Bloomberg/Bloomberg via Getty Images

The Korea fund overview

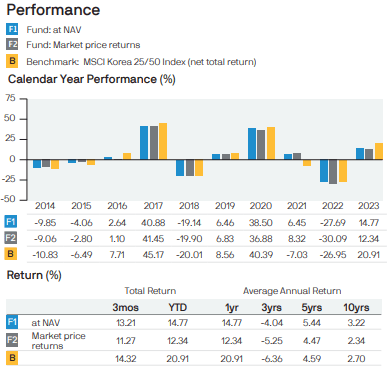

The Korea Fund (NYSE:KF) is a closed-ended fund that is focused on South Korean equities. Its performance in NAV terms over the last decade has slightly beat its benchmark.

From that perspective, I would normally consider the expense ratio of nearly 1.5% too high. The Korea Fund discount to NAV has averaged more than 17% in the last 6 months though, offering enough appeal to go with this active manager. There is scope for the discount to contract substantially in the event of a bullish run in South Korean stocks. Aside from that, a discount of this magnitude continuing throughout 2024 may lead to more pressure from activists.

How did South Korean stocks perform in 2023?

Heading into 2023, I was bullish on the Korea Fund when I last covered this fund here. Whilst it has shown modest positive returns since, I would describe this as a little disappointing. One reason I was optimistic back then was the potential for an increase in shareholder activism and improvement in corporate governance. Despite the lackluster performance of the Korea Fund in this time, I believe these are still potential catalysts for 2024.

As it turned out, the theme of increasing shareholder activism and improving corporate governance was a major talking point in a different market. Now it is Japanese stocks that are rising to 34-year highs as a corporate governance revolution begins to take effect.

During this time, I have observed South Korea watching this theme, and they appear to be taking a leaf out of Japan’s book. This has led me to again examine if the Korea Fund is still a buy, perhaps even a better buy now.

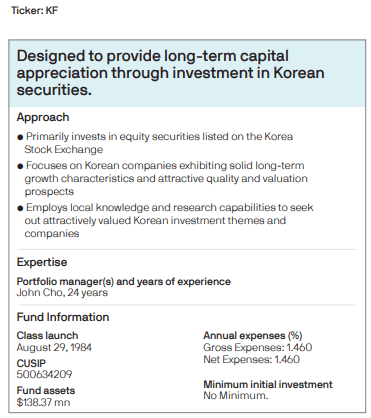

Korea fund facts

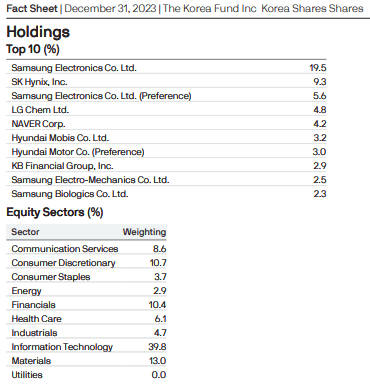

Korea fund factsheet December 31, 2023

Korea fund past performance

Korea fund factsheet December 31, 2023

Korea fund distribution history and capital management

There have been some large distribution payments in recent years, however the Korea Fund is not one for those looking for steady income. This was more to do with the South Korean market being extremely volatile around 2020 to 2022. Stocks bought amidst the “covid crash” early in 2020 delivered enormous returns if sold a year later.

There is a buyback policy in place to address the large discount to NAV. Do not expect much action on this though given it reduces the fund size. To quote from the Korea Fund 2023 annual report, “Whilst your board monitors the Fund’s total expense ratio closely, reducing assets under management are pressuring the total expense ratio which, at June 30, 2023 was 1.46%.”

South Korea economic outlook 2024

Weighing on South Korean shares last year was falling exports, in particular relating to the disappointing performance of the Chinese economy. Last month the Ministry of Economy and Finance were lowering their 2024 GDP forecast to 2.2%. Previously back in last July they were forecasting 2.4% GDP for 2024.

Like elsewhere across the globe, South Korea may pivot to rate cuts later this year, but is weighing this up against somewhat sticky inflation pressures.

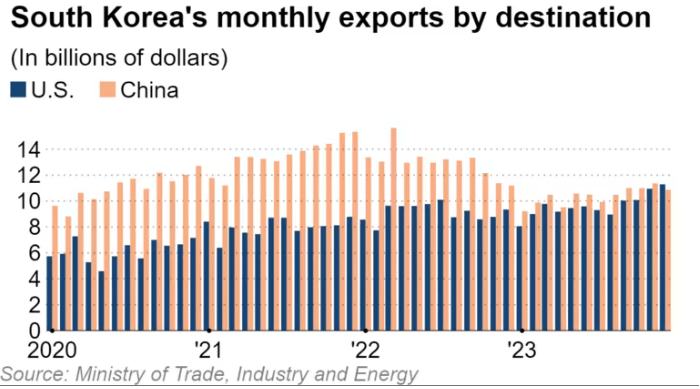

Potential rate cuts will be an important area to watch in 2024 for the prospects of South Korean stocks, as too will be China’s economy. Last year South Korea recorded its first trade deficit with China in 31 years.

The bright side to South Korea’s declining exports

The below chart shows a major change in recent years to South Korea’s export destinations.

Ministry of Trade, Industry and Energy

The outlook for China is still certainly worrying for 2024. I would caution however in letting this make you bearish on South Korean stocks. Stock markets after all are a discounting mechanism. It may only need investors to become less worried about China than they already are, in order to help the South Korean market rally.

In that context, the latest Bank of America fund manager survey shows just how pessimistic investors are on China already. The “long Magnificent Seven” trade was judged as the most crowded trade since October 2022, and the second most crowded trade was short Chinese equities.

There is also a bright size to the South Korean exports’ destination chart above. To quote directly from the Nikkei Asia article linked to earlier, “Growing exports to the U.S. are also in sync with the diplomacy of President Yoon Suk Yeol that favors close ties with Washington. Responding to that political stance, major conglomerates such as Samsung, Hyundai Motor, LG, SK, and Lotte have been increasing their investments in the U.S.”

There are also tentative signs of South Korea exports growth seen late in 2023, citing demand for emerging technologies.

Are South Korean stocks undervalued in 2024?

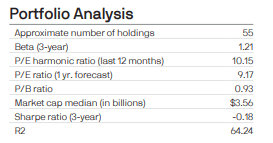

The Korea Fund portfolio trades at a mere 9 times forward P/E ratio according to their December 31 factsheet. The price to book ratio is still below 1. These measures appear very cheap, as they do versus peers such as Japan and Taiwan.

What strikes me from the chart below is the expansion in the price to book ratio in Japan and Taiwan through 2023, whereas this ratio was little changed in South Korea.

Bloomberg

Readers might now be thinking about the “value trap” or the perennial “Korea discount” as reasons to still stay clear of the Korea Fund.

I acknowledged earlier how the “corporate governance revolution” in Japan caught many investors by surprise last year.

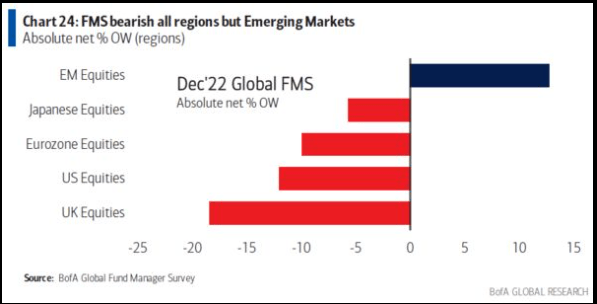

No doubt prior to 2023, many fund managers cited the usual “Japan discount”, as a reason to stay clear of Japanese stocks. Perhaps they pointed to demographic issues and weak corporate governance. Below is a snippet from the Bank of America Fund manager survey from December 2022.

B of A global research dec 2022

We all know how that turned out now, as Japanese stocks happened to chalk up some of 2023’s best asset class returns.

Corporate governance improvements, South Korea to follow in Japan’s footsteps

If South Korea is therefore keeping a close eye on Japan’s corporate governance reforms last year, perhaps we shall see a similar strong performance here.

Last month we saw South Korea taking a cue from Japan’s corporate reforms. It was getting plenty of news coverage as they attempt to end the “Korea discount”, with the announcement of their Value Up Program.

South Korea is keen to improve corporate governance and shareholder returns. This will assist it in transitioning from emerging to developed market status. It appears they are now taking these issues seriously, with potential tax reform to encourage companies highlighting their true higher worth. There was also a ban on short selling in South Korea last year.

Expect higher dividends, improved incentives and structures for foreign investors, and better protection measures for minority shareholders in the future.

Activist campaigns have already been surging in South Korea over the last couple of years, and this development is likely to ensure this trend continues. Given all these recent developments, the South Korean stock market seems to be slow in digesting these potential positive catalysts. Performance has been fairly flat thus far in 2024.

Korea fund risks, are Samsung shares a good buy for 2024?

The main risks I see to the Korea Fund I touched one earlier. The outlook for global growth is worrying, particularly surrounding China’s contribution. As a very export dependent economy, South Korean stocks are still very vulnerable to this risk. This is despite their low valuations to begin with.

The other risk is the concentrated nature of investing in the South Korea stock market, where typically the funds there will have a huge weight to Samsung. Top-down market analysis therefore deserves some commentary purely about this stock.

The potential reward though is worth taking on such risk. Samsung is quite symbolic of the whole market being able to positively re-rate on the back of corporate governance reform. The company is already under pressure, as activist shareholders target Samsung to unlock value. Three activist shareholders already submitted proposals just a few weeks ago.

One local hedge fund made an interesting remark in the above-mentioned article, “Every time share prices rise in Japan while remaining flat in Korea, it strengthens the arguments of local advocates for reform,” said Lee.”

The Korea Fund at the end of last year had a 20% weight in Samsung.

Why invest in South Korea via this Korea Fund?

I acknowledge that the Korea Fund’s track record over the last decade does not show a huge amount of alpha. They have beaten their benchmark on an NAV return basis though longer term.

I believe it stands up as a better alternative to similar funds and ETFs for a variety of reasons:

- Generally, emerging markets like South Korea offer active management a better chance of delivering alpha than more efficient developed markets.

- In 2024 the likely reforms in corporate governance in South Korea may favor certain companies over others. This gives extra opportunities to skillful stock pickers that we have not seen historically.

- If I am wrong on the above points, any underperformance may bring about an attractive tender offer anyway, which I shall discuss further down.

- The Korea fund is currently available at a very large discount of 17% to NAV, an opportunity that does not exist with ETFs. Activists may look to try and close this discount.

Korea Fund portfolio details

Korea fund factsheet December 31, 2023

Korea fund factsheet December 31, 2023

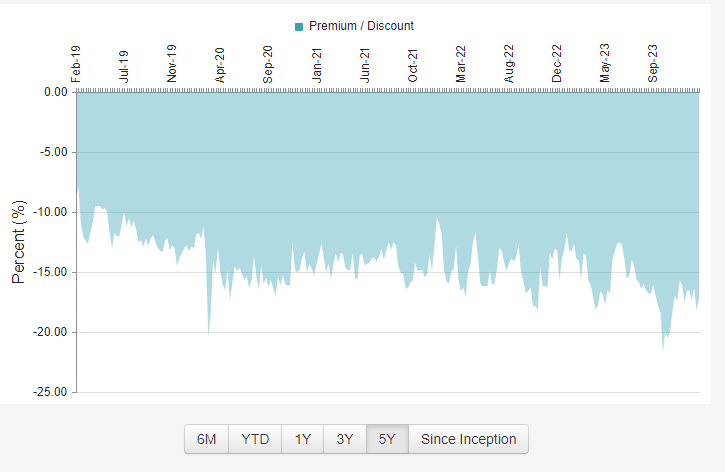

Korea Fund discount to NAV

CEFConnect

I highlighted in my article last year the large discount to NAV, and how the Korea Fund was hoping to address this. In 2020, they made a tender offer for 25% of shares.

Note that in the 2023 annual report they highlighted this could potentially occur again in late 2024 depending on the following; to quote “if the Fund’s total return investment performance measured on a net asset value basis does not equal or exceed the total return investment performance of the MSCI Korea 25/50 Index during the period commencing on April 1, 2021 and ending on June 30, 2024 and for three-year testing periods thereafter.”

Here is another interesting quote from that annual report, “As at this Period end the Fund’s NAV return for the tender period to date, namely from April 1, 2021 to June 30, 2023 was -25.94% slightly outperforming the benchmark return of -26.02%.”

I regard this as a little bit of inbuilt protection in the event they perform poorly over the next few months. Should it trigger another tender offer for 25% of shares, a shareholder could tender and get a nice pickup from the deeply discounted entry price.

Aside from whether this gets triggered or not, I see the fund as vulnerable to shareholder activism anyway. It is evident from the chart above that their measures to reduce the discount have failed. I could therefore see activist funds on the register pushing more aggressively for change soon.

Given the small fund size, perhaps the managers may also not put up much of a fight in such a scenario.

Conclusion

South Korean stocks are still out of favor in part due to the poor history of shareholder governance. It sounds like the setup in Japan before last year. That market then surprised many investors by being one of 2023’s best performing markets.

Despite the global economic risks and particular those stemming from China, South Korean shares are so discounted that such risks are worth taking on. The Korea Fund, with it itself being a potential activism target, is a good way to gain exposure at a large discount to NAV.

All of a sudden being bullish on Japanese stocks has become fashionable of late. The South Korean stock market is now poised to become fashionable in 2024 on the back of a similar thematic.

Q2 2024 Earnings Call Transcript")