digicomphoto/iStock via Getty Images

Dear readers,

Alexandria Real Estate Equities (NYSE:ARE) is a blue-chip REIT focused on leasing exclusively to life science tenants in biotech and big pharma. The REIT has generated impressive shareholder returns since going public in 1997 and continues to deliver growth year after year with a 10-year FFO per share CAGR of 7.4%.

Last year, the stock price plummeted on fears that life science is not that different from office and may experience occupancy issues. I addressed this (main) bear argument in my article called Why The Bears Are Wrong. In short, I saw the fear as vastly overblown and ARE became one of my high conviction buys with a position size of about 5% and a break-even at $119 per share.

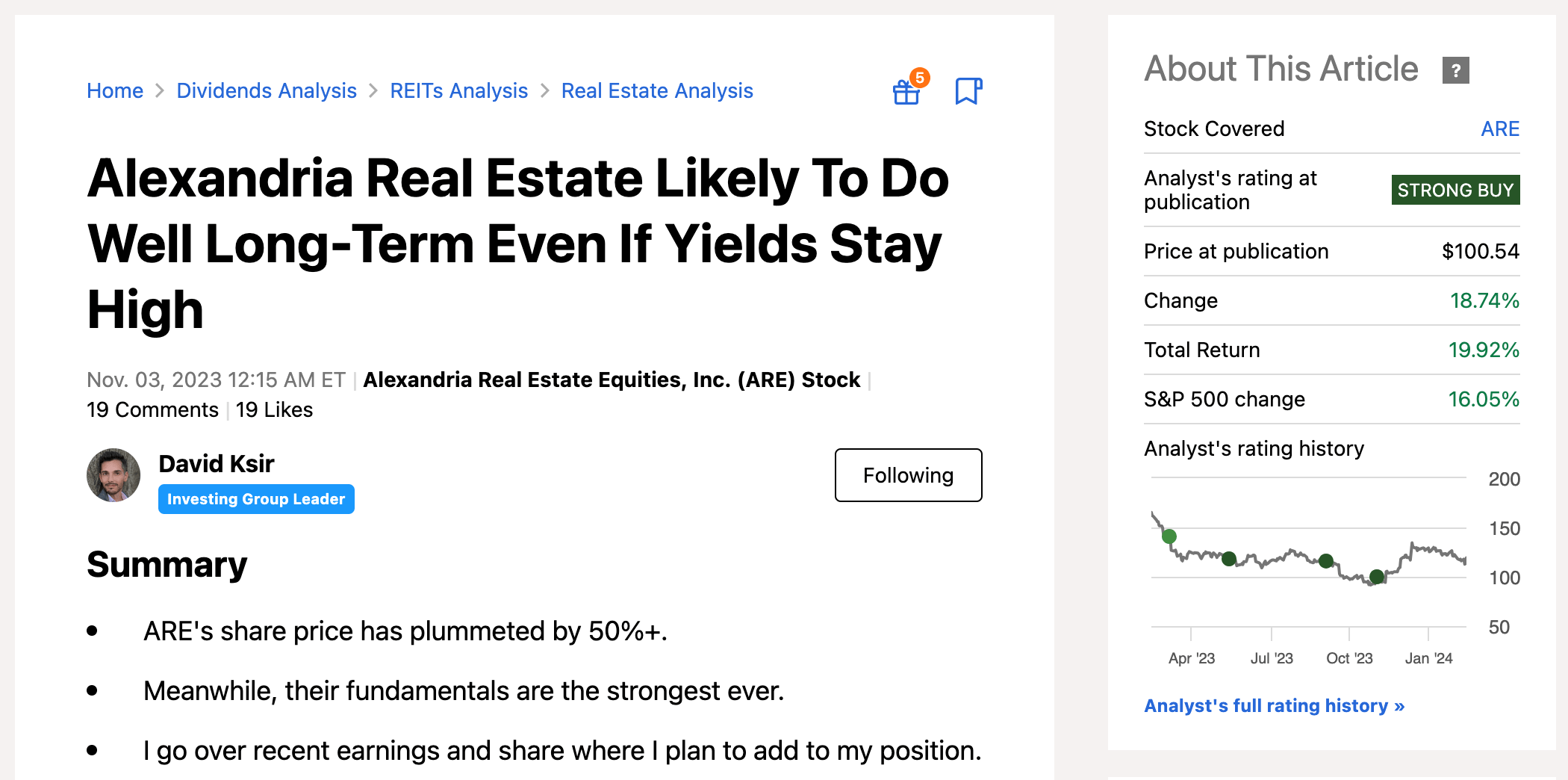

Most recently, I covered the stock in early November (with a STRONG BUY rating) and argued that ARE was very well positioned to tackle the second bear argument – high rates. My thesis was supported by its ability to grow rents rapidly and a long-duration balance sheet with predominantly fixed rate debt, which combined result in very resilient (and growing) cash flow.

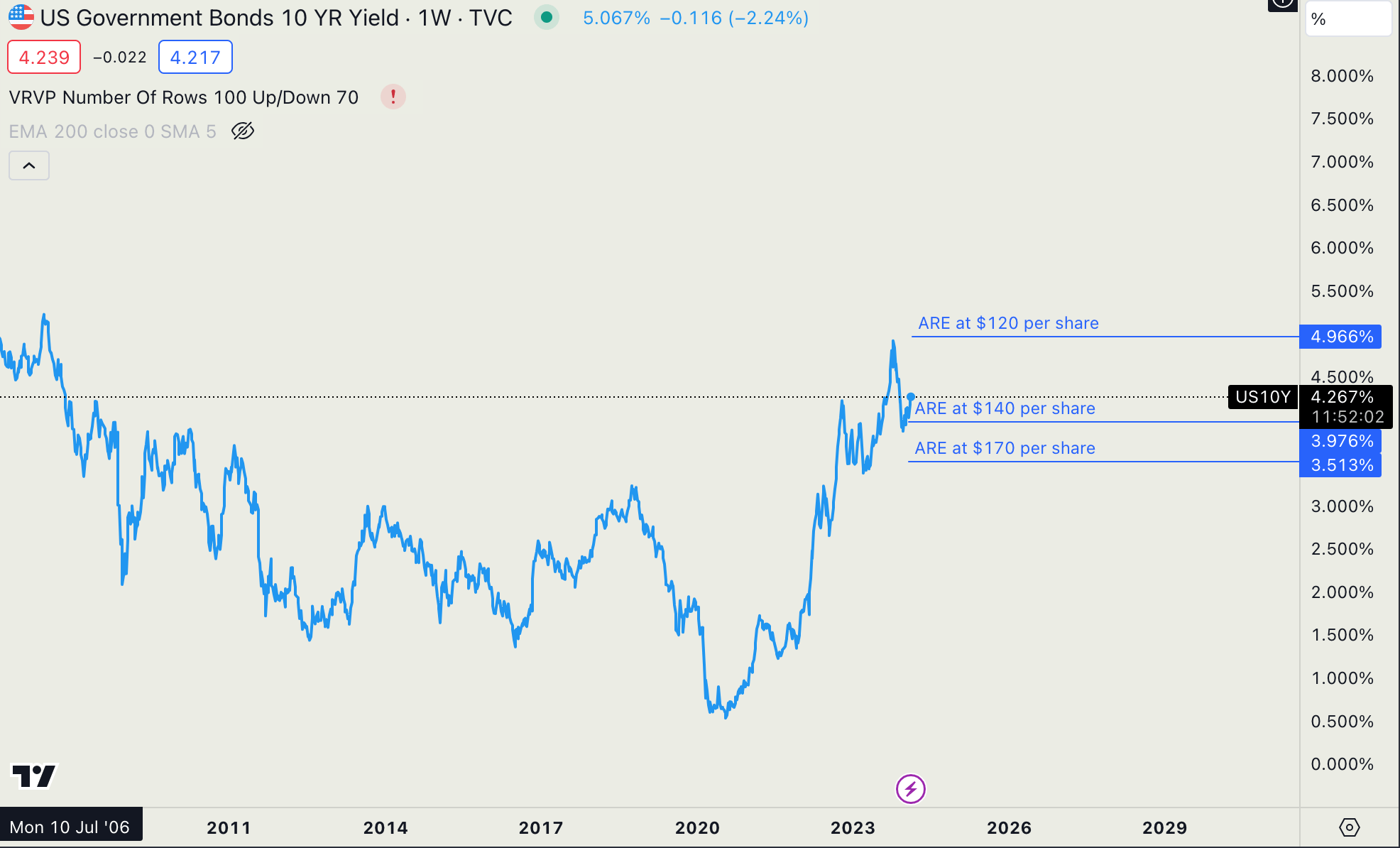

Since my last article, interest rate pressures have eased slightly as the 10-year yield dropped from about 4.7% to 4.2% today. Consequently, ARE’s price increased from $100 per share to $120 today, an RoR of 20%, slightly above the return of the S&P 500 (SPX).

Seeking Alpha

ARE has also released very good Q4 2023 results which reaffirm a lot of the positives I’ve been writing about. Therefore, I continue to see substantial upside potential to my price target of $170 per share. In this article, I want to go over the most recent earnings report from January 30th and present my outlook for the stock given current interest rate expectations.

Latest results reaffirm ARE’s operational strength

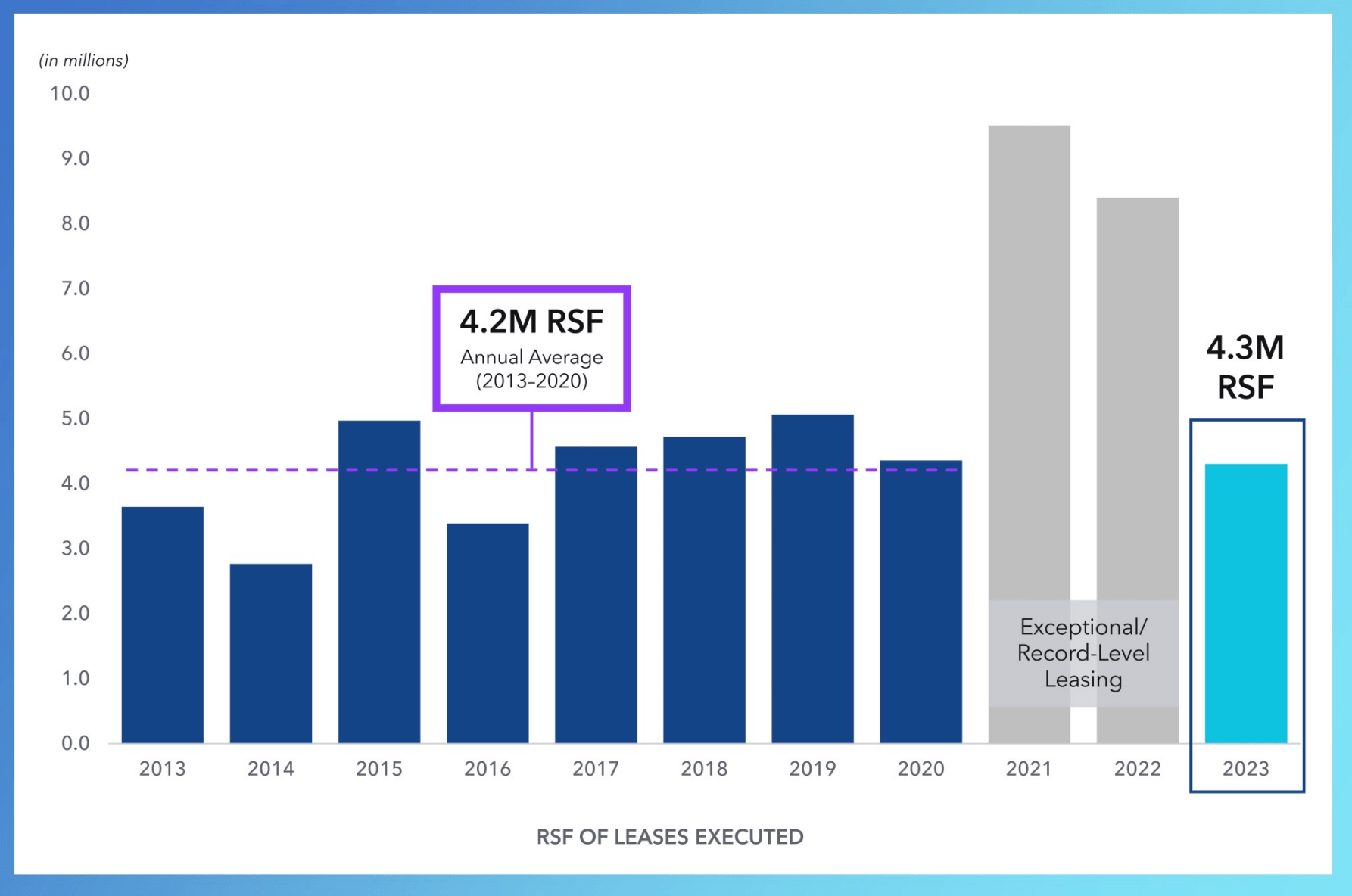

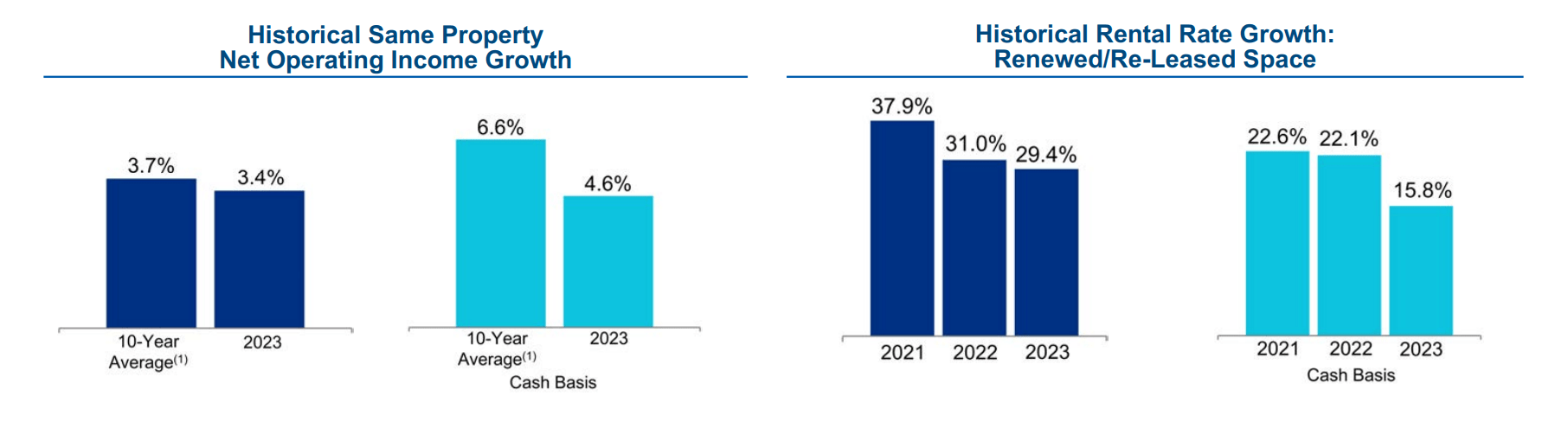

During the last quarter of 2023, ARE has continued to maintain near perfect rent collections of 99.9% and ended the year with a solid occupancy of 94.6%, in line with historical averages. This was supported by high leasing volumes which reached 4.3 Million sft, in line with the annual average between 2013 and 2020. Notably, the leases executed in 2023 had an exceptionally long weighed average lease term of 11.3 years which was above the 10-year rolling average of 8.8 years. Not only that, but leases were also executed at significantly higher prices with rent spreads on renewed/re-leased space at 29.4% (and 15.8% on a cash basis) in 2023. Once again, ARE’s ability to lease space for substantially longer periods and high rents is a clear sign that tenants continue to value their space and have little intention of downsizing their operations.

ARE IR

High rent spreads have contributed 3.4% YoY growth in same store NOI, more or less in line with the 10-year average. Going forward, NOI (and FFO) are likely to continue to grow quite rapidly thanks to a combination of:

- high build in rent escalators in 96% of leases that average 3% per year

- high re-leasing rent spreads which can easily add 1-1.5% growth each year

- a strong development pipeline

ARE IR

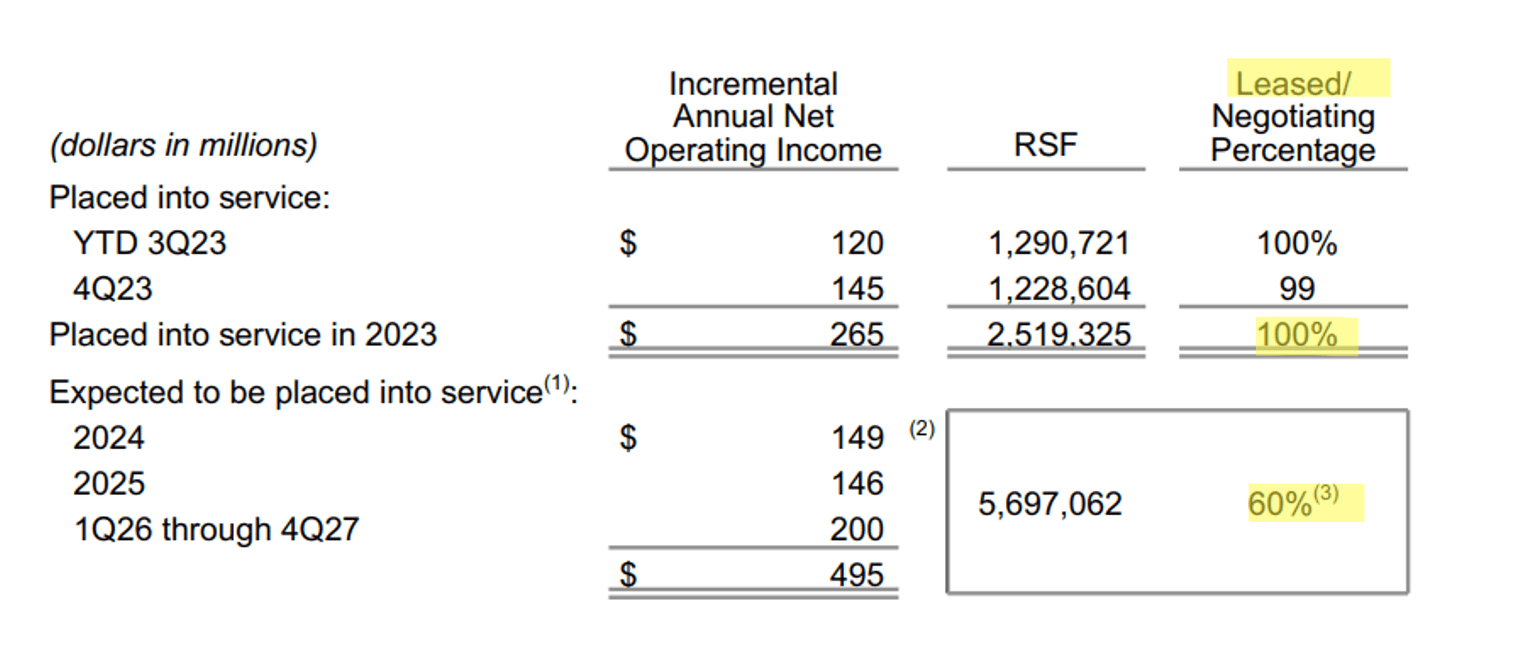

ARE’s development pipeline is arguably second to none. During the fourth quarter, the company started operation of 1.2 Million sft of space and, for the full year, 2.5 Million sft were placed into service. Importantly these new portfolio additions were fully leased from day one and will add $265 Million in incremental annual NOI. This year and beyond, a similar pace is expected with about $150 Million in incremental NOI generated each year through new development projects, which is highly visible thanks to 60% of space already under contract. The pipeline is likely to help ARE grow its NOI significantly above the 4-4.5% generated by internal rent growth which should translate to some FFO per share growth as well.

ARE IR

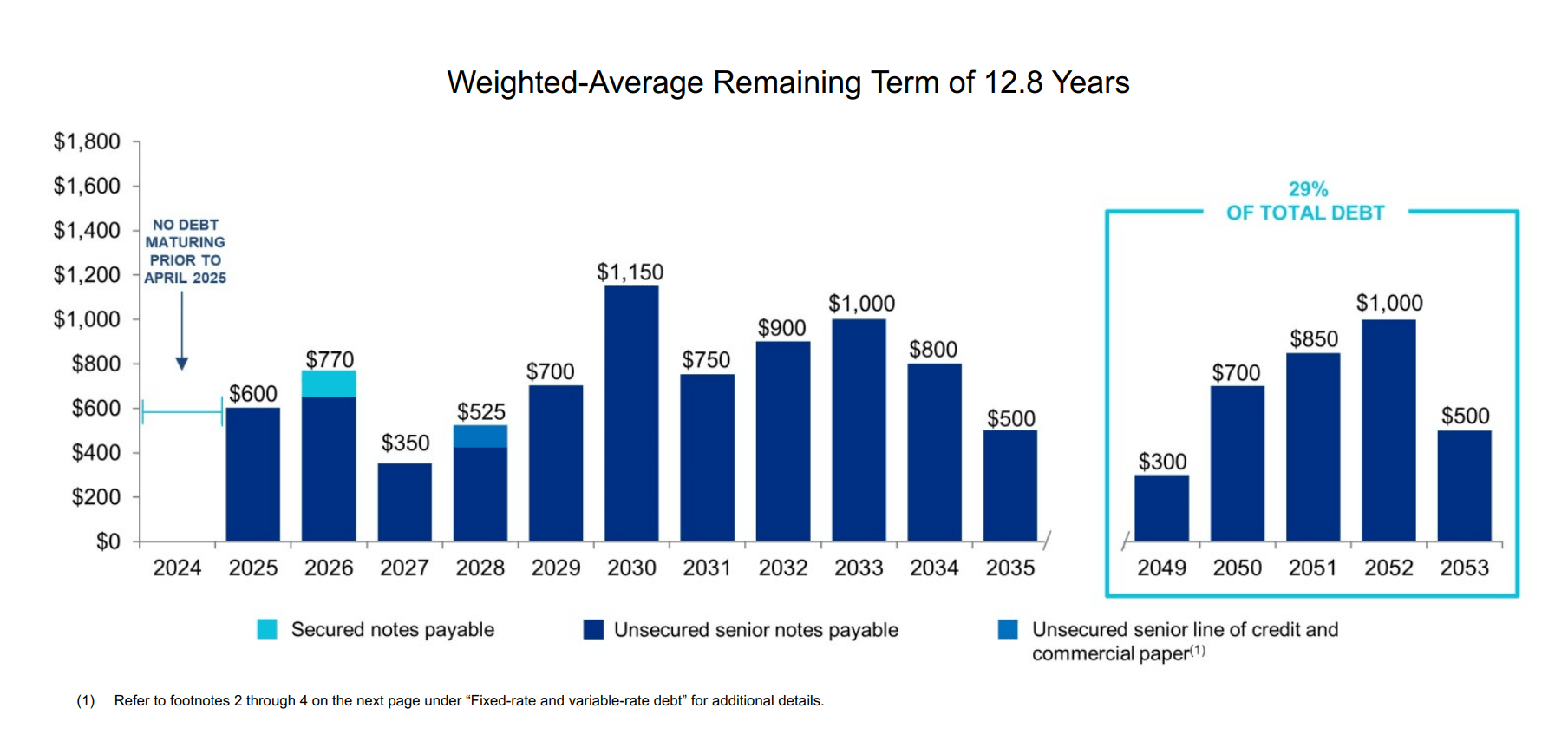

While NOI is likely to climb higher, the REIT’s interest expense is unlike to rise much, even if rates stay higher for longer. ARE has one of the longest duration balance sheets ion the sectors with an average term of 12.8 years. Moreover, there are no maturities before April 2025 and 98.1% of debt is fixed-rate. As a result, the REIT will not see its interest expense rise at all this year and even next year’s potential increase if the entire $600 Million of debt due gets refinanced at 6% (vs 3.6% today) would have a minuscule negative impact on NOI of 0.7%, well below any sort of build-in rent increase.

ARE IR

Valuation

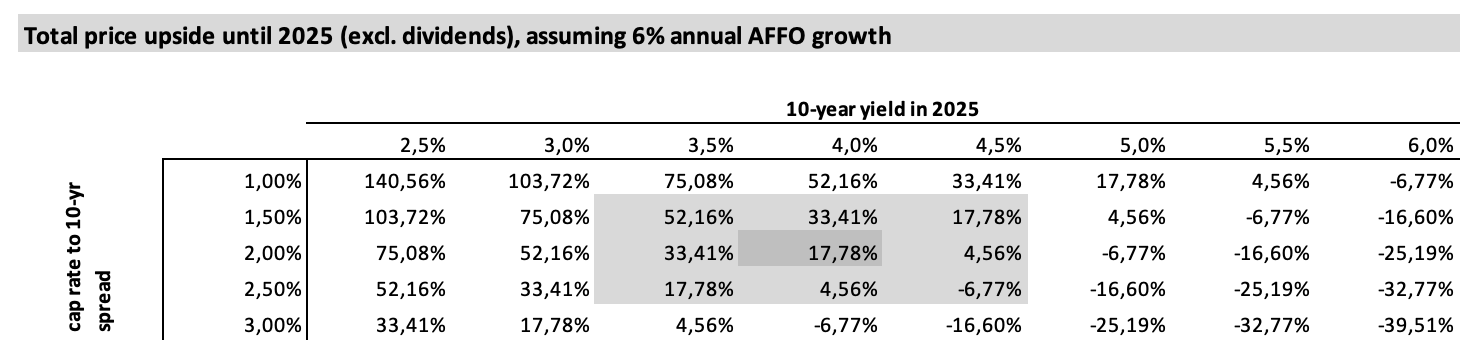

My expectation remains that ARE’s cash flow will steadily grow by 6-8% per year going forward. Moreover, I think that there are very few things that could put my forecast in jeopardy. The question is how much are we willing to pay for ARE’s (growing) stream of cash flows. With a relatively low 4.2% dividend yield, any rational investors has to expect some sort of price appreciation to make the investment worthwhile.

Annualizing Q4 number, ARE generates NOI of $1.9 Billion which translates into an implied cap rate of 6%. That’s a 180 bps spread to 10-year treasury yields of 4.2%. I’d argue that the spread is relatively fair, given ARE’s strong BBB+ rated balance sheet and a high portion (85%+) of investment grade tenants. Therefore, any sort of upside will have to come from either NOI/FFO per share growth or a fall in yields.

Assuming 6% annual growth, an unchanged spread of 180 bps to long-term yields and a decline in yields from 4.2% to 4%, ARE could return 18% in price appreciation over the next two years. That would give a price target of $140 per share and an annual RoR (with dividends) of 13%.

Author’s calculations

My personal base case is that yields may fall further, once the Fed starts cutting rates, which is why my price target stands at $170 per share which corresponds to yields at 3.5% and gives an annual RoR of 20%+. I rate ARE a BUY here at $120 per share.

Tradingview

The risk to this investment is that interest rates (and long-term yields) will climb higher from today’s levels. If, for example, yields return to 5%, then all growth will be offset by a lower valuation multiple and stock price will likely remain flat from today. Any increase above 5% would likely result in capital losses. But with interest rate expectations improving, I see the upside for ARE as quite likely, I just don’t know the exact time horizon.

Q2 2024 Earnings Call Transcript")