JLGutierrez

Written by Nick Ackerman.

For some background on this monthly publication, here is my view on dividend growth stocks:

Dividend growth stocks aren’t always the most exciting investments out there. They often aren’t grabbing the headlines, and they aren’t the stocks running up hundreds of percentages in a year. In fact, they are often some of the least exciting stocks. And that is precisely their strongest selling point. With such a vast world of dividend growth stocks available out there, it is important to screen through to see if there are any worthwhile investments to explore.

They are stocks that provide growing wealth over time to income investors. Dividend growers are often larger (not always), more financially stable companies that can pay out reliable cash flows to investors. Some are slower growers than others. Some are going to be cyclical that require a strong economy. Some are going to be secular, which doesn’t generally rely on a more robust economy.

Dividend growth can promote share price appreciation. Of course, that is if these companies are growing their earnings to support such dividend growth in the first place. Trust me. There are yield traps out there – I’ve owned a few that I’m not particularly proud of.

I like to think of investing in dividend stocks as a perpetual loan of sorts. Essentially, every dividend is a repayment of your original capital. Eventually, holding long enough, you have the position “paid off.” It is all returned back into your pocket from that point forward.

All of this being said, it is important to understand my approach to dividend stocks and why screening dividend stocks can be important for income investors. As with any initial screening, this is just an initial dive – more due diligence would be necessary before pulling the trigger.

The Parameters For Screening

I’ll be using some handy features that Seeking Alpha provides right here on their website for this screen. In particular, I will be screening utilizing their quant grades in dividend safety, dividend growth and dividend consistency.

Dividend Safety is relatively self-explanatory. These will be stocks that SA quants show reasonable safety compared to the rest of their various sectors. The grade considers many different factors, but earnings payout ratios, debt and free cash flow are among these. This category will be stocks with A+ to B- ratings.

For the dividend growth category, we have factors such as the CAGR of various periods relative to other stocks in the same sector. Additionally, the quants also look at earnings, revenue and EBITDA growth. As we will see, this doesn’t mean that every stock with a higher grade has the growth we are looking for. This just factors in that the dividend has grown or earnings are growing to support dividend growth possibly. For these, the grades will also be A+ through B- grades.

Finally, for dividend consistency, we want stocks that will be paying reliable dividends for us for a very long time. In particular, hopefully, they are raising yearly, though that isn’t an explicit requirement. We will also include stocks with a general uptrend in dividend payments, which means there could have been periods where they paused increases for a year or two.

After looking at those factors alone, we are left with 406 stocks at this time from the 420 listed last month. I’ll link the screen here, though it is a dynamic list that constantly updates regularly. When viewing this article, there could be more or less when going to the link.

From there, I wanted to narrow down the list a lot more. I then sorted the list by forward dividend yield, from highest to lowest. Since these will be safer dividend stocks in the first place, screening for those among the higher payers shouldn’t hurt.

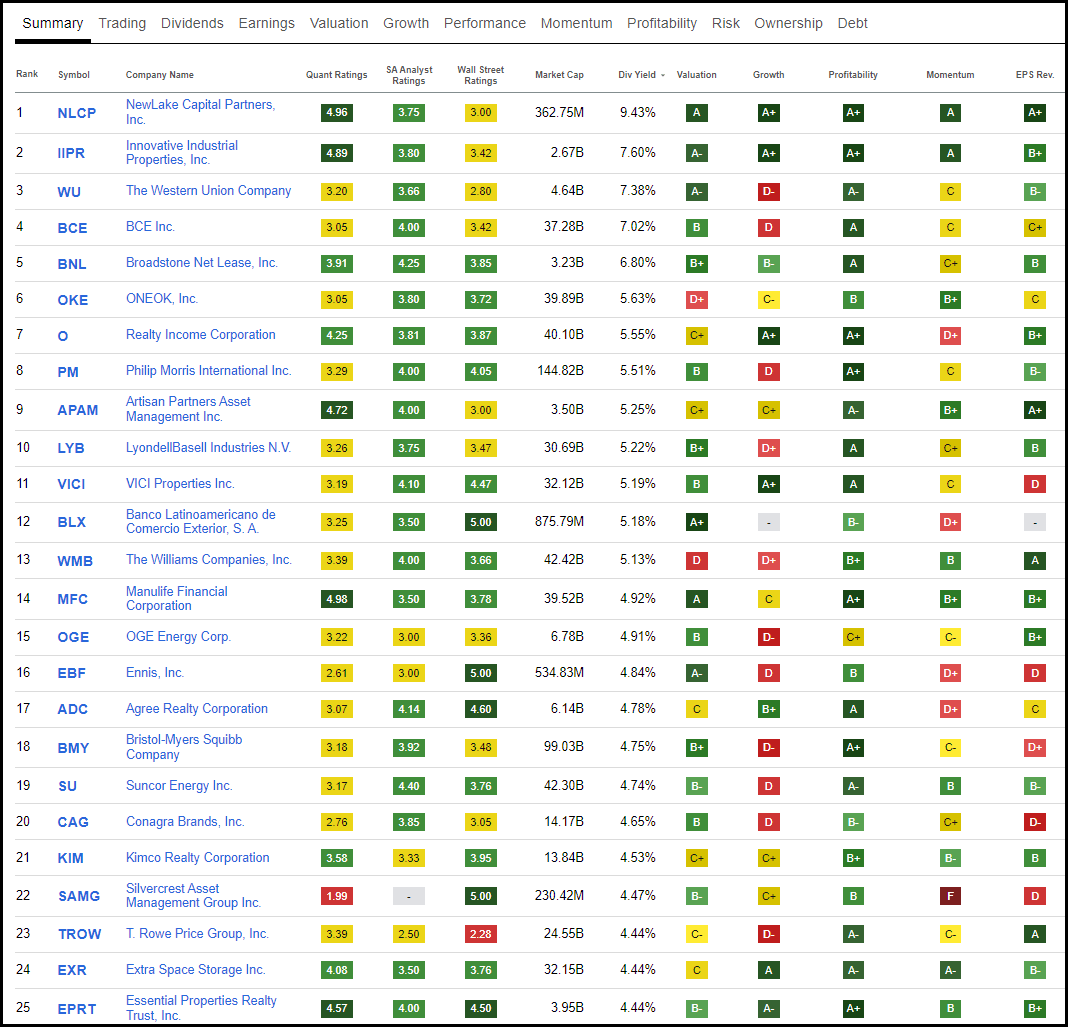

I will share the top 25 that showed up as of 02/03/2024.

Top 25 Screening (Seeking Alpha)

Right at the top of the list are the cannabis REITs, NewLake Capital Partners (OTCQX:NLCP), and Innovative Industrial Properties (IIPR). These are high-yielding, provide some dividend growth, and are definitely interesting. However, we actually just recently touched on those last month. Given the nature of the list, we generally have a lot of repeats, but I avoid giving some quick updates except for once a quarter.

From there, we have Western Union (WU) come up again, but this one no longer meets the criteria of a growing dividend, as they’ve held it steady for several years now. They are in a position where the best bet is just holding a flat dividend, which could be a struggle, let alone raising it. Artisan Partners Asset Management (APAM) is another one we skipped over due to a variable dividend policy.

We then have BCE (BCE), Broadstone Net Lease (BNL), Philip Morris (PM), LyondellBasell Industries N.V. (LYB), The Williams Companies (WMB), Manulife Financial Corp (MFC), all interesting names, but all names we recently covered.

That leaves ONEOK (OKE), VICI Properties (VICI), OGE Energy Corp (OGE), Agree Realty (ADC) and Bristol-Myers Squibb Company (BMY) as names we’ll be giving a quick dive into today.

Before diving into these names, there is one name I wanted to go back to and briefly mention: Medifast (MED). This was a name that had previously made this monthly screening piece on occasion, but one I thought would only be a speculative bet. I was definitely skeptical about the dividend, which they ultimately eliminated the quarterly dividend in a December press release.

ONEOK 5.63% Yield

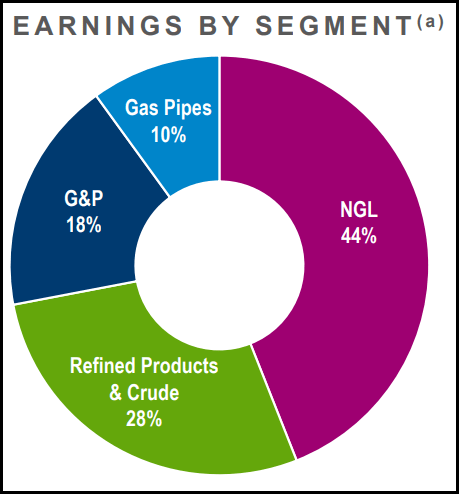

OKE is a name that appears frequently, with the last time being November 2023, when we touched on this energy name. Last year, this company acquired Magellan Midstream (MMP), and that was completed last September. The company is primarily focused on natural gas liquids, from which it derives the largest portion of its earnings. The breakdown below is as of their latest investor presentation and includes both ONEOK’s and Magellan’s operating income.

OKE Earnings By Segment (ONEOK)

The company had previously been an MLP, but they converted to a corporation in 2017. That means they report on 1099, and investors can avoid a K-1, as some often prefer.

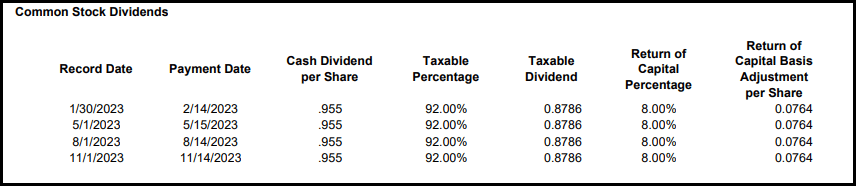

That said, the distributions from OKE can still contain a portion of return of capital – it is quite a small portion but a portion, nonetheless. That can also be a benefit because ROC distributions reduce an investor’s cost basis rather than become taxable in the year received.

OKE Distribution Breakdown (ONEOK)

Hold onto the shares long enough to pass down to your heirs, and you may never have to pay a tax on at least a portion of these distributions ever.

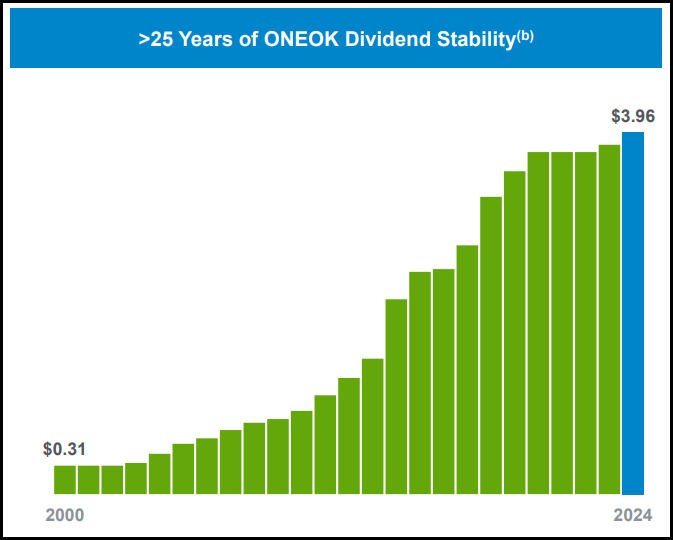

Holdings shares of OKE can be pretty easy to hold as they offer a generous yield that has been tending higher for decades now. While they took a pause during the Covid pandemic, they have since returned back to rewarding shareholders.

OKE Dividend History (ONEOK)

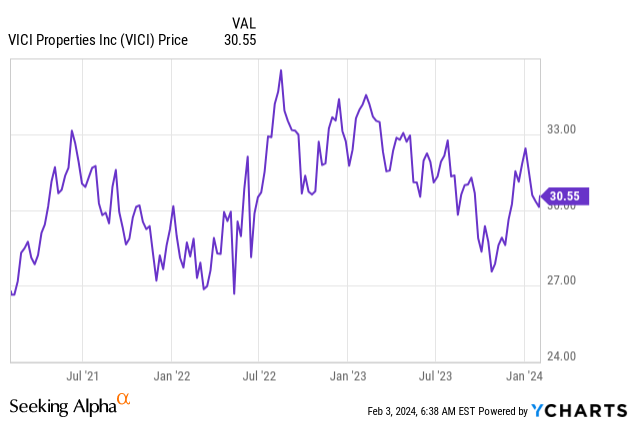

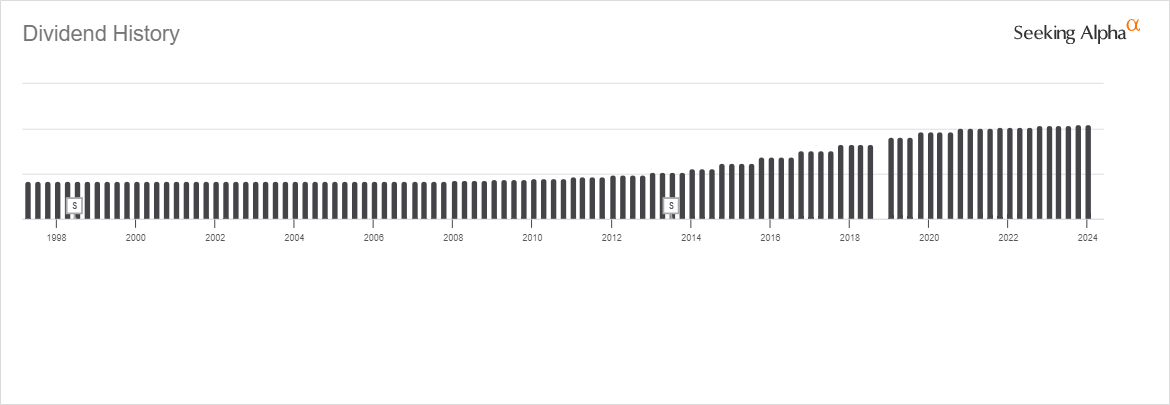

VICI Properties 5.19%

VICI has also made the list this month. This one isn’t always so common, but we had just touched on this name back in November 2023 as well. Prior to that, we haven’t given this one attention for this monthly publication since going back to April 2022. One of the problems was that the share price rising through that period would have ended up pushing the yield lower. With the shares sinking, the yield is increasing, and it’s pushing it higher up on this screening list.

YCharts

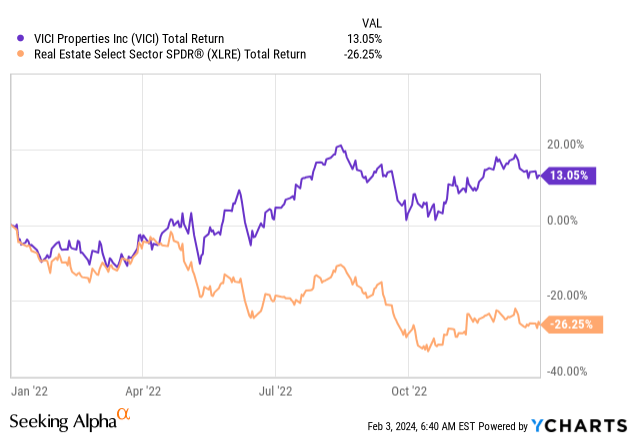

Even when REITS were getting slammed throughout most of 2022, VICI was able to hold up better. In fact, they weren’t just holding up better; they were thriving in terms of total return relative to the Real Estate Select Sector SPDR (XLRE), which performed terribly through 2022.

YCharts

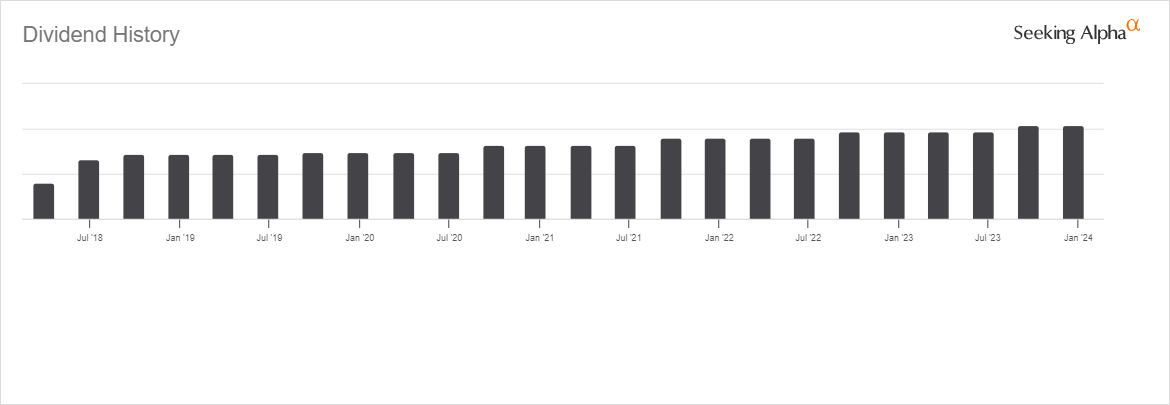

Further helping out the yield here to push it higher was that they’ve continued to raise their dividend. This is a well-supported dividend that can continue to grow, as well as the forecast for continued FFO growth in the coming years.

VICI Dividend History (Seeking Alpha)

This is an experiential REIT that was primarily focused on owning casino properties. That has been shifting into more broad entertainment experiences with acquisitions such as 38 bowling alleys from Bowlero Corp last fall. They’ve also recently provided a construction loan to develop a Margaritaville Resort in Kansis City, Kansas, as well as three youth sports facilities. Within this deal is a call right where VICI could take control of the properties at their option.

So, their portfolio is definitely expanding. While it’s making it a less focused play on casinos, diversification doesn’t necessarily hurt either. Being limited to one experiential type of property would eventually seem to limit growth in earnings going forward at some point, anyway.

We took a gamble with this one by selling the March 15, 2024 puts at the $30 strike price. We took in some options premium and will potentially be picking up a position.

OGE Energy Corp 4.91% Yield

This is a new one to the list this month that we haven’t taken a look at before. Its name, “OGE,” stands for Oklahoma Gas and Electric. Being a utility company, it certainly is something that I’m usually interested in. They had previously been an electric utility company with a midstream business. However, the mainstream business was exited in 2022 when they sold their Energy Transfer units.

Their earnings seemed to be a bit messy around that period, but forecasts are for some modest growth going forward after we get through 2023.

OGE Earnings History and Estimates (Portfolio Insight)

Even with that volatility in earnings, the company has been able to deliver dividend growth for a number of years now. That was starting with raises going back to 2007, after holding the payout steady for many years.

OGE Dividend History (Seeking Alpha)

(They did pay all the dividends in 2018; the chart above just has an error that one was missing.)

In an earnings call, they noted that their dividend policy was to have a payout ratio of 65 to 70%. Given the payout based on EPS is pushing closer to around 80%, that is a good reason why the last few increases have been much smaller. Given their stated policy, small increases are likely to continue if they want to keep up the streak of dividend raises. Alternatively, they could freeze the dividend where it is until earnings catch up. Of course, another option is to cut the dividend to get it back in line with their policy, but most companies use that more as a last resort.

Ultimately, OGE could be an interesting utility name. Still, upon this cursory surface look at the name, nothing would really draw me away from preferring WEC Energy Group (WEC), DTE Energy (DTE), or NextEra Energy (NEE) utility names that I currently own. It’s a bit cheaper relative to DTE and NEE but close to the same P/E multiple as WEC, with WEC having better growth prospects going forward.

Agree Realty 4.78% Yield

ADC is not a familiar name for this monthly screening article. We covered it only one other time, coincidentally going back to February 2022 and making it two years later that we are finally touching on this name again for this monthly publication.

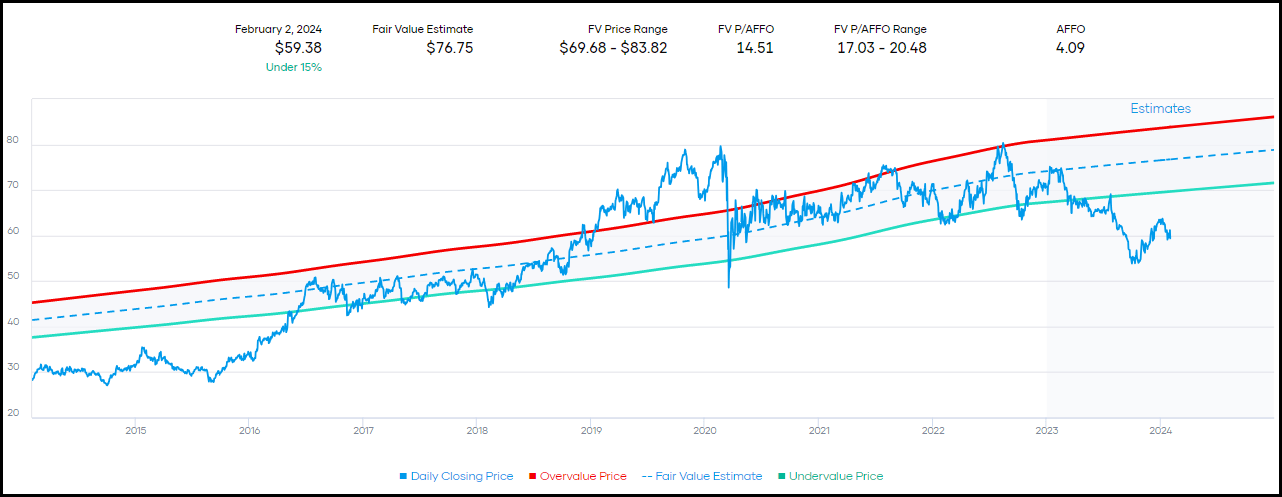

That said, ADC is one REIT I’m more than a little familiar with, as it’s a holding in my portfolio. In fact, we just recently took a fresh look at this one, giving it a full review. I thought, despite a big run-up from the last October lows, that ADC was still a decent value. It subsequently reversed some of that run-up with risk-free rates rising once again, but I don’t regret saying it was attractive then. It’s just even more attractive now.

ADC Fair Value Range (Portfolio Insight)

It is attractive enough that I sold the February 16, 2024, $60 puts to take in some premium while potentially being on the hook to buy the shares at that strike price. Which, at this point I am looking to take assignment of the shares.

Bristol-Myers Squibb Company 4.75% Yield

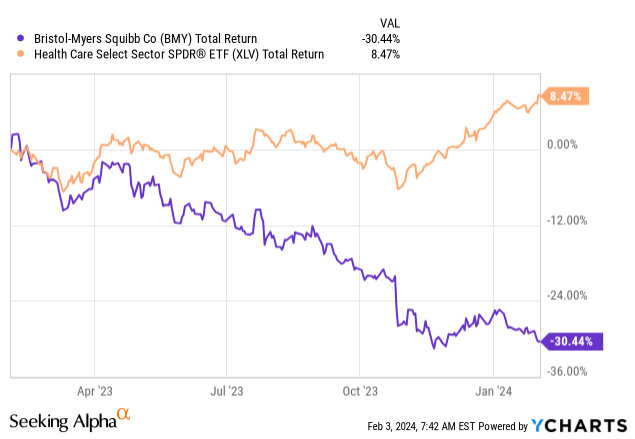

A newcomer to the list this month is BMY, which we have not touched on before in this monthly piece. Most companies in the healthcare space haven’t been performing well despite being usually a solid defensive sector with steady earnings. In the last year, the Health Care Select Sect SPDR (XLV) was mostly flat before turning higher off the October lows. That said, BMY seems to be facing an even tougher time in the share price department relative to the sector the broader sector. Instead of rebounding in October, it only sunk further lower.

YCharts

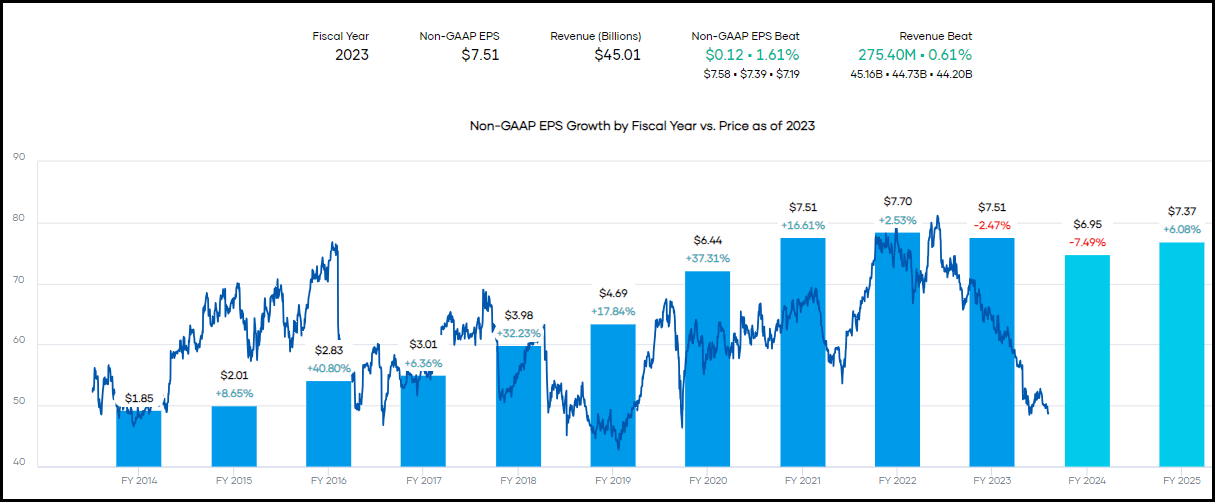

The outlook for earnings shows that 2024 appears to be another year of decline, which follows 2023’s trend. Analysts expect earnings to return to growth in 2025, but that still wouldn’t reach the peak earnings that they had in 2022.

BMY Earnings Vs. Price (Portfolio Insight)

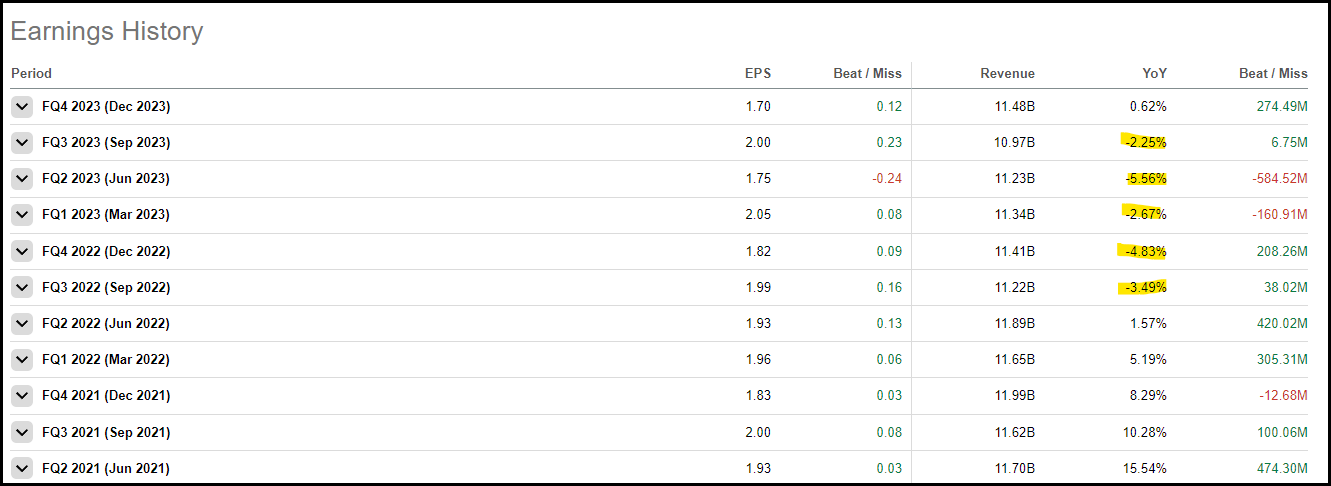

This had been after earnings were growing at a really healthy clip from 2014 to 2022. What has hit the stock appears to be the “loss of exclusivity for its blockbuster multiple myeloma therapy Revlimid.” Revlimid revenue declined 39% in 2023 from 2022. That put pressure on the entire company, causing revenues to decline for several consecutive quarters. Elqiquis and Opdivo are larger contributors to the company’s revenue, which they were able to grow revenue by 4 and 9%, respectively, in 2023. These three drugs account for nearly 61% of BMY’s entire revenue.

That said, in the most recent quarter, they were finally able to buck the trend of declining revenue. It was only a slight buck of the trend with some shallow year-over-year growth, but it is heading in the right direction, nonetheless.

BMY Earnings History (Seeking Alpha)

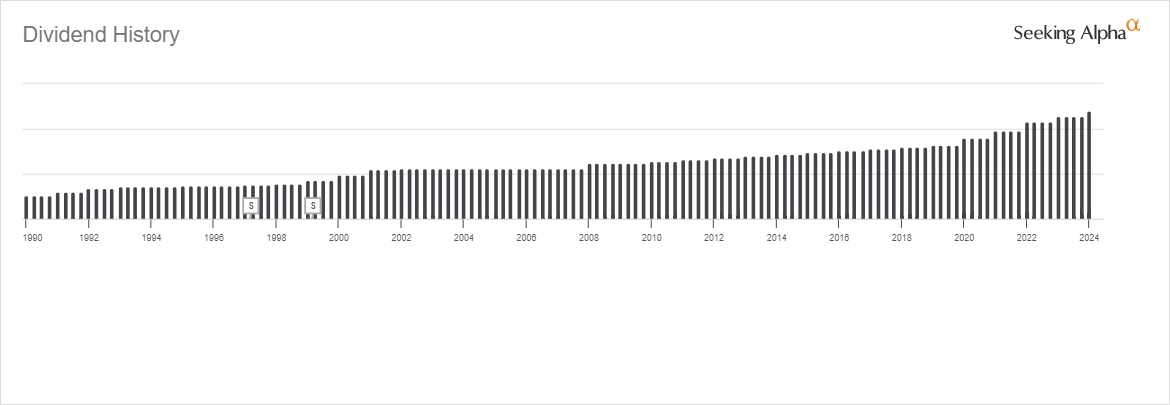

The company has been able to continue growing its dividends despite the headwinds that it is facing. The last dividend raise of 5.26% was even fairly aggressive for a company that is seeing some decline in its earnings. One of the reasons for this appears to be that they are paying a very conservative dividend, with a forward payout ratio of only 34% based on EPS. The free cash flow payout ratio comes to less than 44%. That’s despite the anticipated contraction in earnings and upping the dividend. There is a lot of room here.

BMY Dividend History (Seeking Alpha)

Further, they did provide their own 2024 guidance with their latest earnings. They are expecting revenue to grow in the low single digits and non-GAAP EPS to be in the range of $7.10 to $7.40. That’s still a slight decline year-over-year but not a decline as much as analysts were expecting.

With the shares down in the dumps, it could be time to consider this pharma giant at a forward P/E of 7x. That said, I’m nursing my own wounds in the healthcare pharma turnaround play category with Pfizer (PFE) in the Satellite Portfolio. Fortunately, holding positions in Merck (MRK) and AbbVie (ABBV) in the healthcare space has been much more rewarding in my Core Portfolio.

Q2 2024 Earnings Call Transcript")