Olena Ruban/Moment via Getty Images

Introduction

During 2021 cannabis stocks were the new hot ticket item in the market, but since then the burning fire surrounding them has seemed to cool. In turn, this has caused many of them to trade at attractive valuations currently. Especially, if you believe in the long-term outlook on the industry.

I remember watching Innovative Industrial Properties (IIPR) price surge to nearly $300 a share. That same year was the birth of another REIT and peer of IIPR, NewLake Capital Partners (OTCQX:NLCP). I had done research on this REIT some time ago but it was again brought to my attention by fellow analyst, Julian Lin. So, I decided to give them another look and in this article I discuss some things I like about NLCP, why I currently rate them a hold & why they may be a REIT for those looking for a high-yield.

Who Is NewLake Capital Partners?

NewLake Capital Partners is a real estate investment trust who leases properties to operators in the cannabis sector. The company IPO’d in 2021 when cannabis stocks were the new thing, similar to how Artificial Intelligence is the hot topic now.

Since then, the stock’s share price has been cut by roughly half. So, if you held the stock you’re in the red by roughly 50%. One reason for the share price decline in NLCP and many cannabis stocks is the uncertainty surrounding the industry.

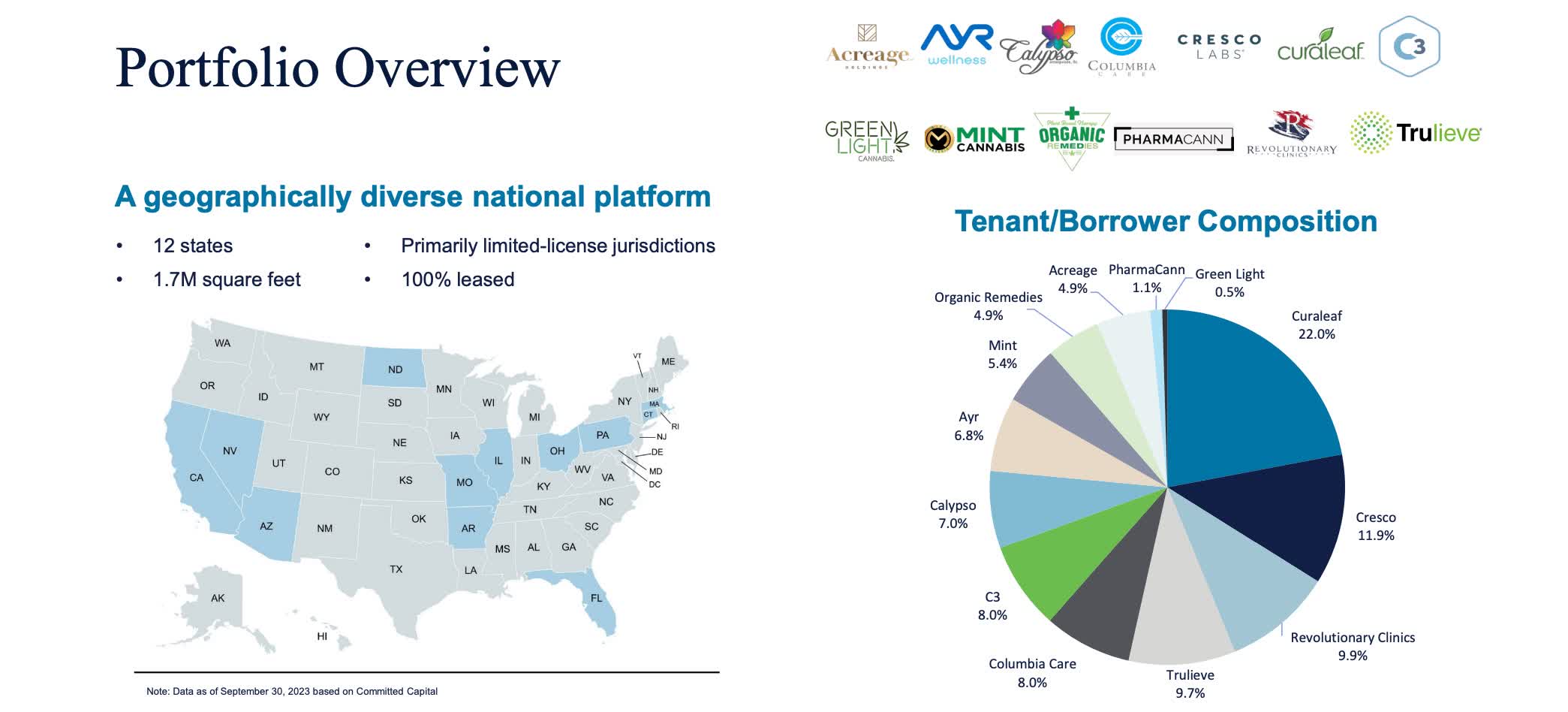

The REIT is fairly small and still growing with 32 properties across 12 states. Their largest operator is Curaleaf (OTCPK:CURLF), who also happens to be the largest public cannabis company with a market cap of $3.65 billion at the time of writing and is currently 22% of their total portfolio.

NLCP investor presentation

The good thing about NewLake is that they are a triple net lease REIT, which means all the onus of responsibility falls on the tenants. Maintenance, taxes, etc. Unlike single and double net leases where the owner is responsible for some of the costs. As a REIT guy I typically only invest in NNN leases so that’s a check mark for NLCP. Additionally, they are internally-managed as well, something else I look for when investing in REITs.

Cannabis Industry Growth

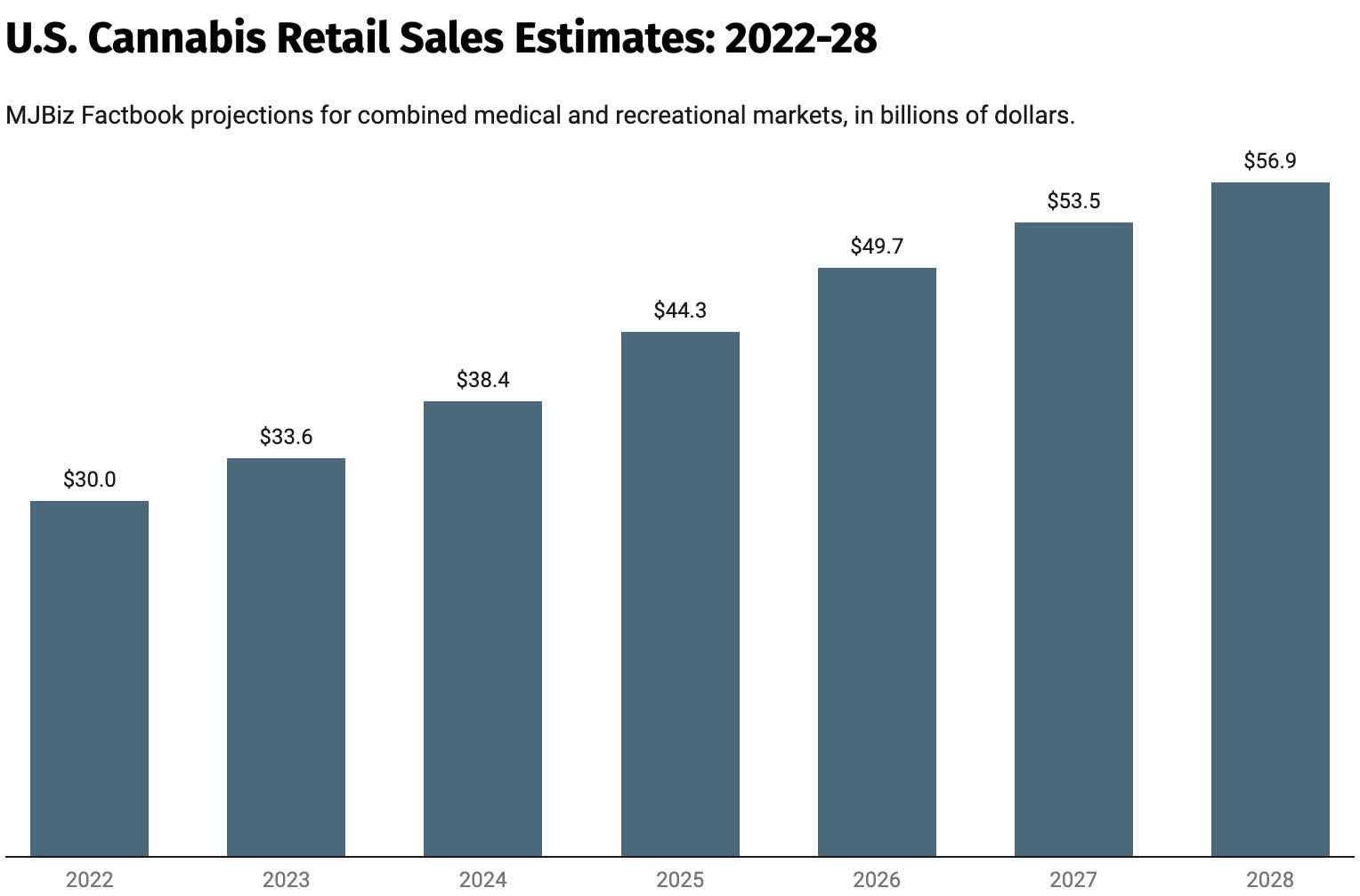

Last year the cannabis industry grew to roughly $34 billion from $30 billion the year prior. Looking out to the next four years the industry is projected to grow roughly 67% to $56.9 billion in retail sales.

MJBiz

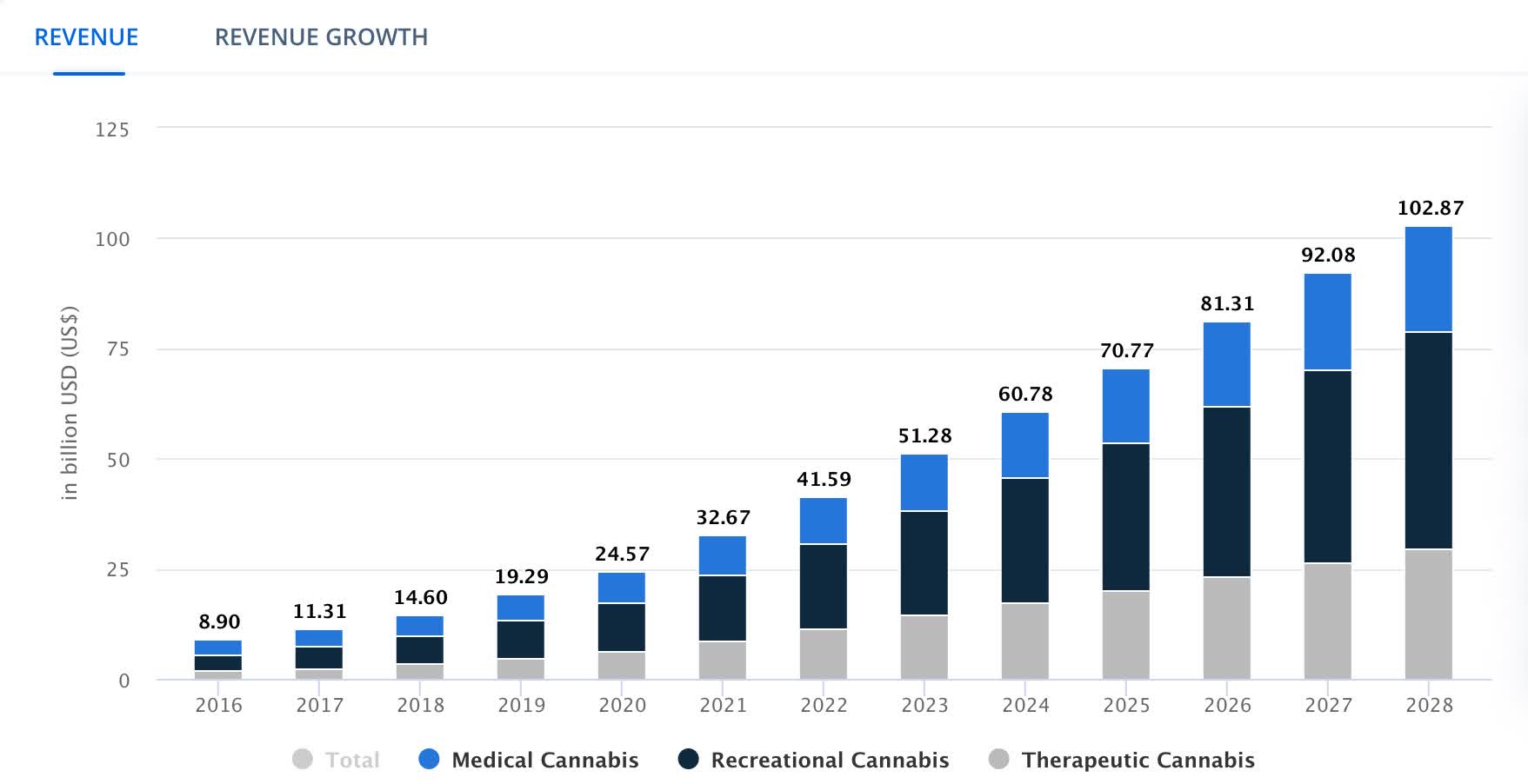

According to Statista, revenue is expected to climb to nearly $103 billion from $60.78 billion. So, the industry looks poised for some nice growth in the coming years. But with the uncertainty, I feel like the outlook feels a little like the uncertainty surrounding whether rates will be cut this year or not. No pun intended.

Statista

However you look at it, the industry has a lot of potential for growth in the future and I wouldn’t be surprised if rising demand will make it even more socially acceptable, leading to sustained growth for the foreseeable future. If this happens, the industry will evolve and more and more businesses will pour capital into the industry helping it grow even larger.

Solid Dividend Coverage

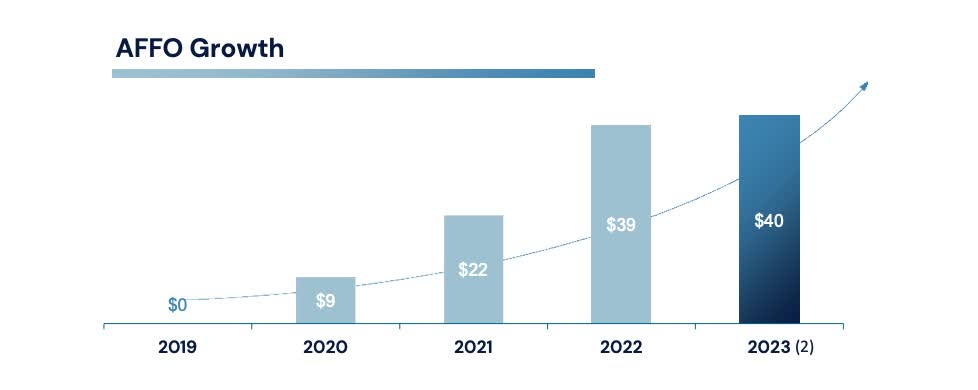

Since going public, NewLake has grown their dividend from $0.31 to the current $0.40 with the most recent raise of 2.6% coming not too long ago in December.

In the time of dividend growth, AFFO growth has followed ascending from $22 to $40. And management expects this to be $39.8 million to $40 million for the full-year. Slow growth from 2022, but some growth is better than no growth.

NLCP investor presentation

Through 3 quarters their FFO & AFFO have grown slightly quarter-over-quarter. FFO was flat for 2 quarters at $0.44 before ticking up a hair in Q3 to $0.45. AFFO also ticked up $0.01 in each quarter growing from $0.45 to $0.47. Again, little growth but their dividend coverage remained solid throughout the year giving them an AFFO payout ratio of roughly 82% for the last quarter.

AFFO for the full-year is expected to be $1.89, giving them roughly the same full-year payout ratio of 83%. Analysts expect Q4 FFO of $0.45 to round out the year. I expect FFO to be in the range of $0.46 to $0.48, posting a slight beat for the cannabis REIT.

Although their payout ratio is in between management’s target of 80% – 90%, I prefer to see a lower payout ratio, below 80%. However, REITs are required to pay out most of their earnings in the form of dividends, so NLCP’s payout ratio currently is safe. Me, personally, I just like to see REITs retain more cash to grow internally.

The only peer to compare them to in the industry is Innovative Industrial Properties who has a current AFFO payout ratio of 79%. Here, I compare them to some of my personal favorites in the sector: VICI Properties (VICI) and NNN REIT (NNN). VICI is scheduled to report Q4 earnings later this month but ended Q3 with a AFFO payout ratio of roughly 77%.

NNN on the other hand ended the full-year with a very low AFFO payout ratio of 68.4%. Their conservatism is one of the reasons I prefer to invest in these two REITs, especially NNN REIT. The more cash one retains, the more capital they have to reinvest back into the business without diluting shareholders by issuing shares to raise capital. Of course, this is a part of their business model so it’s not necessarily a bad thing. But I’d rather the company retain capital by covering the dividend by a respectable amount.

Low Debt & Buybacks

Something else I like about NewLake is the REIT has virtually no debt with a net-debt-to EBITDA ratio of just 0.2x. Additionally, they had $89 million available liquidity on their credit facility and $31 million in cash with debt of only $2 million. So, from a balance sheet standpoint the REIT is in a strong financial position.

Furthermore, the company announced a second buyback program for $10 million during the third quarter. This was shortly after buying back a substantial amount of shares over the year. The second program signifies management believes the stock is undervalued at the moment. I think it is good the company is taking advantage of cheap shares by buying them back, something REITs don’t do all that often.

Risks

Something that seems to plague cannabis companies and could be a reason they trade at discounts are their troubled tenants. Some seem to have problems collecting rent. And NewLake Capital Partners has been no exception with trouble over the year from tenants, including Revolutionary Clinics.

Their EBIDTA coverage for properties also declined from 4.5x in Q2 to 4x in the latest quarter. Non-payments of $1.3 million from Revolutionary Clinics caused revenue to decline year-over-year by 4.9%. This forced the REIT to enter into an amendment and a forbearance agreement. Furthermore, they collected $480k of unpaid rent and applied the remaining $315k of security deposit to rent, which is expected to be recognized as income in the upcoming quarter.

An additional tenant, Calypso, also defaulted on rent payments but got back to paying rent on a weekly basis to support their cash flow cadence. This is something for current investors or those looking to start a position in NLCP to be aware of going forward.

With interest rates looking like they will remain higher for longer with core inflation creeping up, the challenging backdrop will likely continue to place downward pressures on portfolio companies going forward. If so, NLCP’s financials will likely see a drop in the coming quarters.

Undervalued

With AFFO expected to be $1.89 for the full-year, this gives NewLake a FWD P/AFFO ratio of just 8.5x, below the sector median of 14.65x. So, currently the stock is very undervalued but because of the uncertainty surrounding the industry, I think that plays a big part in the company’s valuation.

Peer IIPR trades slightly higher at roughly 10x P/AFFO, but is currently undervalued as well, sitting well-below their 5-year average of roughly 18x. So again, if you believe in the outlook of the cannabis industry, NLCP could turn out to be a great investment at the current valuation. Furthermore, they currently trade at less than 1x their Book Value per share of $19.72. So, I think it’s safe to say the stock is compelling here.

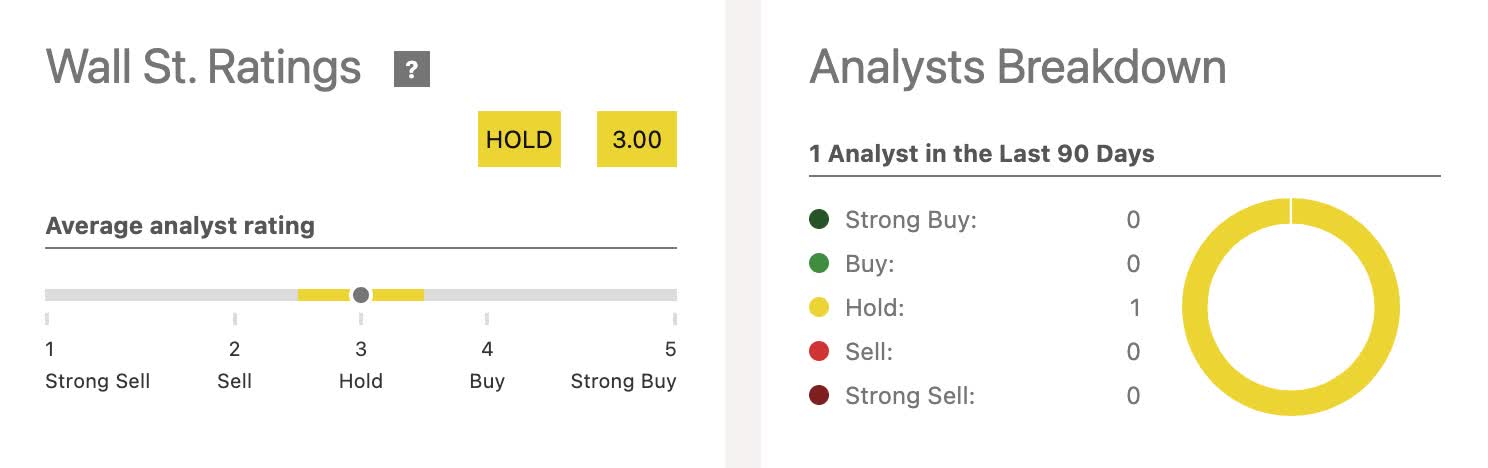

Wall Street also seems to be in agreeance with my current rating also with a hold for NewLake Capital, likely due to the cloudy outlook on the industry. But if you want a high-yield and are a short term investor, then NewLake is a speculative buy. As a more conservative investor that holds stocks for the long-term, I currently rate them a hold.

Seeking Alpha

Wrap-Up

All in all, I think NewLake Capital Partners is a solid REIT with what seems to be like a strong management team. There are things I like that the newcomer is doing like taking advantage of the suppressed share price by buying back a substantial amount of shares. This will likely grow their financials over time and further increase their dividend coverage for the foreseeable future.

But as stated in the article, the uncertainty surrounding the industry as a whole makes investors skeptical of the REIT. Additionally, their tenant problems continue to plague the company and will likely continue with rates possibly remaining higher for longer.

Despite their dividend coverage and low debt, I would like to see more from the company; more so how their tenants hold up in the challenging environment in the coming quarters. Due to this, I rate the stock a hold for now with the potential to upgrade to buy in the near future if tenant quality increases along with a more favorable outlook for the industry.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")