urfinguss

Please note all $ figures in $AUD, not $USD, unless otherwise stated.

Introduction

James Hardie Industries (NYSE:JHX) is a manufacturer of fiber cement siding. After shares fell 12% following the company’s earnings, I view shares of James Hardie as attractive at today’s prices. While I don’t normally invest in companies in the Materials industry, James Hardie has a proven track record of generating high margin returns as it innovates in the fiber cement siding space and steals market share from competitors who manufacture other, inferior products. In this article, I’ll explain the company’s competitive advantages and what I believe the market is missing after its latest earnings results.

Company Overview

James Hardie Industries is a manufacturer of interior and exterior products for construction applications. The company is most commonly associated with its exterior fiber cement siding and cement backerboard products, a category that James Hardie has been an innovator in as the #1 producer of fiber cement siding. Its products are used in a wide range of building constructions including new residential, manufactured housing, repair and remodeling, and even for industrial applications. Known for their durability and longevity, James Hardie is a world leader in its product segment with nearly 5300 employees and a global reach that spans North America, Europe, Australia, New Zealand and the Philippines. Its products can be found on 10 million homes across North America.

James Hardie has a 90% market share in North America and it occupies similar market positions in the Australia and New Zealand as well. James Hardie has been around for a long time (founded in 1888) but the modern James Hardie we know today got its start in the 1980s when it patented a cellulose-reinforced fiber cement, a material that is essentially made up of cellulose fiber, Portland cement, sand, and water. In 1990 it entered into the U.S. market and more recently has expanded into international markets.

Over time, the brand has become essentially synonymous with ‘fiber cement siding’. Its not uncommon to hear builders refer to its products by name. Over time, the company has growth its market share by taking share from competitor products like vinyl, that while somewhat cheaper, isn’t nearly has long-lasting and durable as fiber cement siding. With a 23% market share today, James Hardie believes it can grow its market share to 33% in the future.

While the company’s patent has since expired in the ‘90s, it still has a moat among builders and those who are familiar with their products. They’re often reluctant to switch to competitor or alternative products given the company’s record of standing the test of time and kids and accessories that make the installation process easier for builders.

Background

I generally tend to avoid companies in the Materials sector. Like energy and commodity companies, their prices tend to be highly correlated to the economy and it’s more important to get the timing of the cycle right than pick the best companies.

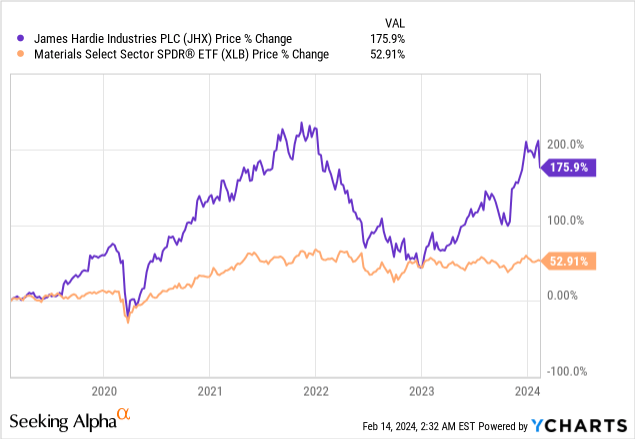

However, I believe James Hardie is different. As a company with pricing power, the ability to be profitable in a variety of markets, and benefitting from secular tailwinds and favorable market dynamics, James Hardie has been a stellar performer over the last 5 years. Compared to the Materials Sector ETF (XLB), James Hardie has returned 175.9%, compared to the ETF’s return of just 52.9%.

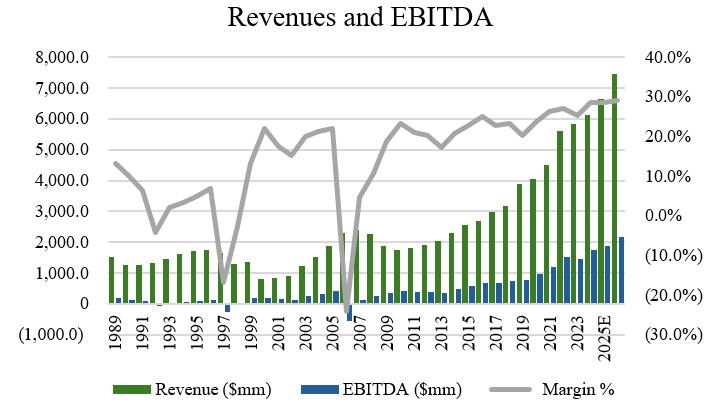

That record of strong share price outperformance shows up in the financials too. Over the last two decades, James Hardie has compounded revenues and EBITDA at CAGRs of 7.2% and 8.8%, respectively. Over the last ten years, the company has compounded revenues and EBITDA at CAGRs of 10.2% and 13.8%, respectively (source: S&P Capital IQ). With the ten-year CAGRs higher than the twenty-year CAGRs, this shows that James Hardie’s growth rate has accelerated in recent years. Moreover, with profitability growth outpacing revenue growth, this illustrates that the company has been successful in capturing efficiencies and improving margins, further solidifying its position as a market leader in the industry.

Author, based on data from S&P Capital IQ

Importantly, all of this has also been done with a relatively stable share count with minimal dilution. Twenty years ago, the company had 458.7 million shares outstanding and that number has been fairly stable over time (435.7 million, as per S&P Capital IQ) so most of this growth can be viewed on a per share basis as well. As dilution is one of the silent killers that hampers long-term shareholder returns, it’s reassuring to see management focus on creating shareholder value on a per share basis and not having the need to issue stock to fund future growth.

Recent Results

In James Hardie’s most recent quarter for Q3 2024 released on February 12, the company announced a beat on both earnings and revenue, with EPS coming in at $0.41 and revenues coming in at $978.3 million (a beat of $17.8 million). Coming off a weaker period, the growth in sales and profitability looked strong.

Compared to last year, net sales and net income were up 14% and 39%, respectively, largely driven by volume growth in North America. The reason for the disproportional increase in profitability versus sales is due to an expansion of 440 basis points in the company’s adjusted EBITDA margin which came in at 28.7%.

On a year-to-date (or nine-month) basis, the revenue and EBITDA were up 3% and 18%, respectively. Abroad internationally, the company has been seeing growth among its high-value products. Impressively, APAC and EU made up $24 million out of the year-to-date net income figure, highlighting the international growth James Hardie has in this category.

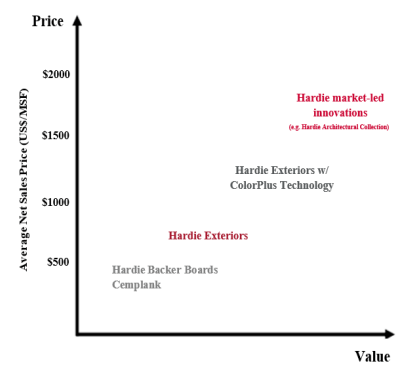

High value products are an important growth category for James Hardie. By offering value-add products, the company builds out innovations that are consistently ahead of their competition and allow the company to charge a higher price point for the product. Products like the Hardie Architectural Collection as well as their exterior products with ColorPlus technology (patented by James Hardie) are good examples of this that have been resonating with the company’s customer base.

James Hardie Price/Value Matrix (Author, based on company chart)

So why then did James Hardie’s shares tank post-earnings? I think the market got spooked by the mention of higher costs going forward into the rest of 2024 and into next year. As an example, cement prices in particular have been on a steady climb upwards, which offsets price increases for James Hardie.

Despite some higher SG&A expenses and higher capex cost into next year (capex estimated at $515 million), we should keep in mind that margins are expected to remain at 32% (currently 32.7%) and that James Hardie is still expecting to do between 750 million and 780 million standard feet of North American volume for 2024.

Another way of looking at this (and perhaps is the market and consensus view) is to say that James Hardie doesn’t expect any margin expansion from here. With EBIT margin expansion across all geographies (North America alone had margin expansion of almost 400 basis points over the last year), we shouldn’t get excited about profitability growth next year if volume growth is expected to be flat.

Outlook

As for my forward-looking expectations and outlook for next quarter and into 2025, I expect that Q4 should be stronger than Q3. Seasonally, Q4 is a stronger quarter that’s on average 4% higher than Q3 (source: S&P Capital IQ). With pricing increases having begun for Jan 1, that 4% growth figure should look more like 10% in my estimation. So with an increase in pricing greater than the expense increase of this year, we may even see a slight margin improvement (although this is not my base case, given management’s comments).

Those price increases are being rolled out in several geographies and James Hardie has generally been much slower to increase prices compared to competition, so I don’t expect customers to switch suppliers. Helping to build this brand loyalty is the company’s Contractor Alliance Program, which gives contractors lead generation support and training that is simply unmatched by James Hardie’s peers. So even though James Hardie’s pricing is competitive, I think they have an opportunity to increase it long-term as a premium product in the market place with many of its value-add services and features. To me, James Hardie isn’t just a siding company, it’s really building a brand.

Longer-term, I think there’s still many reasons to be bullish on James Hardie.

In a recent report, the American Housing Survey conducted by the US Census Bureau estimated that there are over 44 million homes over 40 years old, meaning that old siding will need to be replaced and repaired over the next decade, which should act as a long-term tailwind for James Hardie.

Despite some indications that consumer debt is rising, home values have also increased meaning that this should result in tappable home equity for consumers. As for the macroeconomic outlook, James Hardie’s success is somewhat tied to new housing construction and repair and remodeling activity. The Leading Indicator of Remodeling Activity, a metric published by the Joint Center for Housing Studies at Harvard University, predicts that the downturn we’ve witnessed in repair and remodeling activity should bottom out sometime later this year. So with relatively flattish growth expected for James Hardie, demand could increase pretty sharply in 2025 if we are to resume to more normal levels of construction and renovation activity.

Finally, in a survey conducted by James Hardie, 76% of homeowners said their renovations plans were impacted by the possibility of extreme weather events. For homeowners in coastal regions where extreme weather is more common, siding is the often first line of defense that protects a home from the elements. The same survey also found that 70% of homeowners felt that their home exterior needed a facelift, which indicates that demand is also strong in regions where extreme weather is not an issue. I believe this is also an indication that James Hardie’s investments into ColorPlus Technology and its unique designs to bring in customers should be a recipe for continued demand into 2025.

Valuation

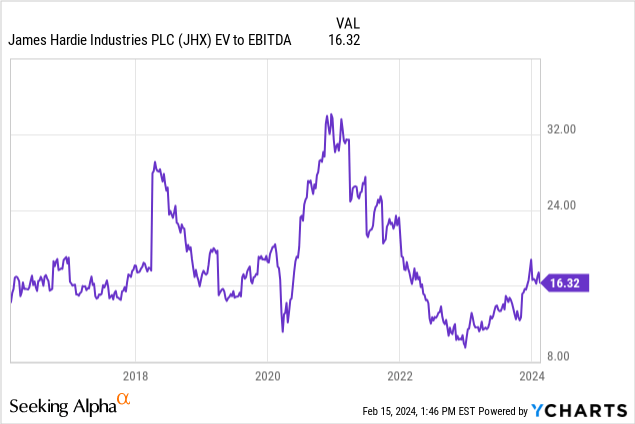

When looking at the valuation for James Hardie, the company trades at 16.3x EBITDA, which seems like a fair multiple based on the fact that we are below the historical average multiple over the last 10 years. At the 10-year average multiple of 19.0x EBITDA, which I feel would be a reasonable one-year target based on the fact that we should approach mid-cycle soon, this would imply upside of 17%. During the pandemic, shares became fairly stretched but I think the recent year or so has provided investors an opportunity to buy shares at a reasonable valuation. At 16.3x EBITDA, the multiple seems reasonable for this business, given that it can grow in the mid-teens (based on historical performance).

Compared to its closest peer, Louisiana-Pacific (LPX) which trades at 11.6x EV/EBITDA, James Hardie might look expensive at 16.3x at first glance. But in my view, the premium valuation is justified given the fact that James Hardie is stealing market share away from Louisiana-Pacific and the fact that its products also tend to be much more cyclical than James Hardie. For those reasons, I’m comfortable paying a higher multiple, especially given the fact that James Hardie has proven it can grow revenues and EBITDA over the long-term compared to LPX (source: S&P Capital IQ).

As for the risks to the investment thesis, the main one would be the impact of rising rates. So far, interest rate rises haven’t materially dampen consumer sentiment or put us into a recession. That said, it’s also made the cost of home-ownership more unaffordable. For homeowners faced with the decision to remodel and renovate their homes or continue to pay rising mortgage payments, the decision to invest more into their homes doesn’t seem feasible.

There’s also the risk of consumers moving to increasingly urban areas, either apartments or multifamily units, which could limit demand for James Hardie’s products. While the trend lately has been to move outside cities for much of the U.S. into single-family homes, a reversion of this trend would be negative for demand of fiber cement siding.

Conclusion

Despite a recent dip in share prices following James Hardie Industries’ earnings report, I believe the company presents an attractive opportunity for long-term investors. With a dominant market position in North America and a strong international presence, James Hardie has demonstrated its ability to innovate in the fiber cement siding space and maintain good margins. While I don’t expect much margin expansion near-term, I don’t believe the market’s reaction is reflective of the company’s results this quarter. Even if higher costs pose short-term challenges, I think this will be offset by the company’s pricing increases. Historically, James Hardie has had a track record of steady revenue and EBITDA growth, coupled with a focus on value-added products and long-term market tailwinds. So I think its future prospects look promising. At 16.3x EBITDA, I think shares are a good buy today.

Q2 2024 Earnings Call Transcript")