bjdlzx

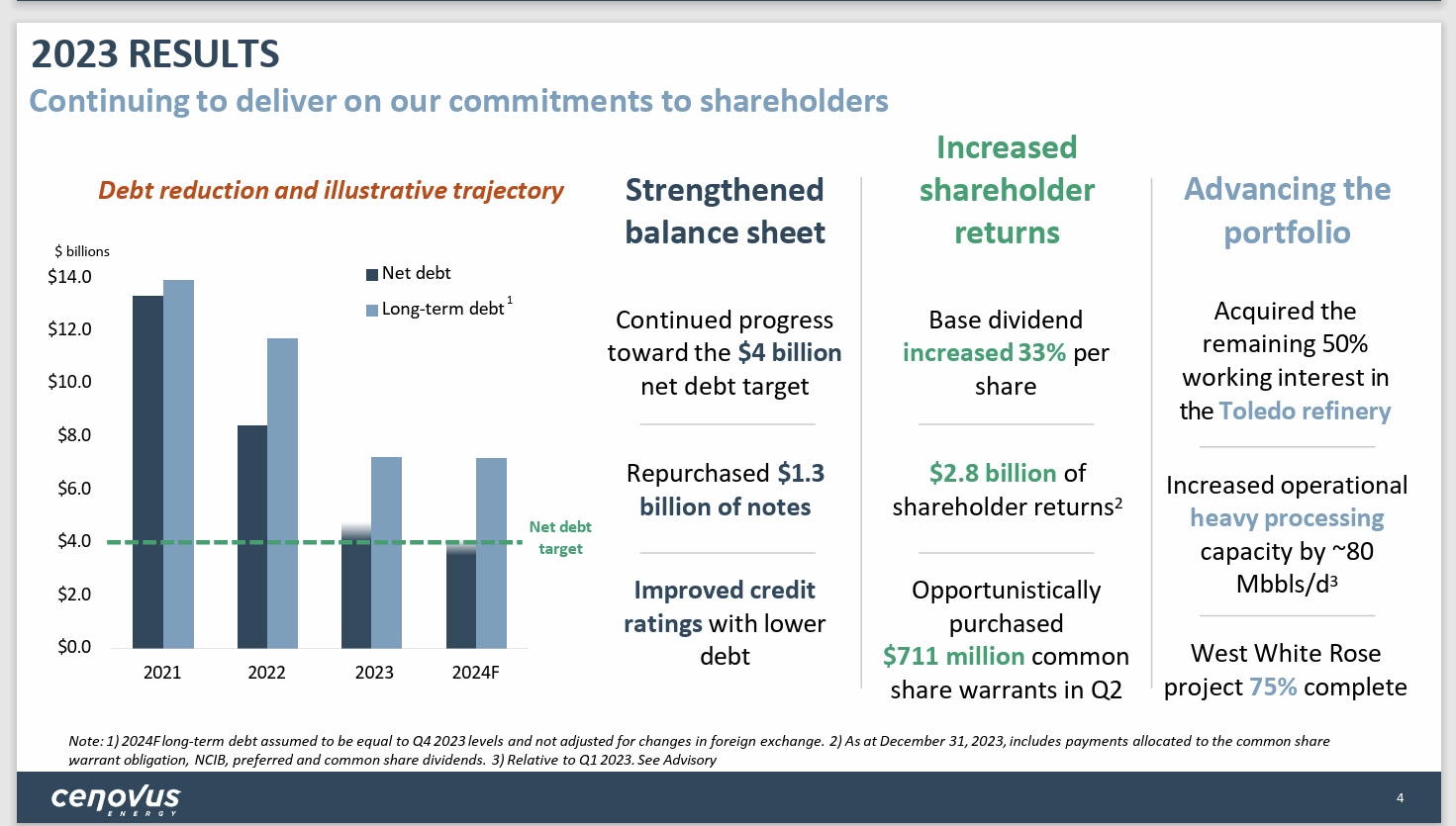

Cenovus Energy Inc. (NYSE:CVE) just announced that they reduced debt by more than C$900 million. At the current pace of debt retirements, management should achieve net debt of C$4 billion early in the second quarter. Even if they reduce net debt in the future by half that pace, the amount of free cash flow available to shareholders will go from 50% to 100% within the next fiscal year. At least some of that will go to more dividends in the future. That “some more” could amount to a rather generous yield on a stock where management intends to grow the business (and likely the dividend as well) still more.

The Latest Q4 Results

Thermal producers tend to cash flow generously even when they are losing money. A well-run integrated thermal producer can cash flow with a little less exposure to the cyclical upside business. This provides unusual dividend protection for an upstream (and in this case, a diversified upstream player with considerable downstream ability).

(Note: This is a Canadian Producer That Reports In Canadian Dollars Unless Otherwise Noted)

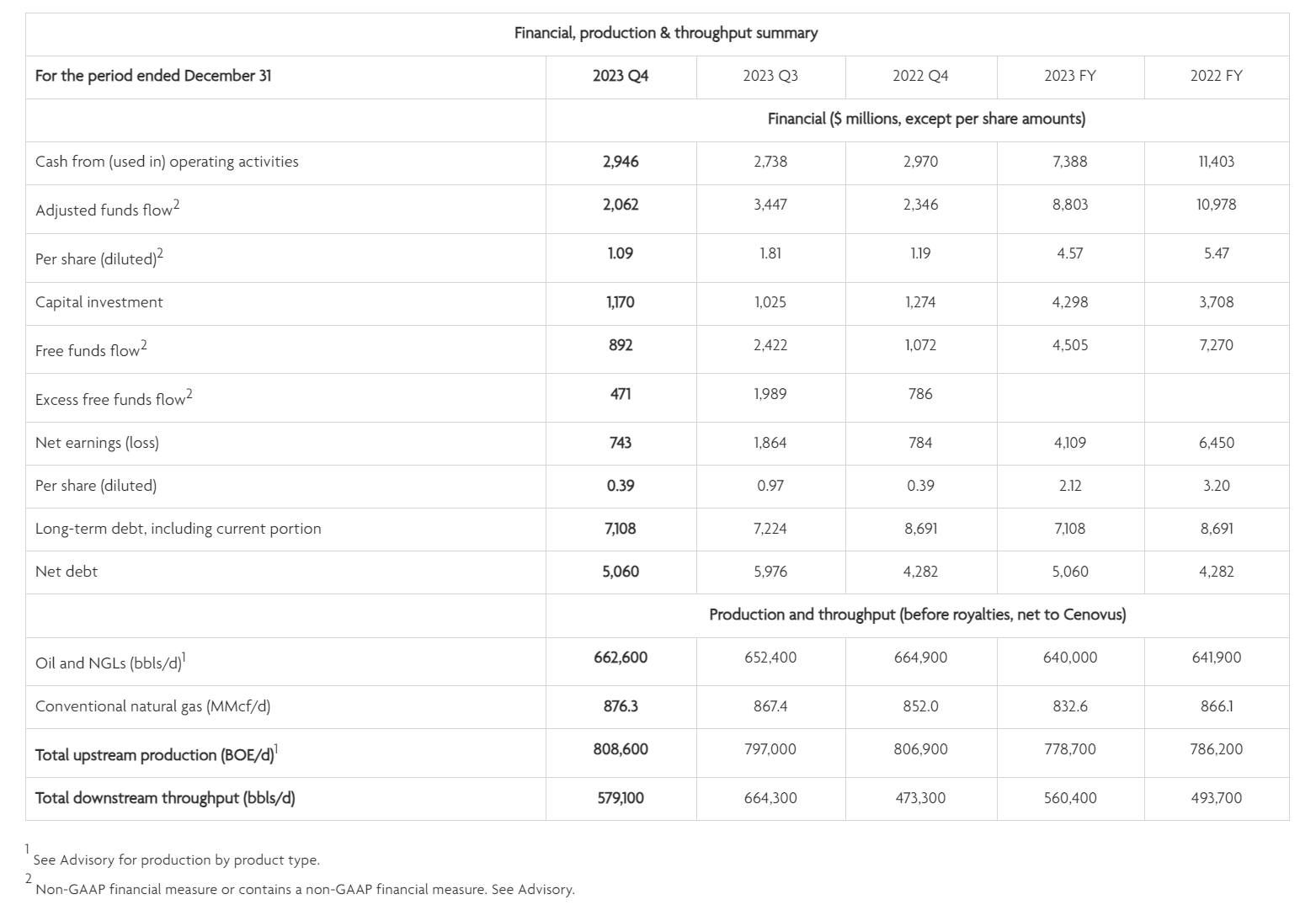

Cenovus Energy Summary Of Fourth Quarter and Fiscal Year Results (Cenovus Energy Fourth Quarter 2023, Earnings Conference Call Slides)

The net debt goal is C$4 billion. Last year the acquisition of an interest in the Toledo refinery, combined with the startup of the Superior Refinery, and the acquisition of the Sunrise interest, all combined to delay the free cash flow percentage increase. Right now, there is nothing in the future that would prevent the continuing repayment to the C $4 billion goal.

Cenovus Energy Debt Progress As Of Yearend 2023 (Cenovus Energy Fourth Quarter 2023, Earnings Conference Call Slides)

It is probably very reasonable to expect a future dividend increase sooner rather than later given the historical pace of repaying debt. The refining abilities of the company mostly insulate a lot of production from any widening of the thermal oil pricing discount. Now, as long as there is not a major reason to increase the debt load as there was last year, investors could end up being very happy about the returns in the current fiscal year.

As the integration process continues and management continues to optimize the acquisitions made in the last few years, there is likely to be more cash flow at various pricing points in the future.

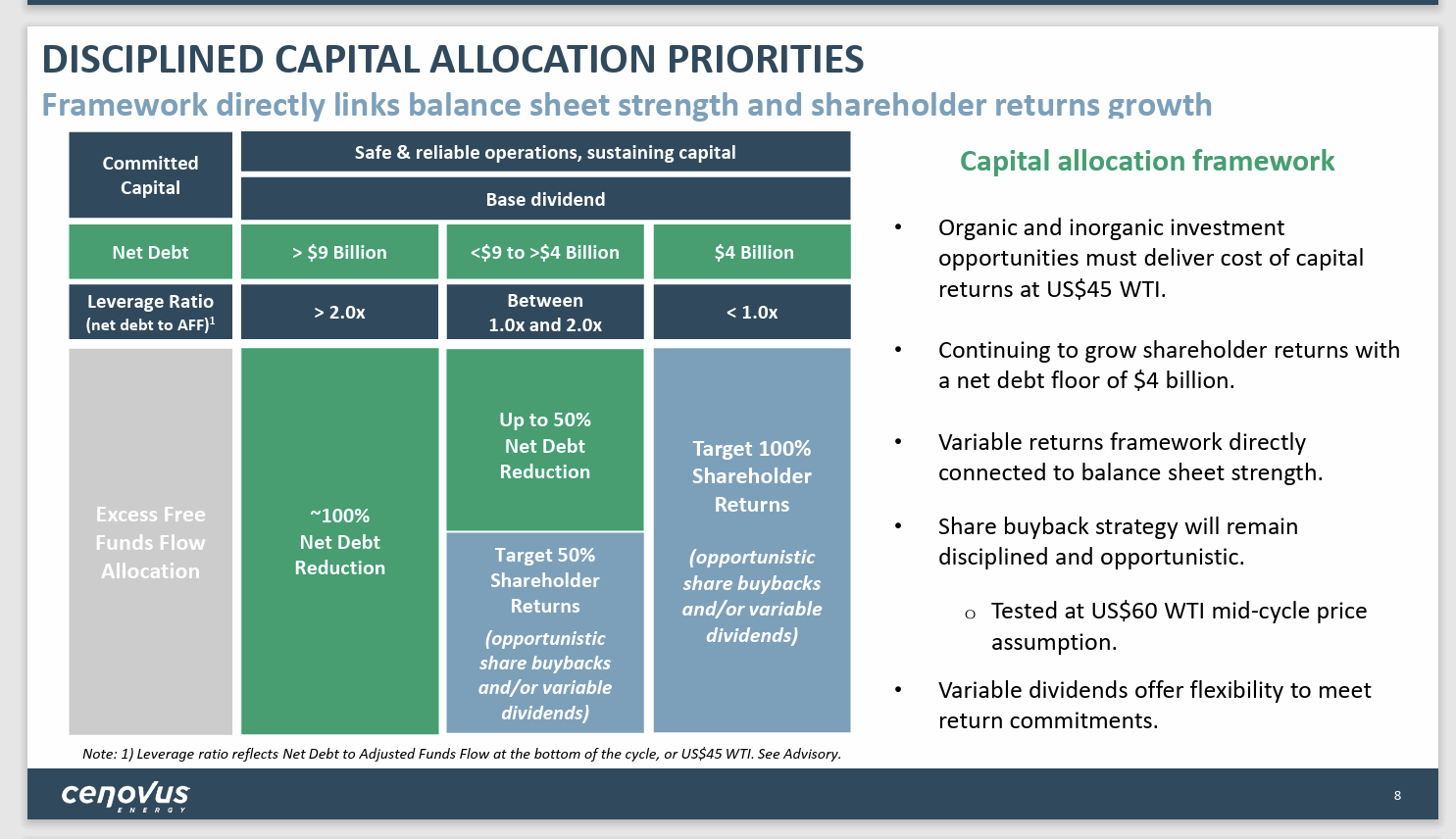

Cenovus Energy Management Framework About Shareholder Returns (Cenovus Energy Earnings Conference Call Slides Fourth Quarter 2023)

Once the net debt reaches C$4 billion, then the free cash flow available to shareholders will double. That should allow for a significant increase in the dividends. Any share repurchases means that the same cash flow is available to fewer shares in the future. That would make more room for more dividend increases.

The nice part about this is the oil and gas sector is largely out of favor. Many times, when this happens, that growing dividend soon becomes a decent return on the original investment. The investment itself is likely to appreciate as this sector returns to favor.

Management does want to establish a base dividend that can be maintained at WTI $45. That varies from a lot of upstream producers that do not hesitate to cut dividends during any cyclical downturn.

Right now, the industry consolidation that is going on tends to protect against the massive overproduction that often marks a market top. While commodity prices are often volatile, there does not appear to be a cyclical downturn in the near future that would bring commodity prices anywhere close to WTI $45 in the near future.

However, this is a low visibility industry. So, there can always be a surprise that no one saw coming. Even with that consideration, right now, it looks more like we are at the beginning of a cycle with more growth and good years ahead rather than a cyclical peak where losses and shut-in production would be the rule.

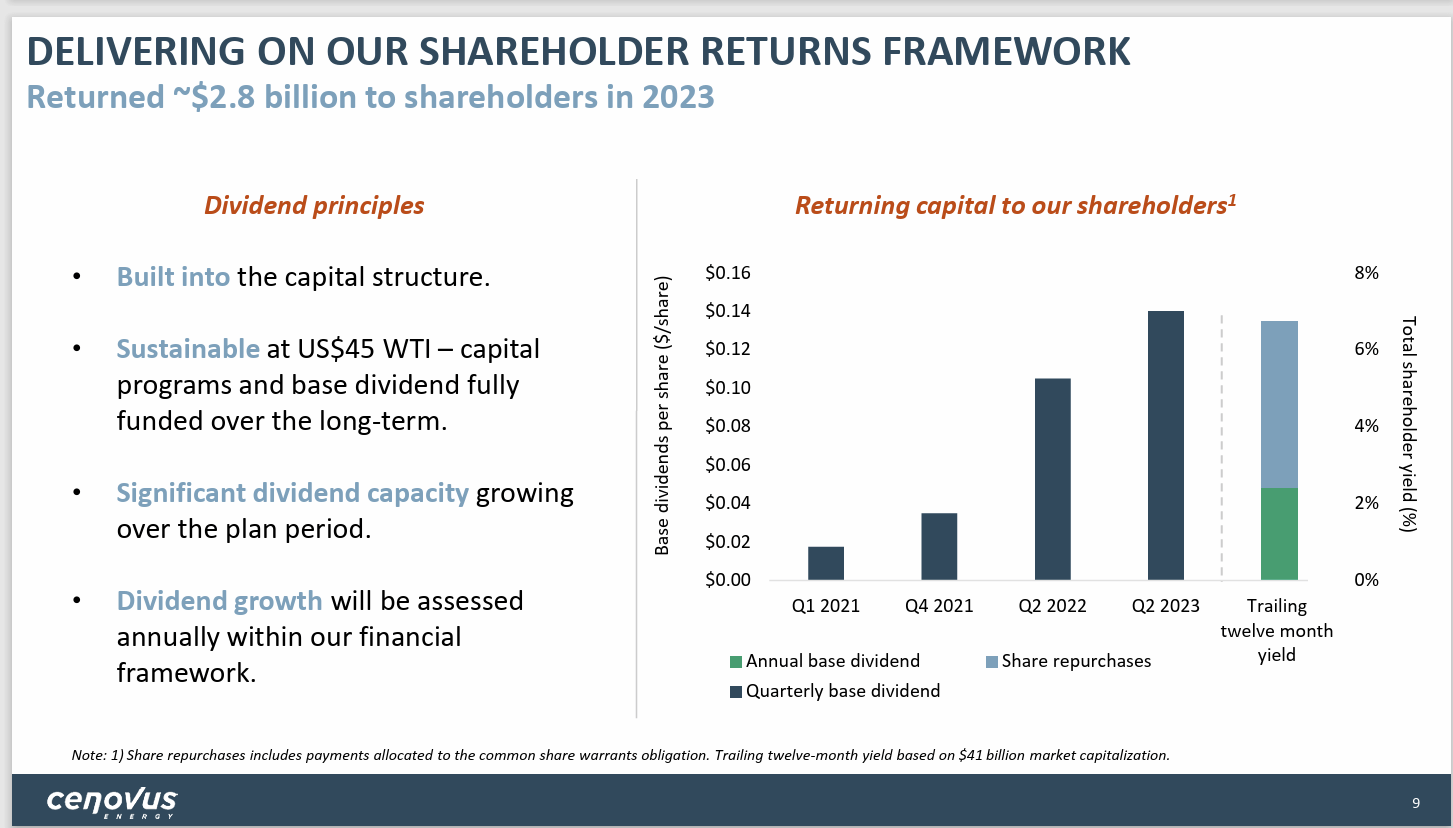

Cenovus Energy Percentage Per Share Spent On Dividends And Stock Repurchases (Cenovus Energy Earnings Conference Call Slides Fourth Quarter 2023)

As shown above, the current yield is in the two percent range. An immediate base rate increase when the C$4 billion net debt level target is achieved would raise the base dividend to at least 4%. Share repurchases would assure future increases to raise the yield on the original investment more.

Management lists some growth projects as well. Any growth would aid dividend increases in the future. A company this size typically grows in the single digit range. Some optimization projects for the recent acquisitions could raise that progress to the high single digits for a few years.

The combined return for the dividend plus the growth of the business should yield a long-term return in the teens. The benefit of owning the refining is that the company is not exposed to widening price discounts for its thermal products. Therefore, the cyclical swing is less (although still significant).

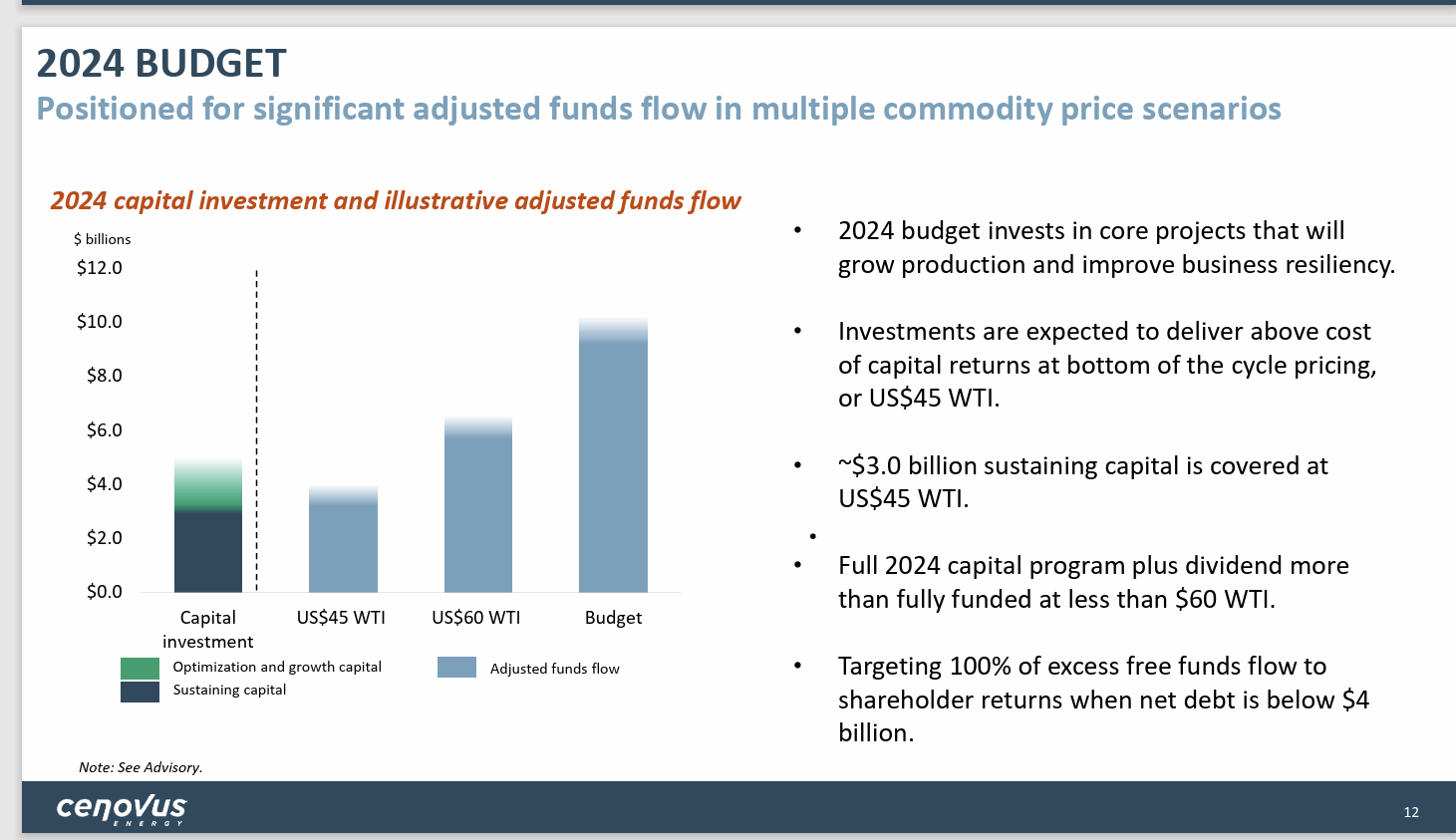

Cenovus Energy Free Cash Flow Forecast At Various Commodity Price Levels (Cenovus Energy Earnings Conference Call Slides Fourth Quarter 2023)

Given that management is using a WTI price (CL1:COM) in the $70 range, it looks like it will take management at most two quarters to achieve the net $4 billion goal. Most likely the first quarter will make substantial progress towards the net debt goal and the second quarter will finish cleaning up what is left.

Summary

Cenovus has some of the lowest cost thermal projects in the business. That alone can make for a very profitable operation now that the company has the refining ability to upgrade much of the production.

But management is now improving the benefits of the upstream and downstream diversification of the company. That should promise profit increases in excess of sales growth for a few years.

The recent integration of the refining capacity is new enough that the market really does not value the integration yet. However, that will likely change as management optimizes the combined operations.

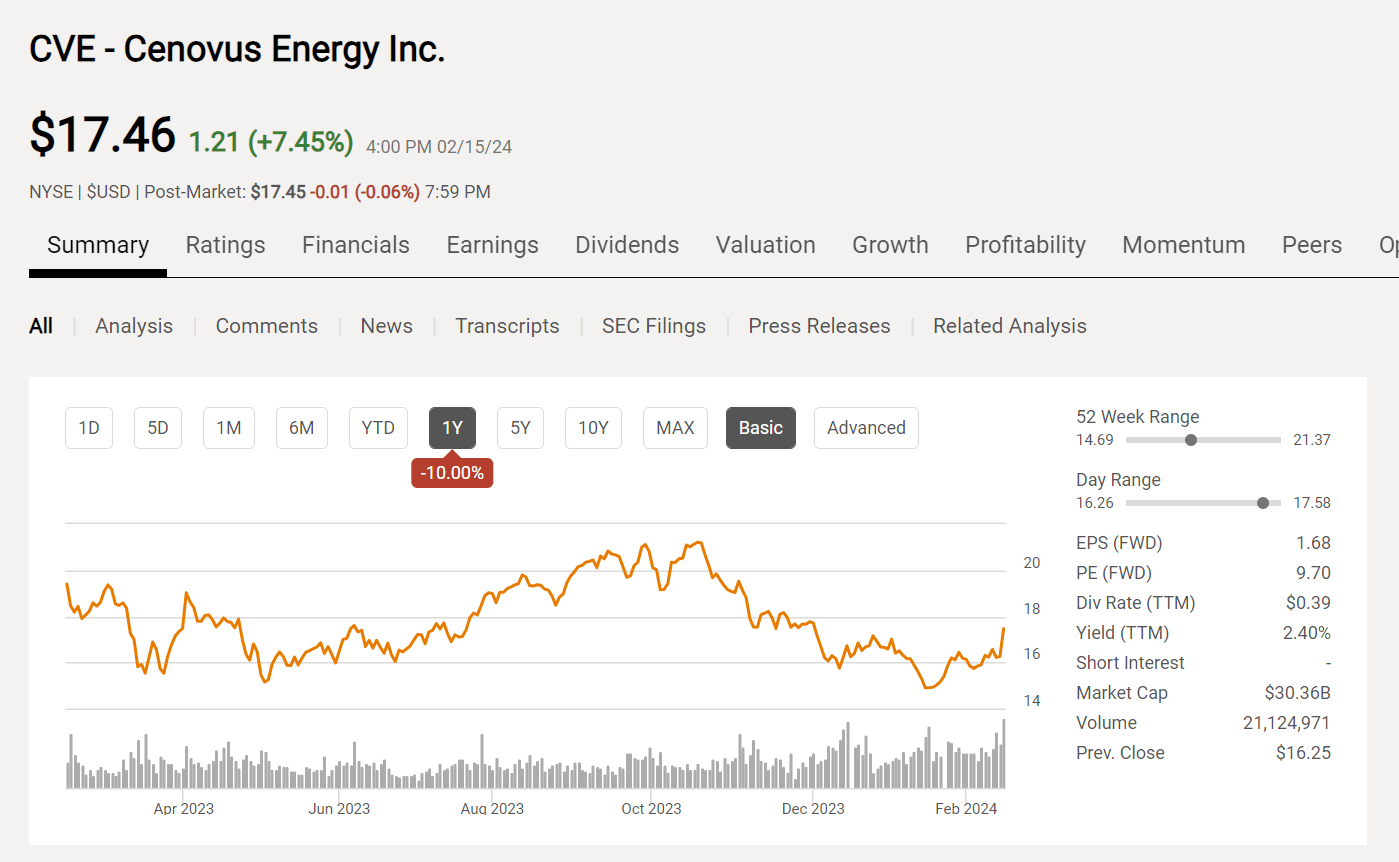

Cenovus Energy Common Stock Price History And Key Valuation Measures (Seeking Alpha Website February 15, 2024)

The common stock has yet to be valued anything close to the typical integrated major. That should change as the company acquires a reporting track record as a large integrated company. This would provide additional returns for the investor.

Most of the “majors” have a price earnings ratio in the teens. The stock is likely undervalued by at least 30% as a result. The interesting thing is that this company has thermal operations that are more profitable than many larger integrated companies.

There is plenty here for many kinds of investors both in terms of a dividend increase, the undervaluation, and the growth ahead. That makes Cenovus Energy Inc. still a strong buy for most investors. The investment grade rating of the debt will appeal to even risk-averse investors. Shares can be volatile at times because commodity prices are volatile. Therefore, a basket of well-chosen stocks put together over time should treat an investor well.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")