Tim Boyle

Summary

Shares of Topgolf Callaway Brands Corp. (NYSE:MODG) are down more than 50% since its all-time highs set in 2021. The widely known golf company reported better than expected revenue this week, sending shares higher. Despite this, Wall Street is still skeptical on the longer-term plans with Topgolf Management’s expansion plans have been expensive and unsurprisingly have impacted bottom-line earnings and short-term valuations. However, I think the sell-off over the past few years could be overdone for a few reasons, especially when looking at competitors. Some keynotes:

- MODG’s EV/EBITDA multiple is now considerably below its direct peer, Acushnet Holdings (NYSE: GOLF).

- Many attribute MODG’s share price decline to increased debt levels, lower profit margins, and growth concerns.

- The golf industry has historically held up well during recessions.

Ultimately, I believe a pairs trade between MODG and GOLF could present an interesting short-term opportunity. Long MODG, short GOLF.

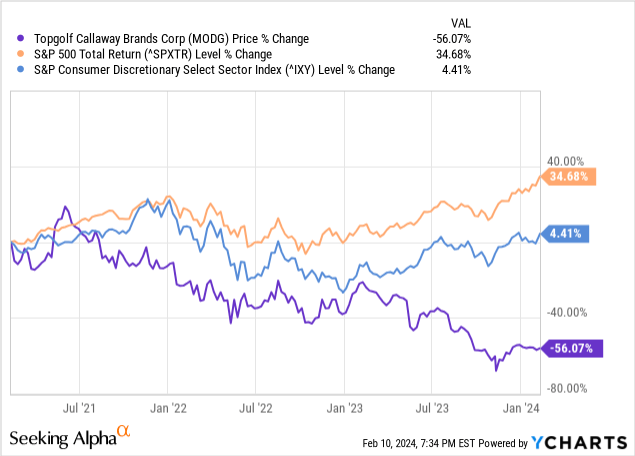

MODG has underperformed a lot since COVID. It has lagged the broader S&P 500 and even its own sector by a wide margin, as seen below:

3-Year Performance For MODG Has Lagged S&P 500 and Consumer Discretionary Indexes

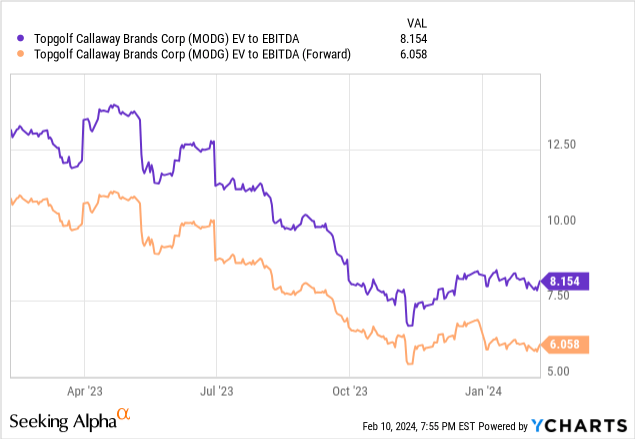

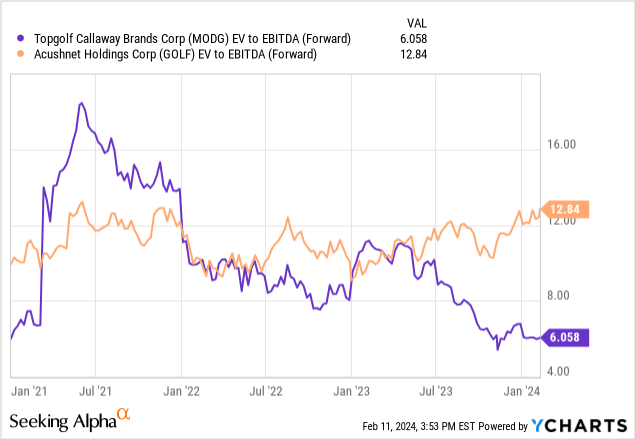

This share price decline has impacted its enterprise value, leading to a much lower trailing and forward EV/EBITDA multiple. MODG now trades only 6x its forward EV/EBITDA.

MODG EV/EBITDA Multiple Has Trended Lower In 2023

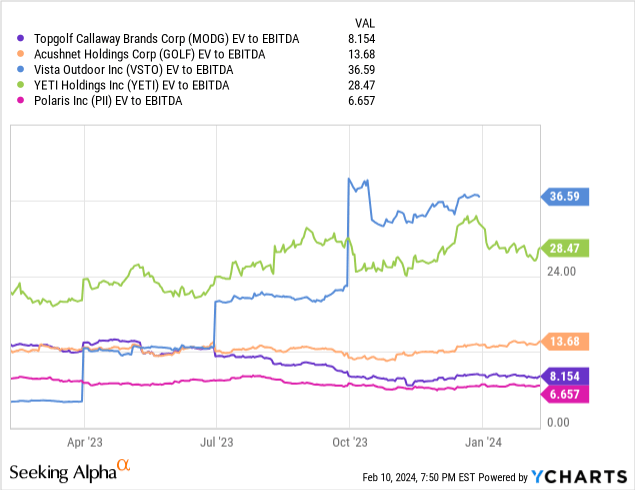

While MODG has seen its EV/EBITDA multiple decline considerably over the past year, its competitor Acushnet Holdings (GOLF) has remained relatively flat around 13x. In my opinion, a forward EV/EBITDA multiple of 6x is low considering MODG is heavily focused on growth right now. If the company were to slow down its expansion of Topgolf across the U.S., margins would likely improve as the company could use its free cash flow to reduce debt.

EV/EBITDA Comparison For Leisure Stocks With Similar Market Caps

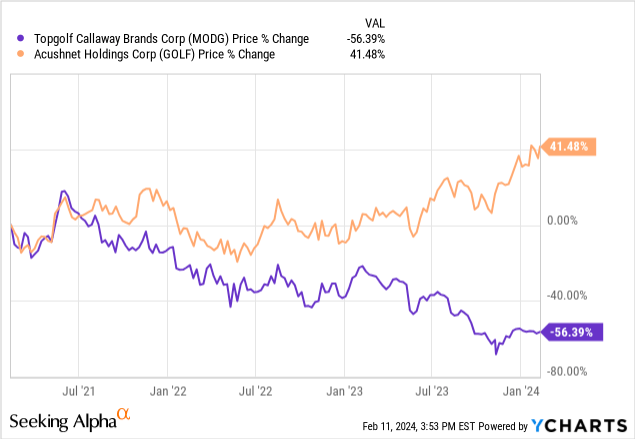

While companies such as VSTO, YETI, and PII are not necessarily direct comparables, it’s still helpful to see the differences across the leisure industry. Ultimately, GOLF and MODG are likely to be considered the closest comparisons, although even then it can be questionable with MODG’s Topgolf business. As you can see below, performance has been drastically different over the last few years:

GOLF’s share price appreciation has helped bolster its high EV/EBITDA multiple compared to MODG:

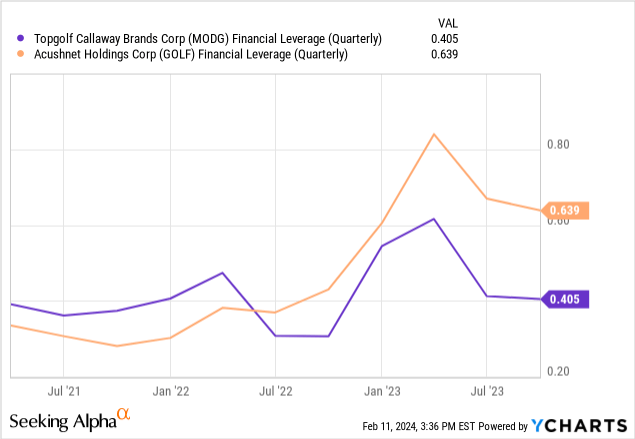

While some may point to MODG’s recent debt increase, leverage is still not necessarily the reason, as seen below. MODG has lower leverage than GOLF.

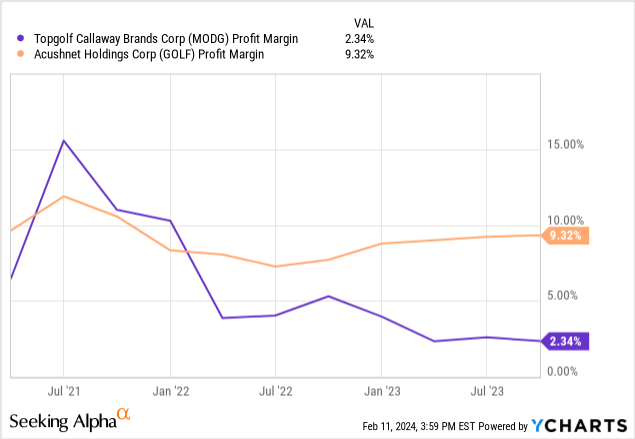

The biggest driver of EV/EBITDA multiple decline, in my view, is MODG’s decline in net profit margin from over 10% to 2% over the past two years. GOLF has maintained its net profit margin of around 10% during this time. MODG’s rapid increase in debt has played a role in impacting margins, but is likely a near-term headwind in my view. Longer-term, once the expansion of Topgolf facilities has been completed, margins should improve.

The Golf Industry Has Historically Held Up During Recessions

While the market-implied odds of a recession in the United States have somewhat declined recently, it’s still well above historical averages. Many still believe a technical recession could occur in 2024 based on the 10-year / 3-month yield curve inversion:

Federal Reserve Bank of New York

As mentioned in MODG’s investor presentation below, the golf industry has surprisingly done pretty well during economic downturns. If history is any indicator, MODG should not see any slowdown in demand due to a recession.

Investor Presentation

Risks To Consider

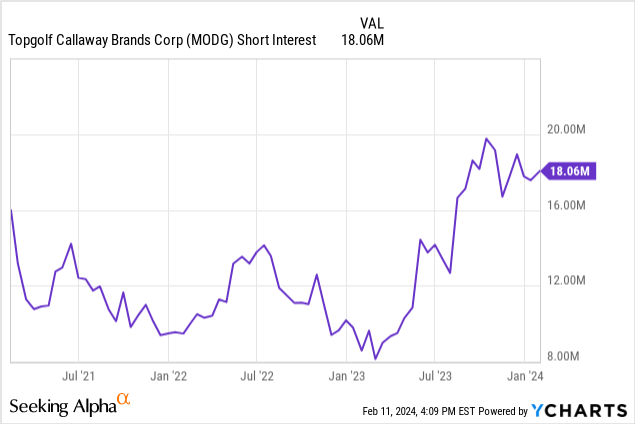

MODG currently has negative market sentiment, as evidenced by the high short interest over 18mm shares or roughly 10% of the equity float. High short interest often reflects a pessimistic outlook among investors, indicating that many believe the stock’s value will decline. This negative sentiment can create a self-fulfilling prophecy as more investors may be discouraged from buying, further pressuring the stock.

It may also signal that investors lack confidence in the company’s fundamentals or management’s ability to deliver positive results. This can make it challenging for the company to attract new investors or secure financing, potentially hindering its growth prospects.

Conclusion

MODG is not a perfect company by any means. The company is trying to rapidly expand in a very upfront cost-intensive business (Topgolf) which requires a lot of debt and impacts profits in the near-term. In my opinion, management may be trying to grow too fast and, as a result, has become unfavorable on Wall Street. Despite this, I do think the dispersion that has occurred between MODG and GOLF presents an interesting short-term (less than 1 year) opportunity as a pair trade.

Q2 2024 Earnings Call Transcript")