY2022.

The company’s total backlog on December 31st was $917 million, about 13% lower than prior year levels. Full-year 2023 orders totaling $2.82 billion, remaining flat year over year, however, decreased by $32 million on a currency-neutral basis.

MTW’s diluted EPS for the full year climbed 43% to $1.52 as compared to $1.09 in the prior year, however, missed the EPS estimates by $0.14.

Overall, apart from strong growth in FY2023, the company has consistently delivered double-digit topline growth year over year post-pandemic and margins have also improved significantly expanding by more than 200 bps from 5.8% in FY2020, which benefited the company’s bottom line in recent years.

MTW’s Annual adjusted EBITDA margin (MTW Q4’23 presentation)

Outlook

While the Americas and MEAP segments have shown strength throughout 2023, the continued softness in demand particularly in the Europe region of the EURAF segment has dragged down the overall topline growth turning negative in the last quarter.

I anticipate that the company’s revenue should continue to be under pressure in 2024 as well as the demand softness continued in the Europe region, which is on a higher end than anticipated. The TTM housing permits in the region were also negative with France and Germany declining 24% and 28% respectively during the last twelve months, which is also expected to hurt the segment’s revenue at least in the first half of 2024. In addition to this, the rental rate for top sewing cranes is also experiencing significant pressure in France further indicating towards weakening topline in the region.

While most of the company’s business in Europe is weak, the demand for Mobile cranes is still holding up in the region. In my opinion, support from this category should partially offset the negative impact of weakness in another category in this region. And, along with continued strength across the Americas and MEAP segment should help the company drive positive revenue growth in the second half of 2024, resulting in a flat to slightly positive topline growth for FY 2024.

What does the long-term hold?

While the company’s near term looks sustainable despite more than anticipated softening in Europe, thanks to strong America and MEAP, the long-term prospects of the company look promising as well, primarily due to multiple development projects of enormous scale in Saudi Arabia that continue to move forward.

Saudi Arabia is currently building the world’s largest roller coaster, which is expected to open in late 2024. And, the Cranes, that are being used in this mega project is the MTW’s Potain cranes. Just like this project, the construction of many more mega-projects is expected to continue in the next decade. A few more such projects include the construction of a large soccer stadium and a Formula One racetrack along with the necessary accommodations, which should fuel the company’s revenue in the coming years.

In addition to this, to support this rapidly growing region, the company launched two tower cranes in 2023 and is also in the process of developing three high-capacity models designed to serve its business operations in the Middle East market while also being well-suited for use in Hong Kong and Singapore.

While there are some near-term headwinds in the European region, the longer-term prospects appear to be favorable due to support from the heavier infrastructure market, which has benefited the demand for the company’s crane in the region. At the same time, the large commercial construction remains weak. This favorable factor should benefit the company’s revenue in the region once the overall economy starts to recover. Apart from this, the company is also increasing its fleet size to generate a recurring rental income and so far the company has increased its fleet from 124 units to 149 units during the last year, which should further support the company revenue in the longer term.

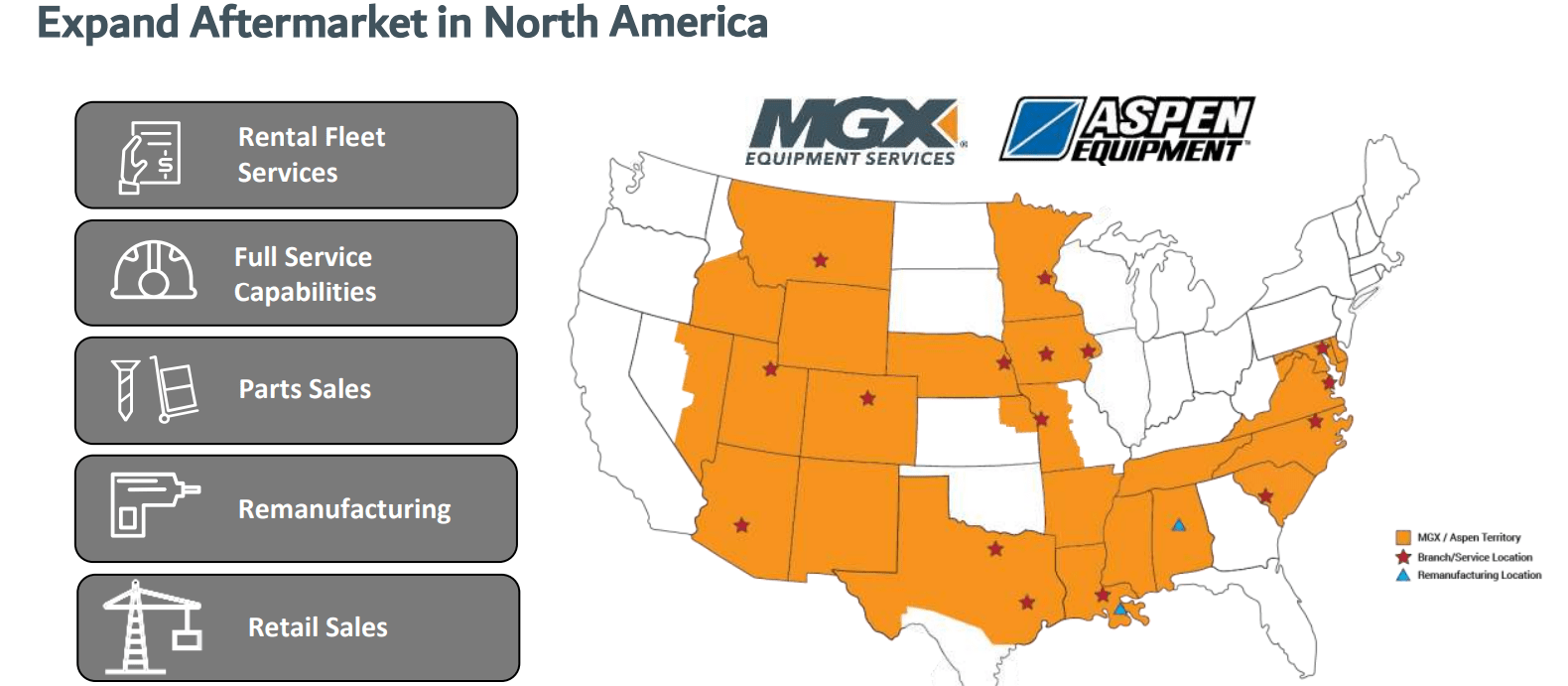

Talking about the Americas segment, MTW is working to expand its aftermarket in North America. And, to enhance its aftermarket services and support growth, the company established new facilities in Denver, Kansas City, and Aiken, South Carolina, and also added 22 new field service techs in the region. Not just in America, but the company is also focusing on its aftermarket growth in Europe as well, for which it hired new service techs and managers in the region.

Apart from these, the company is also working to increase its market share in the Boom truck business by benefiting from Aspen’s uplift capabilities and MGX’s reach, two businesses, that MTW acquired in 2021. And, as these acquisitions along with the acquisition of H&E’s crane business have been successful, the company continues to actively look for more expansion opportunities in the region. In my opinion, these initiatives by the company in North America should further drive the company’s revenue in the coming years.

MTW’s aftermarket growth (MTW presentation)

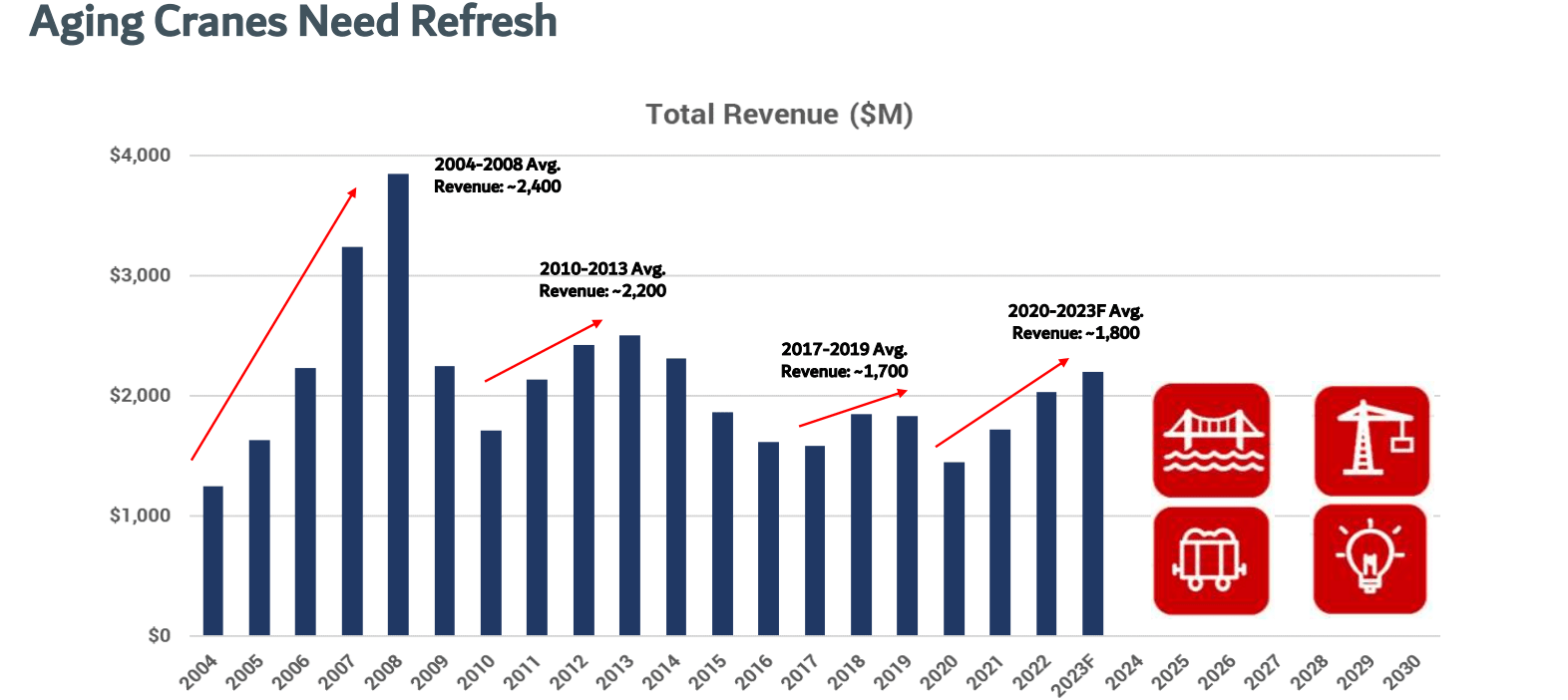

Overall, I am optimistic about the company’s long-term prospects across all the segmental regions due to anticipated healthy demand in the crane market globally. The backlog is also at a strong level, which, along with tailwinds from aging crane fleets around the world, investment under the infrastructure bill in North America, and a strong demand outlook due to a robust pipeline of Giga projects in Saudi Arabia should benefit the company’s business in the longer term.

Aging cranes data (Company presentation)

Valuation

On YTD, MTW’s stock was up about 7% until the beginning of this week. However, right before the earnings release for the fourth quarter, investors started to panic because of the consensus estimates which were expecting adjusted EPS to be down 67.6% to $0.24 for Q4’24. As soon as the company reported its EPS missing the estimates by $0.15 in its latest earnings, the company’s stock price fell by approximately 20% in just 2 days. However, in my opinion, the bottom line contraction is temporary and was primarily driven by lower sales and EBITDA due to the softening demand environment in the Europe region.

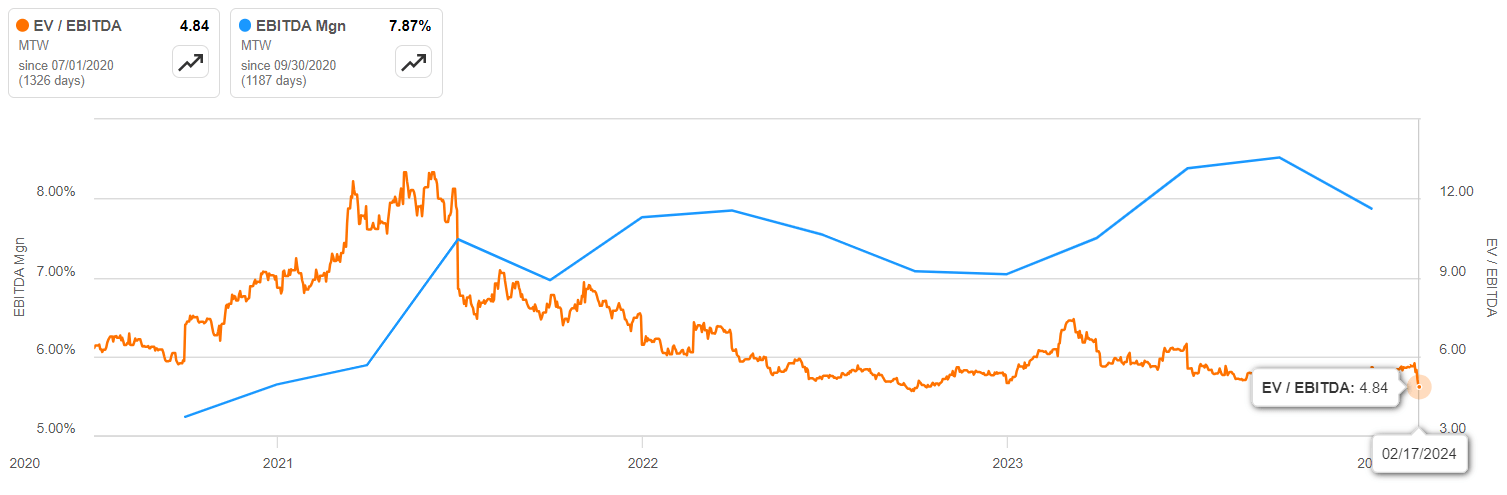

Currently, the stock is trading at a forward EV/EBITDA of 5.14 times, which is significantly below its five-year average of 7.47 and its sector median of 11.95. Post covid, the company has significantly improved its EBITDA expanding it to more than 200 bps to 7.9% in FY23 despite a weaker 2H23. I anticipate that the company is well positioned to continue this margin expansion in the longer term expansion with growing aftermarket services across the business which has a relatively higher margin, which should further improve the company’s valuation in the coming years.

EV/EBITDA chart (Seeking Alpha)

Risk

My thesis is built upon a consideration that, the softness in the European region should start to improve in the latter half of 2024. However, as the EURAF accounts for 37% of the company’s overall revenue, a major part of which comes from the European region can significantly impact the company’s business further if the weak demand environment persists, which could potentially drag the overall margins of the company resulting in a poor stock performance in the future.

Conclusion

As we discussed earlier, the company’s stock has corrected heavily in the past week due to below-expected results for Q4’23. Following this correction, the stock is presenting an even more attractive price point. In my opinion, the company’s long-term prospects look promising followed by robust pipeline of projects in Saudi in the coming decade and market share growth in certain businesses in the Americas segment. Topline growth in the longer term should also help the company in its margin expansion. The company’s valuation looks really good at the current levels, and considering the favorable longer-term outlook, I would recommend a rating of “STRONG BUY” on this stock.

Q2 2024 Earnings Call Transcript")