Bloomberg/Bloomberg via Getty Images DBS logo (DBS Group)

Investment Thesis

We titled our previous article on DBS Group (OTCPK:DBSDF) (OTCPK:DBSDY) “A Good Place To Be Invested For Dividend Safety”, as that was our conclusion at the time.

South East Asia’s largest bank, DBS has exceeded our expectations in terms of being shareholder-friendly. Since we bought in, which was in March of 2020, the bank has increased its dividend five times. An increase from Singapore cents 18 to 54 cents. That is 200% higher. At the end of 2022, they also gave a special dividend of 50 cents.

The three large home-grown banks here in Singapore, which apart from DBS are OCBC (OTCPK:OVCHF) and UOB (OTCPK:UOVEF) have all announced their Q4 2023 results.

We will, as usual, share our thoughts on DBS’s performance and prospects

Q4 and FY 2023 Financial Results

It sounds like a broken record player when we keep stating that DBS had another record year. But they did.

It was not only a record year, in terms of FY earnings, which was a net profit of S$10.3 billion, but it was also a record in terms of its ROE which hit 18%. Year-on-year, that was an improvement of 22% for the net profit and 20% higher ROE.

EPS, on a TTM basis, was S$3.87

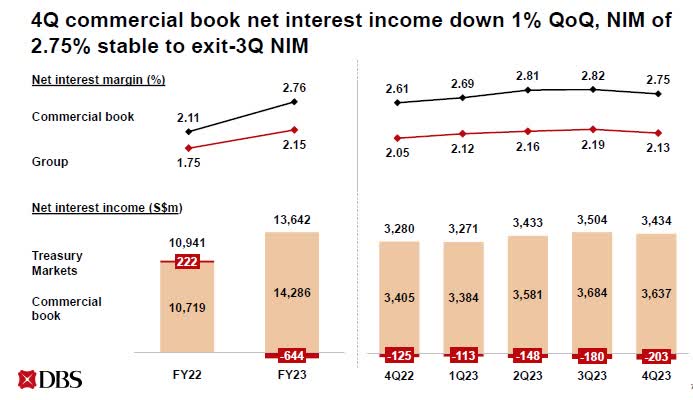

However, when we compare the numbers on a Quarter-on-Quarter basis, we see that the important NIM might have peaked in Q3 at 2.19% on the group level, falling slightly to 2.13% in Q4. The NIM for their commercial book is 62 basis points higher

DBS Group Net Interest Income (DBS Group)

It is important to keep things in context. NIM above 2% is quite high on a historical basis.

If we go back to 2020, when we became shareholders, the NIM was 1.62%. Before 2020 it had been hovering around 1.7 to 1.9%.

Sometimes, banks can increase the volume to offset a lower NIM, however this did not happen for DBS in the last quarter. Their net interest income came down from S$3.684 billion to S$3.637 billion. It is not a big difference, but we do think this trend of lower NIM, and potentially lower income, will continue going forward.

Higher fees and commission income in Q4 offset the lower interest income somewhat. It increased from S$843 million to S$867 million. When we look at this income on a Y-o-Y basis, we see that it has increased from S$2.697 billion in FY 2022 to S$4,124 billion last year.

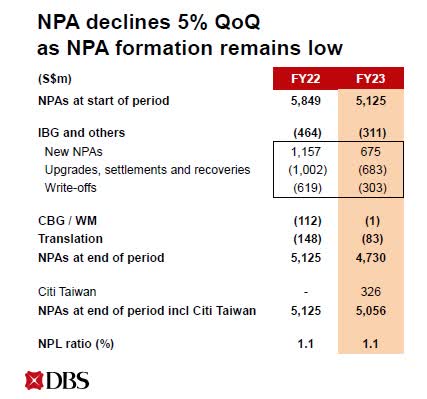

Non-performing assets came down by 5% from S$5.125 billion to S$4.730 billion.

Non-Performing Assets (DBS Group)

CET-1 ratio has been stable at 14.6% Y-o-Y

Finally, we want to circle back to the issue of shareholder friendliness. Apart from the growing dividend, the bank has decided to give 1 bonus share for each 10 shares.

The bank is not only taking good care of its shareholders, they are also taking care of its Corporate Social Responsibility. The bank has committed S$1 billion over ten years with S$ 100 million each year which will go towards vulnerable segments of the society. We support that.

The Share Price

DBSDY’s share price against peers (SA)

When we look at the share prices over one year, we can see that they are slightly lower for UOB and OCHBC.

HSBC (HSBC) is the only one that is up. DBS is down 10%.

Valuation

Let us start with the Price to Net Asset Value. Its book value is S$ 23.14 and as of 16th February, the price in Singapore for one share is S$ 33.76, giving us a ratio of 1.46

That is not cheap. When we compare it to its peers here in Singapore, we see that OCBC is trading at a P/NAV of 1.17 and UOB is trading at a P/NAV of 1.16

DBS’s P/E is quite attractive, and more important than the P/NAV in our opinion. That ratio is 8.7

In terms of dividend yields, based on TTM and excluding any special dividends, DBS beats its peers. Their yield is 5.69%, OCBC is 5.14% and the lowest is UOB at 4.63%.

Economic Landscape

The two main markets for DBS are Singapore and Hong Kong. FY 2023 net profit from Hong Kong was S$ 1.578 billion. That constitutes 15.7% of the group’s net profit.

Macroeconomic data from Singapore and Hong Kong has just been released.

Singapore’s Ministry of Trade and Industry announced that the Singapore economy expanded by 1.1% last year. They have a GDP growth forecast of 1.0 to 3.0% for 2024. Manufacturing output dropped by 4.3% last year but did register a strong growth of 4.5% in the last quarter.

Construction is also strong, on the back of government-led infrastructure projects.

Inflation in 2023 came in at 4.8%, down from 6.1% Y-o-Y.

The official unemployment rate for 2023 for Singaporeans and Permanent Residents was 2.7%, down from 2.9% Y-o-Y. In the past, we have commented that our personal view is that the real unemployment number could be higher, as Singapore does not have unemployment benefits, such as seen in Europe. As such, we believe there is little to gain for a person who has lost his/her job by registering as unemployed. Retrenchment more than doubled last year. It was especially in the technology sector that we saw retrenchments.

Things are somewhat different for Hong Kong’s economy. We need to bear in mind that they came off from a weak economy later and slower from the pandemic than that of Singapore.

For 2023, Hong Kong’s real GDP grew by 3.2%, following a contraction of 3.7% in 2022. The GDP growth forecast for 2024 will be released on 28 February 2024.

Unemployment, in Hong Kong is very similar to that of Singapore. As of the end of December, it stood at 2.9%

There is no alarming data from Singapore and Hong Kong which could point towards higher delinquencies on loans. Real estate prices are elevated, but DBS and other local banks are conservative in terms of loan to valuations.

We see no concern from this to come.

Risks And Conclusion

The only risk we can think of is just lower income.

A lower interest rate environment will reduce the bank’s ability to maintain its NIM. With lower interest income, it is going to be harder to compensate for this by increasing fees and commission income enough to cover this going forward.

At least, theoretically, DBS could continue to grow through a larger pool of customers. Their recent expansion in India and Taiwan should see slightly higher earnings going forward, despite a lower net interest income. However, this depends on how well they can execute in these new markets. That remains to be seen.

Returning to valuation, as we know, the “price is what we pay and the value is what we get.”

DBS is priced at a fair price. We are confident that it will continue to deliver a solid stream of earnings in the future. They have proven that they are also treating all shareholders well.

However, we are not adding to our position at this moment. Perhaps we are suffering from anchoring bias, bearing in mind that our average price is considerably lower.

If we have to put a stance on DBS, it would be a Hold.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")