Kobus Louw

About 16 months, since I suggested people avoid John Wiley & Sons (NYSE:WLYB) in an article with the monumentally creative title “Avoid John Wiley & Sons Inc.” Since then, the shares are down a total of about 6.8% against a gain of 34% for the S&P 500. The fact that I sidestepped this underperformance is gratifying on some level, but it imposes on me a sort of obligation to return to the name. After all, a stock trading at $33.84 is a less risky bet than the same stock when it’s trading at $38.50. So, I’m going to review the name again to see if this is a great entry price, because what was a terrible investment at $38.50 could potentially be a great investment at $33.84. I’ll make that determination by reviewing the financials and by comparing this to the risk-free alternative. After all, a stock is a more risky investment than is a government bond, and for that reason, I think it’s reasonable for stock investors to receive compensation that at least matches what they could receive from the 10 Year Treasury Note.

I know that my writing can be “a bit much”, and for that reason, I offer up a thesis statement at the beginning of each of my articles as a way for readers to minimize the painful exposure to my awful jokes and proper spelling. You’re welcome. I think the financial history here is troubled, and I’m particularly worried about the deterioration of the capital structure at a time when operating income is falling. I like the fact that the dividend yield is only slightly lower than the risk-free rate, but that’s not good enough to warrant a buy in my view. Being “only slightly lower” than the risk-free rate, while offering much more risk than same disqualifies this stock from consideration at current prices. I’d become more interested if the shares hit the mid to high $20s, but at current levels, I’ll pass. Also, I don’t want to read any comments below about the risks of government bonds, specifically the risk of inflation eroding their purchasing power. My response is always something akin to “I know that, and do you believe that the stock elves magically keep inflation from eroding dividend cash flows?”

Financial Snapshot

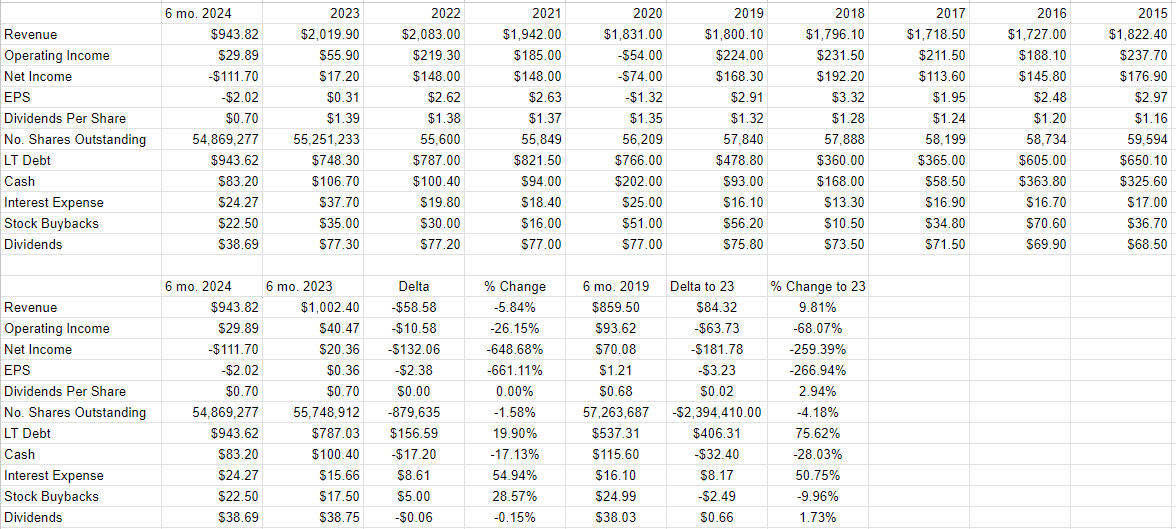

When reviewing the recent financial history here, the first word that leaps to mind is “sclerotic.” Compared to the same period last year, revenue and operating income are down by 5.8% and a whopping 26% respectively. It’s not like last year was anything “to write home about” as the young people say. Specifically, operating income last year was lower than the previous year by 74%. Additionally, operating income during the most recent reporting period is about 68% lower than it was in 2019.

Unfortunately, the situation in the capital structure is no better in my view. Cash is down by about 17%, and long term debt has exploded by $157 million, or 20%. Long term debt now sits at a decade record. At a time of relatively higher interest rates, this is troublesome, obviously. Speaking of that, unsurprisingly, interest expenses have risen dramatically by about 55%. This may offer a clue about why the dividend hasn’t grown at all over the past year.

I could go on about the problems associated with the financial results here, but my readers don’t need me to review history. My readers eagerly wait with bated breath for my insights on whether a stock is worth buying or not. In my view, the financial history here is relatively poor, but that doesn’t mean that you should eschew this enterprise. It just means that we investors need to be compensated for buying, given the relative risk of ownership. In the next section, I want to quantify as much as I can the level of extra risk investors are taking with this stock.

John Wiley & Sons Financials (John Wiley & Sons investor relations)

The Stock v The Treasury Note

I measure everything against Treasury Notes because these represent the risk-free rate. If an investment that comes with risk offers less than compensation than the risk-free alternative, it is illogical to buy the risky investment. I feel somewhat embarrassed for needing to point this out, but given some of the conversations I’ve had lately, I do feel the need. When I compare a stock to a Treasury, I ask the question “at what rate will the dividend need to grow in order for the stockholder to receive the same cash flows as the Treasury Note holder?”. Note, I’m asking what is needed to match the risk-free, but since stocks have risk associated with them, they should offer more than the risk-free rate, but never mind.

In terms of John Wiley, the yield on the stock (4.17%) approximately equals the 10 Year Treasury Note yield of 4.258%, so there isn’t much growth required. Because I’m a bit of a math nerd, “there isn’t much growth required” is not sufficiently precise, so I “ran” the numbers, and I present them below for your enjoyment and edification. In order to receive the same cash flows as investors in the risk-free Treasury Note, this dividend will only need to grow at a CAGR of about .5% over the next decade. In other words, the dividend could remain flat for a decade and investors would receive about the same as they do with the risk-free rate. That’s actually relatively rare, and is a significant positive here in my view.

Stock V Treasury Note (Author calculations)

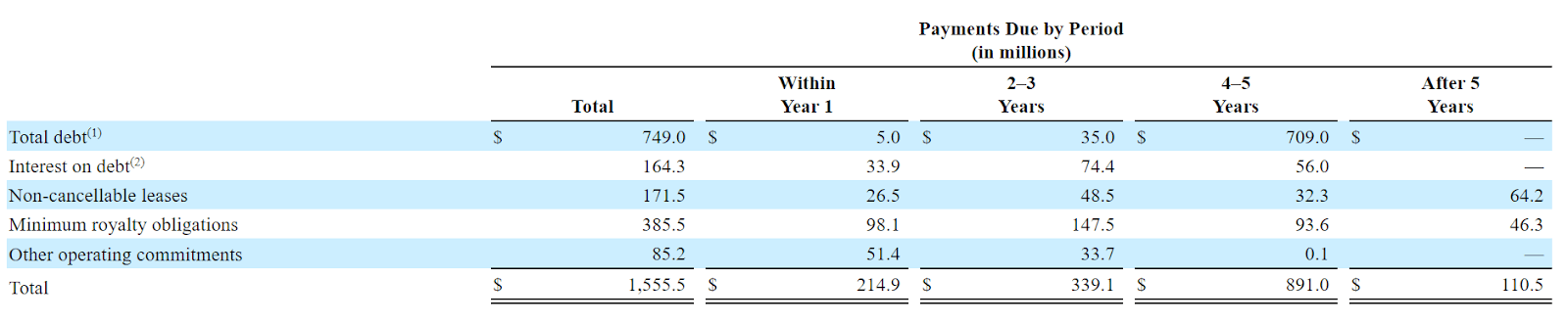

There’s only one fly in the soup, though. There’s a risk that the dividend will be cut over the next decade, and that’s a risk not presented by the 10 Year Treasury Note. To highlight this point, I’ve plucked the size and timing of upcoming cash obligations from page 48 of the latest 10-K, and I present it below for your reading pleasure. It seems that there will be many demands on the company’s cash over the next several years. Given the fact that operating income is down significantly, that presents a problem. This is perhaps not an insurmountable problem, but in a world where an investor can simply buy a Treasury and sleep at night, or buy this stock, why would they choose the latter course?

Wiley Upcoming Cash Obligations (Latest 10-K)

Given the slowdown in operating income, the deterioration of the capital structure, the significant cash obligations over the coming years, I think there’s a risk that the dividend will need to be cut. In that case, it makes sense to eschew the stock and buy the Treasury.

Q2 2024 Earnings Call Transcript")