grandriver

Investment Introduction

Diamond Offshore Drilling, Inc. (NYSE:DO) is trading in the middle of its 52-week range, which is between $9.56 and $17.32. It is quite a volatile stock but the past 6 months have been a consistent downtrend for the stock, despite strong operational results from the core business along with new contract awards on a nearly consistent quarterly basis. Just a little over a week ago DO secured another rig contract valued at $360 million as a continuation contract from an already existing one with BP. DO has come from a very hard point in 2020 when it filed for bankruptcy and in 2021 put itself up for sale. The bankruptcy filing ultimately ended up converting $2 billion of debt into equity. The whole ordeal began as it got stuck between what was cited as a “price war” between OPEC and Russia. DO is securing new and more favorable contracts these days instead of old legacy contracts it had signed previously at very low rates, ultimately ending up hurting the business earnings. DO is a company that has come from a lot of challenges, like unprofitable years, and bankruptcy, so being a little more cautious would be my recommendation here and jump the gun too fast. With this line of thinking I will be assessing DO as a hold as we approach earnings in a few weeks.

Company Introduction

DO is included in the energy sector and more specifically in the oil and gas drilling industry. Here it has been operating for a very long time, dating back to 1953. DO focuses on providing contract drilling services to a global energy market.

The company used to have a very large fleet but following what I cited as “price wars” between OEPC and Russia during the pandemic when oil prices plummeted it seems DO was stuck in between and the operations were no longer profitable. In 2020 DO had negative earnings of $1.254 billion, and the year after it was a negative $2.139 billion. Since then it has managed to regain a profitable bottom line through new contract signings that include higher rates which are of course beneficial to DO and its earnings.

Looking at the energy sector, one of the fastest growing parts here is anticipated to be offshore drilling of oil and gas. Many areas where oil is drilled are already somewhat saturated. Take the Permian Basin for example in the US, the major players here are energy behemoths with vast amounts of capital and we have seen how to expand in the region you need to spend capital the amount of a small nation. However, one area that hasn’t seen such saturation is offshore drilling, and DO does anticipate this as well, stating the following in the Q3 report, “we see a continuation of positive indicators of a strong and lasting upcycle, including growing rig demand, increased investment in offshore upstream projects, and shrinking rig availability”.

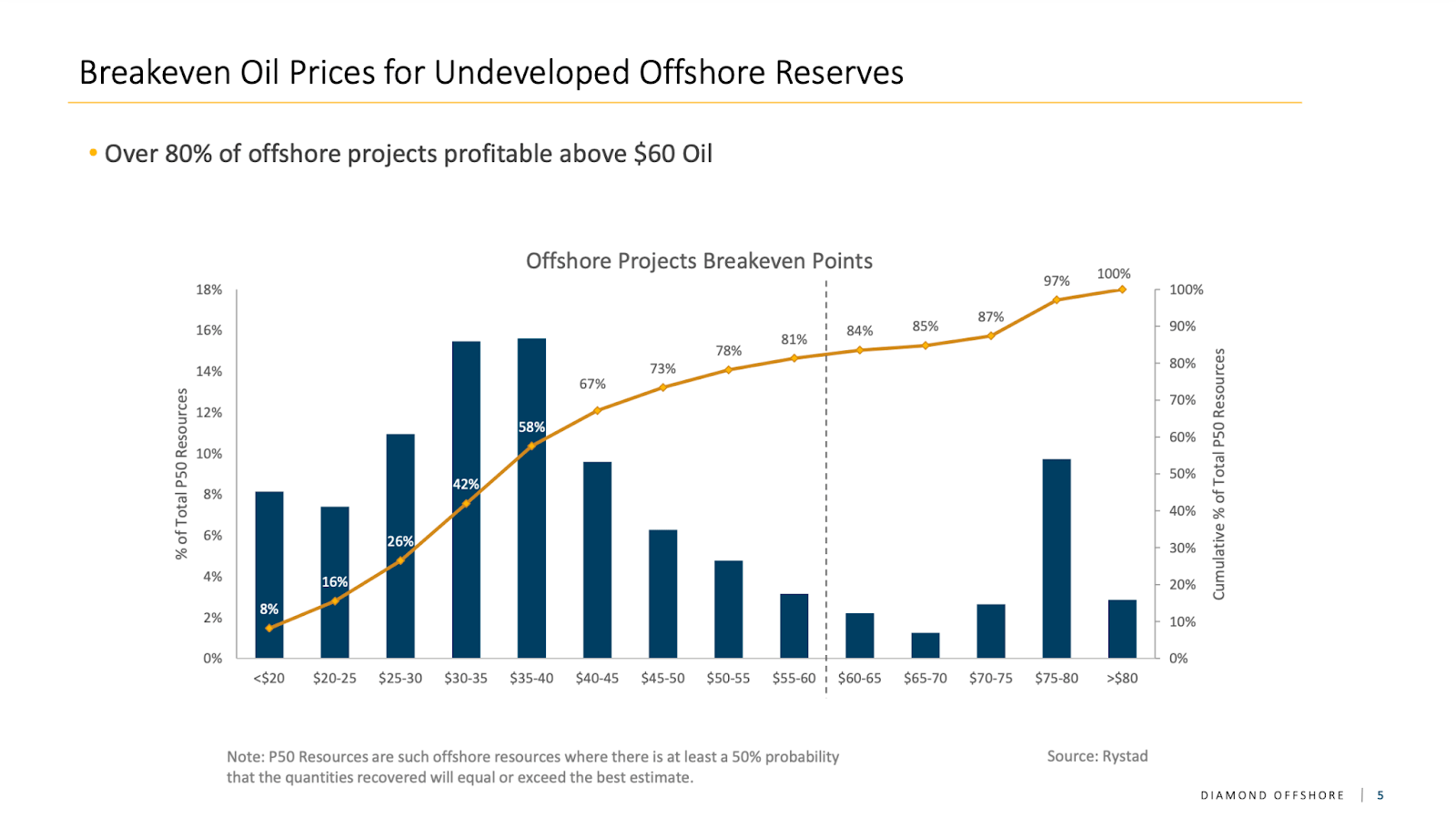

Oil Price Profitability (Investor Material)

Along with this the offshore projects it has going for it are 80% profitable above an oil price of $60. Estimates are for oil to stay a fair bit above this in 2024 and beyond. The two-year outlook is estimating a higher oil price of $80 per barrel which would mean strong earnings potential for DO and likely other offshore drilling contractors too. DO also notes how that floater demand is expected to continue to increase and that supply of it might slip, further putting DO in an even better position to sign favorable contracts as fewer of them are available.

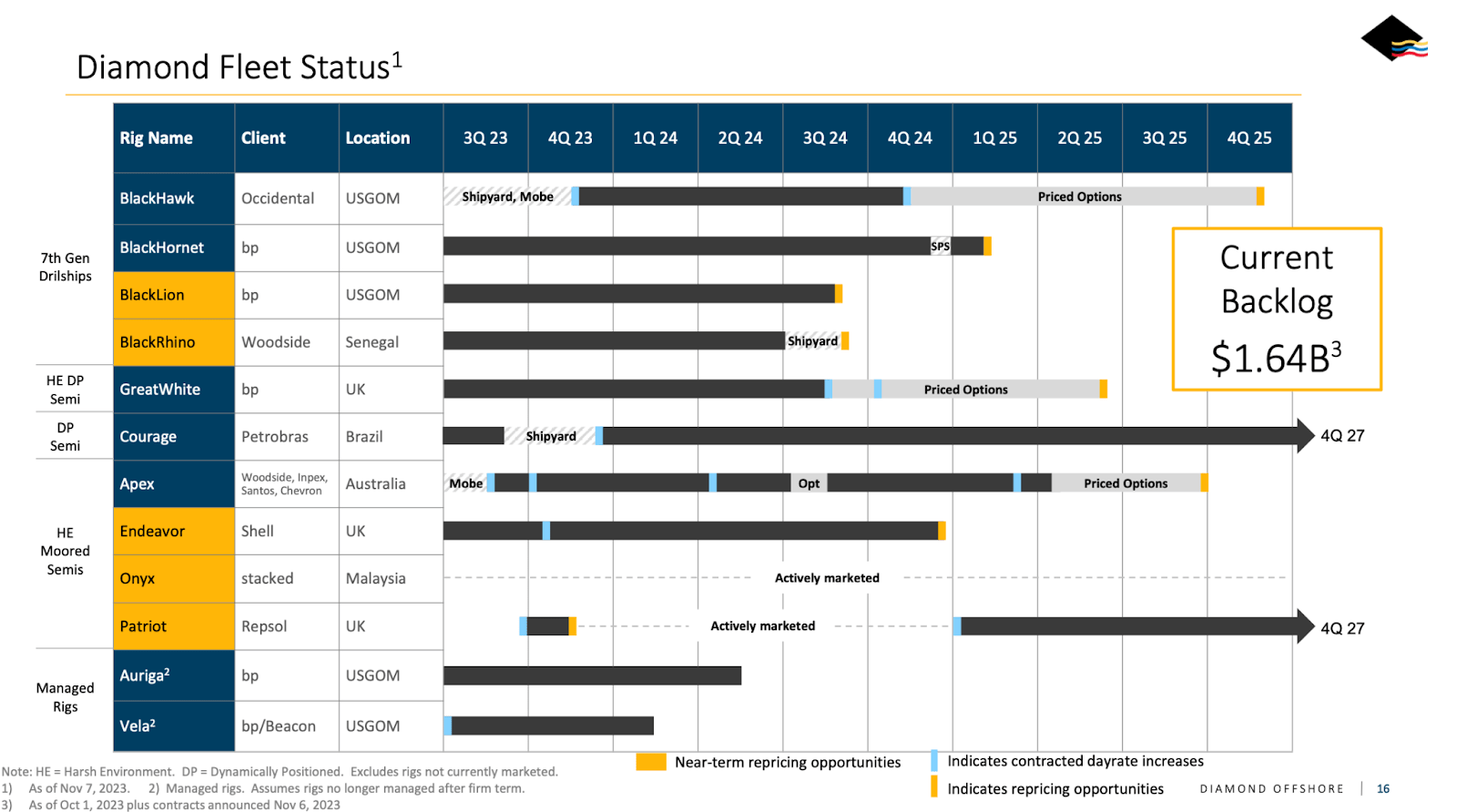

Fleet Status (Investor Material)

Looking a little closer at the current fleet status, it indicates a significant amount of contracted day rate increases in just the next 12 months. I think DO is evolving and the business is finally getting back on track with the market and rid of these low-rate contracts it used to have. One attribute that DO has is relatively short contract times as well, with 85% of the total rig count underutilization last quarter. This of course is both positive and negative. It means fewer revenues on one side, but then also more opportunities to sign favorable contracts at higher rates.

Valuation

Ratings Summary (Seeking Alpha)

Both SA analysts and Wall Street are bullish on the company as I think a lot of people have concluded that the new signing of contracts will result in strong earnings growth, which could mean an upswing in the stock price finally as well. The quant rating tells a different story though at a 2.04 rating, indicating a sell. This comes largely from the poor profitability that DO has had the past 12 months, but I don’t think that should be in too much consideration. As I have stated throughout the article, DO is signing new contracts at higher rates which will bring both higher revenues and higher earnings. Old contracts are in a way capping the revenue of DO and creating a ceiling. But DO is breaking through this one contract signing at a time, the latest just a little over a week ago in the Gulf of Mexico for the Ocean BlackLion which will begin in Q3 FY2024 as the old contract runs out and a new one instantly commences with higher rates.

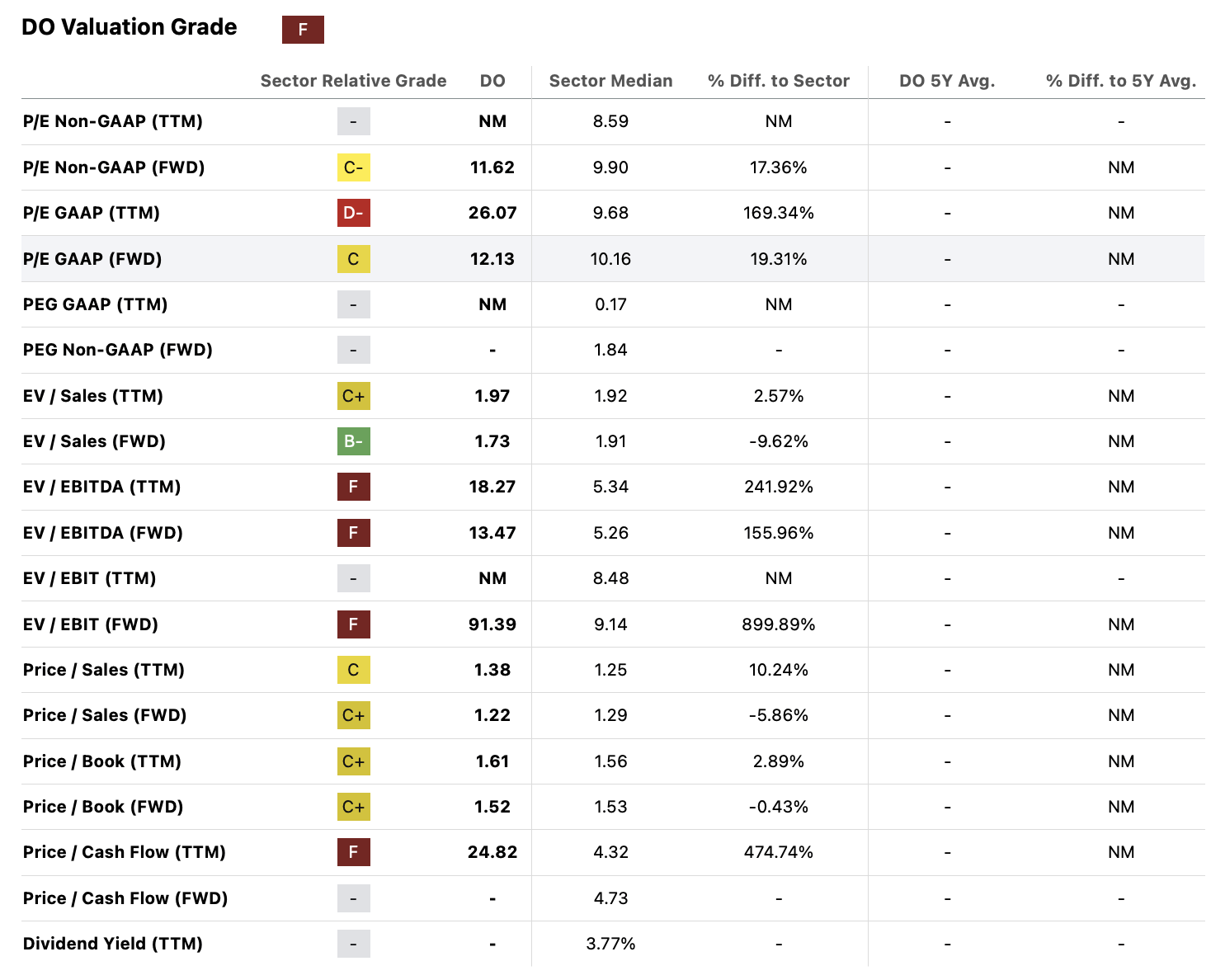

Valuation Grades (Seeking Alpha)

Looking at the valuations it’s hard to base it on historical valuations as DO has largely had a negative operation the past few years following 2020 struggles and bankruptcy filings. The FWD p/e is at 11.62, which is a 17.36% premium to the broader energy sector. DO is expecting 2023 to finish with $135 – $145 million in EBITDA which would be the highest since 2018 when it was $252 million.

The EV/EBITDA is quite high though on a FWD basis at 13.47 still, far above the 5.26 for the sector. Another company I have covered is Valaris Limited (VAL) which works with similar things as DO but with a much larger rig count. Its EV/EBITDA is 36.49 right now, which makes DO not look too bad. What has been diminishing the EV of DO is the trend of taking on more debt, most recently with $500 million in secured senior notes due in 2030. It might be 6 years out, but a higher leveraged balance sheet and operation should result in a lower valuation in my mind.

The EBITDA guidance for 2024 will be crucial to see this next quarter but if the contract is signed with significantly higher rates then I see DO returning potentially to annual revenues of $252 million like in 2018. However, getting some more clarity on this will be needed for me before I rate it higher than a hold.

The Value You Get

The two areas I look at when assessing the value that investors get revolves around a dividend or a buyback program. DO has currently no dividend but had one up until 2015 when it stopped continuing with it. It was paid every quarter. In terms of buybacks, DO has a pretty solid history of doing this, reducing shares from 138 million in 2020 to 101.6 million as of now, totaling a reduction of 36.6% or 9.15% annually. I think that this won’t really continue and during this period DO was also trading over the desk which means it wasn’t fully publicly available to people or institutions either. The value that you get right now can’t be determined as DO would have to prove they can continue with these share reductions if it is to be considered.

Price Target

I stated earlier that in 2025 DO could reach $250 million in EBITDA if they manage to sign favorable contracts this year. At $250 million in EBITDA and no changes in the EV as of now, which is $1.79 billion, would mean a ratio of 7.16. In comparison to the energy which has 5.56 as an average multiple here, DO still exhibits a pretty steep price tag. I would argue that a 6.2x multiple is fair given the growth that DO is estimated to have, and has given proof of achieving as well. If the $250 million grows at 12% YoY by 2027 it would be $350 million. It’s a conservative number perhaps and could be beaten should rates increase even further on average in 2024. With that, the EV/EBITDA is instead 5.1 and leaves an upside of 21.5%. On an annual basis that is 5.37% which isn’t necessarily worth buying into. This would mean a price target of $14.66 and goes in line with my thinking that being more neutral and assessing a hold until more contract clarity is provided along with more robust EBITDA estimates are established makes sense.

The Bear Thesis

The main risk to DO is that the offshore drilling market sees lower demand which would come from lower Capex spending by businesses that are customers of DO. What would trigger this is if interest rates continue to be high and pressure companies’ growth ability. We very recently got a pretty poor inflation report with higher than anticipated results which would make the argument to keep interest rates higher for longer more credible. With that said, DO has a long history of working with its customers so I do expect them not to be cut off completely, offshore drilling is still a very lucrative profitable industry at times to operate in.

State Of The Company

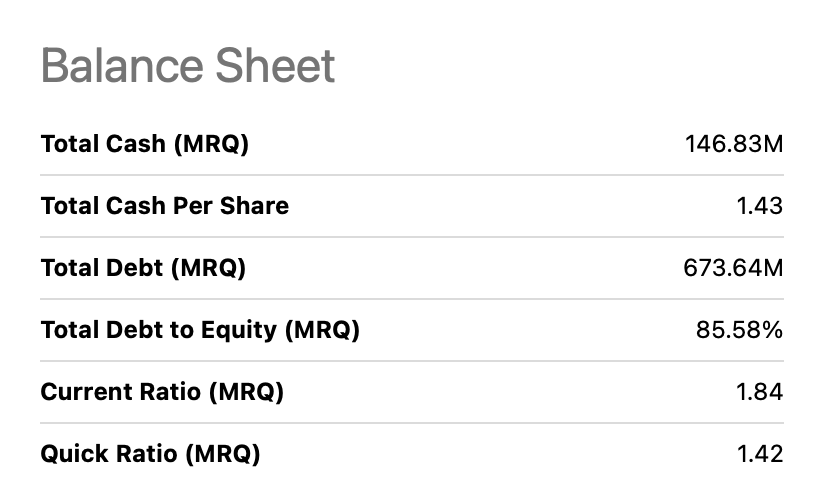

Balance Sheet Highlights (Seeking Alpha)

The balance sheet of DO reveals a cash position of $146 million in comparison to a debt position of $673 million. The current ratio is 18.4 which is incredibly strong, bolstered by the steadily growing cash position. Along with this, the accounts receivables have been climbing as well to $169 million further building up the current assets. This means that total assets have been growing by $300 million since 2021 when DO became publicly traded again. The debt has been trending higher and higher though much from long-term debt and not from capital leases. I would assess the balance sheet of DO to be solid but if the debt rises much faster than this I would start to be worried.

Investment Conclusion

DO comes from a few years of struggle with revenues being capped through having to operate with legacy contracts containing far lower rates than today. This is quickly changing and in 2024 DO seems to be exchanging a majority of the contracts for new and more favorable ones. This should have a positive impact on the revenues and EBITDA. Earnings are around the corner, expected to be released on February 27 after the market closes. The stock has been in a downtrend for the past 6 months as I think most investors are anticipating some market updates for 2024, myself included. I will be assessing DO therefore as a hold.

Q2 2024 Earnings Call Transcript")