JoeLena

Introduction

It’s time to talk about a company I made a core position in my dividend growth portfolio in early January. That company is Antero Midstream (NYSE:AM), the Colorado-based owner of midstream assets used by Antero Resources (AR), one of America’s largest natural gas producers.

On December 24, I wrote an article titled Dividend Investors Take Note! 7%-Yielding Antero Midstream Is One Of My Favorites For 2024.”

As the title suggests, I explained what makes Antero Midstream such a fantastic high-yield dividend stock.

Here’s a part of the takeaway:

Supported by Antero Resources, AM benefits from stable, long-term contracts, insulating it from commodity price risks.

Its strategic expansions, coupled with a robust financial performance, signal a return to dividend growth in 2024.

With a current 7.1% yield and promising free cash flow projections, AM presents a rare combination of high yield and growth prospects.

The reason I’m writing an update is the fact that the company just reported its earnings.

Usually, earnings aren’t that spectacular in the midstream business. However, the company revealed a ton of valuable intel, including strong free cash flow generation, used to reduce debt and buy back stock.

After I started buying AM rather aggressively earlier this year, I decided to buy even more, as we are dealing with a unique investment opportunity.

Not only does AM offer a well-covered 7% yield, but it also has the ability to aggressively hike this dividend in the years ahead, supported by buybacks and debt reduction.

It also benefits from consistent growth thanks to its relationship with Antero Resources and strong fundamentals in the natural gas liquids (“NGL”) market.

Although some of my AM titles may sound like clickbait, I am very serious when I say that I consider AM to be one of the best high-yield investments on the market, with tremendous total return potential.

So, let’s get to it, as we have a lot to discuss!

Better Times For Midstream Companies

As I often mention in articles, generally speaking, I am not a huge fan of high-yield investments.

Not only do I have an expected time horizon of many decades for my investment, but I also believe that the high-yield space is full of pitfalls.

So many stocks with juicy rates come with elevated risks, including risks of long-term underperformance.

The midstream space is one of the areas where investors have encountered turmoil in the past.

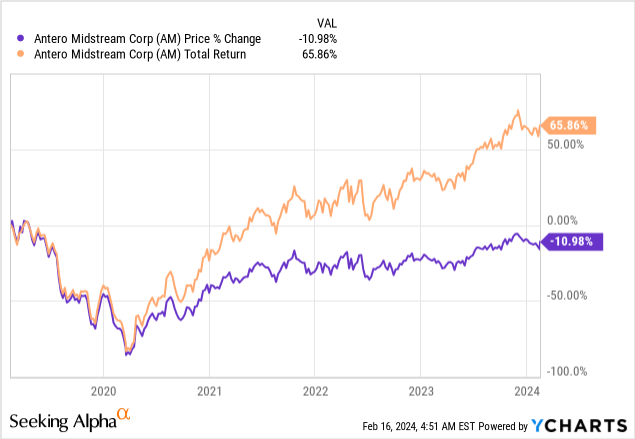

As the AM chart above shows, during the pandemic years, AM investors went through a massive sell-off, which also came with a dividend cut.

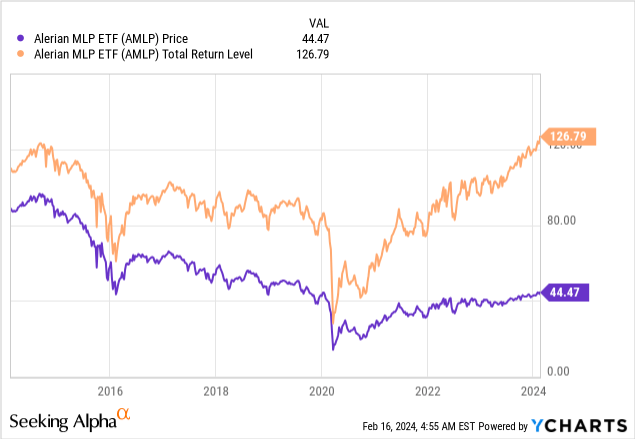

Looking at the chart below, we see that Alerian MLP ETF (AMLP), an ETF tracking midstream Master Limited Partnerships, has been through two major sell-offs, one in 2015 and one during the pandemic.

Also, until 2021, the overall performance of MLPs was just poor.

The problem was that midstream companies had to invest billions in expanding their asset base to provide upstream companies with opportunities to boost production. The U.S. saw massive fossil fuel production growth between the Great Financial Crisis and the 2020 pandemic.

Eland Cables

This resulted in significant capital requirements, often funded by debt.

When oil and gas prices imploded in 2015 and 2020, investors wanted nothing to do with midstream companies, fearing a situation would occur where upstream producers would reduce output, leaving midstream companies with expensive debt and lower revenues.

The good news is that we are now in a totally different environment!

Most midstream companies have mature business models with lower capital requirements and strong income from past investments.

Even if the economy were to enter a recession again, most midstream companies are much stronger, which makes a third massive sell-off very unlikely.

Having said that, before I continue, it is important to mention that Antero Midstream is not a Master Limited Partnership. It is one of the few midstream companies that is taxed like a regular C-Corp, which makes it easier for foreign investors like me to invest in them.

I’m Impressed By AM’s Numbers

The company’s just-released 4Q23 earnings gave us a lot of valuable info that not only confirmed my thesis but also shed some light on favorable long-term developments.

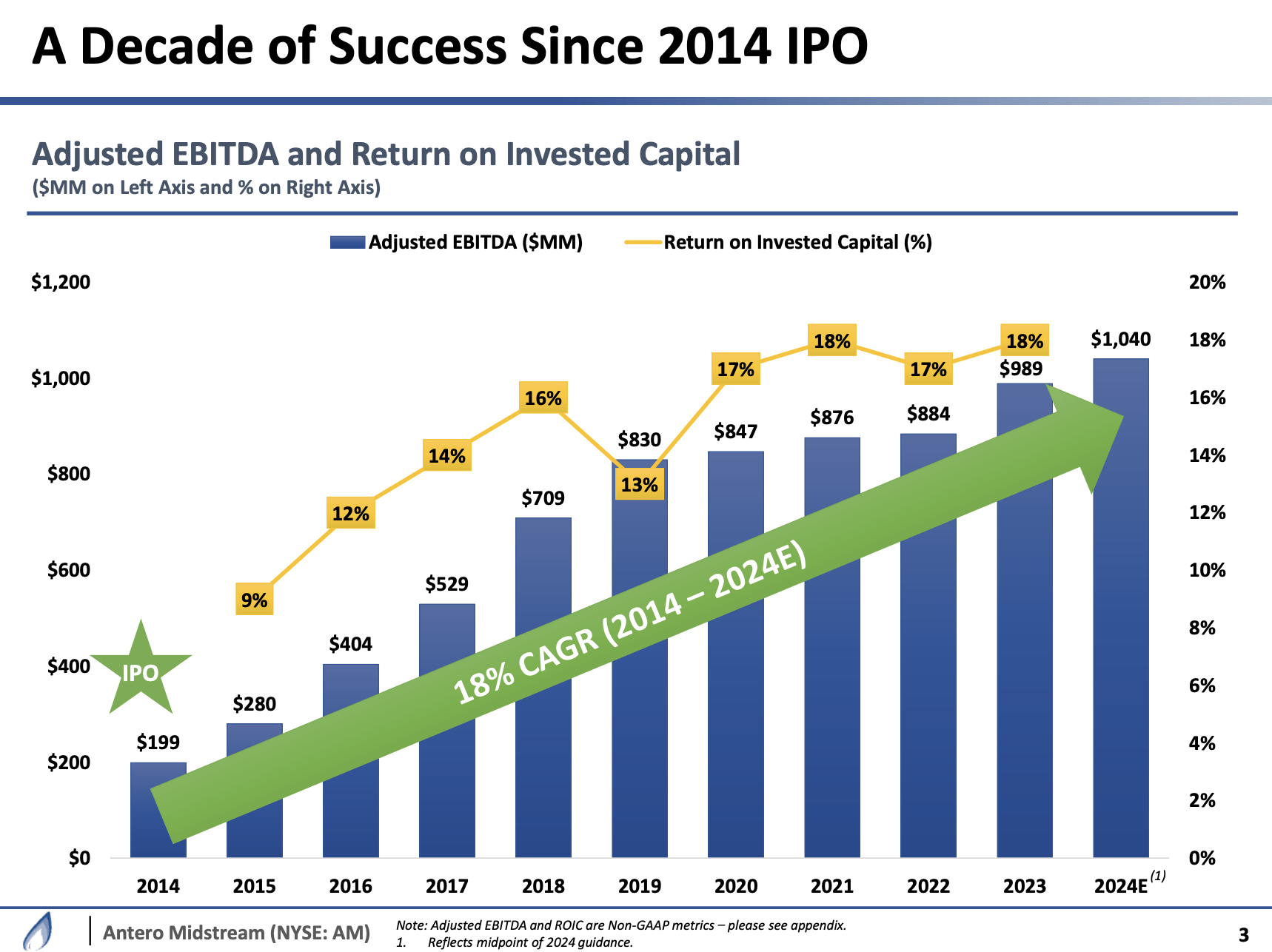

For example, the company started its earnings call by highlighting that since its initial public offering in 2014, it has demonstrated robust financial and operational performance.

In 2023, the company achieved a record $981 million in EBITDA and an 18% return on invested capital (“ROIC”), which, according to the company, underscores its operational expertise.

Despite temporary struggles, over the years since its IPO, the company has maintained an impressive 18% compound annual growth rate in EBITDA, indicating sustained success and value creation for shareholders.

Antero Midstream

A key factor contributing to this success is Antero Midstream’s close partnership with Antero Resources, one of the largest exploration and production (E&P) operators in North America.

The synergy between the two companies has enabled Antero Midstream to gain valuable insights into Antero Resources’ development plans, thereby optimizing its operations and capital allocation strategies.

Antero Resources has a 29% ownership interest in Antero Midstream, which makes this cooperation even closer.

Going into this year, AM owned more than 400 miles of low-pressure pipelines, 230 miles of high-pressure pipelines, and 4.5 billion cubic feet of compression capacity to support AR’s operations.

It also has a huge water business, consisting of close to 380 miles of water pipelines.

Thanks to the AR-AM connection, AM does not have competitors, except if it were to decide to grow more rapidly with other customers.

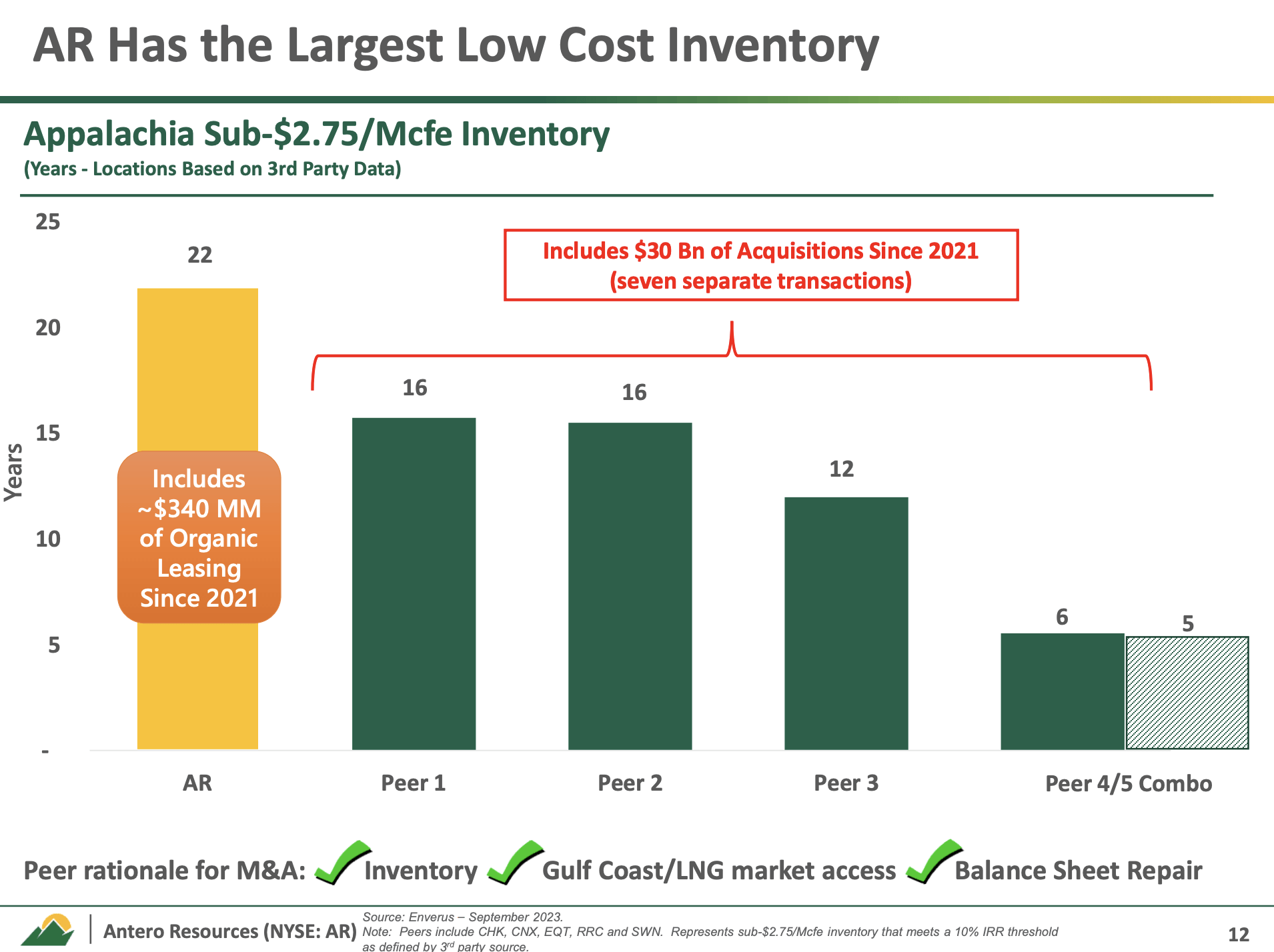

Furthermore, AR has more than 20 years worth of low-cost inventory, which allows the company to produce natural gas when other players are forced to reduce output due to pricing headwinds.

This adds a lot of safety to the AM thesis.

Antero Resources/Antero Midstream

Going back to its performance, in the fourth quarter of 2023, the company achieved record-breaking financial results, with $254 million in EBITDA, marking a 10% increase compared to the previous year.

Additionally, the company generated $156 million in free cash flow before dividends, with $48 million after dividends.

During the same period, the company saw significant increases in low-pressure gathering and compression volumes, rising by 10% and 14%, respectively, compared to the previous year.

These metrics set new company records, indicating strong operational performance and efficiency.

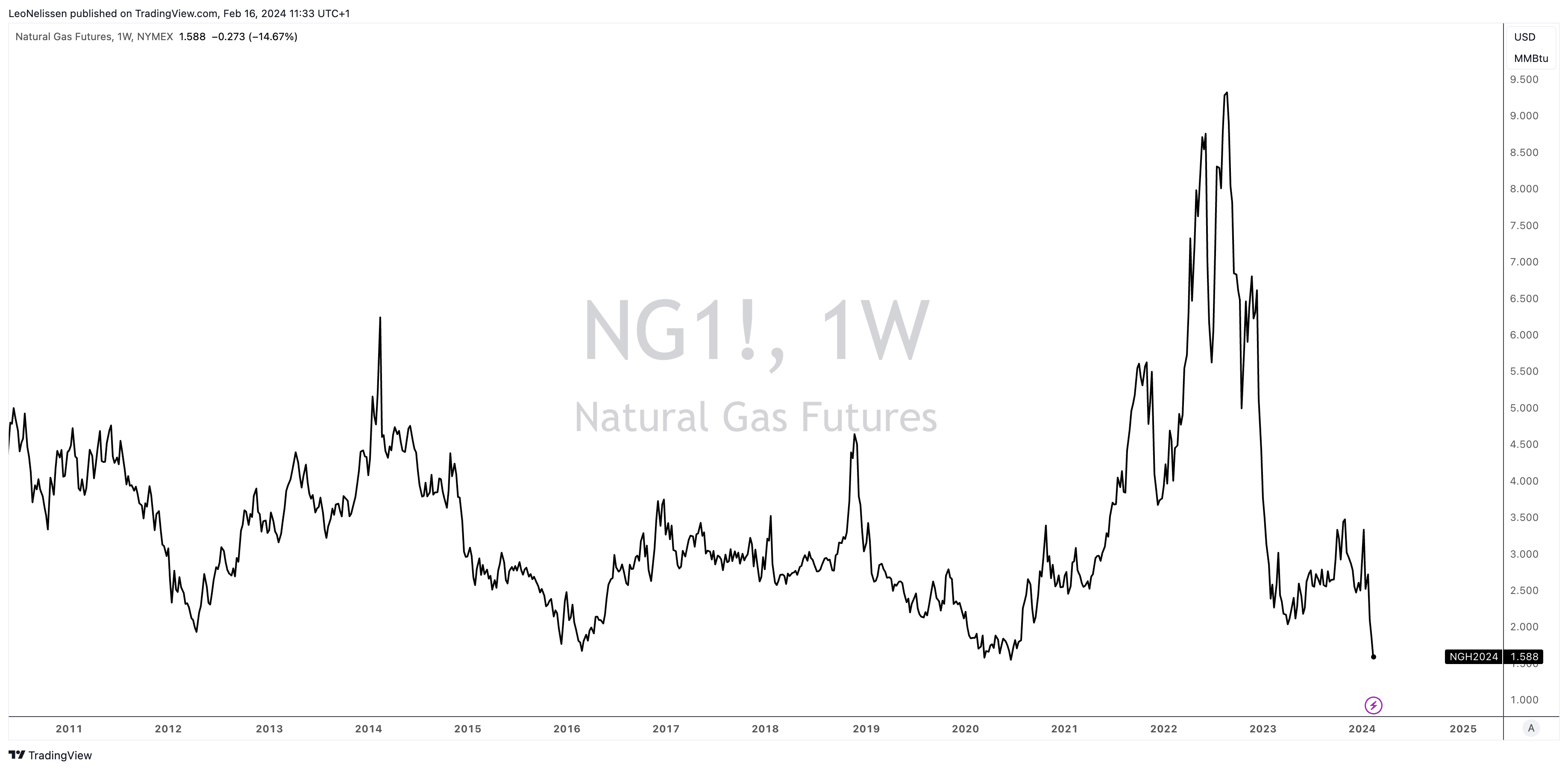

In other words, with natural gas prices having imploded recently, these numbers show the benefit of owning midstream assets, as income is related to product flows, not the pricing of underlying commodities.

TradingView (NYMEX Henry Hub Futures)

Furthermore, the company is in a fantastic spot to generate elevated shareholder returns for many years to come.

Future Growth & Shareholder Value

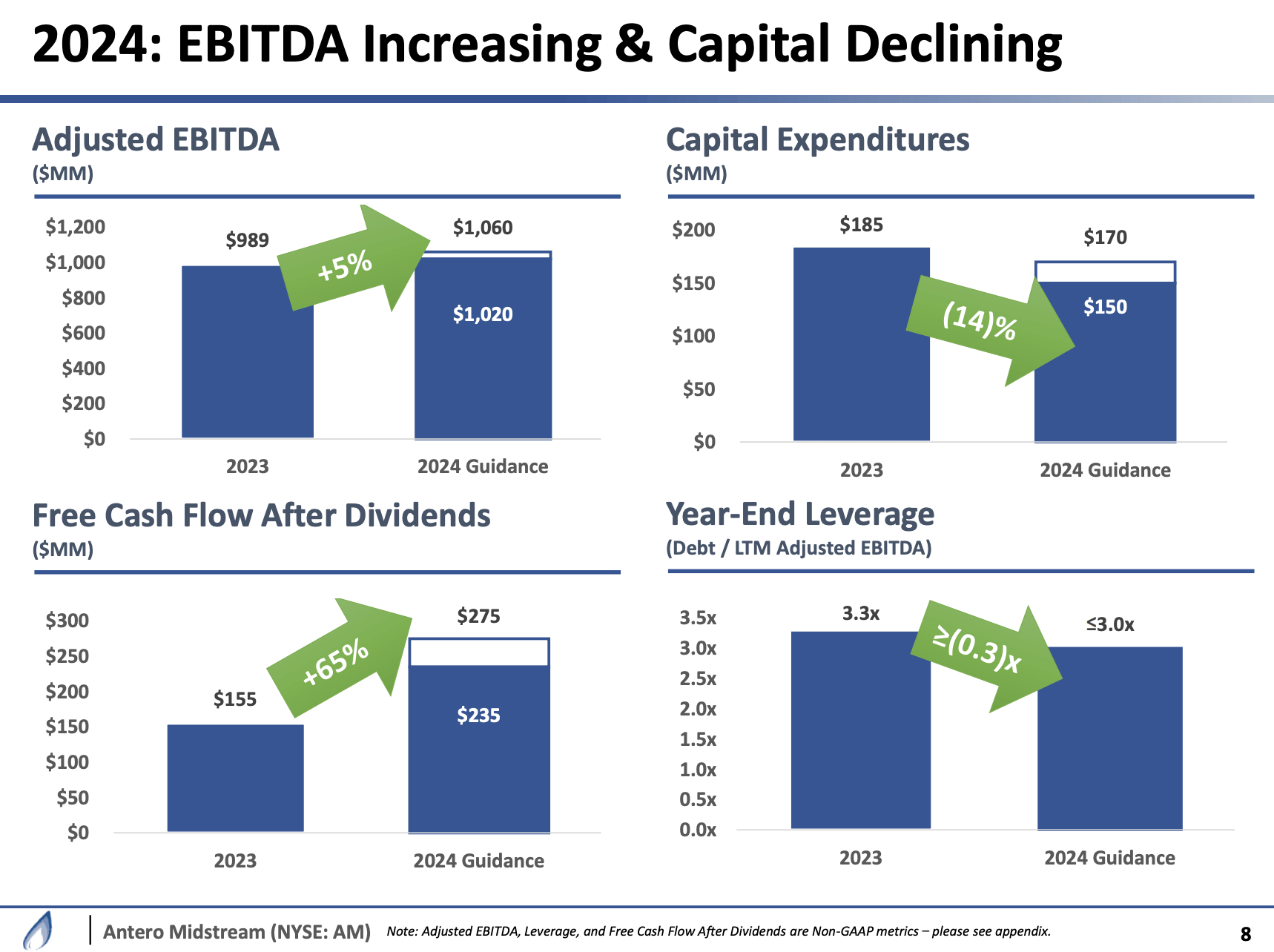

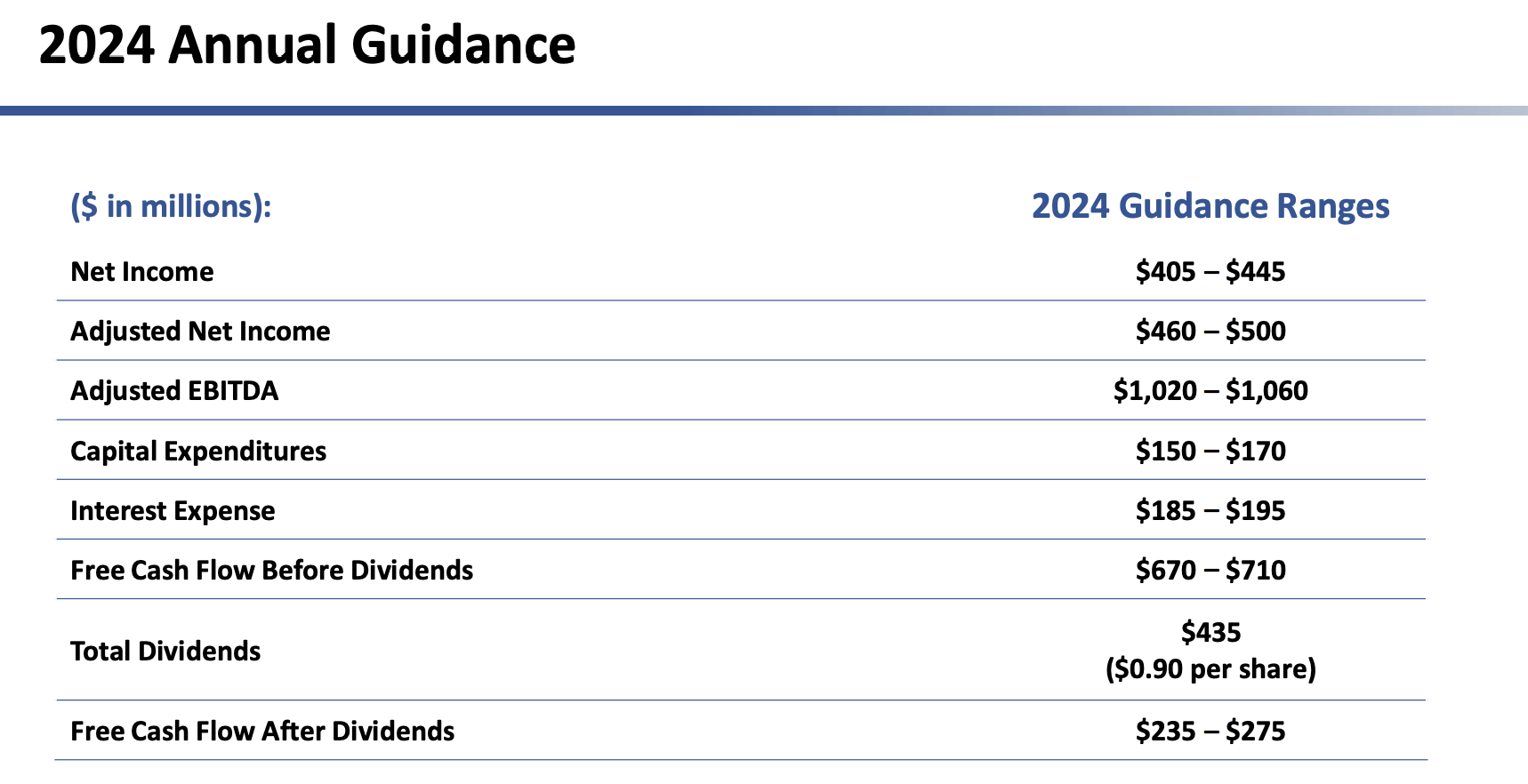

Looking ahead to 2024, Antero Midstream anticipates continued financial growth and stability.

The company is guiding towards $1.1 billion in EBITDA for the year, reflecting a solid performance driven by a maintenance capital program at Antero Resources.

Antero Midstream

This capital program is designed to optimize capital efficiency and generate a high teen ROIC.

In terms of capital allocation, Antero Midstream plans to invest between $150 and $170 million in capital expenditures for 2024.

The majority of these investments will be directed towards the Marcellus liquids-rich midstream corridor, underscoring the company’s strategic focus on maximizing value from its core assets.

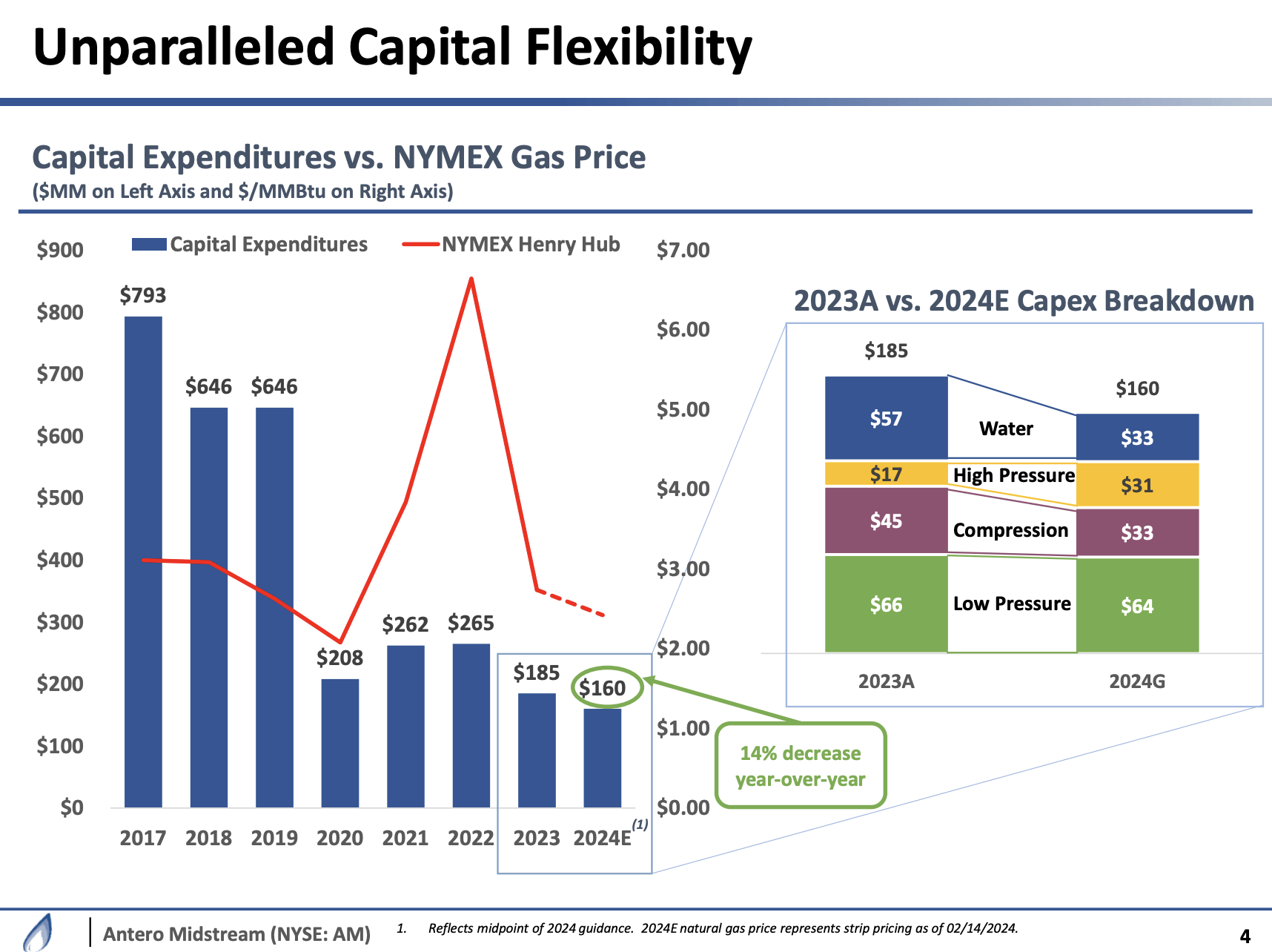

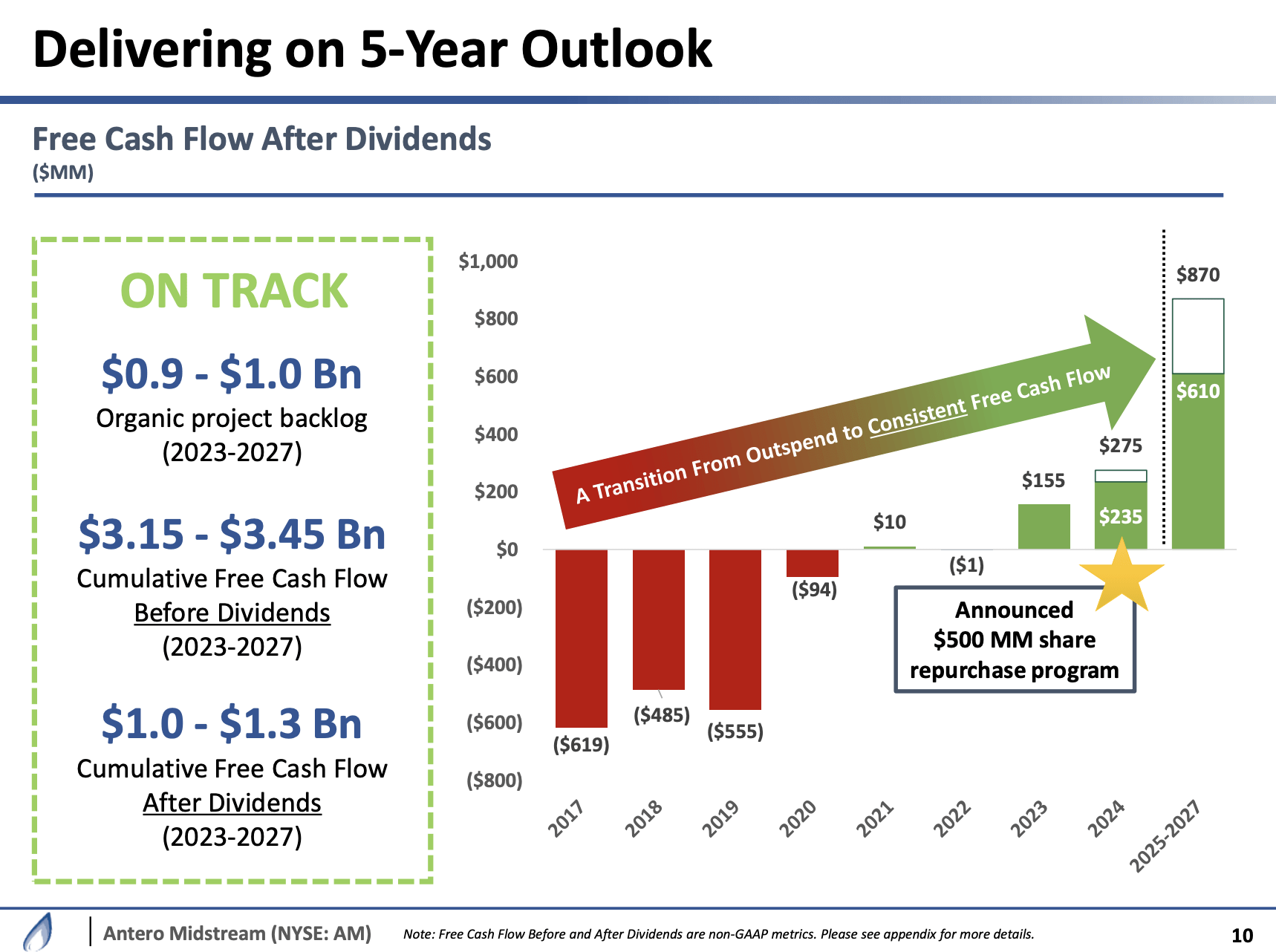

As we can see below, after many years of aggressive investments, the company is now moderating its CapEx, which bodes well for free cash flow.

The midpoint of the 2024 CapEx range is 14% below the prior-year number.

Antero Midstream

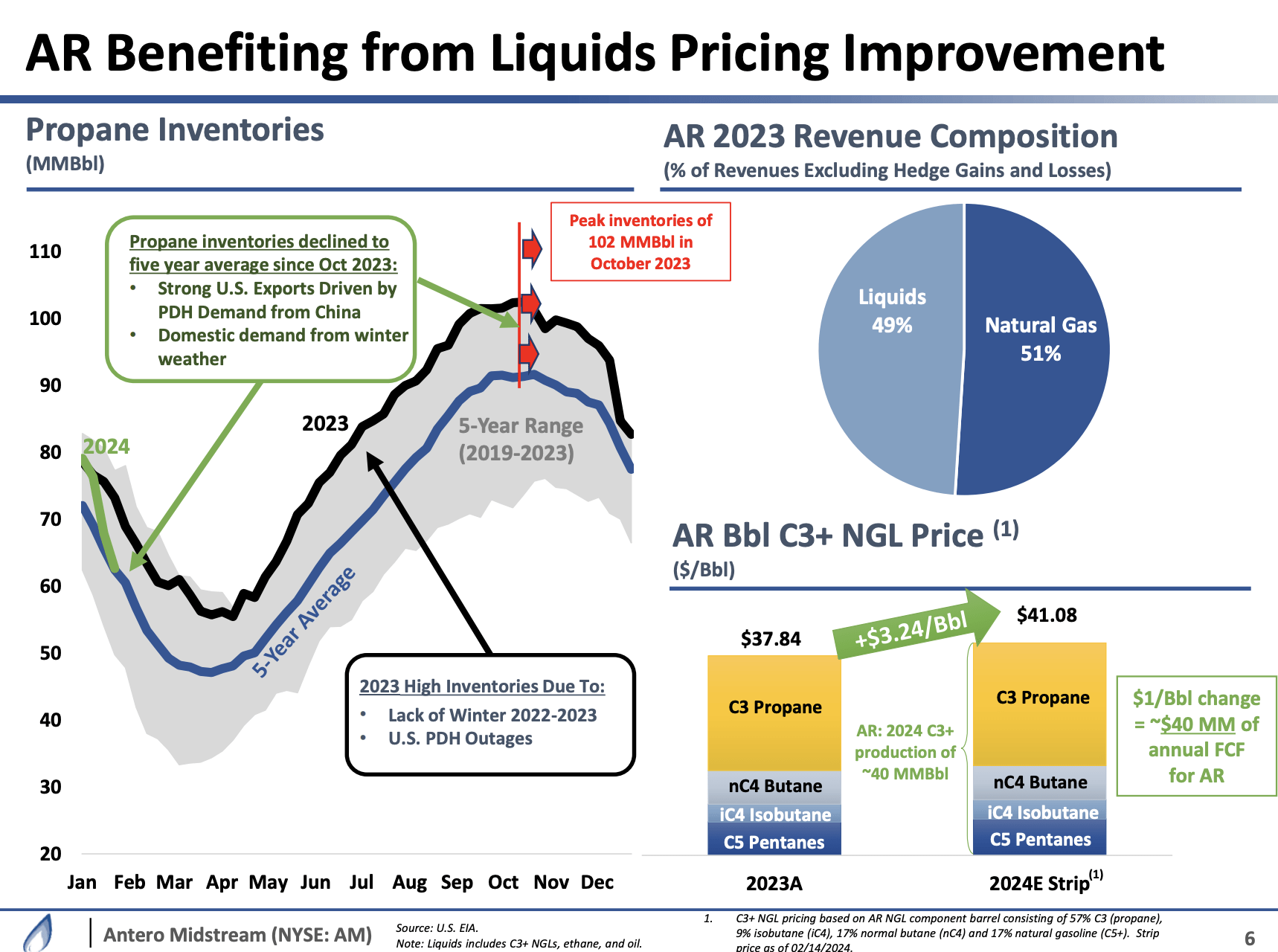

With that said, despite the current weakness in natural gas prices, Antero Midstream stands to benefit from improvements in liquids pricing, particularly in propane, which plays a significant role in its revenue stream.

According to Antero Midstream, strong exports and winter weather have led to a tightening of the propane market, driving bullish sentiment in propane prices.

This pricing uplift uniquely benefits Antero Midstream due to its exposure to liquids, including natural gas liquids (“NGL”). After all, roughly half of AR’s revenue comes from higher-margin products.

The company expects each dollar-per-barrel change in C3+ NGL pricing to result in approximately $40 million of incremental free cash flow.

This additional cash flow, combined with reduced maintenance capital at Antero Resources, helps offset the impact of declining natural gas prices and supports a stable development plan for the company.

Antero Midstream

Overall, Antero Midstream’s ability to capitalize on improvements in liquids pricing enhances its financial resilience and reinforces its position as a leading player in the midstream sector.

This is a huge pro for the company!

But wait, there’s more!

This year, the company plans to maintain a stable dividend of $0.90 per share, representing an attractive 7.3% yield at current share prices.

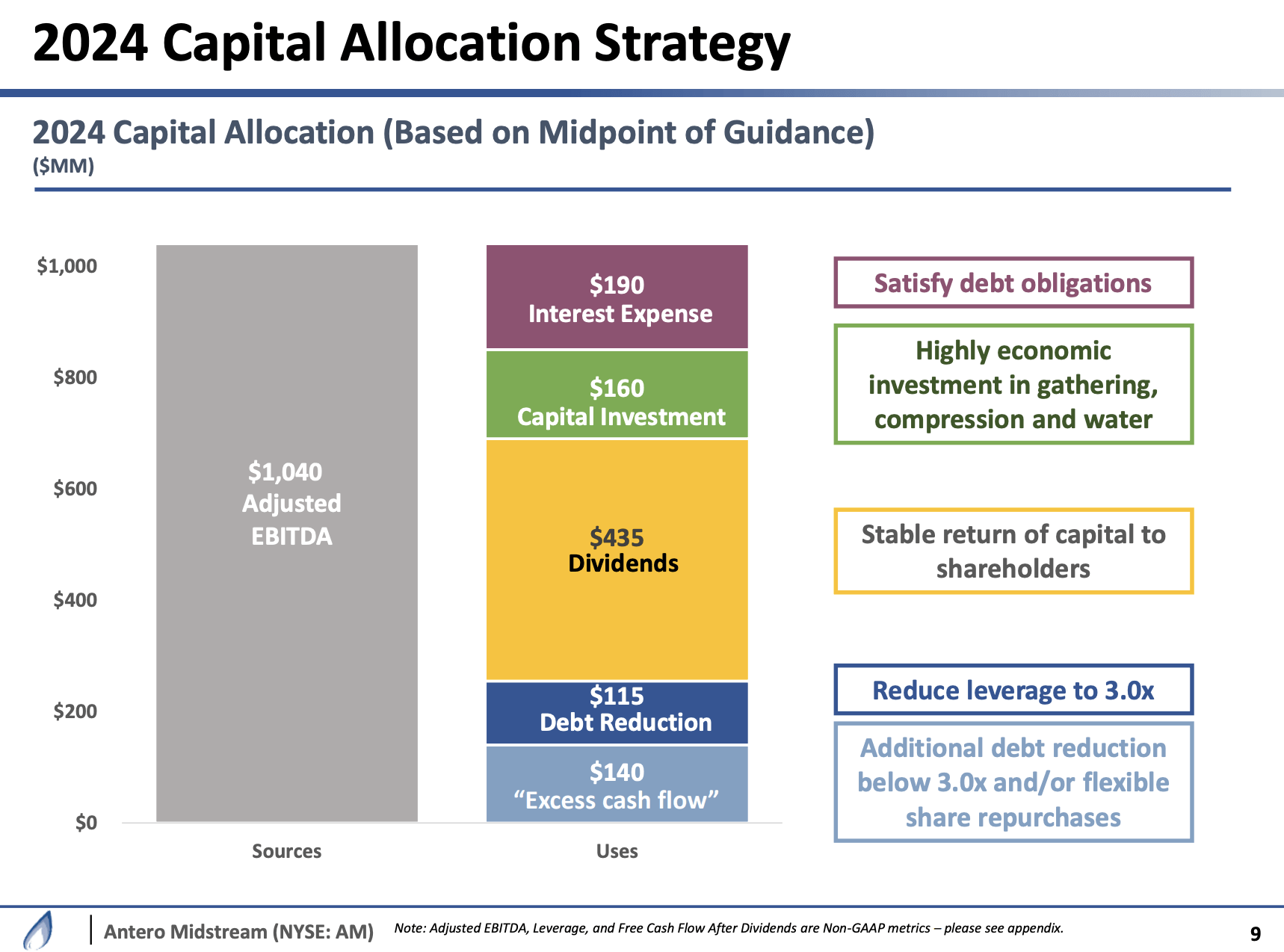

Any excess cash flow will be directed towards debt reduction to achieve a target leverage ratio of 3x by the end of 2024, followed by opportunistic share repurchases under a new $500 million open market share repurchase program.

In other words, the company is expected to reach its target leverage this year and use additional cash to buy back stock. It is now one of the few high-yield plays that also comes with buybacks!

In the case of Antero Midstream, $500 million in buybacks translates to 8.4% of its market cap, which is a big deal.

Furthermore, this year, the company is expected to generate between $670 and $710 million in free cash flow ($690 million midpoint). It expects to need $435 million to service its dividend.

After dividends, it will likely generate between $235 and $275 million in free cash flow ($255 million midpoint).

- These numbers indicate a 2024E dividend coverage ratio of 159% or a payout ratio of 63%.

- Post-dividend FCF is expected to be 4.3% of its market cap.

Antero Midstream

Next year, analysts expect the company to boost free cash flow to $700 million, potentially followed by a surge to $750 million in 2026.

These numbers indicate a free cash flow yield of 12% and 12.7%, respectively.

In other words, after the company reaches its debt target, it can start hiking its dividend again and deploy additional cash for buybacks.

Given that the company can potentially distribute more than 12% of its market cap, investors are in for a surge in distributions in the years ahead!

Below, we see the visualization of 2024 capital spending. Once the company hits its 3.0x leverage ratio, the dark blue field labeled “debt reduction” will likely turn into “excess cash flow.”

Antero Midstream

With that in mind, despite potential challenges posed by volatile commodity prices, the company remains committed to achieving its 5-year targets from 2023 through 2027.

With a highly economic organic project backlog of $900 million to $1 billion, the company expects to sustain a high teen return on invested capital and generate $1.0 billion to $1.3 billion of free cash flow after dividends.

The aforementioned buyback program aims to deploy roughly half of the free cash flow of its five-year program through 2027.

Antero Midstream

So, what does this mean for its valuation?

Valuation

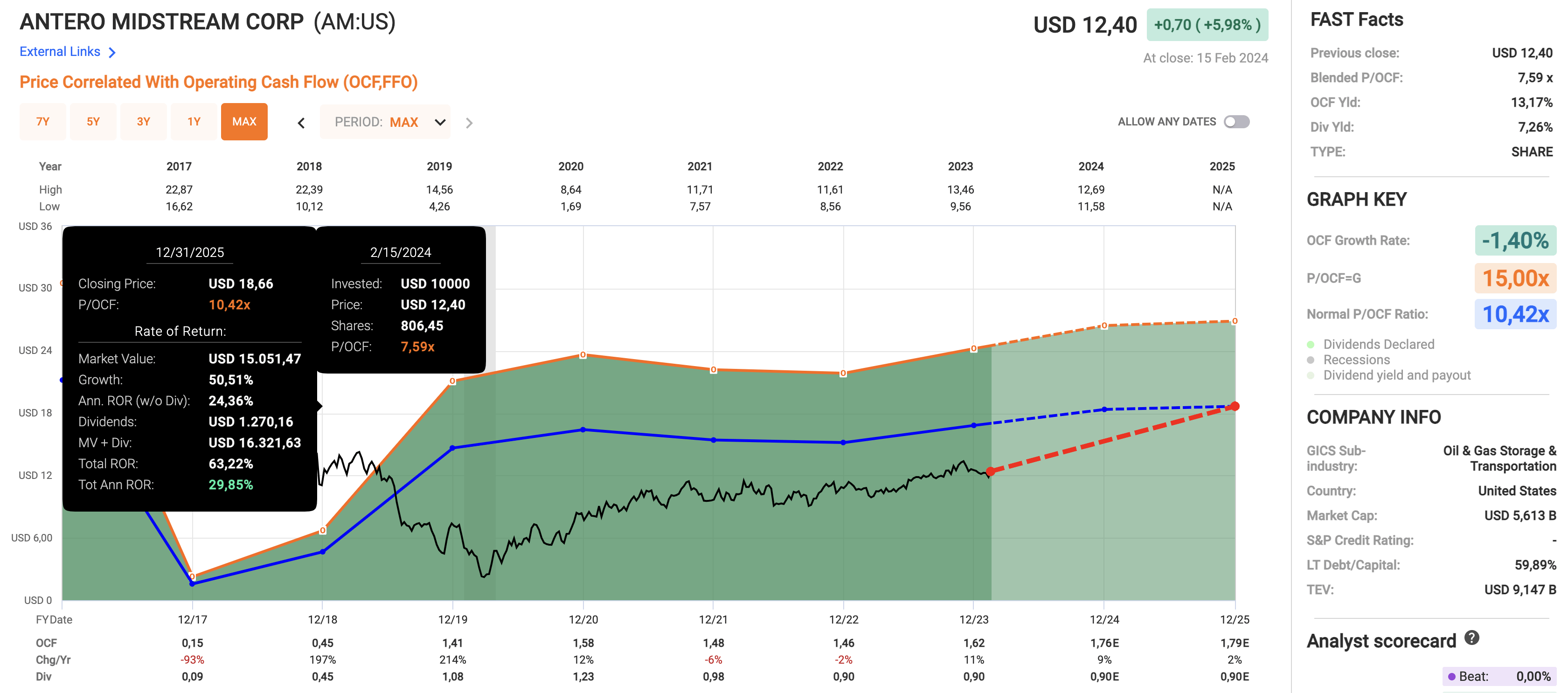

In addition to offering an attractive yield and strong future dividend growth potential, I believe that AM is very cheap.

Using the data in the chart below:

- Antero Midstream is trading at a blended P/OCF (operating cash flow) ratio of just 7.6x, which is below its normalized long-term multiple of 10.4x.

- This year, analysts expect OCF to grow by 9%, potentially followed by 2% growth in 2025.

- As such, the company would have room to run to more than $18 per share, which is 45% above its current price.

FAST Graphs

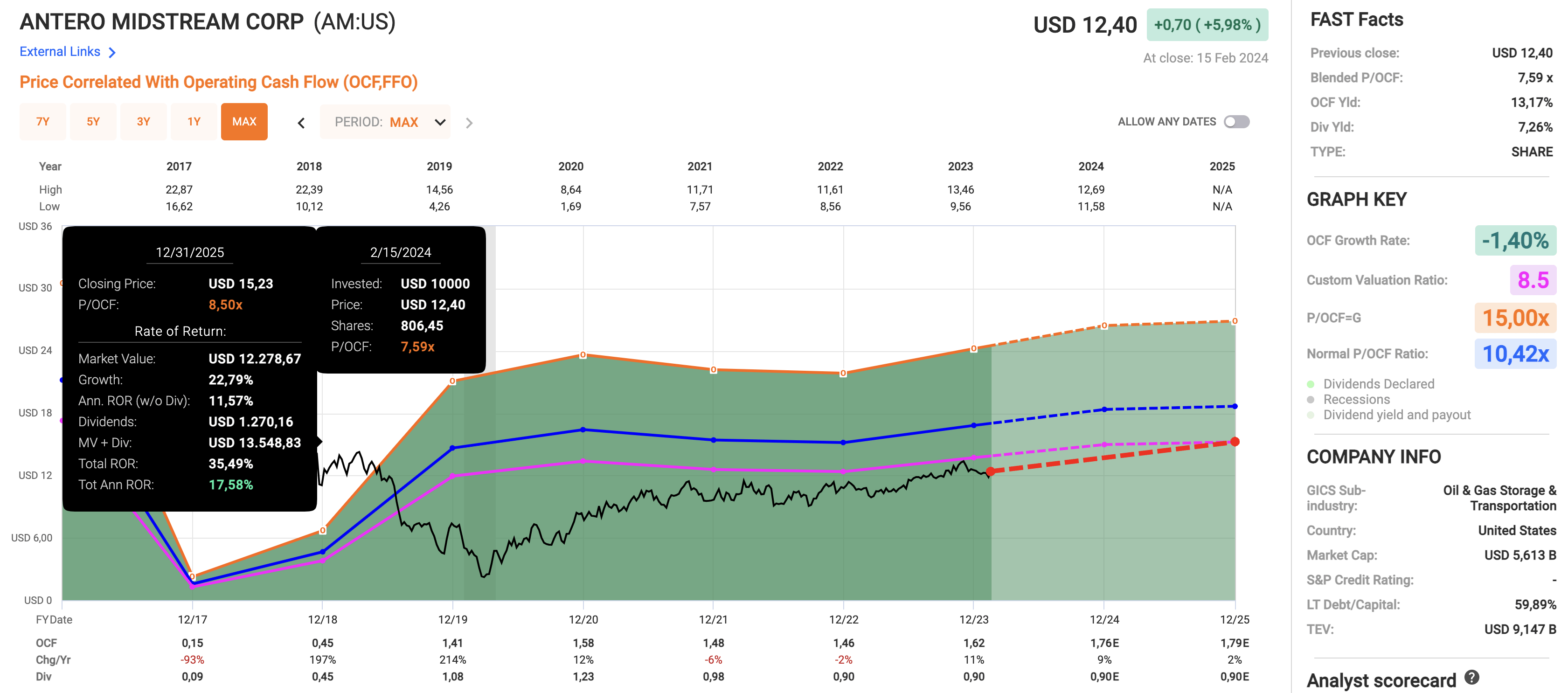

Even if I apply a much lower 8.5x OCF multiple, the stock has a fair value of $15.20, 23% above the current price.

FAST Graphs

All things considered, my thesis remains in great shape, which is why I am looking to expand my already large position in AM and buy it for income-focused family accounts.

On a long-term basis, I expect AM to leave most other high-yield stocks in the dust, as it benefits from a well-protected 7% yield, plenty of free cash flow growth, and a strong underlying business and relationships with Antero Resources.

Takeaway

Antero Midstream continues to impress with its robust financial performance and strategic position in the midstream sector.

Supported by stable, long-term contracts and a close partnership with Antero Resources, AM stands out as a high-yield investment opportunity with promising growth prospects.

The recent earnings report further solidifies AM’s potential, with strong free cash flow generation and a focus on debt reduction and share buybacks.

Despite past industry challenges, AM’s resilient business model and strategic initiatives position it for sustained success.

With an attractive dividend yield, projected free cash flow growth, and compelling valuation, AM represents a compelling investment for income-focused investors seeking long-term value.

In my view, AM stands out as one of the best high-yield stocks in the market, poised for significant total return potential in the years ahead.

Pros & Cons

Pros:

- High Yield: With a current yield of 7.3%, AM offers an attractive income opportunity for dividend-focused investors.

- Stable Contracts: AM benefits from stable, long-term contracts, reducing exposure to commodity price volatility.

- Strong Financial Performance: Record-breaking earnings and free cash flow generation demonstrate AM’s financial resilience and operational efficiency.

- Strategic Partnerships: The close partnership with Antero Resources provides valuable insights and supports AM’s growth and capital allocation strategies.

- Potential for Dividend Growth: Supported by buybacks and debt reduction, AM has the potential to increase its dividend in the future, enhancing shareholder returns.

Cons:

- Industry Volatility: Despite recent improvements, the midstream sector remains prone to steep(!) commodity price declines and regulatory challenges.

- Dependence on Antero Resources: AM’s close relationship with Antero Resources poses a risk if Antero encounters operational or financial difficulties.

- Market Sentiment: Negative market sentiment towards high-yield stocks may impact AM’s share price, potentially leading to short-term volatility.

- Competition: While AM benefits from its exclusive relationship with Antero Resources, it may face challenges in expanding its customer base and diversifying its revenue sources.

Q2 2024 Earnings Call Transcript")