urbancow

Investment action

I recommended a neutral rating for Sensata Technologies Holding (NYSE:ST) when I wrote about it the last time, as I was worried about ST losing market share given that the win rate was soft. Because of that, I expected valuation to continue facing pressure at 10x forward PE. Based on my current outlook and analysis of ST, I recommend a hold rating. ST 4Q23 performance led me to become more bearish on the stock, but because my model suggests no major downside or upside, I am giving it a hold rating. The reason I became more bearish is because ST continues to face headwinds in the automotive end-market, which makes the near-term performance very uncertain. Also, management revised their margin guidance downwards in less than 6 months after the presentation in Sep’23, making me doubtful whether they can achieve the margin target for FY24 as well.

Review

For 4Q23, ST reported $992 million in revenue, ahead of consensus expectation for $979 million, and is at the high end of management guidance ($950 million to $1 billion). By segment, Performance Sensing reported revenue of $753 million, and Sensing Solutions reported revenue of $239 million. While revenue beat estimates, gross and EBIT margins underperformed. Gross margin was reported at 31.5%, 50bps below consensus of 32%, and EBIT margins saw 18.5%, also 50bps below consensus. Poor profitability led to EPS missing consensus at $0.81 vs. $0.86. Looking forward, management guided FY24 revenue growth of 2%–3% and EBIT margins sequential improvement of 20–30 bps throughout FY24, implying an operating margin of ~19.4% for 4Q24.

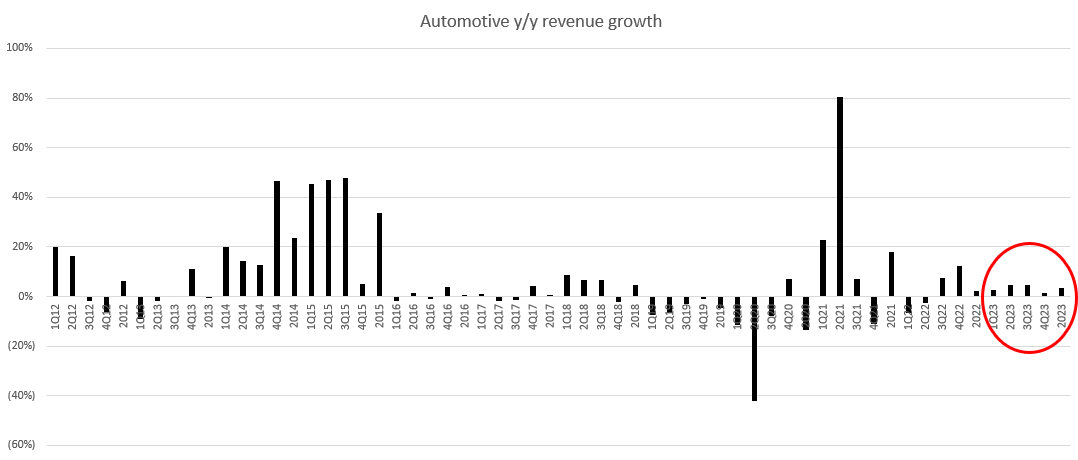

ST 4Q23 results led me to become more bearish on the stock. In particular, the results and guidance continued to highlight the end-market challenges (all end markets were down except automotive, whose growth was not spectacular as well) that the company has been trying to navigate. Automotive in particular has an uncertain outlook due to the following: uncertain auto volume outlook; a slowdown in the electric vehicle adoption; and challenges in the industrial and heavy vehicle off-road markets. Given that automotive only grew in the low single-digit percentage, these weaknesses could easily pull FY24 automotive performance into negative territory.

Author’s work

That trend is going to continue to the extent there is puts and takes in terms of the migration toward electrification, we have that natural edge in the business, and we’ve talked about the fact that if EV penetration slows down, it may impact the overall growth rate of the business, but it would be positive to the margin profile in the business.

We have also experienced market declines in inventory destocking in our heavy vehicle off-road and industrial end markets, adding to the pressure on growth. 4Q23 call

The pushback from bullish investors on this front is that the bookings will be structurally better from here onwards (ST booked $660 million in 2023, which was above the 5-year average), as a meaningful percent of recent bookings have been for EVs, which have a longer runway and more electronic parts than ICE cars. Management also specifically noted that they expect this elevated booking strength to continue into 2024; hence, the growth outlook is going to get more positive. My take is that, while EV penetration is positive, I am not sure if this tailwind is going to be as impactful as it seems. There has been an accelerating shift of market share from the western OEMs to the Chinese local OEMs, which is a margin headwind, as can be seen from management pulling back its 2024 margin targets, which were in the range of 20%–21%, to now track closer to ~19% (margins expected to improve 20–30 bps sequentially each quarter through the year as per the 4Q23 call), even as it maintains its outlook in relation to electrification revenues.

This has been disappointing. Specifically, revenue in our automotive business was negatively impacted by region mix, especially in China, where local OEMs have taken share from multinationals.

Further within China, we saw the added impact of share shift to more local OEMs from multinational players. In North America, EVs are 50% ahead of ICE vehicles in terms of average content given our higher market share among EVs. 4Q23 call

We expect savings of $4 million to $6 million in Q4 as part of our guide and savings of $40 million to $50 million in 2024. These actions are designed to help the company reach its stated goal of 20% to 21% adjusted operating margins in 2024. 3Q23 call

Regarding the sequential margin improvement in FY24, which is expected to be realized through productivity gains, I am not willing to take the leap of faith to assume it is surely achievable today. The reason is because a big assumption that management made is that the inventory situation in the industrial segment will see improvement in 2H24, while 1H24 will continue to face headwinds. From an expectation perspective, if the 1H24 inventory situation does not recover as much as expected, 2H24 will need to see a stronger destock in inventory. I just don’t think the market will be willing to take the risk of assuming a major recovery if 1H24 remains challenging. As such, what may happen is consensus taking a more conservative view and downgrading their estimates, further hurting the stock sentiment that is already under pressure from the margin guidance downgrade.

With an exception that destocking — with the expectation that destocking will end, our industrial end-markets will begin to grow again, reversing some of this trend later in ’24.

As such, if we combined the above outlook and narrative, the equity story for ST is as follows:

- Soft revenue growth (low single-digits) that is below the historical average

- Weak margin outlook

- Poor sentiment as management revise margin guidance downwards

Valuation

Author’s work

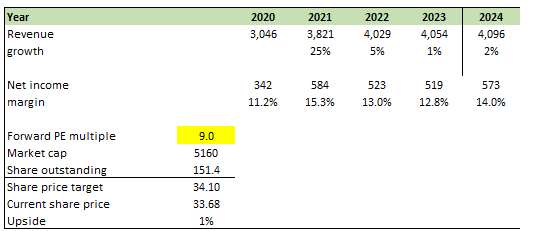

Giving management the benefit of the doubt, using their FY24 guidance, I got FY24 revenue of $4.096 billion (2% growth) and net income of $573 million (14% margin). Unlike my previous model, where I modeled 2 years out, I am now focusing more on the near-term (1-year outlook), as I am uncertain whether management can actually improve margin by as much as they guided for. Especially after they guide down margin expectations in just less than 6 months (the previous guide of 20–21% was in Sep’23). I have also downgraded my valuation multiple assumption, as I don’t see the market upgrading the multiple anytime soon unless ST can show that it is able to drive stronger-than-expected margin expansion or better-than-guided revenue growth.

Final thoughts

I remain hold rated for ST as it still faces a challenging outlook with uncertainties in the automotive end-market, which I believe contributed to a downward revision in margin guidance. Despite 4Q23 revenue surpassing expectations, weak profitability, particularly in gross and EBIT margins, led to a disappointing EPS. The reliance on EV bookings for future growth poses risks amidst market share shifts to Chinese OEMs. I am also slightly doubtful of management’s optimistic margin outlook for 2024, with sequential margin improvement. Considering the uncertainties, I am sticking to my hold rating.

Q2 2024 Earnings Call Transcript")