StudioEasy

Overview

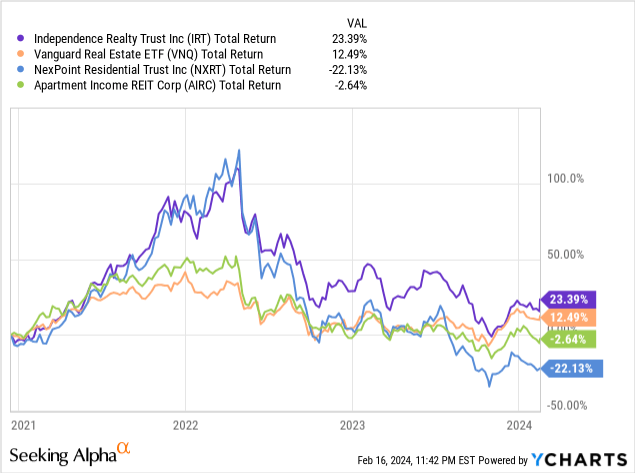

As an investor that values dividend income, REITs hold a valuable part of my portfolio as they can provide unique exposure to the real estate sector and usually have yields larger than traditional stocks. In the case of Independence Realty (NYSE:IRT), the dividend yield doesn’t quite meet my needs at 4.5% but the total return has outperformed in comparison to the Vanguard Real Estate ETF (VNQ) and competitors such as NexPoint Residential (NXRT) or Apartment Income REIT Corp (AIRC). Therefore, I decided to take a look into the REIT to determine if it belongs a spot in my portfolio after this most recent earnings report.

Independence Realty is a real estate investment trust specializing in multifamily communities situated in non-gateway U.S. markets. “Non-gateway U.S. markets” refers to secondary cities and regions in the United States that are not considered primary gateways for international trade or business activity. Gateway cities typically have major international airports, significant global financial centers, and serve as major hubs for commerce and cultural exchange. The company aims to deliver compelling risk-adjusted returns to shareholders by employing rigorous portfolio management practices, achieving robust operational performance, and consistently generating value through distributions and capital appreciation.

Earnings Recap

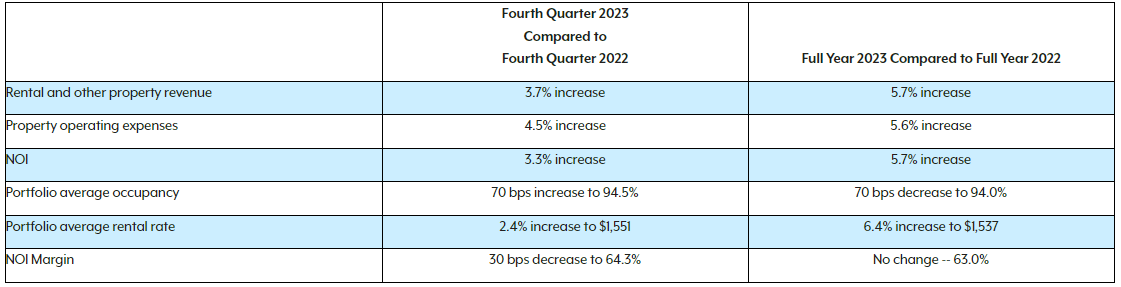

The recently reported Q4 earnings showed us a mixed financial performance in my opinion. This is because the net loss amounted to $40.5 million which is a decrease of approximately 220% from the $33.6 million net income available to common shares reported for the same quarter in 2022. At the same time, we see increased levels of revenue, NOI (net operating income), and portfolio occupancy. This drop in net income can mostly be attributed to a previously discussed asset impairments, debt reduction, and portfolio adjustments such as nit renovations. So as a result, I don’t think there’s necessarily anything here to worry about as it seems to be a one-time thing.

IRT Q4 Press Release

Despite the downturn in net income, the portfolio demonstrated some areas of growth with an increase in net operating income of 3.3%. CFFO (Core Funds from Operations) saw a modest uptick, totaling $68.7 million in the fourth quarter of 2023 as well which is slightly higher than the $66.8 million reported for the same period in the prior year. The average occupancy also saw an increase to 94.5%.

Management seems to be very confident on the outlook of IRT as they believe they are positioned to thrive in all market cycles. As stated by the CEO:

I just want to reiterate my confidence in IRT’s business model and strategy, which was constructed to succeed during all market cycles. Despite near-term market conditions, we expect to deliver growth in 2024, driven by a combination of occupancy gains and rental rate growth. Overall, we are optimistic as we have the right assets in the right markets that continue to perform well, supported by strong employment growth and population migration. – Scott Schaeffer – Chairman, President & CEO

On a positive note, Adjusted EBITDA increased to $95.6 million in the fourth quarter of 2023. Additionally, the value-add program achieved significant milestones, completing renovations for 486 units during the fourth quarter of 2023 and attaining an impressive weighted average return on investment of 17.1% during the period. While these highlight some short comings, it also highlights measurable growth in some areas. For example, as part of the latest earnings call, management discussed some portfolio updates that I see as improving fundamentals and an active effort to reduce debt.

Portfolio Improvements

During the earnings call, management stated they are implementing a portfolio optimization and debt reduction strategy that involves selling 10 properties across seven markets to exit or reduce presence in those areas and decrease debt. While their debt levels are currently a bit high, I think this is a smart move towards aligning with better financials. Four properties were sold as recently as December 2023 which generated about $200 million in gross sales.

Those proceeds used to repay $196 million worth of debt. Six properties still remain part of this strategy, with two sold after December 31, 2023, and the remaining four expected to close in Q1 2024. Once all 10 properties are sold, a reduction in outstanding debt by approximately $519 million is anticipated, alongside a decrease in net debt to Adjusted EBITDA ratio and exiting of five markets. This would help create a larger cash cushion which in turn can also lead to a well-needed dividend raise.

In addition, they implemented a “Value Add Program” in order to boost the rents they can charge tenants so that profitability can rise. This initiative resulted in renovations on 486 units in Q4 which achieved a return on investment of 17.1%. The average cost per renovated unit was $18,264 and this was offset by an average monthly rent increase of $260. Expansion of this program is planned, with renovations at new communities slated to commence in the first half of 2024. This is a great move and can increase the reputation, quality, and demand for IRT properties.

Dividend & Valuation

As of the latest declared quarterly dividend of $0.16/share, the current dividend yield is about 4%. While the yield is on the lower end of the spectrum for REITs, at least the dividend payout is well-covered. For reference, the dividend payout ratio is conservative at 57%. With such a relatively low payout ratio for a REIT, I am thrown off by the lack of dividend growth here.

In fact, the dividend was reduced in Q2 of 2020 in order to preserve capital during the uncertainty around Covid. I think the cut was completely understandable given the craziness around the time with the pandemic. However, it is disappointing that the dividend has not returned to the same level prior to the pandemic. I interpret this as management remaining on the safe side to prevent the stretching of capital, however the AFFO & free cash flow growth supports further increases.

In terms of valuation, the average price target is $17.50/share which represents a potential upside of 12.5%. FFO growth supports this valuation as the YoY growth has been 6.5% and the average revenue growth over the last 5 year period has been 28%. However, we get a mixed picture here are the price to FFO ratio is currently 13.5 which sits above the sector median of 12.5. While FFO over the sector median doesn’t necessarily mean that IRT is overvalued, it does give us a good reference point.

IRT’s FFO does seem to be trending in the right direction though. Over the last 5-year period, the FFO as grown at a CAGR (compound annual growth rate) of 9.22%. On a small time period of only 3 years, the FFO has grown at a more impressive 12.86% CAGR. Free cash flow per share has grown tremendously and outpaces the sector median FCF by a wide margin. The free cash flow per share has grown at a 17.71% rate.

For reference, the current P/AFFO ratio is 14.66. If we dividend this by the current price of $15.56/share we get a FFO of 1.06 for the year. Management has reported their projected FFO for the full year is between 1.16 – 1.20. This means that they expect FFO to grow my at least 10% over the next year.

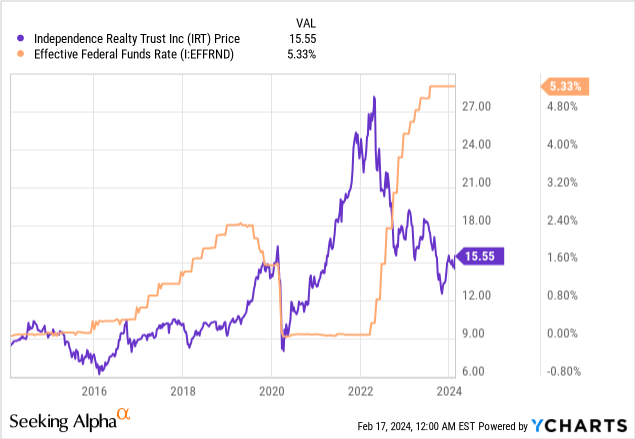

As rates come down, I believe the REIT sector as a whole will see some nice price upside. As you can see, the price of IRT was drastically affected by the rapidly rising rates. We can see the same pattern play out over time and the dramatic effect of 2020.

The Fed previously said they anticipated several rate cuts. However, after the last meeting the tone has changed a bit. The consensus is that the Fed seems to be awaiting to see how inflation plays out before interest rate cuts can take place. This takes me to the risks next as interest rate sensitivity can play out on the downside as well.

Risk Profile

If interest rates do not get cut as originally anticipated, we are likely to see the share price remain sideways, alongside the rest of the REIT sector. The main risk here is underperformance. Normally this would be okay if we were talking about a REIT with a 7% yield for example. In this case it would be a lot easier to wait out the cycle and collect a fat yield in the meantime. However, this 4.5% yield that management has held off on raising, doesn’t make up for the potential side ways movement.

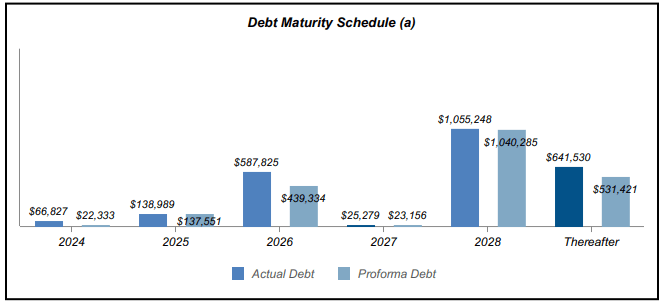

(numbers represented in thousands) (IRT Investor Presentation)

In addition, management has been making active strides to reduce debt levels but if the value add program or sales of properties don’t align with expectations, we can see a delay in this debt reduction effort. Thankfully, IRT does not have a significant amount of debt due until 2028. However, it’s worth mentioning that this REIT’s market cap is only $3B and they have $1B in debt due in 2028. In addition, proforma debt refers to a projected or estimated amount of debt that a company will have after a particular event, such as an acquisition, merger, or restructuring. IRT’s debt primarily consist of 97% fixed rate loans.

Takeaway

While Independence Realty Trust (IRT) presents a interesting opportunity because of its outperformance relative to peers and initiatives for portfolio optimization and debt reduction. However, caution is warranted due to uncertainties surrounding interest rate movements and debt management.

Although the recent earnings report highlighted mixed financial performance, operational improvements and proactive measures by management underscore a commitment to enhancing long-term shareholder value. However, the slightly lower dividend yield and lack of dividend growth doesn’t make this a compelling hold for the long term. I do think we can benefit by initiating a position here on the recovery play but I would not hold for a longer period of time unless the dividend payout reached above pre-pandemic levels again.

Q2 2024 Earnings Call Transcript")