Tanja Ivanova/Moment via Getty Images

Oatly (NASDAQ:OTLY) had a solid 2023 considering the difficult macro environment, with margins improving significantly and growth stabilizing towards the end of the year. The company has cut overheads and is pursuing asset-light production, which is beginning to pay off. In addition, Oatly has pulled back on investments in Asia, reducing losses substantially.

The market reaction to Q4 2023 earnings appears to have been driven by Oatly’s soft EBITDA guidance. While there is likely some conservatism baked into this, Oatly seems to be more comfortable investing in growth again given recent improvements in margins. This pushes back the timeline to breakeven, but is probably the right move given the 660 billion USD global dairy opportunity ahead of the company.

EMEA

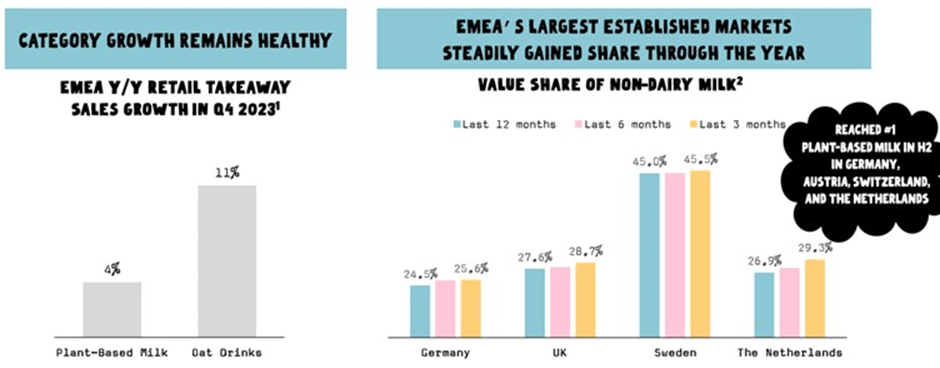

EMEA revenue growth was 11.8% YoY in the fourth quarter, with adjusted EBITDA margin moving up to 15.9%. This is a solid result given that the year ago period experienced strong volume growth as customers bought product ahead of price increases. Capacity utilization also remains in the mid-70s, suggesting further margin upside if Oatly can better leverage its fixed cost base.

Figure 1: EMEA Category Growth and Oatly Value Share (source: Oatly)

Americas

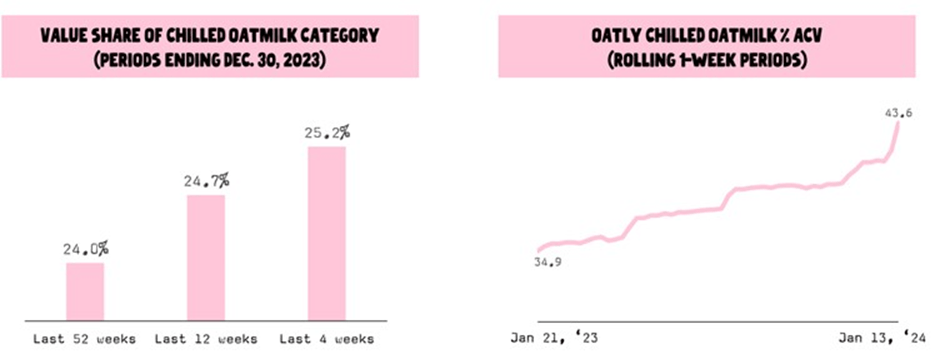

The Americas returned to modest YoY revenue growth in the fourth quarter, with adjusted EBITDA margins continuing to improve. The Americas region also reported its first-ever month of positive adjusted EBITDA during the quarter.

Figure 2: Oatly Chilled Oatmilk Retail Share (source: Oatly)

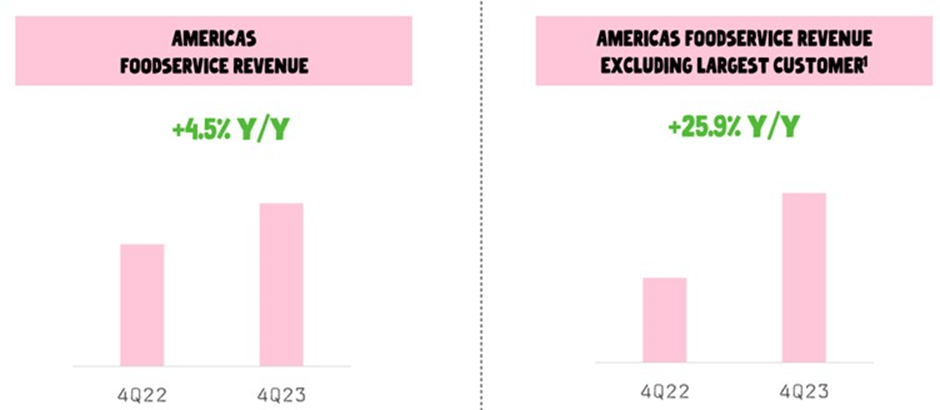

Revenue mix and cost-saving actions have both been important contributors to the improvement in profitability, and also help explain why growth has been low. Oatly is rebalancing growth between low margin food service customers and higher margin channels.

Figure 3: Diversification of Americas Revenue (source: Oatly)

Asia

Asia revenue dropped 18% YoY in the fourth quarter, driven by strategic actions designed to improve profitability. In the past two quarters, Oatly has seen adjusted EBITDA loss in Asia fall from 22 million USD to 8 million USD, with much of this coming from a reduction in production costs.

I actually think that Oatly could increase its share price in the short term by abandoning the Asia business. The company has demonstrated a willingness to invest in future growth though, and based upon 2024 guidance, appears to be doubling down on its pursuit of profitable growth.

Production Costs

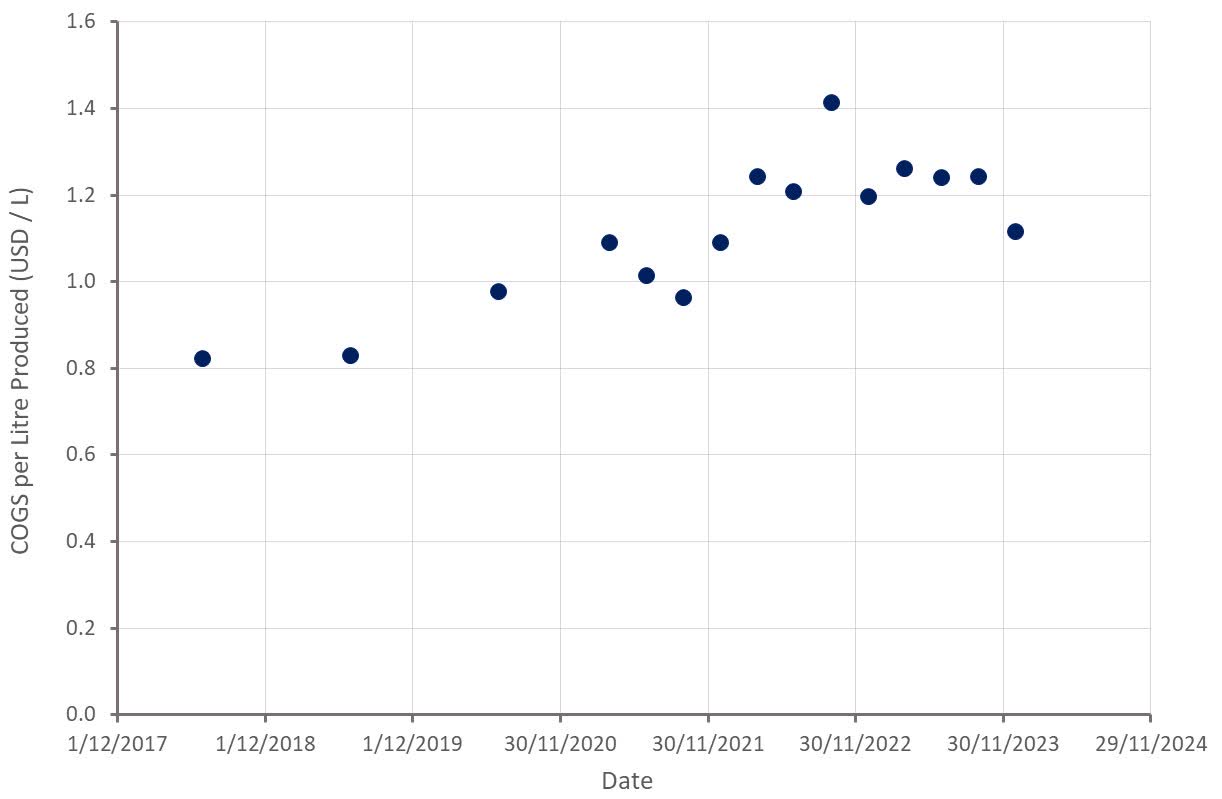

Depressed gross profit margins have caused Oatly difficulties over the past 2.5 years, but the company is now recovering. Some of this is due to higher prices, with the majority coming from lower costs.

Oat prices are down significantly from the highs of late 2021 and early 2022. Oatly has also discontinued the construction of its Americas and EMEA production facilities, choosing to pursue an asset-light production strategy.

Figure 4: Oatly COGS per Liter (source: Oatly)

COGS per liter in the Americas declined steadily in 2023 as Oatly’s third-party partnership began to pay off.

Figure 5: Americas Total COGS per Liter (source: Oatly)

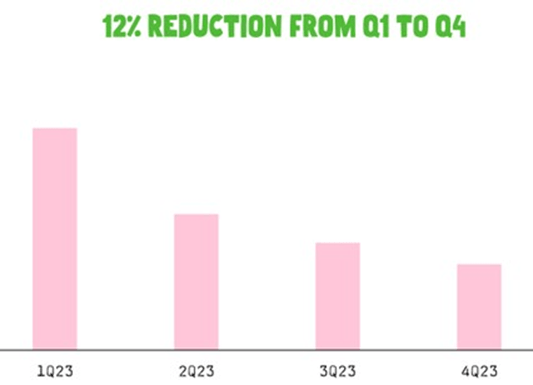

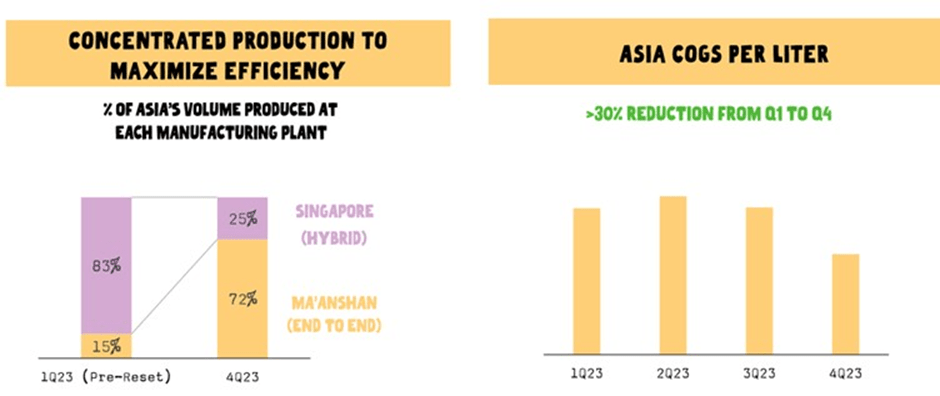

Given its poor performance in Asia (weak growth and large losses), Oatly has chosen to reduce SKUs by over 70%. While this is impacting revenue, it has allowed the company to simplify production and more efficiently operate its plants. Oatly is also shifting production to its end-to-end facility in China, which also happens to be closer to distribution points. COGS per liter in Asia is now down by over 30% since the first quarter of 2023.

Figure 6: Asia Production Cost Decline (source: Oatly)

Growth Investments

Part of the reason for Oatly’s soft adjusted EBITDA guidance appears to be a shift in focus back towards profitability. In particular, Oatly has stated that it is prioritizing brand investments. Oatly also continues to pursue product innovation and plans on introducing an improved Oatgurt with live bacteria in selected geographies. The company is also trying to drive growth with its Go Blue strategy and is introducing new varieties and pack sizes.

Financial Analysis

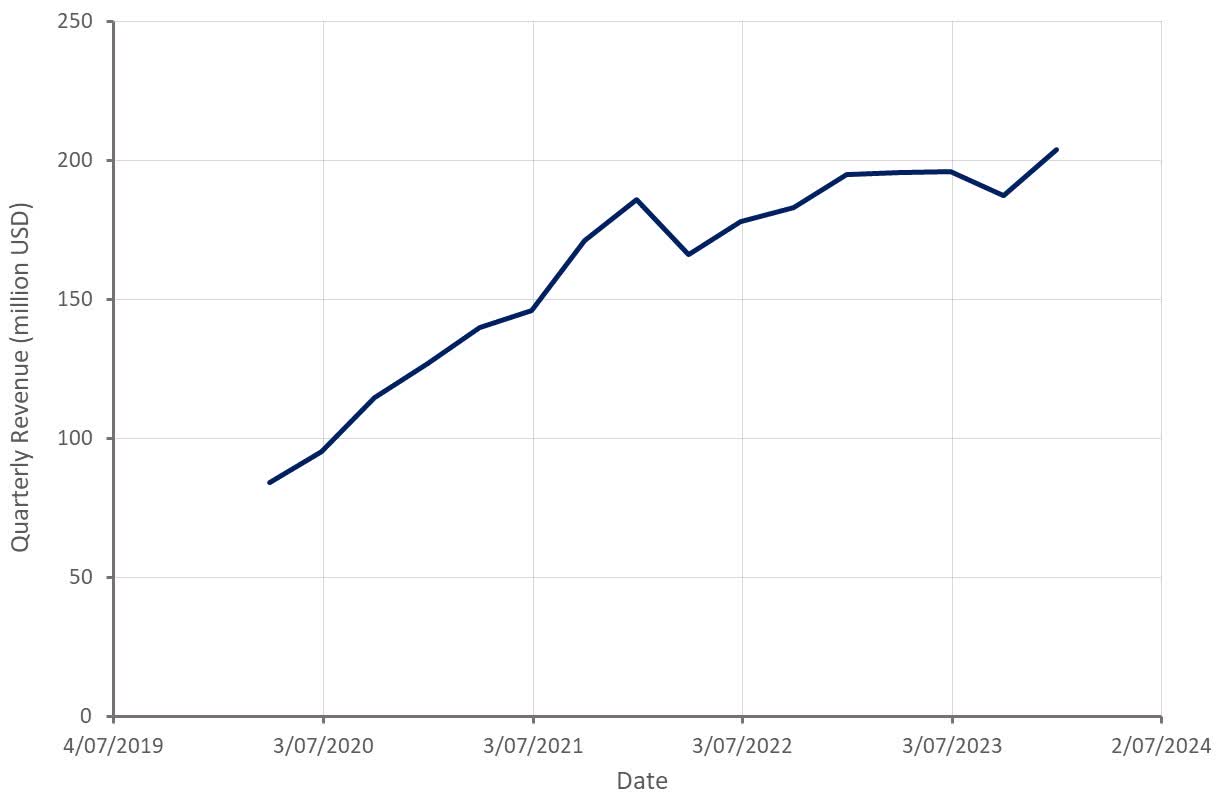

Oatly’s revenue was up around 5% YoY in the fourth quarter, even though the Asia business is currently a large drag. While the ability of Oatly to continue driving growth is a positive, it isn’t really necessary for the stock to move higher. Oatly has guided to 5-10% revenue growth in 2024, which may seem soft, but is still distorted by the company’s strategic shift in Asia and the Americas. As a result, revenue growth will likely be back in the double digits in the second half of 2024. Unlike the past few years, growth in 2024 will also need to be led by volume.

Figure 7: Oatly Revenue (source: Created by author using data from Oatly)

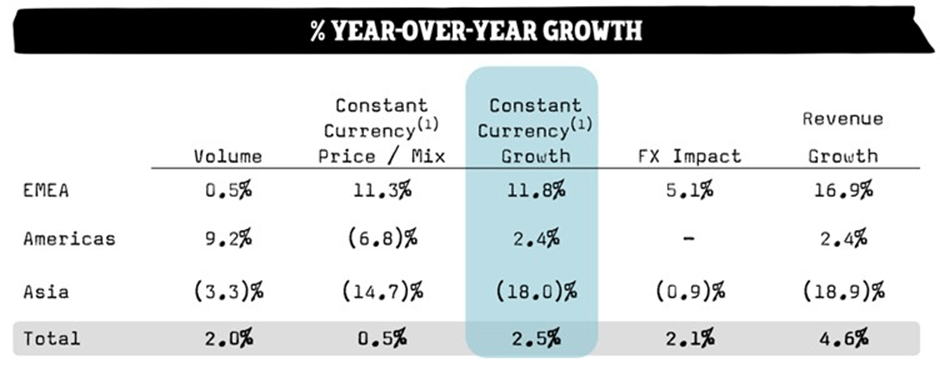

Revenue growth, and growth drivers, varied significantly across geographies in the fourth quarter. Pricing was a headwind in the Americas and Asia but supported growth in EMEA. Volume growth was solid in the Americas but declined in Asia due to Oatly’s shift in strategy.

Figure 8: Oatly Q4 2023 Segment-Level Revenue Bridge (source: Oatly)

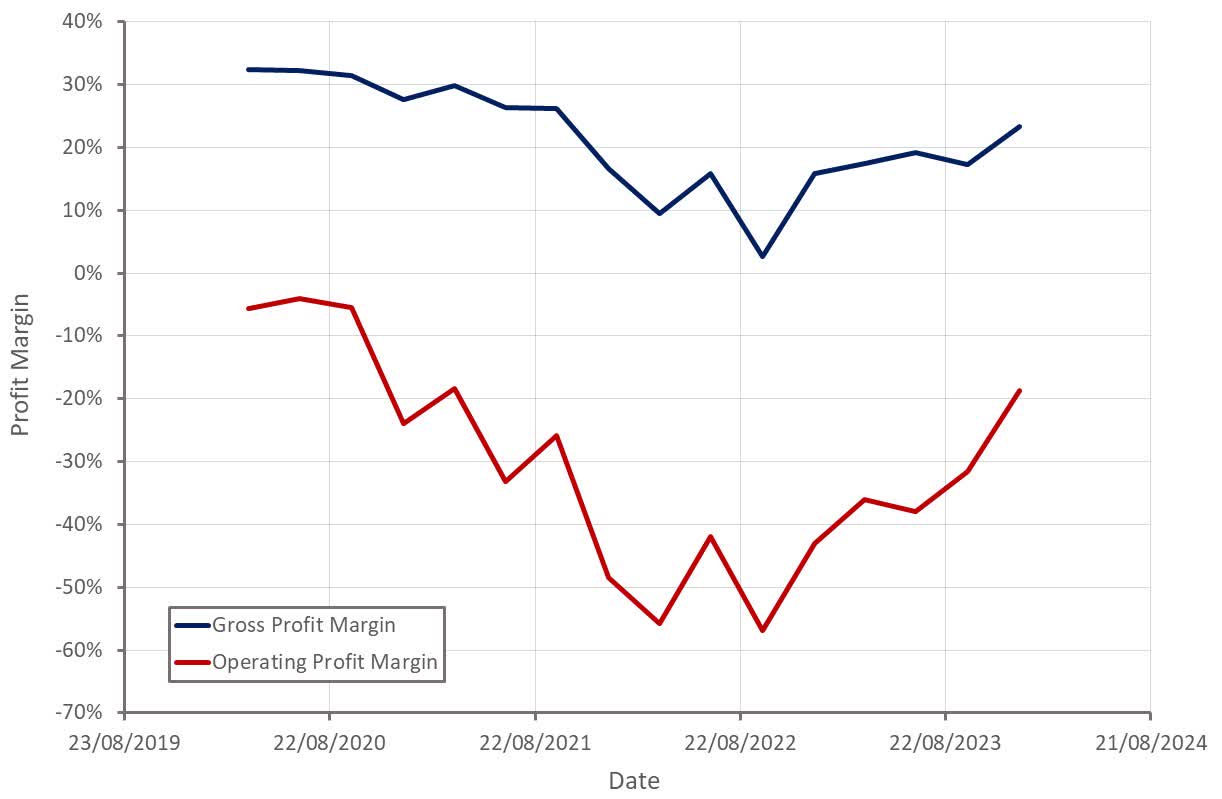

Oatly’s gross profit margin improved to 23% in the fourth quarter. Longer-term, Oatly is still targeting 35-40% gross profit margins. Operating profitability also improved significantly, mainly on the back of lower SG&A expenses. Oatly expects its adjusted EBITDA loss in 2024 to be between 35 and 60 million USD. The YoY improvement in profitability is expected to mainly come from COGS, with SG&A expected to decline between 20 and 25 million USD.

Oatly also expects capital expenditure to be below 75 million USD in 2024, meaning cash burn will still be relatively high. Oatly still has 454 million USD of available liquidity, though, which should be sufficient to see the company through to breakeven.

Figure 9: Oatly Profit Margins (source: Created by author using data from Oalty)

While Oatly’s losses in Asia have narrowed significantly, the region continues to be a significant driver of the company’s losses. EMEA and the Americas should be profitable on an adjusted EBITDA basis in 2024, but Oatly still remains some way off genuine GAAP profitability.

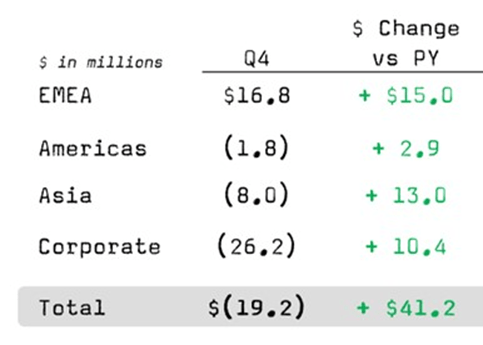

Figure 10: Oatly Segment Level Adjusted EBITDA (source: Oatly)

Conclusion

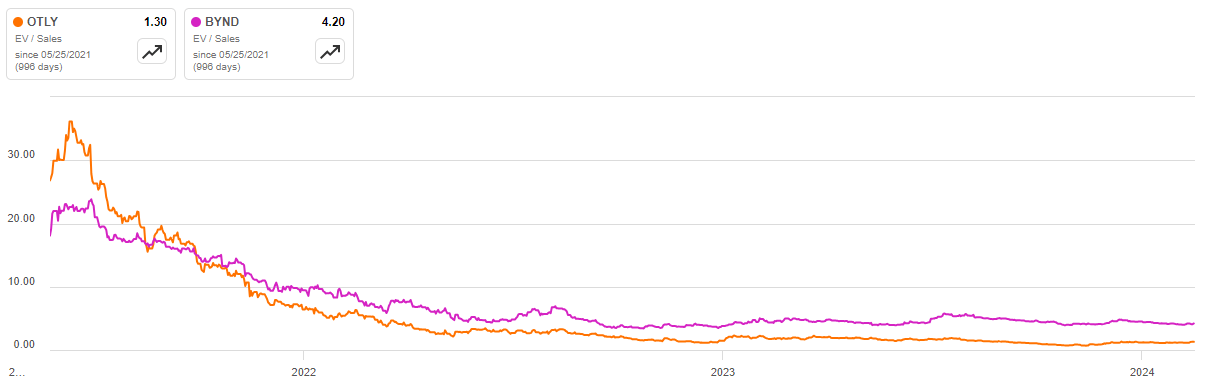

While I believe Oatly is undervalued on an absolute basis, the business has issues, and it is not difficult to envision scenarios where the stock performs poorly. I cannot understand the ongoing valuation discrepancy with Beyond Meat (BYND) though. The two companies compete in different categories but face similar demand drivers and have had similar issues in recent years.

Oatly has far better margins than Beyond Meat and continues to grow in the face of current headwinds. Despite this, Oatly trades on a far lower EV/S multiple.

Figure 11: Oatly EV/S Multiple (source: Seeking Alpha)

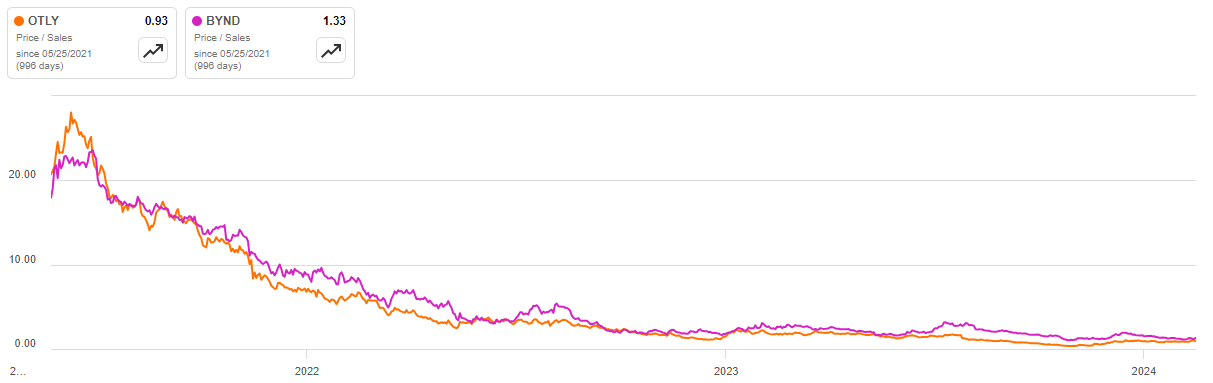

It appears that the two companies are being value-based more on P/S multiples. This doesn’t really make sense given the vast difference in capital structure for the two companies, though.

Figure 12: Oatly P/S Multiple (source: Oatly)

I think a long position in Oatly will perform ok over a multi-year period, but this involves significant risk. Oatly probably needs to progress further towards profitability before the stock rerates higher. Given management’s recent commentary, this likely won’t occur until the second half of 2024.

Q2 2024 Earnings Call Transcript")