Andriy Onufriyenko/Moment via Getty Images

Investment Thesis

This article will touch on Enphase Energy, Inc. (NASDAQ:ENPH) that I see as a compelling investment in the renewable energy sector. My focus will mainly be on the company’s innovative solar solutions, and solid financials, and strategic expansions. Enphase has rolled out its IQ8 micro inverters and are expanding in a global sense to be sustainable for long-term growth. This is a great vision. My thesis will pick apart why Enphase, to me, is a valuable opportunity for investors. And I think it is showcased through their strategic initiatives. In essence, Enphase’s has innovative ideas, market insight, and financial strength that makes it an attractive stock for potential upside.

Enphase Energy Rating: Strong Buy

Introduction

Enphase Energy Inc. is a global energy technology company known for its innovative solar photovoltaic solutions. It specializes in the design and manufacture of micro-inverters. This is a critical technology that converts direct current (DC) generated by solar panels into alternating current (AC), which is used by homes and businesses. The company also offers an entire home energy solution through solar, storage, and management systems (very unique). Therefore, this provides people with a sustainable and reliable energy solution that is an alternative to industry standards.

Earnings Report and Forward Outlook

From what I see, Enphase Energy’s latest quarterly report illustrates financial discipline and strategic direction. The CEO, Badri Kothandaraman, commented stating that the company is operationally sound, which in his eyes is backed by the 1.6 million microinverter shipments and solid market share retention, despite inherent challenges. Notably, Enphase focused on aligning inventory with forecasts, demonstrating commitment to efficiency critical for success. I see Enphase as an attractive investment due to strong gross margins, free cash flow generation, and prudent market expansion efforts.

Financially, Enphase exhibits stability via $302.6 million in quarterly revenue and strategic inventory control. Global growth efforts position Enphase to capitalize on the accelerating renewable energy transition worldwide. While near-term guidance reflects justifiable conservatism, Enphase’s product pipeline and operational discipline reinforce its growth prospects.

At its core, Enphase impresses me with balanced financial prudence, client centricity, and next-generation offerings. Renewables shift rapidly but Enphase adapts. The company has managed volatility while advancing efficiency, sustainability, and storage breakthroughs. This collective operational excellence, financial diligence, and conscientious innovation make Enphase a compelling clean energy play. I think the company has ingrained the ingredients for continued outperformance.

While some investors may think the company’s potential has already peaked, I believe there remains significant upside still yet to materialize. The implications of Enphase’s strategic initiatives cannot be overstated in their importance and promise. Now I’d like to shed light on the outlook from management to keep shareholders well-informed.

Research firms predict solar installations booming over the next decade. I am bullish on Enphase due to the surging demand and increasing global adoption we continue to see for its microinverters and solar energy solutions. In the past, managing inventory has posed challenges, but Enphase is in a better position now after reducing channel inventory by $147 million last quarter. Right-sizing supply proactively enables Enphase to control costs and maintain profitability. The company’s laser-focus on expanding its international footprint also signals to me a willingness to invest in next-generation products and enter new markets to fuel widening industry demand – a very promising development for Enphase investors.

What I find to be especially promising is Enphase’s potential to keep gaining market share. The earnings call disclosed that their recent customer satisfaction survey revealed the company garnered a world-class 77% Net Promoter Score. The ability to deliver an exceptional solar experience across installed base cuts is wonderful, since there is always the risk customers will turn to competitors. This reaffirms my rating on Enphase as I love customers who are satisfied.

Additionally, Enphase maintained strong 50% gross margins and $15.4 million in quarterly cash flow. This illustrates the company’s operational discipline even amidst turbulent markets. Safeguarding profitability and cash reserves is critical to reassure both customers and investors about Enphase’s staying power for the long haul. By keeping costs low and margins high, Enphase retains flexibility to keep investing in next-gen innovations. RBC Capital’s initiation of Enphase Energy with an ‘Outperform’ rating illustrates the company’s robust position and growth potential in the renewable energy sector. This rating from a leading financial institution reflects confidence in Enphase. In my opinion, management appears to have their finger on the pulse, which is imperative in this space.

A Recovery In Europe?

In my view, Enphase Energy’s optimistic outlook for the second quarter for Europe is a big part of my thesis. The company’s strategic maneuver through a demanding environment could create a solid rebound in Q2. CEO, Badri Kothandaraman, mentioned recovering demand levels in France and incremental progress in the Netherlands. I think this is signaling a turning tide. Moreover, there has been an introduction of new products in Italy and the U.K. (and other European countries), which shows that Enphase is committed to innovation and market expansion. Even though there has been a temporary slowdown, this strategy, to me, positions Enphase for a solid recovery. That is, in a normalized market. As we move forward, the company’s active inventory management and anticipation of channel normalization by the end of Q2 reflect a plan that is in place. They are aligning supply with the existing demand patterns, which I believe is a unique aspect of the company and my thesis.

Extension of Solar Net Metering

The Dutch Senate’s recent approval to extend solar net metering is a very big stride forward for Enphase Energy. This policy extension has now incentivized homeowners to invest in solar energy. It also is boosting the potential market adoption, which includes Enphase, for solar solutions in the Netherlands. For me, this development is a clear indicator of the growing influence that Enphase has. It is evident of the increasing global shift towards sustainable energy sources; this is something clean energy investors were excited to hear about.

For more understanding, solar net metering allows homeowners to offset their electricity bills with the energy they generate– but don’t use. Why is this attractive to potential customers? Because solar installations are financially better with this component. And as for Enphase, benefits will directly increase the demand for their products.

Furthermore, the legislative support for solar energy in the Netherlands illustrates the entire macro/global trend towards renewable energy. Who is well-positioned for success in this sector? Enphase. The question remains if this pattern will continue. Because if more countries across the globe adopt similar incentives to encourage solar energy use, Enphase is likely to see an increased adoption for the solutions they offer. This will be very good for stockholders and a thought to have in the back of your head. Ultimately, this policy extension signifies immediate opportunities for Enphase in the Netherlands and even highlights the company’s potential to capitalize on the global transition to renewable energy; this is where Enphase will prevail.

New Launch of IQ8 Micro-inverters

The recent launch of Enphase Energy’s new IQ8™ Micro-inverters is a notable event for the company; for more information, this included the IQ8HC™ and IQ8X™ models. To dive deeper, these micro-inverters are a leap forward in the industry as their peak output AC power is 384W and are compatible with solar modules up to 540W DC. I see this launch as a push to get ahead of the curve and meet the demand for higher powered solar modules.

What stands out to me is the product’s capabilities and what is means for Enphase, too. The company is broadening its market appeal to ensure they are the go-to choice for solar energy solutions across North America. As we can see, Enphase offers an industry-leading 25-year warranty in the U.S. and Canada, and a 12-year warranty in Mexico. Through this strategy, they are marketing both the quality and reliability of their products. And I then see how it translates to a stronger brand loyalty, which makes sense when rethinking about their customer surveys. Brand image is always a crucial moat, maybe even something more significant in today’s competitive landscape.

Furthermore, the integration and pairing capabilities with the micro-inverters, batteries, and energy systems illustrate an ecosystem, which I find unique to their company. Enphase is bringing appeal to homeowners and businesses that target energy independence, savings, and/or complete backup functionality.

I love a company that is forward-thinking, and Enphase has positive testimonials from solar installers about the ease of installation and value the product brings to customers, which reinforces my belief in the company’s growth trajectory. They are innovating and adapting in the fast-paced solar energy market. I see Enphase as a compelling option for growth oriented investors, too.

Risks

In my view, Enphase Energy’s restructuring efforts that aim to boost efficiency and slash costs carry risks worth mentioning. There are potential disruptions in cutting down the workforce and streamlining operations. They might seem like great financial moves, but looking deeper is needed. Even though I am a bull, I would be concerned about the impact these changes could have on research and development. I know that R&D is very crucial for a tech-forward company like Enphase as it drives innovation and keeps the company competitive among peers. Negative effects that arise in this area could hinder their progress and long-term market position.

Financially, I see potential pitfalls with the restructuring, too. This includes inventory write-offs, severance payments, and facility consolidation charges. All of this could weigh on Enphase in the near term via operational results and cash flow. I see that they are trying to build a more streamlined and competitive model, but these are risks that could strain the company, too. However, supporters of the restructuring might argue that these are necessary sacrifices for future success. Such as myself, I commend the importance of staying ahead in a competitive landscape.

As I look back in the earnings call, a risk factor is the reliance on the Inflation Reduction Act (IRA) benefits, which significantly boosts gross margins. So, any changes or challenges in this policy could affect the benefits and, therefore, Enphase’s financials. Moreover, the global expansion strategy carries execution risk. This includes new markets having different competition and regulations. I am optimistic in their expansion, but it has its potential downfalls that should be mentioned.

There’s also high interest rates, which might decrease consumer spending on solar installations. This could be for products requiring a higher upfront investment– an example being solar storage systems.

Valuations

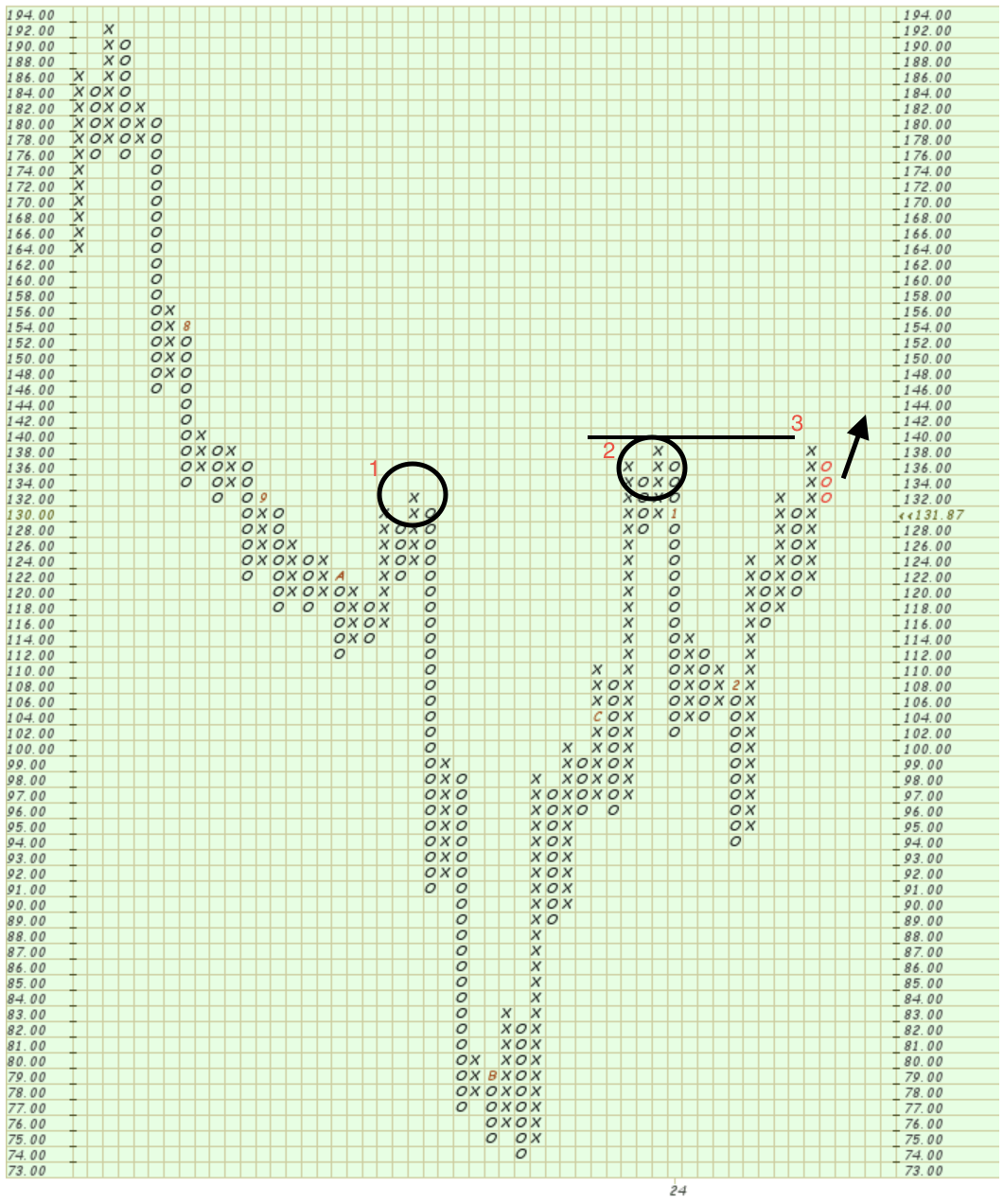

First, let’s take a glance back at Enphase’s performance. The stock is flat at -0.20% year-to-date and down +34.98% in a 1-year timeframe. When choosing a graph, I always like analyzing a point and figure chart, which I have inserted below. This is the traditional three box reversal method to understand trend lines and support and resistance levels. I have added a few circles and lines to better interpret this graph. Let’s walk through this– direct your attention to the two circles. We have had a resistance level at 132.00 and 138.00, which means the stock price has had trouble pushing through these “ceilings.” In a graphical perspective, think of these as constraining factors that are almost trying to hold the stock back. So, I am analyzing a triple top breakout, which means that I view this stock printing an X at 140.00 or higher. If we do indeed break through this resistance level (which can be seen as the black line I inserted in the graph), I could very well see the stock return to greater highs. Solely in a technical perspective, I am setting my target price at 162.00. I always seek out double or triple top breakouts. For better understanding, think of this as a potential new “section” where the stock fluctuates, that is, at higher levels.

ENPH Point & Figure (Stock Charts)

Conclusion

When reflecting on this analysis of Enphase Energy Inc., my rating stands. This company is one that each renewable energy investor should have on their watchlist. I see sustained growth for Enphase due to their financial health, inventory management, and expansion efforts. These efforts are all aimed at capturing more market share in the energy space. My belief is centric on the company’s ability to navigate risks and leverage opportunities as they arise. Graphically, I think there is a unique opportunity of short-term upside with the triple top breakout pattern that is depicted. All in all, Enphase Energy, in my eyes, is a company that illustrates innovation, resilience, and growth potential.

Comment below with your thoughts on Enphase Energy. Add questions and your insights to the conversation and I will respond promptly!

Q2 2024 Earnings Call Transcript")