MarioGuti

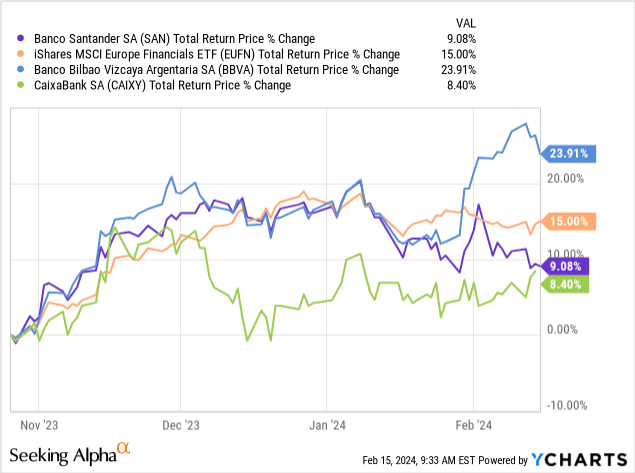

Shares of Banco Santander (NYSE:SAN) have underwhelmed since I last covered the Spanish multinational banking giant in October. The ADSs have delivered a circa 9% total return in that time, roughly matching domestic-oriented peer CaixaBank (OTCPK:CAIXY)(OTCPK:CIXPF) but trailing similarly Spanish/LatAm-focused BBVA (BBVA) as well as European financials (EUFN) more generally.

I have by-and-large been a firm supporter of Santander’s vast geographic diversity. Banks being banks, local regulations and ring-fencing mean that scale-related competitive advantages typically don’t apply. Instead, the main bullish argument is that Santander’s operating geographies are often at different points in the business cycle, ultimately acting to smooth overall group-level earnings and profitability metrics like return on tangible equity (“ROTE”).

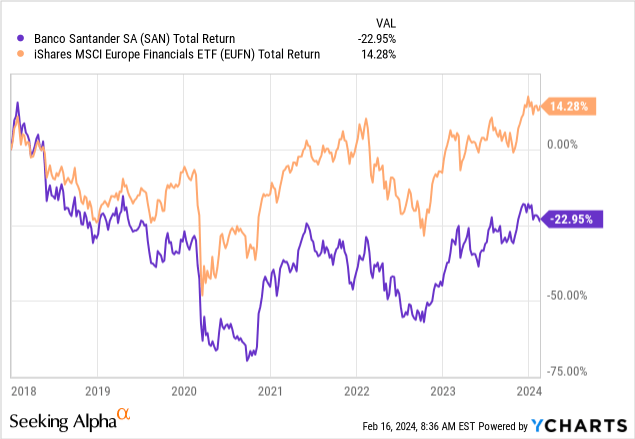

The above said, a bullish thesis is only as good as the results it delivers, and the fact is Santander has significantly underperformed over longer timeframes too, with the stock garnering a reputation as being something of a value trap as a result.

I think that is a touch harsh on the bank. While the above chart is definitely as poor as it looks, a simple total return figure can often mask the drivers of performance, and Santander looks a little better when returns are broken down into their constituent parts. With the bank already hitting 2025 profitability goals, I remain upbeat regarding the stock’s forward returns potential, and I keep my previous Buy rating in place.

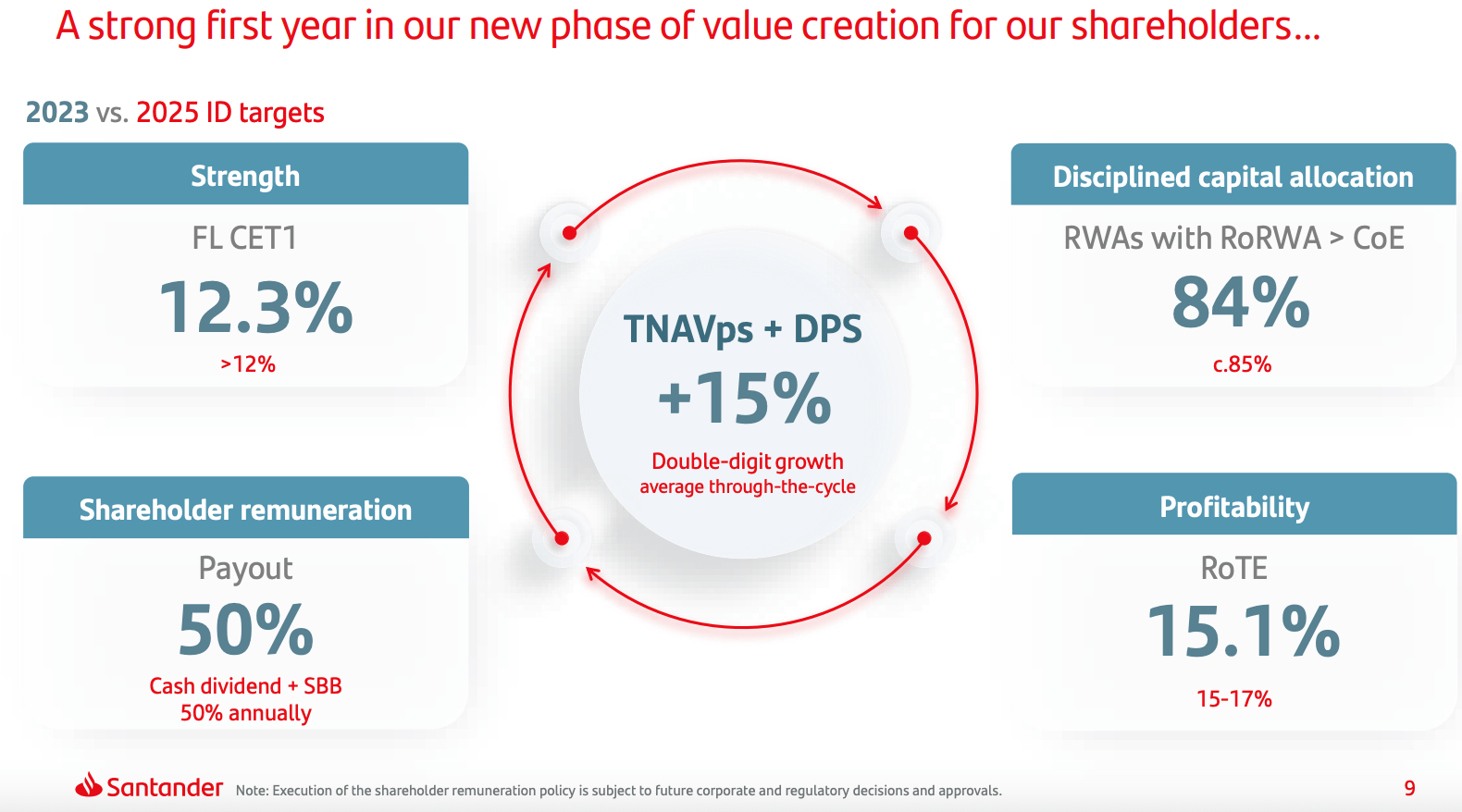

Profits Dip, But Guidance Looks Bullish

Santander reported record net income of €2.933 billion in Q4, up a touch quarter-on-quarter and mapping to a very respectable ~15.6% ROTE. That brought total 2023 net income to €11.1 billion, up from €9.6 billion in 2022, equating to an annual ROTE of 15.1%, ~170bps higher than 2022 and 10bps ahead of the low-end of management’s 15-17% 2025 target.

Source: Banco Santander 2023 Results Presentation

As strong as the Q4 print looks on paper, last quarter’s bottom-line and ROTE figures were flattered by tax-related tailwinds, with pre-tax numbers looking much more modest for the bank. With that, pre-tax profit of €3.922 billion dipped 12% quarter-on-quarter in Q4, driven by a modest top-line decline and negative jaws. Net interest income (“NII”) was €11.122 billion, down around 1% sequentially on Q3. Core European markets like Spain and the United Kingdom have expectedly seen their peaks in NII for this cycle, with weaker loan growth and higher funding costs leading to flat sequential NII in the former and a circa 8% QoQ decline in the latter.

With the above in mind, targets for 2024 look incredibly bullish, with management aiming for a circa 16% ROTE, driven in large part by top line growth, positive jaws and a relatively stable cost of credit still seen at the through-the-cycle average of ~120bps.

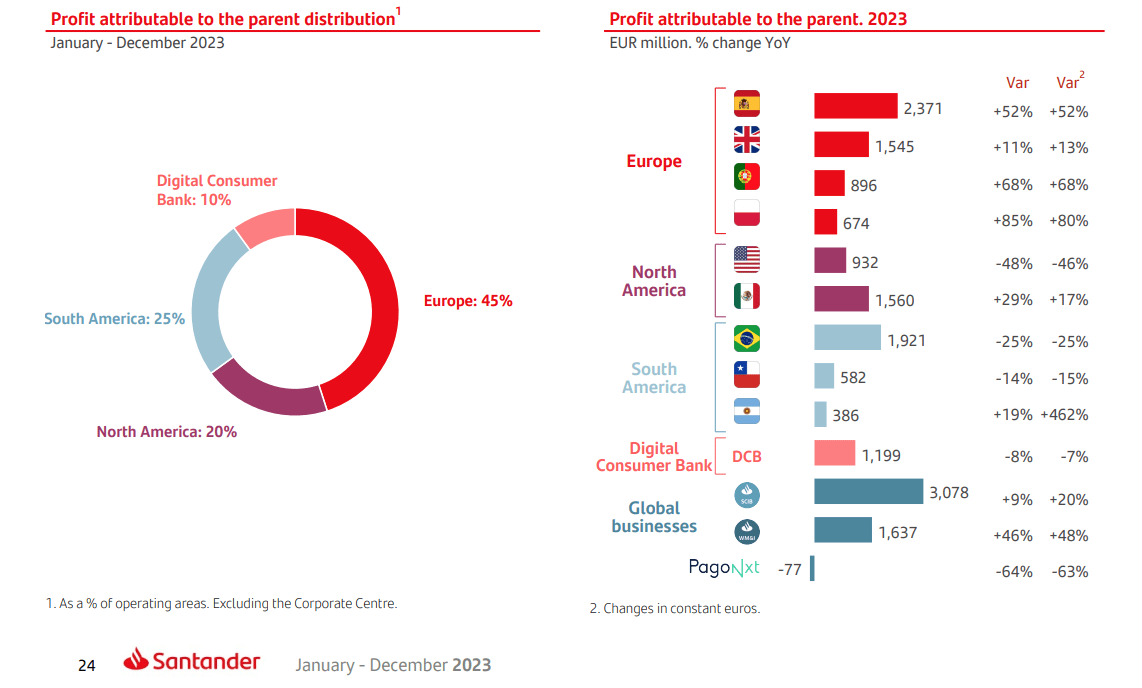

Management’s ROTE target looks aggressive to me, essentially implying around 9% net income growth this year, even though core European markets face tough comps. That said, geographic diversity will again be a factor in smoothing out earnings volatility this year. While markets like the United Kingdom (~9% of 2023 pre-provision operating profit) face a particularly hard comp, others like Brazil (~25%) are at a different stage of the cycle. There, the central bank has already put through 200bps of rate cuts from the peak as inflation has moderated to within its tolerance level.

Source: Banco Santander Q4 2023 Results Release

While Santander’s publicly-listed Brazilian business (BSBR) saw net income decline 25% last year on a combination of weak NII growth, cost inflation and higher provisioning for potential bad debt, there should be a reversal there this year, with Santander and Brazilian peers like Banco Bradesco (BBD) and recently-covered Banco do Brasil (OTCPK:BDORY) all guiding for lower provisioning expenses in 2024.

Shares Remain Materially Undervalued

Santander’s ADSs trade for $3.94 at the time of writing, putting them at 5.6x 2023 EPS and around 0.75x year-end 2023 tangible book value per share (“TBVPS”), broadly unchanged from previous coverage.

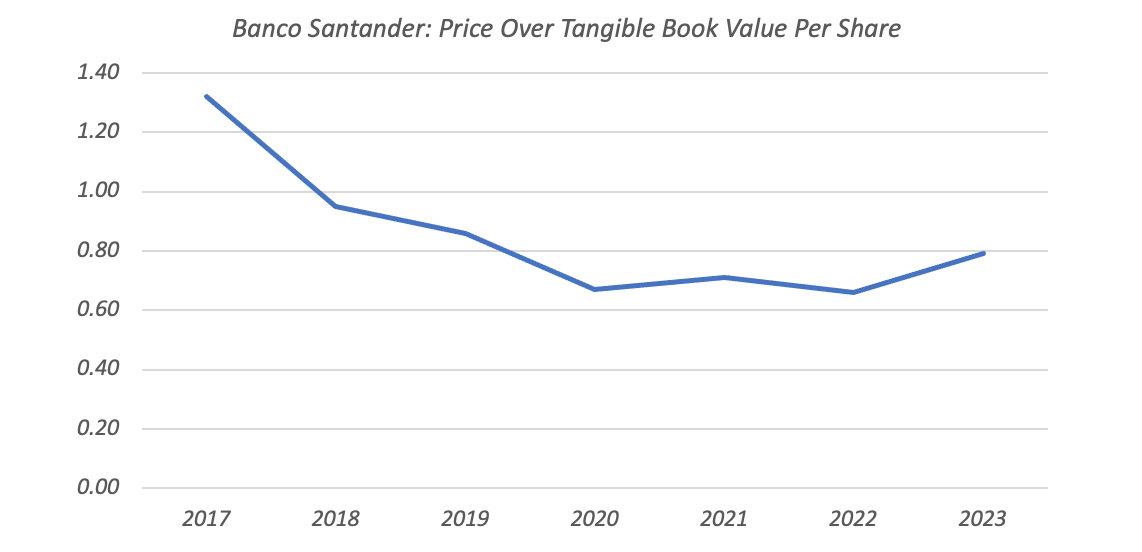

The valuation here continues to look much too cheap. I said in the introduction that Santander’s history of underperformance was not quite the picture it appeared to be. To expand on that a little, stock returns can broadly be broken down into three components: per-share growth, cash returns from dividends and changes to the valuation multiple. For a bank stock, we could define this as TBVPS growth, plus dividends, plus any changes to the price-to-TBVPS multiple. While TBVPS growth plus dividends hasn’t been spectacular here, Santander’s underperformance has largely been a result of a contracting P/TBVPS multiple, which has fallen from over 1.3x in 2017 to 0.75x currently.

Data Source: Banco Santander Results Releases

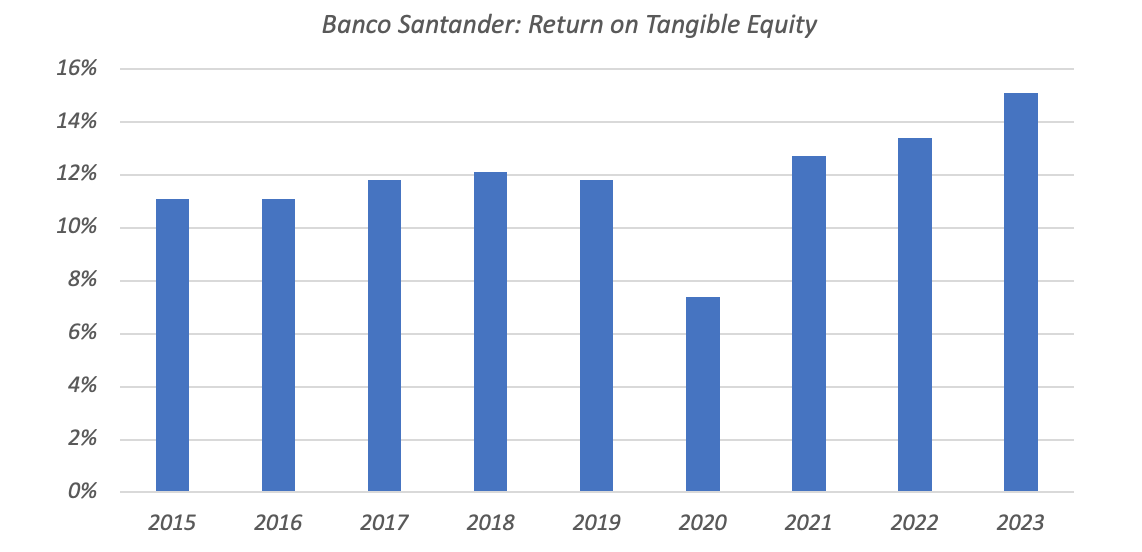

With that, Santander is a much better bank than its total returns performance suggests. ROTE has averaged around 12% over the past decade or so, and due to aspects of its business model which I have already mentioned, earnings volatility is typically lower.

Data Source: Banco Santander Results Releases

One key point for investors to appreciate going forward is the potential structural improvement in the bank’s profitability due to higher interest rates in Europe. While the forward curve is implying around 140bps in cuts this year in the Eurozone, remember that for much of Santander’s recent history interest rates there were actually zero-to-negative. Even rates in the 2% region would present a material step-up in profitability for the bank’s operations there. So, while management’s 2024 ROTE target looks bold, there is still scope for improvement vis-à-vis the recent historic average.

I expect the above to result in a gradual re-rating of the bank’s TBVPS multiple over time. If Santander can average a ROTE of around 13% across the cycle, that should be good for a multiple of around 1.1x-1.2x TBVPS, ultimately driving around 50% upside to a fair value of ~$5.90 per ADS.

Capital returns potential is reasonable in the meantime, with management’s shareholder remuneration policy set at a circa 50% payout ratio, split evenly between dividends and buybacks. Call it a 10% shareholder yield based on current earnings, which is okay, though less attractive than certain other European banks I have covered recently like ING (ING) and UniCredit (OTCPK:UNCRY)(OTCPK:UNCFF). While not the best capital returns play in the European banking space, the overall value case at Santander nonetheless remains compelling, and I keep my Buy rating in place.

Q2 2024 Earnings Call Transcript")